Global Acute Coronary Syndrome Market

Размер рынка в млрд долларов США

CAGR :

%

USD

13.77 Billion

USD

20.65 Billion

2025

2033

USD

13.77 Billion

USD

20.65 Billion

2025

2033

| 2026 –2033 | |

| USD 13.77 Billion | |

| USD 20.65 Billion | |

| % | |

|

Global Acute Coronary Syndrome Market Segmentation, By Type (Non-St-Elevation Myocardial Infarction, St-Elevation Myocardial Infarction, and Unstable Angina), Diagnosis (Stress Test, Blood Tests, Imaging and Others), Treatment (Medication and Surgery), End User (Hospitals and Clinics, Diagnostic Centers, Academic Institutes and Others) - Industry Trends and Forecast to 2033

Acute Coronary Syndrome Market Size

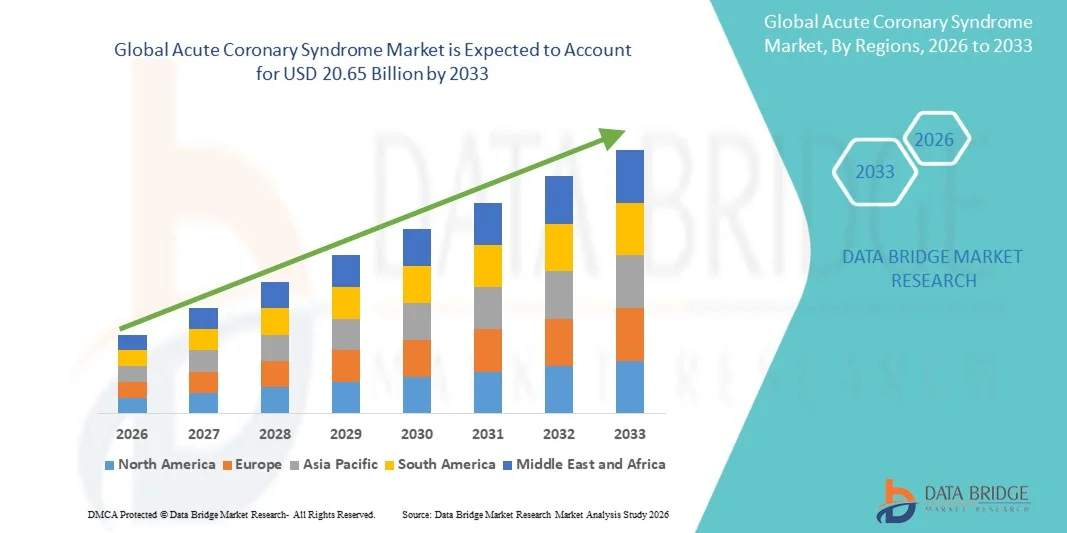

- The global acute coronary syndrome market size was valued at USD 13.77 billion in 2025 and is expected to reach USD 20.65 billion by 2033, at a CAGR of 5.20% during the forecast period

- The market growth is largely driven by the increasing prevalence of cardiovascular diseases, rising awareness about early diagnosis, and advancements in treatment options for acute coronary syndrome. Moreover, technological innovations in diagnostic tools, minimally invasive procedures, and novel therapeutics are enabling better patient outcomes, thereby accelerating the adoption of ACS solutions across hospitals and clinics

- Furthermore, growing patient demand for rapid, accurate, and cost-effective interventions is positioning advanced ACS therapies as the preferred choice for healthcare providers, collectively contributing to significant growth in the acute coronary syndrome market

Acute Coronary Syndrome Market Analysis

- The Acute Coronary Syndrome market is witnessing significant growth due to the rising global burden of cardiovascular diseases, increasing awareness regarding early diagnosis, and continuous advancements in diagnostic and treatment technologies. Enhanced clinical protocols and improved access to healthcare services are further supporting the adoption of ACS management solutions across hospitals and cardiac care centers

- The market growth is primarily driven by the increasing demand for rapid, accurate, and cost-effective treatment options, along with the growing use of advanced pharmacological therapies and minimally invasive procedures. In addition, ongoing innovations in drug development and interventional cardiology are contributing to improved patient outcomes and fueling market expansion

- North America dominated the acute coronary syndrome market with a revenue share of approximately 40.5% in 2025, supported by well-established healthcare infrastructure, high healthcare expenditure, and strong adoption of advanced treatment solutions. The United States leads the region due to the high prevalence of cardiovascular conditions and the presence of major market players

- Asia-Pacific is expected to be the fastest-growing region in the acute coronary syndrome market during the forecast period, driven by rapid urbanization, increasing disposable incomes, improving healthcare infrastructure, and a rising incidence of lifestyle-related cardiac disorders in emerging economies such as China and India

- The medication segment dominated the largest market revenue share of 53.6% in 2025, driven by the widespread use of antiplatelet agents, anticoagulants, beta-blockers, and statins in the initial management of ACS

Report Scope and Acute Coronary Syndrome Market Segmentation

|

Attributes |

Acute Coronary Syndrome Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Pfizer Inc. (U.S.) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Acute Coronary Syndrome Market Trends

“Advancements in Diagnostic Technologies and Early Detection Approaches”

- A significant and accelerating trend in the global acute coronary syndrome market is the growing adoption of advanced diagnostic technologies aimed at early and accurate detection of cardiac events

- For instance, the increasing use of high-sensitivity cardiac troponin assays is enabling clinicians to detect myocardial infarction at earlier stages with improved precision

- These diagnostic advancements help in rapid risk stratification of patients presenting with chest pain, thereby improving clinical decision-making and treatment outcomes

- Furthermore, the integration of point-of-care testing and rapid diagnostic kits in emergency settings is enhancing the speed and efficiency of diagnosis

- The growing emphasis on early diagnosis and timely intervention is significantly reducing mortality rates and hospital stays associated with Acute Coronary Syndrome

- This trend is further supported by continuous research and development activities focused on improving biomarker accuracy and diagnostic reliability

- Consequently, the demand for advanced diagnostic solutions in the Acute Coronary Syndrome market is increasing across hospitals and emergency care settings

Acute Coronary Syndrome Market Dynamics

Driver

“Rising Prevalence of Cardiovascular Diseases and Increasing Geriatric Population”

- The increasing prevalence of cardiovascular diseases worldwide is a major driver for the Acute Coronary Syndrome market

- For instance, lifestyle changes, unhealthy dietary habits, rising obesity rates, and lack of physical activity have significantly contributed to the growing incidence of heart-related conditions

- In addition, the rapidly expanding geriatric population, which is more susceptible to cardiac disorders, is further accelerating the demand for Acute Coronary Syndrome diagnosis and treatment solutions

- Improvements in healthcare infrastructure and increasing awareness regarding early diagnosis are also encouraging patients to seek timely medical attention

- Moreover, government initiatives and healthcare programs focused on reducing cardiovascular mortality are supporting market growth

- The availability of advanced treatment options such as antiplatelet therapies, anticoagulants, and interventional procedures is further enhancing patient outcomes

- These combined factors are significantly contributing to the expansion of the Acute Coronary Syndrome market

Restraint/Challenge

“High Treatment Costs and Limited Access to Advanced Healthcare Facilities”

- One of the major challenges in the Acute Coronary Syndrome market is the high cost associated with diagnosis, hospitalization, and treatment procedures

- Advanced diagnostic tests and interventional treatments such as angioplasty and bypass surgery can be expensive, limiting accessibility for patients in low- and middle-income regions

- For instance, In addition, inadequate healthcare infrastructure and limited availability of specialized cardiac care centers in rural areas further restrict timely diagnosis and treatment

- Delays in diagnosis and treatment can lead to severe complications, increasing mortality rates associated with Acute Coronary Syndrome

- Furthermore, lack of awareness regarding early symptoms among the general population also contributes to late hospital admissions

- Stringent regulatory requirements and the need for highly skilled healthcare professionals can also pose challenges to market growth

- Addressing these issues through cost-effective solutions, improved healthcare access, and awareness programs will be crucial for sustained market development

Acute Coronary Syndrome Market Scope

The market is segmented on the basis of type, diagnosis, treatment, and end user.

• By Type

On the basis of type, the Acute Coronary Syndrome market is segmented into Non-ST-Elevation Myocardial Infarction (NSTEMI), ST-Elevation Myocardial Infarction (STEMI), and Unstable Angina. The NSTEMI segment dominated the largest market revenue share of 46.3% in 2025, driven by its higher incidence rate compared to other ACS types and its strong association with aging populations and lifestyle-related risk factors such as diabetes and hypertension. Clinically, NSTEMI cases are more frequently diagnosed due to improved biomarker-based detection methods and increased hospital admissions for chest pain evaluation. In addition, the availability of well-established treatment protocols and pharmacological management options further supports its dominance. Healthcare providers often prioritize early intervention in NSTEMI cases, contributing to higher diagnosis and treatment rates. The growing awareness regarding cardiovascular health and routine screening programs also enhances case identification. The segment benefits from widespread accessibility to treatment across both developed and developing regions. Moreover, NSTEMI patients often require prolonged monitoring and follow-up care, increasing healthcare utilization. Its relatively lower immediate mortality risk compared to STEMI allows more treatment opportunities, thereby contributing to sustained revenue generation. Increasing hospital admissions and favorable reimbursement scenarios further strengthen this segment’s leading position in the market.

The STEMI segment is anticipated to witness the fastest growth rate of 21.9% from 2026 to 2033, fueled by the rising need for rapid emergency cardiac care and advancements in reperfusion therapies such as percutaneous coronary intervention (PCI). STEMI cases require immediate medical attention, leading to increased demand for advanced cardiac facilities and specialized healthcare professionals. Governments and healthcare organizations are investing heavily in improving emergency response systems, which is supporting faster diagnosis and treatment of STEMI cases. The growing availability of catheterization laboratories and improved ambulance networks also contribute to segment growth. Technological advancements in diagnostic tools, including ECG and imaging, are enabling quicker identification of STEMI events. Increasing awareness about heart attack symptoms and timely intervention is further boosting patient inflow. In addition, rising prevalence of acute cardiac events due to sedentary lifestyles is supporting growth. The segment also benefits from ongoing clinical research and innovations in minimally invasive procedures. Favorable reimbursement policies in developed regions further accelerate adoption. As healthcare infrastructure continues to improve globally, STEMI management is expected to expand rapidly, driving the segment’s strong CAGR.

• By Diagnosis

On the basis of diagnosis, the Acute Coronary Syndrome market is segmented into stress test, blood tests, imaging, and others. The blood tests segment dominated the largest market revenue share of 42.7% in 2025, driven by the widespread use of cardiac biomarkers such as troponin for early and accurate detection of myocardial injury. Blood tests are considered the gold standard in ACS diagnosis due to their high sensitivity, rapid turnaround time, and ability to confirm cardiac events even in early stages. Hospitals and emergency departments heavily rely on these tests for quick clinical decision-making. The increasing availability of advanced diagnostic kits and automated analyzers further supports segment growth. In addition, blood tests are cost-effective and easily accessible across various healthcare settings, including small clinics and diagnostic centers. Rising patient awareness and routine screening practices also contribute to higher testing volumes. The integration of point-of-care testing devices enhances convenience and efficiency in emergency situations. Furthermore, technological advancements are improving the precision and reliability of biomarker detection. Growing prevalence of cardiovascular diseases globally is further driving demand for diagnostic testing. Strong clinical guidelines recommending biomarker testing ensure sustained adoption.

The imaging segment is expected to witness the fastest CAGR of 20.8% from 2026 to 2033, driven by advancements in non-invasive imaging technologies such as CT angiography and cardiac MRI. Imaging plays a crucial role in assessing the severity and location of arterial blockages, aiding in accurate treatment planning. Increasing preference for non-invasive diagnostic methods is boosting the adoption of advanced imaging solutions. Hospitals are investing in high-end imaging systems to enhance diagnostic capabilities and patient outcomes. The growing geriatric population, which requires detailed cardiac evaluation, further supports demand. Technological innovations enabling faster imaging with improved resolution are accelerating growth. In addition, integration of AI in imaging analysis is improving diagnostic accuracy and efficiency. Rising healthcare expenditure and infrastructure development in emerging markets are also contributing to segment expansion. Imaging techniques are increasingly being used alongside biomarker tests for comprehensive diagnosis. Favorable reimbursement policies in developed regions further encourage adoption.

• By Treatment

On the basis of treatment, the Acute Coronary Syndrome market is segmented into medication and surgery. The medication segment dominated the largest market revenue share of 53.6% in 2025, driven by the widespread use of antiplatelet agents, anticoagulants, beta-blockers, and statins in the initial management of ACS. Pharmacological therapy is often the first line of treatment, making it highly prevalent across all healthcare settings. The increasing availability of effective drug combinations and continuous advancements in pharmaceutical formulations support segment growth. Medications are cost-effective compared to surgical interventions, making them accessible to a larger patient population. In addition, long-term medication use for secondary prevention contributes to sustained revenue generation. Rising awareness about early treatment and preventive care further boosts demand. The segment also benefits from strong clinical guidelines recommending immediate drug therapy upon diagnosis. Increasing prevalence of cardiovascular diseases globally continues to drive medication usage. Moreover, the expansion of generic drug markets enhances affordability and accessibility. Continuous research and development activities are leading to the introduction of more effective therapies.

The surgery segment is expected to witness the fastest CAGR of 19.6% from 2026 to 2033, driven by increasing adoption of interventional procedures such as angioplasty and coronary artery bypass grafting (CABG). Technological advancements in minimally invasive surgical techniques are improving patient outcomes and reducing recovery time. The growing number of specialized cardiac care centers and skilled professionals is supporting segment growth. Rising cases of severe coronary artery blockages requiring immediate intervention further boost demand. In addition, increasing healthcare investments in advanced surgical infrastructure contribute to expansion. Favorable reimbursement policies in developed regions encourage patients to opt for surgical treatments. The integration of robotic-assisted surgeries is enhancing precision and efficiency. Growing awareness about advanced treatment options is also driving patient preference toward surgical solutions. Furthermore, improvements in post-operative care and reduced complication rates support higher adoption. As healthcare systems continue to evolve, surgical treatments are expected to witness significant growth.

• By End User

On the basis of end user, the Acute Coronary Syndrome market is segmented into hospitals and clinics, diagnostic centers, academic institutes, and others. The hospitals and clinics segment accounted for the largest market revenue share of 57.4% in 2025, driven by the availability of comprehensive cardiac care facilities and emergency treatment services. Hospitals are the primary point of care for ACS patients due to the need for immediate diagnosis and intervention. The presence of advanced diagnostic equipment, skilled healthcare professionals, and intensive care units further strengthens this segment. Increasing hospital admissions for cardiac emergencies contribute significantly to revenue generation. In addition, the integration of multidisciplinary care approaches enhances treatment outcomes. Government investments in healthcare infrastructure also support hospital growth. The segment benefits from strong reimbursement frameworks in developed regions. Rising prevalence of cardiovascular diseases globally further increases patient inflow. Hospitals also serve as key centers for surgical procedures and long-term management. Continuous advancements in hospital-based technologies enhance efficiency and patient care.

The diagnostic centers segment is anticipated to witness the fastest growth rate of 21.2% from 2026 to 2033, fueled by the growing demand for specialized and early diagnostic services. Diagnostic centers offer cost-effective and accessible testing solutions, making them increasingly popular among patients. The expansion of standalone diagnostic facilities and chain laboratories supports segment growth. Technological advancements in diagnostic equipment improve accuracy and efficiency. Increasing focus on preventive healthcare and routine screening further boosts demand. Diagnostic centers also reduce the burden on hospitals by providing timely testing services. Rising awareness about early disease detection is encouraging patients to seek diagnostic services. In addition, partnerships between hospitals and diagnostic centers enhance service delivery. The adoption of point-of-care testing and digital reporting systems improves patient convenience. As healthcare systems shift toward outpatient care, diagnostic centers are expected to experience rapid growth.

Acute Coronary Syndrome Market Regional Analysis

- North America dominated the acute coronary syndrome market with the largest revenue share of approximately 40.5% in 2025, supported by well-established healthcare infrastructure, high healthcare expenditure, and strong adoption of advanced diagnostic and treatment solutions

- The region benefits from widespread availability of high-sensitivity diagnostic tests, advanced interventional cardiology procedures, and a strong presence of leading pharmaceutical and medical device companies

- This dominance is further reinforced by increasing awareness regarding early diagnosis, favorable reimbursement policies, and a high prevalence of cardiovascular diseases, establishing North America as a key contributor to the Acute Coronary Syndrome market

U.S. Acute Coronary Syndrome Market Insight

The U.S. acute coronary syndrome market captured the largest revenue share of approximately 81% in 2025 within North America, driven by the high prevalence of cardiovascular diseases and a well-developed healthcare system. The country benefits from early adoption of advanced diagnostic technologies, including high-sensitivity troponin assays, along with strong access to interventional treatments such as angioplasty and coronary artery bypass procedures. In addition, the presence of major market players, increasing healthcare spending, and strong focus on preventive care and early intervention significantly contribute to market growth in the United States.

Europe Acute Coronary Syndrome Market Insight

The Europe acute coronary syndrome market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing incidence of cardiovascular diseases and supportive government healthcare policies. The region’s well-established healthcare systems and growing emphasis on early diagnosis and effective disease management are fostering market growth. In addition, advancements in diagnostic technologies and increasing adoption of minimally invasive procedures are contributing to improved patient outcomes across the region.

U.K. Acute Coronary Syndrome Market Insight

The U.K. acute coronary syndrome market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising awareness regarding heart diseases and the increasing burden of cardiovascular conditions. Government initiatives aimed at improving cardiac care, along with the presence of advanced healthcare facilities, are supporting early diagnosis and timely treatment. Furthermore, increasing focus on preventive healthcare and lifestyle management is expected to contribute to sustained market growth.

Germany Acute Coronary Syndrome Market Insight

The Germany acute coronary syndrome market is expected to expand at a considerable CAGR during the forecast period, fueled by the country’s advanced healthcare infrastructure and strong focus on medical innovation. Germany has a high adoption rate of advanced diagnostic tools and interventional cardiology procedures, which supports effective disease management. In addition, increasing healthcare expenditure and growing awareness regarding early detection of cardiac conditions are key factors driving market growth in the country.

Asia-Pacific Acute Coronary Syndrome Market Insight

The Asia-Pacific acute coronary syndrome market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by rapid urbanization, increasing disposable incomes, and improving healthcare infrastructure. The region is also witnessing a rising incidence of lifestyle-related cardiac disorders due to changing dietary habits, sedentary lifestyles, and increasing stress levels in countries such as China and India. Government initiatives aimed at strengthening healthcare systems and improving access to cardiac care are further accelerating market growth across the region.

Japan Acute Coronary Syndrome Market Insight

The Japan acute coronary syndrome market is gaining momentum due to the country’s aging population, which is highly susceptible to cardiovascular diseases. The presence of advanced healthcare technologies, early diagnostic practices, and strong emphasis on preventive care are supporting market growth. In addition, Japan’s well-developed healthcare infrastructure and continuous advancements in cardiac treatment methods are contributing to improved patient outcomes.

China Acute Coronary Syndrome Market Insight

The China acute coronary syndrome market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rapid urbanization, a growing middle-class population, and increasing prevalence of cardiovascular diseases. The country is experiencing significant improvements in healthcare infrastructure and access to advanced diagnostic and treatment solutions. Moreover, rising healthcare expenditure, government initiatives to combat chronic diseases, and increasing awareness regarding early diagnosis are key factors propelling the market growth in China.

Acute Coronary Syndrome Market Share

The Acute Coronary Syndrome industry is primarily led by well-established companies, including:

- Assa Abloy (Sweden)

- Allegion (Ireland)

- Kwikset (U.S.)

- Yale (Sweden)

- August Home (U.S.)

- Schlage (U.S.)

- Level Lock (U.S.)

- Lockly (U.S.)

- U-tec (U.S.)

- TP-Link (China)

- Eufy Security (China)

- Aqara (China)

- Nuki (Austria)

- Danalock (Denmark)

- Samsung SmartThings (South Korea)

- Honeywell (U.S.)

- Brinks Home (U.S.)

- Vivint (U.S.)

- ZKTeco (China)

- Tesa (Spain)

Latest Developments in Global Acute Coronary Syndrome Market

- In October 2023, Abbott Laboratories, a leading medical device company, announced the launch of its advanced drug-eluting stent system designed for patients with Acute Coronary Syndrome (ACS), incorporating enhanced polymer technology to reduce restenosis rates and improve long-term vessel healing outcomes following percutaneous coronary interventions

- In January 2024, Roche, a global diagnostics leader, announced the launch of its next-generation high-sensitivity cardiac troponin assay, aimed at enabling faster and more accurate diagnosis of myocardial infarction in ACS patients, thereby improving emergency department decision-making and patient triage

- In June 2024, European Society of Cardiology reported the increasing clinical adoption of dual pathway therapy (combining antiplatelet and low-dose anticoagulant treatment) for Acute Coronary Syndrome management across Europe, reflecting a shift toward more comprehensive thrombosis prevention strategies and improved cardiovascular outcomes

- In September 2024, Philips Healthcare introduced an advanced digital health platform integrated with remote cardiac monitoring solutions for ACS patients, designed to improve medication adherence, enable real-time patient tracking, and enhance post-discharge care management

- In January 2025, Cyclarity Therapeutics announced the initiation of its first-in-human clinical trial for a novel therapy targeting arterial plaque removal, representing a breakthrough interventional approach aimed at addressing the root cause of Acute Coronary Syndrome

- In February 2025, Idorsia and Viatris announced the revision of their global collaboration agreement to accelerate the development of Selatogrel, an investigational P2Y12 inhibitor for early-stage treatment of Acute Coronary Syndrome, strengthening their joint cardiovascular pipeline strategy

- In March 2025, U.S. Food and Drug Administration granted Fast Track designation to SGC001, a novel monoclonal antibody therapy under development for acute myocardial infarction, aiming to expedite its clinical development and regulatory review as a potential emergency treatment for ACS

- In April 2025, Roche announced that it received CE mark approval for its Chest Pain Triage algorithm, a diagnostic solution integrated with high-sensitivity troponin testing to rapidly rule in or rule out Acute Coronary Syndrome in emergency settings, improving clinical workflow efficiency and diagnostic accuracy

- In August 2025, Gland Pharma Limited announced that it received approval from the U.S. Food and Drug Administration for Cangrelor for Injection, an intravenous P2Y12 platelet inhibitor used as an adjunct to percutaneous coronary intervention in ACS patients, expanding access to cost-effective treatment options

- In August 2025, Roche reported positive results from its TSIX clinical study program demonstrating that its sixth-generation high-sensitivity Troponin T assay delivers improved sensitivity and diagnostic accuracy for Acute Coronary Syndrome, supporting faster and more reliable patient risk stratification

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.