Global Corrosion Inhibitor Market

Размер рынка в млрд долларов США

CAGR :

%

USD

9.76 Billion

USD

13.87 Billion

2025

2033

USD

9.76 Billion

USD

13.87 Billion

2025

2033

| 2026 –2033 | |

| USD 9.76 Billion | |

| USD 13.87 Billion | |

| % | |

|

Global Corrosion Inhibitors Market Segmentation, By Product (Organic and Inorganic), Application (Water-Based and Solvent/Oil-Based), End-Use Industry (Power Generation, Oil and Gas, Chemical Processing, Metal Processing, and Others), Corrosive Agent (Oxygen, Hydrogen Sulfide, and Carbon Dioxide), Corrosion Type (Uniform or General Corrosion, Galvanic Corrosion, Localized Corrosion, Stress Corrosion Cracking (SCC), and Erosion Corrosion), Inhibitor Type (Passivating Inhibitors, Volatile Inhibitors, Cathodic Inhibitors, Anodic Inhibitors, Mixed Inhibitors, Synergistic Inhibitors, Precipitation Inhibitors, Green Corrosion Inhibitors, and Adsorption Action Inhibitors) - Industry Trends and Forecast to 2033

Что такое коррозионные ингибиторы размера рынка и темпов роста

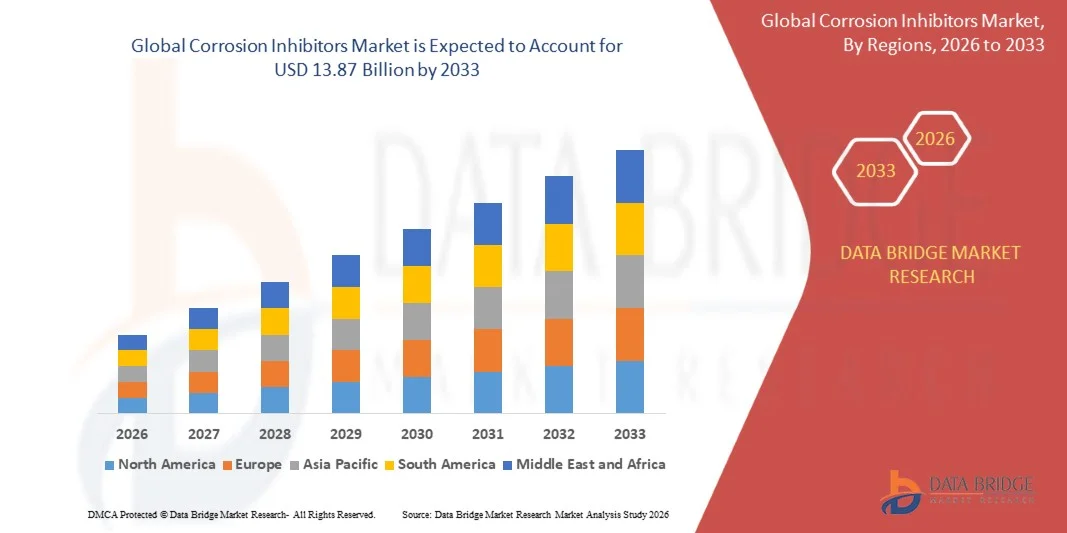

- Согласно анализу Data Bridge Market Research, размер мирового рынка ингибиторов коррозии был оценен как9,76 млрд долларов в 2025 годуОжидается, что он достигнет$13,87 млрд к 2033 году, вCAGR 4,50%в течение прогнозируемого периода

- Рост рынка в значительной степени обусловлен растущим спросом на защиту активов и операционную эффективность в таких отраслях, как нефть и газ, производство электроэнергии и химическая переработка, где коррозия приводит к значительным финансовым потерям и рискам безопасности.

- Кроме того, растущие инвестиции в развитие инфраструктуры, старение промышленного оборудования и необходимость минимизации затрат на техническое обслуживание создают ингибиторы коррозии в качестве важных решений для продления срока службы оборудования и обеспечения надежности процесса. Эти факторы ускоряют внедрение ингибиторов коррозии, тем самым значительно стимулируя рост рынка.

Размер рынка и прогноз:

- Глобальная рыночная стоимость (2025):9,76 млрд. долларов США

- Ожидаемая рыночная стоимость (2033):$13,87 млрд.

- Прогноз CAGR (2026–2033):4.50%

Как анализируются ингибиторы коррозии

- Ингибиторы коррозии представляют собой химические вещества, которые при добавлении в небольших концентрациях эффективно уменьшают или предотвращают коррозию металлов путем формирования защитных пленок или изменения электрохимических реакций в агрессивных средах. Эти ингибиторы широко используются вСистемы очистки водытрубопроводы, котлы, системы охлаждения и промышленные процессоры для повышения долговечности и производительности

- Растущий спрос на ингибиторы коррозии в первую очередь обусловлен быстрой индустриализацией, увеличением воздействия металлической инфраструктуры на суровые условия окружающей среды и строгими правилами, направленными на обеспечение безопасности и соблюдения экологических требований, что приводит к принятию передовых решений по защите от коррозии.

- Азиатско-Тихоокеанский регион доминирует на рынке ингибиторов коррозии с долей 37,7%в 2025 году в связи с быстрой индустриализацией, расширением нефтегазовой инфраструктуры, а также ростом производства электроэнергии и обработки металлов

- Ожидается, что Северная Америка станет самым быстрорастущим регионом в мире.Рынок ингибиторов коррозиив течение прогнозируемого периода в связи с ростом спроса на ингибиторы коррозии в нефте- и газопроводах, электроэнергетике и химической промышленности

- Органический сегмент доминировал на рынке с долей рынка 76,1% в 2025 году, благодаря его эффективности в формировании защитных пленок на металлических поверхностях и совместимости с системами на водной и масляной основе. Органические ингибиторы широко предпочтительны из-за их способности минимизировать воздействие на окружающую среду, обеспечить долгосрочную защиту от коррозии и повысить эффективность работы в промышленных приложениях.

Как сегментируются ингибиторы коррозии

|

Атрибуты |

Коррозионные ингибиторы Key Market Insights |

|

Сегменты покрыты |

|

|

Страны, охваченные |

Северная Америка

Европа

Азиатско-Тихоокеанский регион

Ближний Восток и Африка

Южная Америка

|

|

Ключевые игроки рынка |

|

|

Рыночные возможности |

|

|

Информационные наборы данных с добавленной стоимостью |

В дополнение к информации о рыночных сценариях, таких как рыночная стоимость, темпы роста, сегментация, географическое покрытие и основные игроки, рыночные отчеты, курируемые Data Bridge Market Research, также включают анализ экспорта импорта, обзор производственных мощностей, анализ потребления продукции, анализ ценового тренда, сценарий изменения климата, анализ цепочки поставок, анализ цепочки создания стоимости, обзор сырья / расходных материалов, критерии выбора поставщиков, анализ PESTLE, анализ Porter и нормативную базу. |

Каковы тенденции рынка, препятствующие коррозии

Растущий переход к экологически чистым и экологически чистым ингибиторам коррозии

- Значительной тенденцией на рынке ингибиторов коррозии является растущий сдвиг в сторону экологически чистых и зеленых рецептур ингибиторов, обусловленный строгими экологическими нормами и растущим промышленным акцентом на устойчивость. Этот переход повышает роль биоингибиторов и ингибиторов низкой токсичности в качестве основных решений для снижения воздействия на окружающую среду при сохранении эффективной защиты от коррозии в различных отраслях промышленности.

- Например, BASF SE и Akzo Nobel N.V. разрабатывают экологически чистые ингибиторы коррозии и покрытия, которые соответствуют мировым экологическим стандартам, обеспечивая при этом высокую производительность в промышленных применениях. Эти решения поддерживают отрасли в достижении нормативного соответствия и минимизации опасных химических выбросов.

- Такие отрасли, как нефтегазоочистка и водоочистка, все чаще используют зеленые ингибиторы для снижения экологического следа операций при сохранении целостности оборудования. Эта тенденция усиливает спрос на устойчивые формулы, которые обеспечивают как эффективность работы, так и экологическую безопасность.

- Растущий акцент на правилах очистки и сброса сточных вод поощряет использование биоразлагаемых и нетоксичных ингибиторов коррозии в промышленных процессах. Это ускоряет инновации в зеленой химии и расширяет область применения экологически чистых ингибиторов.

- Производители инвестируют в исследования и разработки для создания высокоэффективных зеленых ингибиторов, которые могут конкурировать с традиционными химическими составами в суровых условиях эксплуатации. Это способствует прогрессу в технологиях разработки и повышению конкурентоспособности продукции.

- Повышение осведомленности о воздействии на окружающую среду и долгосрочной устойчивости способствует внедрению ингибиторов зеленой коррозии в глобальных отраслях. Эта тенденция формирует рынок к более чистым технологиям и постоянному внедрению инноваций в устойчивые решения для защиты от коррозии.

Что такое коррозионные ингибиторы динамики рынка

водитель

Растущий спрос на защиту от коррозии в промышленной инфраструктуре

- Растущая потребность в защите критически важной промышленной инфраструктуры, такой как трубопроводы, резервуары для хранения и технологическое оборудование от коррозии, является основным фактором для рынка ингибиторов коррозии. Коррозия приводит к значительным финансовым потерям, простоям в работе и рискам безопасности, побуждая отрасли инвестировать в эффективные решения по профилактике.

- Например, Ecolab через свое подразделение Nalco Water предоставляет решения для ингибиторов коррозии для нефте- и газопроводов и промышленных систем водоснабжения, помогая снизить затраты на техническое обслуживание и повысить эффективность эксплуатации. Эти решения позволяют отраслям продлить срок службы активов и обеспечить бесперебойную работу

- Быстрая индустриализация и расширение таких секторов, как нефть и газ, производство электроэнергии и химическая переработка, увеличивают воздействие металлической инфраструктуры на суровые условия. Это стимулирует спрос на передовые ингибиторы коррозии, которые могут выдерживать экстремальные температуры, давления и химические условия.

- Инфраструктура старения в развитых странах еще больше повышает потребность в решениях для защиты от коррозии для предотвращения сбоев и дорогостоящих замен. Отрасли отдают приоритет стратегиям профилактического обслуживания, поддерживаемым эффективными технологиями ингибиторов.

- Постоянная потребность в повышении эксплуатационной надежности, снижении затрат на техническое обслуживание и обеспечении соответствия требованиям безопасности усиливает этот драйвер. Этот устойчивый спрос на эффективные решения для защиты от коррозии вносит значительный вклад в общий рост рынка.

Сдержанность/вызов

«Колебание цен на сырье и экологические ограничения»

- Рынок ингибиторов коррозии сталкивается с проблемами из-за колебаний цен на сырье, особенно на специальные химикаты и сырье, используемые в рецептурах ингибиторов. Эти изменения влияют на производственные затраты и создают ценовую неопределенность для производителей, работающих на конкурентных рынках.

- Например, Solvay и Kemira сталкиваются с давлением затрат из-за волатильности химического сырья, необходимого для производства ингибиторов коррозии, что влияет на общую рентабельность и стабильность цепочки поставок. Эти колебания затрудняют поддержание согласованных стратегий ценообразования.

- Строгие экологические нормы, регулирующие использование и удаление химических ингибиторов, повышают требования к соблюдению требований для производителей. Компании должны инвестировать в переформулирование продуктов в соответствии с нормативными стандартами, что увеличивает сложность и стоимость операций.

- Переход от традиционных ингибиторов к экологически чистым альтернативам требует значительных инвестиций в исследования и разработки. Этот сдвиг может замедлить коммерциализацию продукта и создать барьеры для мелких игроков рынка.

- Совокупное влияние волатильности затрат и регуляторного давления создает значительные проблемы для участников рынка. Эти ограничения заставляют компании внедрять инновации и эффективно управлять затратами для поддержания конкурентоспособности на рынке ингибиторов коррозии.

Что такое рынок ингибиторов коррозии

Рынок сегментирован на основе продукта, применения, конечного использования промышленности, коррозионного агента, типа коррозии и типа ингибитора.

• По продукту

На основе продукта рынок ингибиторов коррозии сегментирован на органические и неорганические ингибиторы. Органический сегмент доминировал на крупнейшем рынке с долей выручки 76,1% в 2025 году, что обусловлено его эффективностью в формировании защитных пленок на металлических поверхностях и совместимостью с системами на водной и нефтяной основе. Органические ингибиторы широко предпочтительны из-за их способности минимизировать воздействие на окружающую среду, обеспечить долгосрочную защиту от коррозии и повысить эффективность работы в промышленных применениях. Отрасли часто выбирают органические типы для критического оборудования в химической обработке и нефтегазовых операциях из-за их доказанной производительности и соответствия нормативным требованиям. Универсальность органических ингибиторов в различных агрессивных средах еще больше усиливает их присутствие на рынке.

Ожидается, что в неорганическом сегменте будут наблюдаться самые быстрые темпы роста с 2026 по 2033 год, чему способствуют технологические достижения и растущий спрос на тяжелые промышленные приложения. Например, такие компании, как BASF, используют неорганические ингибиторы для высокотемпературных сред и с высоким давлением при производстве электроэнергии и обработке металлов. Неорганические типы предпочитают за их экономическую эффективность, стабильность и высокую производительность против определенных коррозионных агентов, таких как кислород и углекислый газ. Расширение исследований в области экологически чистых неорганических составов еще больше ускоряет внедрение на развивающихся рынках.

• Подача заявки

На основе применения рынок ингибиторов коррозии сегментирован на ингибиторы на водной основе и на основе растворителя / масла. Сегмент на водной основе занимал самую большую долю рынка в 2025 году, чему способствовало растущее предпочтение экологически чистых и низкотоксичных решений в промышленных секторах. Ингибиторы на водной основе обеспечивают эффективную защиту в трубопроводах, системах охлаждения и технологических схемах водоснабжения, обеспечивая соблюдение нормативных требований и уменьшая воздействие на окружающую среду. Они широко используются в производстве электроэнергии и химической промышленности из-за простоты использования, безопасной обработки и совместимости с различными металлическими подложками. Растущее внимание к устойчивым промышленным операциям усиливает спрос на ингибиторы коррозии на водной основе во всем мире.

Ожидается, что сегмент, основанный на растворителях и маслах, будет иметь самые высокие темпы роста с 2026 по 2033 год, чему способствуют его превосходные показатели в экстремальных условиях. Например, AkzoNobel предоставляет ингибиторы на масляной основе для нефте- и газопроводов высокого давления, где системы на водной основе менее эффективны. Ингибиторы на основе растворителя / масла особенно ценятся за их способность проникать через металлические поверхности, образовывать прочные защитные пленки и противостоять высокотемпературной коррозии. Рост индустриализации и расширение нефтегазовых операций в странах с развивающейся экономикой способствуют росту этого сегмента.

• Промышленность конечного использования

На основе отрасли конечного использования рынок сегментирован на производство электроэнергии, нефти и газа, химическую обработку, обработку металлов и другие. Сегмент нефти и газа доминировал на крупнейшей доле рынка в 2025 году, что обусловлено критической необходимостью защиты трубопроводов, резервуаров для хранения и морской инфраструктуры от коррозионных агентов, таких как сероводород и углекислый газ. Компании отдают приоритет ингибиторам коррозии в нефтегазовых операциях, чтобы сократить время простоя, минимизировать затраты на техническое обслуживание и продлить срок службы активов. Растущее внимание к глубоководным и морским исследованиям еще больше усиливает спрос на высокоэффективные ингибиторы в этом секторе.

Ожидается, что в сегменте производства электроэнергии будут наблюдаться самые быстрые темпы роста с 2026 по 2033 год, чему способствует увеличение инвестиций в тепловые и атомные электростанции. Например, ChemTreat поставляет ингибиторы, которые повышают долговечность котельных и систем охлаждения воды на электростанциях. Приложения для выработки электроэнергии требуют ингибиторов, способных выдерживать высокие температуры, высокое давление и различные химические составы воды, что способствует внедрению передовых решений для защиты от коррозии. Рост спроса на электроэнергию и модернизация стареющих электростанций усиливают рост этого сегмента.

• Коррозионный агент

На основе коррозионного агента рынок сегментирован на кислород, сероводород и углекислый газ. Сегмент кислорода доминировал на крупнейшей доле рынка в 2025 году из-за широкого распространения кислорода в промышленных процессах и его высокой реактивности с металлами, что привело к ржавчине и масштабированию. Кислородная коррозия особенно важна в системах водоснабжения и пара, что делает ингибиторы против кислорода необходимыми для минимизации эксплуатационных сбоев. Сильный спрос сегмента обусловлен отраслями конечного использования, стремящимися снизить затраты на техническое обслуживание и увеличить срок службы оборудования.

Ожидается, что в сегменте сероводорода будут наблюдаться самые быстрые темпы роста с 2026 по 2033 год, обусловленные его коррозионным воздействием в нефтегазовой и химической промышленности. Например, Schlumberger предоставляет ингибиторы, нацеленные на коррозию сероводорода в кислых газопроводах и нефтеперерабатывающих установках. Сульфид водорода ускоряет локализованную коррозию, делая специализированные ингибиторы необходимыми для безопасности и защиты активов. Расширение разведки месторождений в регионах с высоким содержанием сульфида поддерживает рост в этом сегменте.

• По типу коррозии

На основе типа коррозии рынок сегментирован на однородную или общую коррозию, гальваническую коррозию, локализованную коррозию, коррозионное растрескивание под давлением (SCC) и эрозионную коррозию. Унифицированный или общий сегмент коррозии доминировал на крупнейшей доле рынка в 2025 году, так как он происходит в большинстве промышленных процессов и затрагивает широкий спектр металлов. Ингибиторы для равномерной коррозии имеют решающее значение для трубопроводов, резервуаров и технологического оборудования для предотвращения постепенной потери материала и поддержания операционной эффективности. Сильный спрос возникает в отраслях, которые ищут надежные решения для защиты от коррозии широкого спектра действия.

Ожидается, что в сегменте коррозионного растрескивания под напряжением (SCC) будут наблюдаться самые быстрые темпы роста с 2026 по 2033 год, обусловленные растущей потребностью в защите высокопрочных сплавов и критической инфраструктуры. Например, NACE International выделяет ингибиторы для SCC в ядерном и химическом оборудовании. SCC очень опасен, так как может привести к внезапным катастрофическим сбоям, увеличивая принятие передовых ингибиторов. Рост высокопроизводительных промышленных приложений и строгие правила безопасности еще больше ускоряют этот сегмент.

• Тип ингибитора

На основе типа ингибиторов рынок сегментирован на пассивирующие ингибиторы, летучие ингибиторы, катодные ингибиторы, анодные ингибиторы, смешанные ингибиторы, синергетические ингибиторы, ингибиторы осаждения, ингибиторы зеленой коррозии и ингибиторы адсорбционного действия. Сегмент смешанных ингибиторов доминировал на крупнейшей доле рынка в 2025 году из-за их двойного механизма, обеспечивающего как анодную, так и катодную защиту, что делает их высокоэффективными в различных приложениях. Отрасли промышленности предпочитают смешанные ингибиторы для критически важной инфраструктуры и технологических систем, требующих надежной защиты широкого спектра действия. Их способность минимизировать затраты на техническое обслуживание и продлить срок службы оборудования укрепляет рынок во всем мире.

Ожидается, что в сегменте ингибиторов зеленой коррозии будут наблюдаться самые быстрые темпы роста с 2026 по 2033 год, чему способствует усиление внимания регулирующих органов к экологически чистым решениям и целям устойчивого развития. Например, AkzoNobel и BASF ввели биоингибиторы для очистки воды и промышленных процессов. Зеленые ингибиторы снижают воздействие на окружающую среду, соответствуют строгим нормам выбросов и получают предпочтение в странах с развивающейся экономикой. Повышение осведомленности об устойчивой практике и технологических достижениях способствует быстрому внедрению этого сегмента.

В каком регионе находится наибольшая доля рынка ингибиторов коррозии

- Азиатско-Тихоокеанский регион доминировал на рынке ингибиторов коррозии с самой большой долей доходов 37,7% в 2025 году, что обусловлено быстрой индустриализацией, расширением нефтегазовой инфраструктуры и ростом производства электроэнергии и обработки металлов.

- Экономически эффективная производственная база региона, увеличение инвестиций в химическую переработку и сильное присутствие заводов по производству ингибиторов ускоряют расширение рынка.

- Наличие квалифицированной рабочей силы, благоприятное государственное регулирование и растущее внедрение передовых решений по защите от коррозии в промышленных секторах способствуют увеличению потребления ингибиторов коррозии.

Китайская коррозия препятствует пониманию рынка

Китай занимал самую большую долю на рынке ингибиторов коррозии в Азиатско-Тихоокеанском регионе в 2025 году благодаря своей обширной промышленной базе, объемным нефтегазовым операциям и сильным производственным возможностям в химической обработке. Поддерживающая политика правительства страны в области промышленного роста в сочетании с растущим спросом на защиту от коррозии в трубопроводах, электростанциях и обработке металлов являются основными факторами роста. Спрос также подкрепляется экспортом продуктов, ингибирующих коррозию, и продолжающимися инвестициями в высокопроизводительные промышленные химикаты.

Индийская коррозия препятствует пониманию рынка

Индия является свидетелем самого быстрого роста в Азиатско-Тихоокеанском регионе, подпитываемого расширением нефтегазовой инфраструктуры, увеличением мощностей по производству электроэнергии и растущими инициативами по модернизации промышленности. Правительственные инициативы, продвигающие Make in India и самостоятельность в химическом и промышленном производстве, усиливают спрос на ингибиторы коррозии. Кроме того, рост химической обработки, производства металлов и промышленного применения в нисходящем направлении стимулирует устойчивое расширение рынка.

Европейские коррозионные ингибиторы рынка

Европейский рынок ингибиторов коррозии неуклонно расширяется, чему способствуют строгие нормативные рамки, акцент на устойчивость и растущее внедрение высокоэффективных промышленных химикатов. Регион уделяет большое внимание соблюдению экологических норм, стандартов безопасности и передовых химических составов, особенно в нефтегазовом, энергетическом и металлоперерабатывающем секторах. Расширение использования ингибиторов коррозии в защитных покрытиях и промышленных водоочистных сооружениях способствует дальнейшему росту рынка.

Немецкая коррозия препятствует пониманию рынка

Рынок Германии обусловлен ее лидерством в химической обработке, высокоточным производством и ориентированной на экспорт промышленной инфраструктурой. В стране налажены научно-исследовательские сети и партнерские отношения между академическими учреждениями и промышленными игроками, что способствует постоянным инновациям в технологиях защиты от коррозии. Спрос особенно высок для ингибиторов, используемых на электростанциях, химических нефтеперерабатывающих заводах и в высокоценных приложениях для обработки металлов.

Коррозия в Великобритании препятствует пониманию рынка

Рынок Великобритании поддерживается зрелым промышленным сектором, уделяя все больше внимания устойчивости и экологическим нормам, а также растущему внедрению передовых решений для защиты от коррозии. С ростом внимания к исследованиям, промышленно-академическому сотрудничеству и локализованному производству специальных ингибиторов, Великобритания продолжает играть значительную роль на высокоценных промышленных химических рынках.

Коррозия в Северной Америке препятствует пониманию рынка

Прогнозируется, что Северная Америка будет расти самыми быстрыми темпами с 2026 по 2033 год, что обусловлено растущим спросом на ингибиторы коррозии в нефте- и газопроводах, производстве электроэнергии и химической промышленности. Упор на промышленную безопасность, технологические достижения в области защитных химических веществ и растущее внедрение экологически чистых ингибиторов повышают спрос. Кроме того, сокращение масштабов химического производства и сотрудничество между промышленными и химическими игроками способствуют расширению рынка.

Американские коррозионные ингибиторы Market Insight

На долю США приходится наибольшая доля на рынке Северной Америки в 2025 году, подкрепленная обширной нефтегазовой инфраструктурой, мощными возможностями исследований и разработок и передовыми химическими производственными мощностями. Акцент страны на промышленной безопасности, устойчивости и соблюдении нормативных требований способствует принятию высокоэффективных ингибиторов коррозии. Присутствие крупных игроков и хорошо зарекомендовавшая себя распределительная сеть еще больше укрепляют лидирующие позиции США в регионе.

Что такое доля рынка ингибиторов коррозии

Индустрия ингибиторов коррозии в основном возглавляется хорошо зарекомендовавшими себя компаниями, в том числе:

- Advance Products & Systems, LLC.

- Akzo Nobel N.V. (Нидерланды)

- Air Products and Chemicals, Inc. (США)

- Champion Technology Services, Inc. (США)

- ICL (Израиль)

- СУЭЗ (Франция)

- Daubert Cromwell, Inc. (США)

- Dai-ichi India Pvt Ltd (Индия)

- Сольвей (Бельгия)

- ChemTreat, Inc. (США)

- Aegion Corporation (США)

- Kurita Water Industries Ltd. (Япония)

- Кемира (Финляндия)

- Lubrizol Corporation (США)

- Milacron (США)

- Ecolab (США)

- QED Chemicals Ltd (Великобритания)

- Eastman Chemical Company (США)

- ШАВКОР (Канада)

- Ashland (США)

- Corrosion Technologies (США)

- BASF SE (Германия)

Каковы последние тенденции на мировом рынке ингибиторов коррозии

- В январе 2025 года BASF SE представила расширенный спектр биоингибиторов коррозии, предназначенных для промышленной очистки воды и нефтепромысловых применений, уделяя особое внимание снижению воздействия на окружающую среду при сохранении высокой производительности. Это развитие ускоряет переход к устойчивым решениям по защите от коррозии, поскольку отрасли все чаще отдают приоритет экологически чистым химическим веществам для удовлетворения ужесточения нормативных стандартов. Это также позволяет конечным пользователям достигать более длительного жизненного цикла оборудования и повышения эффективности системы при одновременном снижении воздействия на окружающую среду, тем самым укрепляя позиции BASF в зеленом сегменте ингибиторов.

- В октябре 2024 года Ecolab Inc. расширила свои цифровые решения по управлению водными ресурсами, интегрированные с технологиями ингибиторов коррозии, чтобы оптимизировать производительность промышленных систем. Это улучшение улучшает мониторинг в режиме реального времени, профилактическое обслуживание и точное химическое дозирование, что значительно снижает операционную неэффективность и химические потери. По мере того, как отрасли переходят на цифровизацию и интеллектуальную инфраструктуру, это новшество способствует более широкому внедрению интегрированных систем управления коррозией, повышению эффективности затрат и операционной надежности в таких секторах, как производство электроэнергии и производство.

- В августе 2024 года PPG Industries представила PPG PRIMERON Optimal, порошковый праймер, включающий оптимизированную технологию цинка для повышения коррозионной стойкости и долговечности покрытия. Это нововведение значительно улучшает долговечность покрытых поверхностей, особенно в суровых промышленных условиях, где высок риск коррозии. Снижая частоту технического обслуживания и продлевая срок службы активов, это способствует экономии затрат для конечных пользователей, одновременно увеличивая спрос на передовые системы покрытия, интегрированные с эффективными ингибиторами коррозии.

- В июне 2024 года Henkel AG & Co. KGaA запустила новую серию высокоэффективных ингибиторов коррозии, предназначенных для автомобильной и металлообрабатывающей промышленности, подчеркивая улучшенную защиту поверхности и совместимость с передовыми покрытиями. Эта разработка поддерживает производителей в достижении более высоких стандартов долговечности и производительности при минимизации простоев технического обслуживания и эксплуатационных сбоев. Это также способствует растущему спросу на многофункциональные ингибиторы, которые могут одновременно усиливать адгезию покрытия и коррозионную стойкость, усиливая инновации продукта в промышленных производственных средах.

- В марте 2023 года корпорация Cortec запустила VpCI-649 HP, ингибитор коррозии, сертифицированный по стандарту ANSI/NSF 61 для гидротестирования систем питьевой воды. Этот продукт расширяет область применения ингибиторов коррозии в инфраструктуре питьевой воды, устраняя критические требования безопасности и соответствия. Низкие требования к дозировке и минимальное воздействие на окружающую среду повышают эксплуатационную эффективность, устанавливая более высокие отраслевые стандарты для безопасных решений по предотвращению коррозии в чувствительных приложениях.

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.