Global Electrosurgical Instruments Market

Размер рынка в млрд долларов США

CAGR :

%

USD

7.11 Billion

USD

14.16 Billion

2025

2033

USD

7.11 Billion

USD

14.16 Billion

2025

2033

| 2026 –2033 | |

| USD 7.11 Billion | |

| USD 14.16 Billion | |

| % | |

|

Global Electrosurgical Instruments Market Segmentation, By Technology (Radio Frequency, Ultrasonic, and Molecular Resonance), Product (Bipolar, Monopolar and Pencil, Cables), Accessories (Patient Return Electrodes, Cords, Cables and Adapters, and Others), Surgery Type (Gynaecological, Cardiovascular, Neurosurgery, Cosmetic¸ Orthopaedic, Urologic¸ and General Surgery), End User (Hospitals, Laboratories, and Ambulatory Surgical Centers) - Industry Trends and Forecast to 2033

Electrosurgical Instruments Market Size

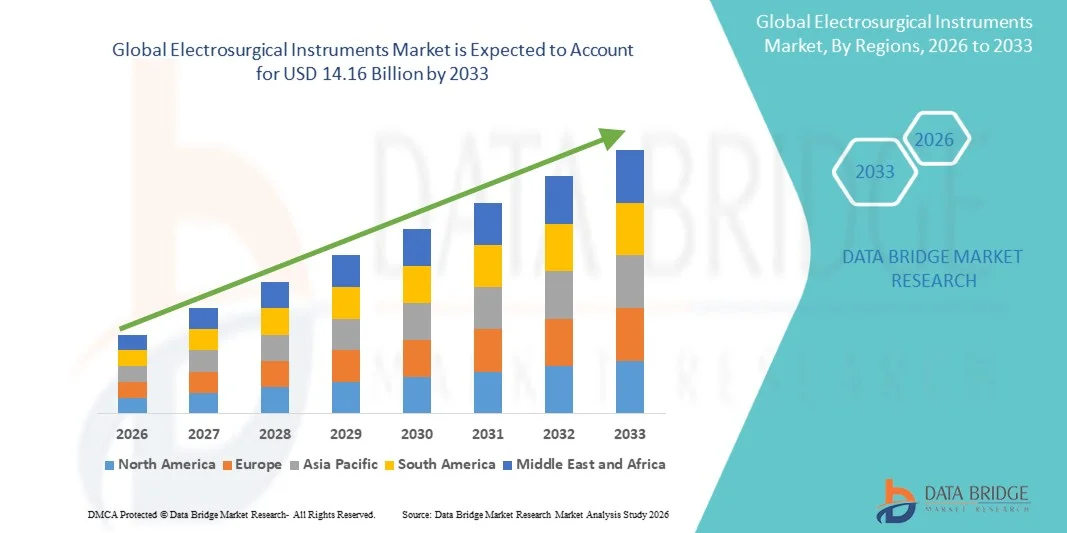

- The global electrosurgical instruments market size was valued at USD 7.11 billion in 2025 and is expected to reach USD 14.16 billion by 2033, at a CAGR of 9.00% during the forecast period

- The market growth is largely fueled by the increasing demand for minimally invasive surgical procedures and continuous technological advancements in energy-based surgical systems, leading to greater adoption of precision electrosurgical instruments across hospitals and ambulatory surgical centers

- Furthermore, rising prevalence of chronic diseases requiring surgical intervention, growing preference for procedures with reduced blood loss and faster recovery, and integration of advanced safety features such as controlled energy delivery and smoke evacuation systems are establishing electrosurgical instruments as essential tools in modern operating rooms. These converging factors are accelerating the uptake of Electrosurgical Instruments solutions, thereby significantly boosting the industry's growth

Electrosurgical Instruments Market Analysis

- Electrosurgical instruments, utilizing high-frequency electrical energy for cutting, coagulation, desiccation, and tissue sealing, are increasingly vital components of modern surgical procedures across general surgery, gynecology, cardiology, and oncology due to their precision, reduced intraoperative blood loss, and improved procedural efficiency

- The escalating demand for electrosurgical instruments is primarily fueled by the rising volume of minimally invasive surgeries, increasing prevalence of chronic diseases requiring surgical intervention, and continuous technological advancements in energy-based surgical platforms

- North America dominated the electrosurgical instruments market with the largest revenue share of 39.8% in 2025, characterized by advanced healthcare infrastructure, high surgical procedure volumes, favorable reimbursement policies, and strong presence of leading medical device manufacturers, with the U.S. experiencing substantial growth in adoption of advanced bipolar and vessel-sealing technologies

- Asia-Pacific is expected to be the fastest-growing region in the electrosurgical instruments market during the forecast period, projected to register a CAGR of 10.7%, due to expanding hospital infrastructure, increasing healthcare expenditure, rising medical tourism, and growing adoption of minimally invasive surgical techniques

- The patient return electrodes segment dominated with a revenue share of 44.1% in 2025, driven by their critical role in ensuring safe current return during electrosurgical procedures

Report Scope and Electrosurgical Instruments Market Segmentation

|

Attributes |

Electrosurgical Instruments Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Medtronic (Ireland) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Electrosurgical Instruments Market Trends

“Advancements in Energy-Based Surgical Devices and Minimally Invasive Procedures”

- A significant and accelerating trend in the global Electrosurgical Instruments market is the increasing development and adoption of energy-based surgical devices designed for precision, efficiency, and minimally invasive procedures. Hospitals and surgical centers are prioritizing devices that reduce operative time, minimize blood loss, and improve patient outcomes

- For instance, companies such as Ethicon (Johnson & Johnson) and Medtronic have launched advanced bipolar and ultrasonic electrosurgical instruments that enable surgeons to perform delicate procedures with improved hemostasis and reduced collateral tissue damage

- These devices are increasingly integrated with multifunctional generators and ergonomic handpieces, allowing for better control during gynecological, cardiovascular, and neurosurgical interventions

- The growing focus on minimally invasive and outpatient surgeries is driving demand for compact, versatile electrosurgical devices that can be used across multiple surgical specialties. In addition, the need for faster recovery, shorter hospital stays, and reduced postoperative complications is encouraging healthcare providers to adopt next-generation instruments

- Market trends also include the expansion of multifunctional instruments capable of performing cutting, coagulation, and vessel sealing in a single device, reducing instrument exchange and operating room time

- The rising adoption of these advanced instruments in emerging economies, supported by increasing surgical volumes and hospital modernization programs, further amplifies the growth trend

Electrosurgical Instruments Market Dynamics

Driver

“Rising Surgical Procedures and Growing Healthcare Infrastructure”

- The increasing number of surgical procedures globally, coupled with expanding healthcare infrastructure, is a major driver for the Electrosurgical Instruments market. Growing patient awareness, rising prevalence of chronic diseases, and the shift toward hospital-based and outpatient surgeries contribute to this demand

- For instance, in 2025, Medtronic introduced its Harmonic ultrasonic devices in multiple Asian and European markets to meet the rising demand for minimally invasive gynecological and general surgeries

- Similarly, Bovie Medical expanded its product line of bipolar and monopolar devices to hospitals in North America to address increasing cardiac and neurosurgical procedures. These initiatives by leading companies are expected to support robust market growth over the forecast period

- Furthermore, the adoption of minimally invasive surgeries, which require precise and efficient energy-based instruments, is rising rapidly in orthopedic, cardiovascular, and urologic procedures

- Increasing government investments in healthcare infrastructure, modern operating rooms, and surgical training programs also facilitate market expansion

- The convenience, reduced operative time, and enhanced safety offered by advanced electrosurgical instruments are further driving their adoption across hospitals, ambulatory surgical centers, and specialty clinics globally

Restraint/Challenge

“High Cost of Advanced Devices and Need for Skilled Personnel”

- The high initial cost of advanced electrosurgical instruments, including generators, handpieces, and accessory sets, poses a significant challenge to market adoption, particularly in developing regions or smaller clinics with budget constraints

- For instance, premium instruments such as Ethicon’s advanced vessel sealing devices or Medtronic’s ultrasonic multifunctional handpieces often come with high acquisition and maintenance costs, making hospitals cautious in procurement

- In addition, specialized training is required for effective use, and lack of skilled surgical staff in certain regions can limit deployment

- Moreover, frequent maintenance, calibration, and the need for compatible accessories such as cords, cables, and electrodes contribute to ongoing operational expenses

- While the prices of some entry-level electrosurgical devices are gradually decreasing, the perceived premium for advanced multifunctional systems can still restrict their penetration in cost-sensitive markets

- Addressing these challenges through affordable product variations, targeted training programs, and local support infrastructure will be critical for sustaining long-term market growth

Electrosurgical Instruments Market Scope

The market is segmented on the basis of technology, product, accessories, surgery type, and end user.

• By Technology

On the basis of technology, the Electrosurgical Instruments market is segmented into radio frequency, ultrasonic, and molecular resonance. The radio frequency segment dominated the largest market revenue share of 41.8% in 2025, driven by its widespread adoption across multiple surgical procedures, including gynecological, cardiovascular, and general surgeries. RF technology is valued for precise tissue cutting, minimal thermal damage, and predictable hemostasis. Hospitals prefer RF-based devices for their proven clinical efficiency and versatility. Rising prevalence of minimally invasive surgeries globally further fuels demand. Technological innovations enhancing energy delivery and safety features support adoption. Surgeons increasingly rely on RF instruments for outpatient and inpatient procedures. Expansion of surgical centers in emerging economies strengthens market penetration. Integration with advanced monitoring systems improves procedural accuracy. Regulatory approvals for next-generation RF devices accelerate growth. RF instruments offer reduced operative time and faster patient recovery, contributing to segment dominance.

The molecular resonance segment is projected to register the fastest CAGR of 9.5% from 2026 to 2033, owing to rising interest in advanced, minimally invasive surgical technologies. Molecular resonance offers precise tissue interaction with reduced collateral damage. Its adoption is growing in complex neurosurgeries and oncological procedures. Technological refinements improve energy efficiency and procedural safety. The segment benefits from increasing investments in high-end surgical devices by hospitals. Growing awareness about innovative surgical solutions supports growth. Molecular resonance is gaining traction in cosmetic and orthopedic surgeries. Surgeons value its accuracy for delicate tissue manipulation. Expansion of medical research in molecular energy applications drives innovation pipelines. Favorable reimbursement policies for advanced surgical techniques further accelerate growth.

• By Product

On the basis of product, the market is segmented into bipolar, monopolar and pencil, and cables. The bipolar segment held the largest market share of 38.6% in 2025, due to its enhanced precision and minimal current spread, reducing the risk of collateral tissue injury. Bipolar devices are extensively used in neurosurgery, gynecological, and urological procedures. Hospitals and surgical centers favor them for complex cases requiring high safety margins. Their compatibility with advanced electrosurgical units strengthens adoption. Continuous innovations in instrument ergonomics and energy modulation improve procedural outcomes. Rising number of surgical interventions globally drives demand. Regulatory approvals for new bipolar technologies encourage market expansion. The segment benefits from growing preference for minimally invasive and outpatient surgeries. Ongoing training programs for surgeons enhance familiarity and adoption.

The monopolar and pencil segment is expected to witness the fastest CAGR of 10.2% from 2026 to 2033, fueled by its wide applicability across general, cardiovascular, and orthopedic surgeries. Monopolar devices offer versatility and cost-efficiency. Increasing hospital infrastructure in developing economies supports segment growth. Advances in pencil-style devices improve precision and handling. Surgeons appreciate the convenience and ease of integration with existing electrosurgical generators. Growing awareness of operative safety and energy-efficient devices further boosts demand. Hospitals prefer monopolar solutions for routine and emergency procedures. The segment benefits from rising adoption in ambulatory surgical centers. Market expansion is also supported by increasing surgical case volumes worldwide.

• By Accessories

On the basis of accessories, the market is segmented into patient return electrodes, cords, cables and adapters, and others. The patient return electrodes segment dominated with a revenue share of 44.1% in 2025, driven by their critical role in ensuring safe current return during electrosurgical procedures. They are essential for minimizing patient burns and enhancing overall procedure safety. Hospitals prioritize high-quality electrodes with advanced sensing technologies. Increasing surgical volumes globally support steady adoption. Technological advancements in adhesive and reusable electrodes enhance clinical efficiency. Regulatory approvals for innovative electrode designs accelerate growth. Expanding hospital infrastructure in emerging regions contributes to adoption. Surgeons prefer electrodes that are compatible with multiple electrosurgical units. Continuous education on safe energy delivery promotes segment growth.

The cords, cables, and adapters segment is projected to grow at the fastest CAGR of 9.8% from 2026 to 2033, driven by rising demand for versatile and durable connections between instruments and generators. Increasing preference for modular and multifunctional accessories boosts segment expansion. Surgeons and hospitals adopt high-quality cords to reduce operational errors and downtime. Technological refinements improve durability and reduce interference. Expanding surgical interventions worldwide fuel accessory demand. Hospitals invest in high-performance adapters for advanced electrosurgical systems. The growth is also supported by increased adoption in ambulatory surgical centers.

• By Surgery Type

On the basis of surgery type, the market is segmented into gynecological, cardiovascular, neurosurgery, cosmetic, orthopedic, urologic, and general surgery. The general surgery segment accounted for the largest share of 36.5% in 2025, due to the wide variety of procedures performed and the consistent requirement for electrosurgical precision. Electrosurgical instruments reduce operative time and blood loss, supporting widespread adoption. Hospitals and clinics favor devices that ensure reliable performance across multiple procedures. Rising incidence of gastrointestinal and abdominal surgeries globally supports growth. Technological improvements in energy modulation enhance safety. Surgeons increasingly adopt electrosurgical tools for minimally invasive operations. Growth is also fueled by expanding surgical infrastructure in developing economies.

The neurosurgery segment is expected to witness the fastest CAGR of 10.7% from 2026 to 2033, driven by the growing number of neurological procedures requiring precise energy delivery and minimal tissue damage. Increasing prevalence of brain and spinal disorders globally fuels segment expansion. Technological advancements in low-thermal devices enhance surgical safety. Hospitals and specialized centers are adopting neurosurgery-specific instruments to improve outcomes. Rising research initiatives in neurological surgery accelerate innovation. The segment benefits from training programs that familiarize surgeons with advanced energy devices. Minimally invasive approaches in neurosurgery further support adoption.

• By End User

On the basis of end user, the market is segmented into hospitals, laboratories, and ambulatory surgical centers. The hospitals segment dominated with a revenue share of 62.4% in 2025, driven by the high number of inpatient and complex surgical procedures performed. Hospitals invest in comprehensive electrosurgical systems to support multiple departments. Regulatory approvals and safety standards increase trust in hospital-grade devices. Growing adoption of minimally invasive techniques in hospitals boosts demand. Hospitals prefer devices offering durability, precision, and energy efficiency. Rising surgical volumes and infrastructure expansion in emerging regions support growth. Continuous innovations in device technology encourage adoption.

The ambulatory surgical centers segment is expected to grow at the fastest CAGR of 11.3% from 2026 to 2033, fueled by the increasing shift toward outpatient procedures for cost-efficiency and reduced hospital stays. The rise in day-care surgeries globally accelerates demand. Electrosurgical instruments offer precision, minimal tissue damage, and faster recovery, making them ideal for outpatient settings. Expansion of ASCs in developed and developing markets supports segment growth. Growing patient preference for outpatient treatment drives adoption. The segment benefits from compact, portable, and multifunctional instrument designs. Technological integration with monitoring systems enhances safety and procedural success.

Electrosurgical Instruments Market Regional Analysis

- North America dominated the electrosurgical instruments market with the largest revenue share of 39.8% in 2025, characterized by advanced healthcare infrastructure, high surgical procedure volumes, favorable reimbursement policies, and the strong presence of leading medical device manufacturers. Growing demand for minimally invasive and laparoscopic procedures, coupled with innovations in energy-based surgical devices, is fueling market expansion

- Favorable reimbursement policies and high healthcare expenditure support widespread adoption across public and private hospitals. Increasing surgeon awareness and training on modern electrosurgical technologies further bolster market penetration. North America remains the leading hub for innovation in electrosurgical solutions, including multifunctional handpieces and automated vessel-sealing systems

- Rising prevalence of chronic diseases requiring surgical intervention is expected to sustain demand for electrosurgical instruments. Research collaborations and hospital partnerships promote clinical adoption and product development in the region. Patient preference for minimally invasive procedures drives investments in advanced electrosurgical technologies. Overall, the region’s robust healthcare ecosystem and high technology penetration underpin its dominant market position.

U.S. Electrosurgical Instruments Market Insight

The U.S. electrosurgical instruments market captured the largest revenue share within North America in 2025, fueled by substantial procedural volumes across surgical specialties. Hospitals and ambulatory surgical centers are increasingly adopting advanced bipolar and vessel-sealing technologies to reduce operative time and improve patient outcomes. Rising awareness of minimally invasive surgical approaches, combined with training programs for surgeons, enhances adoption rates. High healthcare expenditure and favorable reimbursement frameworks enable hospitals to invest in cutting-edge instruments. Continuous innovation by leading medical device manufacturers, including ergonomic designs and multifunctional capabilities, further strengthens market growth.

Europe Electrosurgical Instruments Market Insight

The Europe electrosurgical instruments market is projected to grow steadily at a notable CAGR during the forecast period, supported by increasing hospital infrastructure upgrades and adoption of energy-based surgical devices. Key countries such as Germany, France, and the U.K. are investing in modern operating room technologies. Rising demand for minimally invasive procedures and laparoscopic surgeries drives instrument adoption. Favorable healthcare policies, reimbursement coverage, and an emphasis on surgical safety enhance market growth. Technological advancements in electrosurgical instruments, such as vessel-sealing systems and hybrid devices, strengthen the region’s competitive landscape.

U.K. Electrosurgical Instruments Market Insight

The U.K. electrosurgical instruments market is expected to expand at a healthy CAGR during the forecast period. Growth is driven by increasing adoption of minimally invasive surgeries, rising awareness among surgeons, and investments in operating room modernization. Hospitals prioritize advanced energy-based instruments to improve precision and reduce intraoperative complications. Favorable reimbursement policies and increasing surgical procedure volumes further support adoption. Rising healthcare expenditure and technological collaboration with device manufacturers stimulate market expansion.

Germany Electrosurgical Instruments Market Insight

The Germany electrosurgical instruments market is anticipated to grow at a considerable CAGR, driven by high surgical volumes and widespread use of advanced bipolar and vessel-sealing technologies. The country’s strong healthcare infrastructure and emphasis on patient safety encourage adoption of energy-based surgical instruments. Hospitals are increasingly investing in minimally invasive surgical solutions to reduce recovery times. Collaborative initiatives between hospitals and medical device companies promote clinical integration of cutting-edge electrosurgical instruments.

Asia-Pacific Electrosurgical Instruments Market Insight

The Asia-Pacific electrosurgical instruments market is expected to be the fastest-growing region, projected to register a CAGR of 10.7% during the forecast period. Growth is driven by expanding hospital infrastructure, increasing healthcare expenditure, rising medical tourism, and growing adoption of minimally invasive surgical techniques in countries such as China, India, and Japan. Rapid urbanization and government healthcare initiatives support procedural growth. Rising awareness of advanced surgical technologies and investments by leading medical device manufacturers enhance market penetration. The region is witnessing increasing adoption of bipolar, monopolar, and vessel-sealing electrosurgical instruments.

Japan Electrosurgical Instruments Market Insight

The Japan electrosurgical instruments market is gaining momentum due to growing demand for minimally invasive and laparoscopic surgeries. High procedural volumes, rising healthcare investments, and focus on surgical precision drive adoption. Hospitals increasingly integrate advanced energy-based devices into operating rooms. Technological innovation, including multifunctional handpieces and improved vessel-sealing systems, supports market growth. Government support for healthcare infrastructure and skilled surgical workforce further accelerates adoption.

China Electrosurgical Instruments Market Insight

The China electrosurgical instruments market accounted for the largest share in Asia-Pacific in 2025, fueled by expanding hospital networks, rising medical tourism, and increasing procedural volumes. Adoption of advanced bipolar, monopolar, and vessel-sealing technologies is growing rapidly. Investments in minimally invasive surgery, combined with rising healthcare expenditure, support instrument uptake. Leading domestic and international manufacturers are expanding distribution channels to meet increasing demand. Government initiatives to improve surgical care infrastructure further strengthen market growth in the country.

Electrosurgical Instruments Market Share

The Electrosurgical Instruments industry is primarily led by well-established companies, including:

• Medtronic (Ireland)

• B. Braun S.E. (Germany)

• Johnson & Johnson (U.S.)

• CONMED Corporation (U.S.)

• Smith & Nephew (U.K.)

• ERBE Elektromedizin GmbH (Germany)

• Olympus Corporation (Japan)

• Covidien (U.S.)

• Abbot Laboratories (U.S.)

• Richard Wolf GmbH (Germany)

• Arthrex, Inc. (U.S.)

• Hospira, Inc. (U.S.)

• Stryker Corporation (U.S.)

• KaVo Kerr (U.S.)

• TriMedx (U.S.)

• Octopus Medical (U.S.)

• Mettler Electronics (U.S.)

• GYRUS ACMI (U.S.)

• Erbe Elektromedizin (Germany)

• Hologic, Inc. (U.S.)

Latest Developments in Global Electrosurgical Instruments Market

- In June 2023, Olympus Corporation announced the market availability of a new electrosurgical generator system designed to enhance surgical performance for conditions such as non‑muscle‑invasive bladder cancer (NMIBC) and benign prostatic hyperplasia (BPH). The system provides surgeons with flexible resection loops, band electrodes, and vaporization instruments aimed at improving procedural efficiency and outcomes in urology and related fields

- In March 2024, Medtronic plc announced the launch of its next‑generation Valleylab FT10 Electrosurgical Energy Platform, a state‑of‑the‑art surgical energy generator featuring smart tissue‑sensing technology that automatically adjusts power delivery in real time depending on tissue response, improving precision and minimizing thermal injury during cutting and coagulation in various surgical specialties. This innovation underlines Medtronic’s commitment to advancing electrosurgical safety and performance in minimally invasive and open surgeries

- In March 2025, Johnson & Johnson MedTech (a division of Johnson & Johnson) launched its DUALTO Energy System, an advanced electrosurgical energy platform cleared by the U.S. FDA that integrates multiple energy modalities — including monopolar, bipolar, ultrasonic, and advanced bipolar capabilities — into a unified system. Designed for both open and minimally invasive procedures, DUALTO also integrates with the Polyphonic Fleet software for device management and is engineered for future use with the company’s OTTAVA™ surgical robot

- In April 2025, Erbe Elektromedizin GmbH unveiled the VIO 3n electrosurgical generator series, representing the latest generation of energy platforms tailored for a range of medical specialties with improved control, safety, and versatility. The enhanced system targets precision in both monopolar and bipolar applications across surgical disciplines such as general surgery, gynecology, and gastroenterology, supporting growing demand for adaptable electrosurgical solutions

- In April 2025, Innoblative Designs, Inc. received U.S. FDA approval of its IDE (Investigational Device Exemption) for the company’s SIRA™ RFA electrosurgical device, a novel radiofrequency ablation system designed for use as an adjunct in breast‑conserving surgery (lumpectomy) to treat residual tumor margins and potentially reduce reoperation rates. The approval cleared the way for U.S. feasibility trials to assess safety and effectiveness in patients

- In September 2025, Medtronic expanded its electrosurgical offerings in India with the launch of two advanced electrosurgical generators, the Valleylab FT10 Electrosurgical Generator (VLFT10FXGEN) and the Valleylab FT10 Vessel Sealing Generator (VLFT10LSGEN). These platforms incorporate TissueFect sensing technology that adapts energy delivery based on tissue type, improving precision and reducing procedural risks during surgical cutting, coagulation, and vessel sealing

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.