Global Coating Buffers Market

Размер рынка в млрд долларов США

CAGR :

%

USD

765.00 Million

USD

1,247.17 Million

2025

2033

USD

765.00 Million

USD

1,247.17 Million

2025

2033

| 2026 –2033 | |

| USD 765.00 Million | |

| USD 1,247.17 Million | |

| % | |

|

Global Coating Buffers Market Segmentation, By Type (Bicarbonate Buffer, Basic Buffer, and Others), End Users (Hospitals, Clinical Laboratories, Pharmaceutical and Biotechnology Companies and Cros, Blood Banks, Research and Academic Laboratories, and Others)- Industry Trends and Forecast to 2033

Coating Buffers Market Size

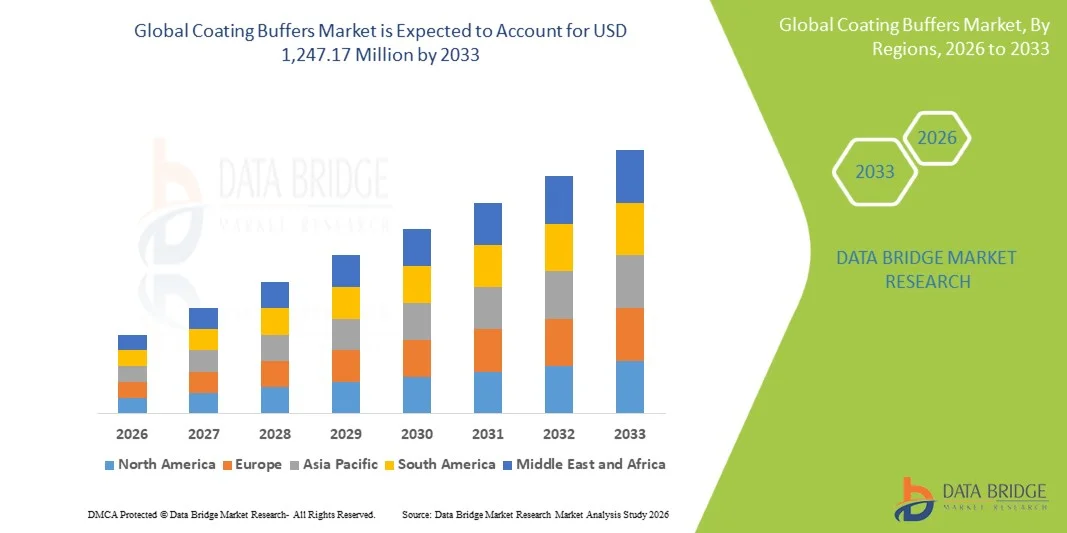

- The global coating buffers market size was valued at USD 765.00 million in 2025 and is expected to reach USD 1,247.17 million by 2033, at a CAGR of 6.3% during the forecast period

- The market growth is largely fueled by the increasing demand for reliable and consistent assay performance in life sciences research, diagnostics, and biotechnology applications, where coating buffers play a critical role in surface preparation and biomolecule immobilization

- Furthermore, rising adoption of immunoassays, ELISA-based testing, and advanced diagnostic techniques, along with expanding pharmaceutical and biotechnology R&D activities, is establishing coating buffers as essential reagents in laboratory workflows. These converging factors are accelerating the uptake of coating buffer solutions, thereby significantly boosting the industry's growth

Coating Buffers Market Analysis

- Coating buffers, widely used in life sciences and biotechnology workflows, are critical reagents that enable effective surface coating, biomolecule immobilization, and assay consistency, making them essential in applications such as diagnostics, pharmaceutical research, and immunoassays across both academic and commercial laboratories

- The escalating demand for coating buffers is primarily driven by the expanding adoption of immunoassays, increasing focus on disease diagnostics, and growing investment in biopharmaceutical R&D, along with the need for high-quality and reproducible laboratory results

- North America dominated the coating buffers market with the largest revenue share of 43.7% in 2025, supported by a well-established biotechnology and pharmaceutical industry, strong research infrastructure, and high adoption of advanced diagnostic technologies, particularly in the U.S., where extensive clinical testing and R&D activities continue to drive demand

- Asia-Pacific is expected to be the fastest growing region in the coating buffers market during the forecast period due to rising healthcare expenditure, expanding biotechnology sector, increasing research activities, and growing diagnostic testing capabilities in countries such as China and India

- Bicarbonate Buffer segment dominated the coating buffers market in 2025, accounting for 52.4% of the market share, driven by its widespread use in ELISA and other immunoassays for efficient protein adsorption and stable surface coating, making it a preferred choice in diagnostic and research applications

Report Scope and Coating Buffers Market Segmentation

|

Attributes |

Coating Buffers Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Coating Buffers Market Trends

“Rising Integration with Advanced Diagnostic and Automated Laboratory Systems”

- A significant and accelerating trend in the global coating buffers market is the increasing integration with automated laboratory platforms and advanced diagnostic systems, improving workflow efficiency and consistency in immunoassay and bioanalytical applications

- For instance, coating buffers are widely used in automated ELISA analyzers and high-throughput screening systems, enabling standardized surface preparation and reducing manual variability in testing procedures

- Advanced formulations of coating buffers are being optimized to enhance protein binding efficiency, stability, and reproducibility, supporting more accurate diagnostic outcomes in sensitive assays. Furthermore, manufacturers are developing ready-to-use and pre-optimized buffer solutions compatible with automated liquid handling systems, reducing preparation time and operational errors

- The seamless integration of coating buffers with modern laboratory workflows facilitates streamlined assay setup, allowing researchers to achieve consistent results across large sample volumes in pharmaceutical and clinical research environments. Through standardized protocols, laboratories can manage multiple assays efficiently while maintaining high data reliability

- This trend towards more standardized, high-performance, and automation-compatible buffer solutions is fundamentally reshaping laboratory expectations for reagent quality. Consequently, companies are focusing on developing specialized coating buffer formulations tailored for specific assay platforms and high-throughput applications

- The demand for coating buffers that support automation, reproducibility, and scalability is growing rapidly across research institutes, diagnostic laboratories, and biopharmaceutical companies, as end users increasingly prioritize efficiency and precision in experimental workflows

- Furthermore, the growing emphasis on quality assurance and regulatory compliance in diagnostic and pharmaceutical laboratories is driving the adoption of standardized coating buffer solutions that meet stringent performance and reproducibility requirements

Coating Buffers Market Dynamics

Driver

“Increasing Demand Driven by Expanding Diagnostic Testing and Biopharmaceutical Research”

- The increasing prevalence of chronic and infectious diseases, coupled with the accelerating adoption of advanced diagnostic testing and biopharmaceutical research activities, is a significant driver for the heightened demand for coating buffers

- For instance, the growing use of ELISA-based diagnostics and immunoassays in clinical laboratories is boosting the need for high-quality coating buffers to ensure accurate antigen-antibody interactions and reliable test results

- As research institutions and pharmaceutical companies expand their focus on biomarker discovery and therapeutic development, coating buffers play a critical role in enabling consistent assay performance and reproducibility across experiments

- Furthermore, the growing popularity of high-throughput screening techniques and laboratory automation is making coating buffers an essential component of standardized workflows, supporting large-scale testing and research operations

- The convenience of ready-to-use buffer formulations, improved assay sensitivity, and compatibility with a wide range of laboratory protocols are key factors propelling the adoption of coating buffers in both academic and commercial settings. The increasing availability of specialized buffer solutions tailored to specific assay requirements further contributes to market growth

- In addition, increasing investments in biotechnology infrastructure and expansion of diagnostic laboratories globally are further accelerating the demand for coating buffers across emerging and developed markets

Restraint/Challenge

“Stringent Quality Requirements and Sensitivity to Formulation Variability”

- Concerns surrounding stringent quality control requirements and batch-to-batch variability of coating buffer formulations pose a significant challenge to broader market penetration, as even minor inconsistencies can impact assay performance and reliability

- For instance, variations in buffer composition, pH stability, or ionic strength can affect protein adsorption efficiency and lead to inconsistent results in sensitive immunoassays, raising concerns among end users

- Addressing these quality challenges through strict manufacturing standards, rigorous validation protocols, and consistent formulation practices is crucial for building confidence among researchers and diagnostic laboratories. Companies emphasize high-purity ingredients and standardized production processes to ensure reproducibility and performance consistency

- In addition, the relatively limited shelf life of certain buffer formulations and the need for proper storage conditions can increase operational complexity and costs for end users, particularly in resource-constrained settings

- While improvements in formulation technologies and quality control systems are being implemented, maintaining consistency across large-scale production remains a challenge, especially for specialized or customized buffer solutions

- Overcoming these challenges through enhanced quality assurance measures, improved formulation stability, and cost-effective production techniques will be vital for sustained market growth and wider adoption across diverse laboratory applications

- In addition, fluctuations in raw material availability and pricing can create supply chain constraints, potentially affecting production consistency and increasing costs for manufacturers and end users

Coating Buffers Market Scope

The market is segmented on the basis of type and end users.

- By Type

On the basis of type, the coating buffers market is segmented into bicarbonate buffer, basic buffer, and others. The bicarbonate buffer segment dominated the market with the largest market revenue share of 52.4% in 2025, driven by its widespread use in ELISA and other immunoassays for efficient protein adsorption and stable surface coating. Laboratories and diagnostic centers prefer bicarbonate buffers due to their optimal pH conditions, which enhance antigen or antibody binding efficiency and improve assay reproducibility. The segment also benefits from its compatibility with a wide range of diagnostic platforms and standardized laboratory protocols, making it a preferred choice across research and clinical applications. In addition, its cost-effectiveness and ease of preparation further support its dominance in routine laboratory workflows. The increasing demand for reliable and consistent assay performance in diagnostics and pharmaceutical research continues to reinforce the adoption of bicarbonate buffers.

The basic buffer segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by its growing application in specialized research assays and conditions requiring higher pH environments for effective biomolecule immobilization. Basic buffers are increasingly being utilized in advanced immunoassays and protein binding studies where specific surface chemistry is required to achieve improved assay sensitivity. Their adoption is rising in pharmaceutical and biotechnology research environments where customized assay conditions are necessary for novel drug discovery and biomarker analysis. The segment is also gaining traction due to ongoing advancements in buffer formulation technologies that enhance stability and performance under varying experimental conditions. Increasing R&D activities and the need for tailored solutions in complex analytical procedures are further driving demand for basic buffers

- By End Users

On the basis of end users, the coating buffers market is segmented into hospitals, clinical laboratories, pharmaceutical and biotechnology companies and CROs, blood banks, research and academic laboratories, and others. The pharmaceutical and biotechnology companies and CROs segment dominated the market with the largest market revenue share in 2025, driven by extensive utilization of coating buffers in drug discovery, assay development, and quality control processes. These organizations rely heavily on coating buffers for ELISA, immunogenicity testing, and biomarker validation studies, where assay precision and reproducibility are critical. The segment benefits from strong investment in R&D activities and the growing pipeline of biologics and biosimilars requiring robust analytical testing. In addition, contract research organizations play a key role in outsourcing laboratory services, further increasing the consumption of coating buffers. The presence of advanced laboratory infrastructure and high adoption of automated systems in these organizations also contributes to their dominant market share.

The research and academic laboratories segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing government and private funding in life sciences research and the expansion of academic research initiatives globally. These laboratories extensively use coating buffers for experimental studies, assay development, and exploratory research in fields such as immunology, molecular biology, and biochemistry. The rising number of research publications, clinical studies, and collaborative projects is contributing to higher consumption of laboratory reagents, including coating buffers. In addition, the growing emphasis on early-stage research and innovation in emerging economies is expanding the demand base for coating buffer solutions. Academic institutions are also increasingly adopting automated and high-throughput systems, which require standardized reagents for consistent results.

Coating Buffers Market Regional Analysis

- North America dominated the coating buffers market with the largest revenue share of 43.7% in 2025, supported by a well-established biotechnology and pharmaceutical industry, strong research infrastructure, and high adoption of advanced diagnostic technologies

- Laboratories and research institutions in the region highly value the reliability, consistency, and performance of coating buffers in applications such as ELISA, immunoassays, and diagnostic testing, where accuracy is critical

- This widespread adoption is further supported by high R&D expenditure, advanced laboratory automation, and the growing preference for high-quality reagents to ensure reproducible results across clinical and research applications

U.S. Coating Buffers Market Insight

The U.S. coating buffers market captured the largest revenue share in 2025 within North America, fueled by the strong presence of biotechnology companies, pharmaceutical manufacturers, and advanced diagnostic laboratories. The increasing adoption of immunoassays, ELISA-based testing, and high-throughput screening in clinical and research settings is driving demand for high-quality coating buffers. Consumers and laboratories in the region highly value reagent consistency, assay reliability, and compatibility with automated laboratory systems. Moreover, the presence of leading research institutions, coupled with significant R&D investments and a well-established life sciences ecosystem, further supports market growth. The growing trend toward laboratory automation and standardized testing protocols is also significantly contributing to the expansion of the coating buffers market in the U.S.

Europe Coating Buffers Market Insight

The Europe coating buffers market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by strong regulatory frameworks, increasing focus on healthcare diagnostics, and rising investments in biotechnology research. The region’s emphasis on high-quality standards and reproducible laboratory outcomes is fostering the adoption of standardized coating buffer solutions across research and clinical laboratories. Increasing prevalence of chronic diseases and the growing demand for advanced diagnostic techniques are further supporting market growth. European laboratories are also increasingly integrating automated systems and standardized workflows, which enhance the utilization of coating buffers. In addition, expanding pharmaceutical research activities and collaborative academic-industry initiatives are contributing to steady market development across the region.

U.K. Coating Buffers Market Insight

The U.K. coating buffers market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the country’s strong biotechnology and pharmaceutical sectors and increasing focus on life sciences research. The rising demand for accurate diagnostic testing and advanced immunoassay techniques is encouraging the adoption of high-performance coating buffers. In addition, concerns regarding healthcare efficiency and early disease detection are supporting the expansion of diagnostic laboratories and research facilities. The U.K.’s robust academic research ecosystem, along with government support for innovation and biotechnology development, is further stimulating market growth. The increasing use of automated laboratory systems and standardized reagents is also contributing to the rising demand for coating buffers across various end-use applications.

Germany Coating Buffers Market Insight

The Germany coating buffers market is expected to expand at a considerable CAGR during the forecast period, fueled by the country’s advanced healthcare infrastructure and strong emphasis on precision diagnostics and research. Germany’s well-developed pharmaceutical and biotechnology industries are key contributors to the demand for coating buffers in applications such as immunoassays and biomolecular studies. Increasing investments in R&D activities and the growing adoption of laboratory automation are further supporting market growth. The country’s focus on high-quality, eco-conscious, and standardized laboratory practices promotes the use of reliable buffer solutions. In addition, the integration of advanced diagnostic technologies in clinical and research laboratories is enhancing the adoption of coating buffers across multiple applications.

Asia-Pacific Coating Buffers Market Insight

The Asia-Pacific coating buffers market is poised to grow at the fastest CAGR during the forecast period, driven by increasing urbanization, rising healthcare expenditure, and expanding biotechnology and pharmaceutical sectors in countries such as China, India, and Japan. The region’s growing focus on improving diagnostic capabilities and research infrastructure is boosting the demand for coating buffers in clinical and academic laboratories. Government initiatives promoting healthcare development and life sciences research are further accelerating market growth. In addition, the increasing availability of cost-effective laboratory reagents and the expansion of contract research organizations are contributing to wider adoption. Asia-Pacific is also emerging as a key manufacturing hub for life science reagents, enhancing accessibility and affordability of coating buffers across the region.

Japan Coating Buffers Market Insight

The Japan coating buffers market is gaining momentum due to the country’s advanced healthcare system, strong emphasis on research and development, and increasing adoption of innovative diagnostic technologies. The demand for coating buffers is driven by extensive use in immunoassays, clinical diagnostics, and pharmaceutical research. Japan’s focus on precision medicine and high-quality laboratory standards further supports the adoption of reliable buffer solutions. The integration of automation and advanced analytical systems in laboratories is also contributing to market growth. In addition, the country’s aging population is increasing the need for accurate and early diagnostic testing, thereby boosting the utilization of coating buffers in both clinical and research applications.

India Coating Buffers Market Insight

The India coating buffers market accounted for a significant revenue share in Asia Pacific in 2025, attributed to the country’s rapidly expanding healthcare sector, growing biotechnology industry, and increasing investment in research infrastructure. Rising awareness of advanced diagnostic techniques and the growing prevalence of chronic diseases are driving demand for immunoassay-based testing, thereby supporting coating buffer usage. India’s strong network of clinical laboratories, research institutions, and academic centers is contributing to increased consumption of laboratory reagents. In addition, government initiatives promoting biotechnology development and the expansion of diagnostic services in urban and semi-urban areas are further propelling market growth. The availability of cost-effective solutions and increasing domestic production of laboratory reagents are also enhancing market accessibility across the country.

Coating Buffers Market Share

The Coating Buffers industry is primarily led by well-established companies, including:

- Thermo Fisher Scientific Inc. (U.S.)

- Merck & Co., Inc. (U.S.)

- Bio-Techne Corporation (U.S.)

- Abcam Limited (U.K.)

- Agilent Technologies, Inc. (U.S.)

- Sigma-Aldrich Co. LLC (U.S.)

- Bio-Rad Laboratories, Inc. (U.S.)

- PerkinElmer, Inc. (U.S.)

- Danaher Corporation (U.S.)

- GE Healthcare (U.S.)

- Tecan Group Ltd. (Switzerland)

- Promega Corporation (U.S.)

- Lonza (Switzerland)

- Cytiva (U.S.)

- Rockland Immunochemicals, Inc. (U.S.)

- Abnova Corporation (Taiwan)

- Cayman Chemical Company (U.S.)

- R&D Systems, Inc. (U.S.)

What are the Recent Developments in Global Coating Buffers Market?

- In January 2025, Merck KGaA (MilliporeSigma in the U.S. and Canada) continued to expand its portfolio of life science reagents, including coating buffers used in immunoassays and diagnostic workflows. These buffer solutions are designed to ensure consistent surface coating, high reproducibility, and compatibility with automated laboratory systems. The company’s ongoing developments highlight its focus on supporting advancements in biotechnology and pharmaceutical research

- In September 2024, Abcam plc strengthened its immunoassay product portfolio by offering optimized coating and blocking buffer solutions tailored for ELISA and related applications. These reagents are developed to support high-quality assay performance by improving antigen binding efficiency and reducing background noise. The initiative reflects Abcam’s commitment to providing comprehensive tools for life science research and diagnostics

- In March 2023, Thermo Fisher Scientific, a leading life sciences company, expanded its portfolio of immunoassay reagents with ready-to-use coating buffer solutions designed to enhance ELISA workflow efficiency and reproducibility. These buffers are optimized to support high-throughput screening and standardized laboratory protocols, enabling researchers to achieve consistent antigen or antibody immobilization on microplates

- In November 2022, CANDOR Bioscience GmbH, a specialist in immunoassay reagents, introduced advanced coating buffer formulations aimed at minimizing non-specific binding in ELISA applications. The innovation improves assay sensitivity and reliability by ensuring more stable and uniform protein adsorption on assay surfaces. This development supports laboratories in achieving higher precision in diagnostic and research experiments

- In June 2021, Bio-Techne Corporation expanded its reagent offerings through its R&D Systems brand by enhancing its immunoassay buffer solutions, including coating buffers used in ELISA workflows. These solutions are designed to improve assay performance, reproducibility, and ease of use in both research and clinical laboratories. The expansion aligns with the company’s strategy to support advanced bioanalytical applications

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.