Global Angiography Equipment Market

Размер рынка в млрд долларов США

CAGR :

%

USD

11.14 Billion

USD

17.68 Billion

2025

2033

USD

11.14 Billion

USD

17.68 Billion

2025

2033

| 2026 –2033 | |

| USD 11.14 Billion | |

| USD 17.68 Billion | |

| % | |

|

Global Angiography Equipment Market Segmentation, By Product (Angiography Systems, Angiography Catheters, Angiography Contrast Media, Vascular Closure Devices (VCDs), Angiography Balloons, Angiography Guidewires, and Angiography Accessories), Technology (X-Ray Angiography, CT Angiography, MR Angiography, and Other), Procedure (Coronary Angiography, Endovascular Angiography, Neuroangiography, Onco-Angiography, and Other), Indication (Coronary Artery Disease, Valvular Heart Disease, Congenital Heart Disease, Congestive Heart Failure, and Other), Application (Diagnostics and Therapeutics), End User (Hospitals and Clinics, Diagnostic and Imaging Centers, and Research Institutes)- Industry Trends and Forecast to 2033

Angiography Equipment Market Size

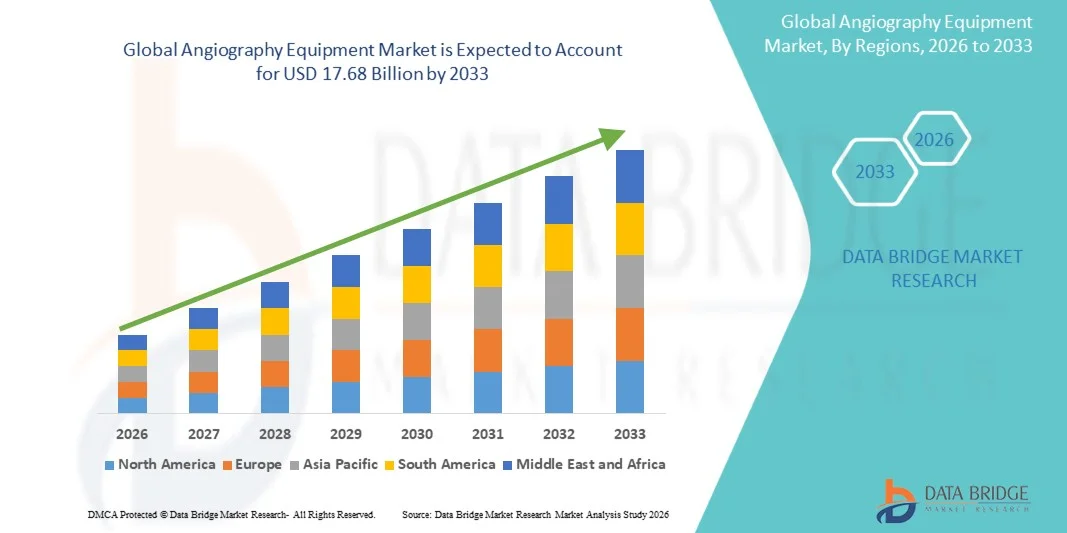

- The global angiography equipment market size was valued at USD 11.14 billion in 2025 and is expected to reach USD 17.68 billion by 2033, at a CAGR of 5.95% during the forecast period

- The market growth is largely fueled by the increasing prevalence of cardiovascular diseases, rising demand for minimally invasive diagnostic procedures, and technological advancements in imaging systems, including high-resolution and hybrid angiography platforms

- Furthermore, the expanding geriatric population, growing hospital infrastructure, and emphasis on early diagnosis and precise treatment planning are driving adoption of angiography equipment across healthcare facilities. These converging factors are accelerating the uptake of angiography solutions, thereby significantly boosting the industry's growth

Angiography Equipment Market Analysis

- Angiography equipment, providing high-precision imaging of blood vessels and cardiac structures, is increasingly critical in modern diagnostic and interventional cardiology procedures across both hospitals and specialized clinics due to its accuracy, minimally invasive capabilities, and integration with advanced imaging and navigation systems

- The escalating demand for angiography equipment is primarily driven by the rising prevalence of cardiovascular diseases, increasing preference for minimally invasive procedures, and continuous technological advancements such as 3D imaging, hybrid angiography, and AI-assisted diagnostics

- North America dominated the angiography equipment market with the largest revenue share of 38.5% in 2025, characterized by early adoption of advanced medical imaging technologies, high healthcare expenditure, and the strong presence of leading equipment manufacturers, with the U.S. experiencing substantial growth in installations, particularly in tertiary hospitals and cardiac specialty centers, driven by innovations in catheter-based interventions and imaging software

- Asia-Pacific is expected to be the fastest-growing region in the angiography equipment market during the forecast period due to increasing incidence of cardiovascular diseases, expanding hospital infrastructure, and rising healthcare spending in countries such as China and India

- Angiography Systems segment dominated the product segment with a market share of 41.3% in 2025, driven by their central role in performing diagnostic and interventional procedures across cardiovascular, neuro, and peripheral vascular interventions

Report Scope and Angiography Equipment Market Segmentation

|

Attributes |

Angiography Equipment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Angiography Equipment Market Trends

“Integration of AI and Advanced Imaging Technologies”

- A significant and accelerating trend in the global angiography equipment market is the incorporation of artificial intelligence (AI) and advanced imaging software into angiography systems, enhancing procedural accuracy and diagnostic capabilities across hospitals and specialty clinics

- For instance, Siemens’ Artis Q.zen angiography system uses AI-based image optimization to reduce radiation exposure while maintaining high-resolution vascular imaging during interventions

- AI integration enables features such as real-time vessel segmentation, predictive procedural guidance, and automated anomaly detection, helping physicians optimize interventions and improve patient outcomes. Furthermore, software-assisted imaging enhances procedural efficiency by reducing manual adjustments during complex cases

- The seamless integration of angiography equipment with hospital information systems and hybrid imaging platforms facilitates centralized management of diagnostic and interventional workflows, allowing physicians to access patient imaging data and procedural analytics from a unified interface

- This trend toward smarter, more intuitive, and interconnected imaging systems is fundamentally reshaping expectations for interventional procedures. Consequently, companies such as GE Healthcare are developing AI-enabled angiography systems with predictive workflow tools and enhanced 3D imaging for complex cardiovascular and neurovascular procedures

- The demand for angiography systems offering AI-assisted imaging and workflow integration is growing rapidly across both developed and emerging healthcare markets, as hospitals increasingly prioritize procedural precision, patient safety, and efficiency

- The trend of cloud-based imaging storage and analytics allows hospitals to access, share, and analyze angiography data remotely, facilitating telemedicine and collaborative clinical decision-making

Angiography Equipment Market Dynamics

Driver

“Rising Cardiovascular Disease Prevalence and Minimally Invasive Procedure Adoption”

- The increasing prevalence of cardiovascular diseases, coupled with the rising adoption of minimally invasive diagnostic and interventional procedures, is a significant driver for the heightened demand for angiography equipment

- For instance, in March 2025, Philips Healthcare launched its Allura Xper FD20 system with advanced imaging and procedural support to improve outcomes in complex cardiac interventions. Such innovations by leading companies are expected to drive angiography equipment adoption during the forecast period

- As hospitals and cardiac centers aim to improve patient outcomes and reduce recovery times, angiography systems offer advanced imaging features such as real-time 3D reconstruction, vessel visualization, and automated measurements, providing a compelling advantage over traditional catheterization methods

- Furthermore, the expansion of hybrid operating rooms and the growing trend of interventional cardiology and radiology procedures are making angiography systems essential in modern clinical practice, offering seamless integration with other diagnostic and surgical tools

- The convenience of precise, minimally invasive imaging, reduced procedural time, and the ability to manage interventions through integrated software solutions are key factors propelling adoption of angiography equipment in both public and private healthcare facilities

- Increasing government initiatives and healthcare infrastructure investments in emerging economies are supporting the acquisition of advanced angiography systems, driving market expansion

- Growing awareness among physicians and patients about the benefits of early diagnosis and image-guided interventions is contributing to higher adoption of angiography technologies across hospitals and specialty clinics

Restraint/Challenge

“High Costs and Regulatory Compliance Hurdles”

- The high capital investment required for advanced angiography equipment, along with strict regulatory requirements, poses a significant challenge to broader market penetration, particularly in developing regions

- For instance, hospitals must comply with FDA, CE, and other regional approvals before deploying complex angiography systems, which can delay procurement and increase overall costs

- Addressing these cost and regulatory challenges through financing options, leasing models, and phased implementation strategies is crucial for expanding market access. Companies such as Canon Medical Systems and Siemens highlight modular and cost-effective solutions to reduce financial barriers. In addition, the complexity of operating high-end angiography systems requires specialized training, which can be a barrier for smaller clinics or facilities with limited staff

- While prices for basic angiography equipment are gradually decreasing, premium systems with hybrid capabilities, AI integration, and advanced 3D imaging often remain expensive, potentially limiting adoption in resource-constrained healthcare settings

- Overcoming these challenges through streamlined regulatory approvals, training programs, and scalable product offerings will be vital for sustained market growth and wider adoption of advanced angiography technologies

- Maintenance and operational costs, including specialized consumables and service contracts, can further restrict adoption by smaller healthcare facilities with limited budgets

- Variations in reimbursement policies and insurance coverage for image-guided procedures across regions may also limit market growth and slow procurement decisions in certain countries

Angiography Equipment Market Scope

The market is segmented on the basis of product, technology, procedure, indication, application, and end user.

- By Product

On the basis of product, the angiography equipment market is segmented into angiography systems, angiography catheters, angiography contrast media, vascular closure devices (VCDs), angiography balloons, angiography guidewires, and angiography accessories. The angiography systems segment dominated the market with the largest revenue share of 41.3% in 2025, driven by their central role in performing both diagnostic and interventional procedures across cardiovascular, neurovascular, and peripheral vascular treatments. Hospitals and specialty clinics prioritize angiography systems for their ability to integrate imaging, procedural guidance, and workflow management, which improves patient outcomes. Advanced features such as 3D imaging, AI-assisted image optimization, and hybrid OR compatibility further strengthen this segment’s dominance. Developed regions show consistent adoption due to high awareness and established healthcare infrastructure. Continuous technological innovation and training support also drive hospitals to invest in these systems.

The angiography catheters segment is expected to witness the fastest growth during the forecast period, fueled by the increasing number of minimally invasive procedures and rising demand for specialized interventional tools. Catheters are essential for delivering contrast media and interventional devices during angiographic procedures, and innovations in materials, flexibility, and imaging compatibility are driving adoption. Hospitals and diagnostic centers prefer advanced catheters that improve patient safety and procedural precision. The growing focus on reducing procedural complications further supports this segment’s expansion.

- By Technology

On the basis of technology, the market is segmented into X-Ray angiography, CT angiography, MR angiography, and other technologies. The X-Ray angiography segment held the largest market share in 2025 due to its established use, high accuracy, and compatibility with existing hospital imaging infrastructure. It is widely used in interventional cardiology and radiology procedures, providing real-time imaging essential for minimally invasive interventions. Hospitals often invest in X-ray angiography for its reliability, proven clinical outcomes, and widespread acceptance among physicians. The technology allows integration with hybrid operating rooms and supports advanced procedural guidance. Its mature ecosystem and extensive technician training further reinforce market dominance.

The CT angiography segment is expected to witness the fastest CAGR from 2026 to 2033, driven by increasing demand for non-invasive diagnostics and rapid, high-resolution imaging. CT angiography allows comprehensive assessment of vascular structures without catheter insertion, improving patient comfort and workflow efficiency. Technological improvements such as faster scanning, reduced radiation dose, and enhanced software for 3D reconstruction increase adoption. Growing awareness among patients and physicians about non-invasive alternatives supports the segment’s expansion.

- By Procedure

On the basis of procedure, the market is segmented into coronary angiography, endovascular angiography, neuroangiography, onco-angiography, and other procedures. The coronary angiography segment dominated in 2025, driven by the high prevalence of coronary artery disease worldwide. It is the most common interventional procedure for diagnosing and treating heart conditions, supported by advancements in real-time imaging, 3D reconstruction, and AI-assisted guidance. Hospitals prioritize coronary angiography for its clinical relevance and critical role in planning interventions. High procedural volumes and reimbursement support further strengthen the segment’s market share. Growing focus on early diagnosis and preventive cardiology also fuels demand.

The neuroangiography segment is anticipated to witness the fastest growth during the forecast period, fueled by the rising incidence of stroke, aneurysms, and other neurovascular disorders. Advanced imaging and AI-assisted navigation enhance procedural accuracy in neuroangiography, driving adoption in specialty neurology centers. Minimally invasive techniques, improved patient outcomes, and rising healthcare expenditure in emerging markets also contribute to growth. Technological advancements make neuroangiography safer and more effective. Hospitals are expanding neurointerventional units to meet rising demand.

- By Indication

On the basis of indication, the market is segmented into coronary artery disease, valvular heart disease, congenital heart disease, congestive heart failure, and other indications. The coronary artery disease segment dominated in 2025 due to the large patient population and the critical role of angiography in diagnosis and treatment planning. Hospitals and cardiology centers focus on coronary angiography as a standard intervention for early detection, stenting, and procedural guidance. High procedural volumes, reimbursement policies, and clinical acceptance strengthen this segment’s dominance. Technological innovations and hospital investments further reinforce its market share. The segment also benefits from global awareness campaigns targeting cardiovascular health.

The congenital heart disease segment is expected to witness the fastest growth during the forecast period, driven by increasing pediatric interventions and advancements in minimally invasive imaging for structural heart anomalies. Early diagnosis and improved survival rates are pushing adoption of specialized angiography techniques in this indication. Emerging hospitals in developing regions are investing in congenital cardiac imaging solutions, supporting market growth. Technological innovations improve procedural safety and outcomes for this patient group.

- By Application

On the basis of application, the market is segmented into diagnostics and therapeutics. The diagnostics segment dominated in 2025, reflecting continuous demand for early disease detection, accurate assessment of vascular conditions, and planning of interventional procedures. Hospitals rely on angiography systems for precise imaging, enabling informed clinical decision-making. Integration with electronic health records and imaging software enhances diagnostic workflow efficiency. Its central role in disease management and high procedural volumes reinforce dominance. The segment also benefits from increasing screening initiatives for cardiovascular and neurovascular conditions.

The therapeutics segment is expected to witness the fastest growth during the forecast period, fueled by rising adoption of image-guided interventional procedures such as stent placements, angioplasty, and vascular closure device deployment. Therapeutic angiography systems reduce patient recovery times and procedural risks, increasing hospital preference. Growing acceptance of minimally invasive treatment protocols and rising procedural volumes in emerging economies drive adoption. Technological advancements in device compatibility further support growth.

- By End User

On the basis of end user, the market is segmented into hospitals and clinics, diagnostic and imaging centers, and research institutes. The hospitals and clinics segment dominated in 2025, driven by large procedural volumes, well-established cardiology and radiology departments, and the ability to invest in high-end angiography systems. Hospitals provide comprehensive infrastructure, trained staff, and high patient throughput, making them the primary end users. Advanced hybrid OR setups and adoption of minimally invasive procedures further reinforce dominance. Their role in critical care and specialized interventions supports consistent revenue generation.

The diagnostic and imaging centers segment is expected to witness the fastest growth from 2026 to 2033, fueled by rising demand for specialized imaging services, outpatient procedures, and the expansion of standalone diagnostic facilities in emerging markets. These centers focus on non-invasive, cost-effective, and efficient imaging solutions to cater to a growing patient base. Increasing awareness about early diagnosis and cardiovascular screening also supports rapid adoption. . Partnerships with hospitals and clinics boost procedural volume. Centers can quickly scale offerings with modern angiography systems.

Angiography Equipment Market Regional Analysis

- North America dominated the angiography equipment market with the largest revenue share of 38.5% in 2025, characterized by early adoption of advanced medical imaging technologies, high healthcare expenditure, and the strong presence of leading equipment manufacturers

- Hospitals and specialty clinics in the region prioritize angiography systems for both diagnostic and interventional procedures, leveraging real-time imaging, AI-assisted guidance, and 3D reconstruction capabilities to improve patient outcomes

- This widespread adoption is further supported by high healthcare expenditure, the presence of major industry players, and increasing investments in hybrid operating rooms, making North America a key revenue contributor for angiography equipment

U.S. Angiography Equipment Market Insight

The U.S. angiography equipment market captured the largest revenue share of 42% in 2025 within North America, fueled by the high prevalence of cardiovascular diseases and early adoption of advanced imaging technologies. Hospitals and specialty clinics are increasingly prioritizing minimally invasive procedures supported by AI-assisted angiography systems, improving procedural accuracy and patient outcomes. The growing demand for hybrid operating rooms and image-guided interventions further propels the market. Moreover, the U.S. benefits from a well-established healthcare infrastructure, high healthcare expenditure, and the presence of key market players, ensuring rapid adoption of innovative angiography solutions. Reimbursement support and physician awareness campaigns also contribute significantly to market growth.

Europe Angiography Equipment Market Insight

The Europe angiography equipment market is projected to expand at a substantial CAGR during the forecast period, primarily driven by advanced healthcare infrastructure and increasing preference for minimally invasive procedures. Rising prevalence of cardiovascular and neurovascular disorders, coupled with government initiatives supporting early diagnosis, is fostering adoption of angiography systems. European hospitals emphasize workflow-efficient systems that integrate AI, 3D imaging, and hybrid procedural capabilities. The market is witnessing growth across diagnostic, interventional, and research applications, with systems being incorporated in both new hospital constructions and facility upgrades.

U.K. Angiography Equipment Market Insight

The U.K. angiography equipment market is anticipated to grow at a noteworthy CAGR, driven by the rising incidence of cardiovascular and neurovascular conditions and growing demand for image-guided interventions. Increasing focus on early diagnosis and preventive healthcare is encouraging hospitals and diagnostic centers to invest in high-end angiography systems. Moreover, integration of AI-assisted imaging, real-time 3D reconstruction, and hybrid OR compatibility is enhancing procedural accuracy and efficiency. The U.K.’s strong healthcare system and adoption of innovative technologies further stimulate market growth. Growing outpatient diagnostic centers also contribute to expanding angiography service adoption.

Germany Angiography Equipment Market Insight

The Germany angiography equipment market is expected to expand at a considerable CAGR, fueled by increasing awareness of cardiovascular health and the rising adoption of advanced imaging technologies. Germany’s well-developed healthcare infrastructure and focus on innovation promote the integration of AI-enabled and hybrid angiography systems. Hospitals and specialty centers emphasize accuracy, safety, and workflow efficiency in both diagnostic and interventional procedures. In addition, the market benefits from government-supported preventive healthcare programs and high procedural volumes. Integration with electronic health record systems enhances clinical workflow and drives adoption further.

Asia-Pacific Angiography Equipment Market Insight

The Asia-Pacific angiography equipment market is poised to grow at the fastest CAGR of 22% during the forecast period of 2026 to 2033, driven by rising cardiovascular disease prevalence, expanding hospital infrastructure, and increasing healthcare expenditure in countries such as China, Japan, and India. Growing awareness about early diagnosis, expanding specialty cardiac and neurovascular centers, and adoption of minimally invasive procedures are boosting market growth. Government initiatives promoting healthcare modernization and the increasing availability of advanced imaging solutions further support adoption. Moreover, the emergence of local manufacturers and affordable imaging solutions is improving accessibility across urban and semi-urban hospitals.

Japan Angiography Equipment Market Insight

The Japan angiography equipment market is gaining momentum due to the country’s advanced healthcare system, high-tech culture, and focus on minimally invasive interventions. The demand for accurate, real-time imaging in cardiovascular and neurovascular procedures is increasing, driving the adoption of AI-assisted angiography systems. Hospitals and diagnostic centers are integrating these systems with hybrid ORs and electronic health records to optimize procedural efficiency. Japan’s aging population is also contributing to higher demand for image-guided interventions, particularly in preventive and therapeutic procedures. Government healthcare programs supporting advanced diagnostics further accelerate market expansion.

India Angiography Equipment Market Insight

The India angiography equipment market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rising cardiovascular disease prevalence, rapid hospital expansion, and increasing healthcare awareness. India is witnessing growing adoption of minimally invasive procedures and advanced angiography systems in both urban and tier-2 cities. The push towards smart hospitals and government initiatives to modernize healthcare infrastructure are key factors propelling market growth. Availability of cost-effective imaging systems and the emergence of domestic manufacturers enhance accessibility. Rising procedural volumes in cardiology, neurology, and oncology also drive demand.

Angiography Equipment Market Share

The Angiography Equipment industry is primarily led by well-established companies, including:

- GE HealthCare (U.S.)

- Siemens Healthineers AG (Germany)

- CANON MEDICAL SYSTEMS CORPORATION (U.S.)

- Boston Scientific Corporation (U.S.)

- B. Braun SE (Germany)

- Koninklijke Philips N.V. (Netherlands)

- AngioDynamics (U.S.)

- Abbott (U.S.)

- Medtronic (Ireland)

- Terumo Corporation (Japan)

- Cordis Corporation (U.S.)

- Shimadzu Corporation (Japan)

- Merit Medical Systems Inc. (U.S.)

- Guerbet S.A. (France)

- Lantheus Medical Imaging Inc. (U.S.)

- Mindray Medical International Limited (China)

- Neusoft Medical Systems Co., Ltd. (China)

- Samsung Medison Co. Ltd. (South Korea)

- FUJIFILM Medical Systems Inc. (Japan)

- Ziehm Imaging GmbH (Germany)

What are the Recent Developments in Global Angiography Equipment Market?

- In December 2025, Canon Medical Systems announced the global commercial launch of its Alphenix 4D CT with Aquilion ONE / INSIGHT Edition, a next‑generation Angio‑CT hybrid suite combining high‑definition angiography with wide‑area CT in a single room for interventional procedures, enhancing workflow, safety, and imaging precision for complex vascular interventions

- In December 2025, Philips announced an agreement to acquire SpectraWAVE, Inc., a developer of AI‑enabled coronary intravascular imaging and angio‑based fractional flow reserve (FFR) technology, which will expand Philips’ image‑guided therapy portfolio and support advanced AI‑driven angiographic diagnostics and physiology assessment

- In September 2025, Canon Medical Systems unveiled the first global reference site for its combined Alphenix 4D CT and Aquilion One Insight Edition angio‑CT suite at Centre Hospitalier Universitaire (CHU) de Montpellier in France, showcasing optimized interventional imaging workflows and improved precision for angiography procedures in real clinical settings

- In May 2025, the Sanjay Gandhi Postgraduate Institute of Medical Sciences (SGPGIMS) in Lucknow installed an AI‑powered intravascular OCT imaging system integrated with 3D angio‑co‑registration to aid precision angioplasty, enabling real‑time high‑resolution imaging of arterial plaque structure for better clinical decision‑making

- In May 2025, the North Eastern Indira Gandhi Regional Institute of Health and Medical Sciences (NEIGRIHMS) in Shillong inaugurated a Biplane Digital Subtraction Angiography (DSA) system, offering high‑resolution dual‑angle imaging that enhances diagnosis and treatment of complex neurovascular conditions such as stroke and aneurysms

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.