Global Embolic Protection Devices Market

Размер рынка в млрд долларов США

CAGR :

%

USD

1.34 Billion

USD

2.60 Billion

2025

2033

USD

1.34 Billion

USD

2.60 Billion

2025

2033

| 2026 –2033 | |

| USD 1.34 Billion | |

| USD 2.60 Billion | |

| % | |

|

Global Embolic Protection Devices Market Segmentation, By Product (Distal Filter Devices, Distal Occlusion Devices, and Proximal Occlusion Devices), Material (Nitinol and Polyurethane), Usage (Disposable Devices and Re-Usable Devices), Application (Cardiovascular Diseases, Neurovascular Diseases and Peripheral Vascular Diseases), Indication (Percutaneous Coronary, Carotid Artery, Saphenous Vein Graft Diseases, Transcather Aortic Valve Replacement, and Others), End Users (Hospital, Ambulatory Surgical Centers, and Others)- Industry Trends and Forecast to 2033

Embolic Protection Devices Market Size

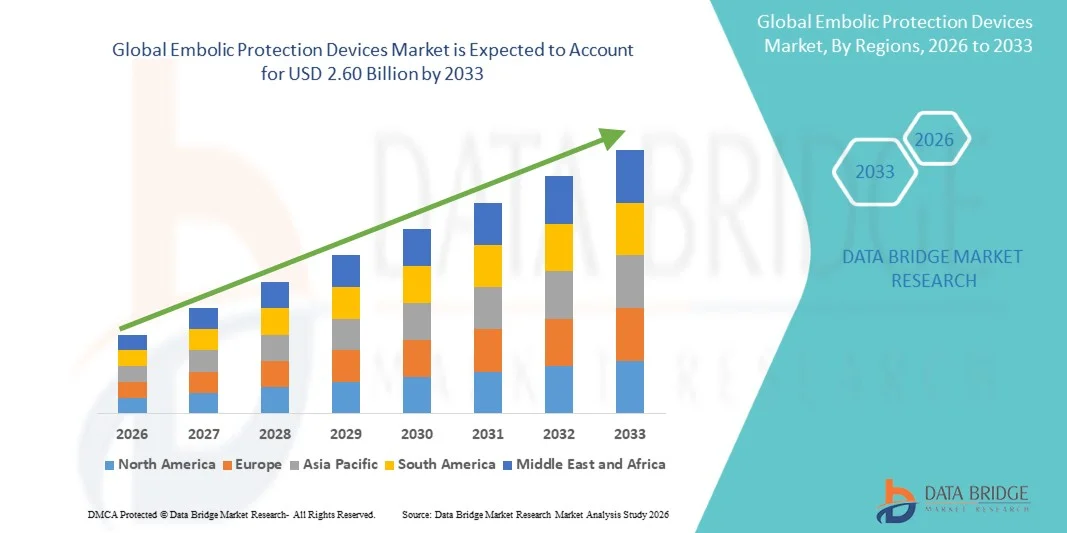

- The global embolic protection devices market size was valued at USD 1.34 billion in 2025 and is expected to reach USD 2.60 billion by 2033, at a CAGR of 8.65% during the forecast period

- The market growth is largely fueled by the rising prevalence of cardiovascular diseases such as coronary artery disease and peripheral artery disease, along with the increasing number of minimally invasive procedures including angioplasty and transcatheter interventions, leading to greater adoption of embolic protection solutions in clinical practice

- Furthermore, growing physician awareness regarding procedure-related complications such as distal embolization, coupled with increasing demand for advanced, reliable, and patient-safe interventional devices, is establishing embolic protection devices as a critical component in modern cardiovascular procedures. These converging factors are accelerating the adoption of embolic protection technologies, thereby significantly boosting the market’s growth trajectory

Embolic Protection Devices Market Analysis

- Embolic protection devices, designed to capture and remove debris generated during interventional cardiovascular and vascular procedures, are increasingly vital components in modern minimally invasive treatments across both hospital and ambulatory surgical settings due to their ability to reduce the risk of procedure-related complications and improve patient outcomes

- The escalating demand for embolic protection devices is primarily fueled by the growing global burden of cardiovascular conditions such as coronary artery disease and stroke, increasing adoption of minimally invasive procedures, and a rising emphasis on patient safety and procedural efficacy among healthcare providers

- North America dominated the embolic protection devices market with the largest revenue share of 41.2% in 2025, characterized by advanced healthcare infrastructure, high adoption of interventional cardiology procedures, and a strong presence of key market players, with the United States witnessing substantial growth driven by favorable reimbursement policies and continuous technological advancements in vascular devices

- Asia-Pacific is expected to be the fastest growing region in the embolic protection devices market during the forecast period due to increasing healthcare expenditure, rising awareness of cardiovascular diseases, and improving access to advanced medical technologies in emerging economies such as China and India

- Distal filter devices segment dominated the embolic protection devices market with a market share of 45.6% in 2025, driven by their widespread use in carotid artery stenting and their effectiveness in capturing embolic debris while maintaining continuous blood flow during procedures

Report Scope and Embolic Protection Devices Market Segmentation

|

Attributes |

Embolic Protection Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Embolic Protection Devices Market Trends

“Rising Integration with Advanced Interventional and Imaging Technologies”

- A significant and accelerating trend in the global embolic protection devices market is the increasing integration with advanced interventional cardiology techniques and imaging technologies such as intravascular ultrasound and real-time guidance systems, which is significantly enhancing procedural precision and patient safety

- For instance, embolic protection systems used during transcatheter aortic valve replacement procedures are increasingly being integrated with imaging guidance to ensure optimal placement and effective debris capture, improving clinical outcomes in high-risk patients

- Technological advancements in embolic protection devices enable improved capture efficiency, reduced crossing profiles, and enhanced deliverability in complex anatomies. For instance, newer distal filter devices are designed to maintain continuous blood flow while effectively trapping embolic debris, reducing the risk of complications such as stroke during procedures

- The seamless integration of embolic protection devices with minimally invasive cardiovascular interventions facilitates improved procedural success rates and reduced recovery times. Through enhanced compatibility with catheter-based systems, clinicians can perform complex interventions with greater confidence and safety, creating a more efficient treatment ecosystem

- This trend towards more precise, efficient, and patient-centric interventional solutions is fundamentally reshaping clinical practices in cardiovascular care. Consequently, companies such as Boston Scientific are developing next-generation embolic protection devices with improved flexibility, enhanced capture mechanisms, and compatibility with advanced interventional platforms

- The demand for embolic protection devices that offer high procedural efficiency and seamless integration with modern interventional technologies is growing rapidly across hospitals and specialty cardiac centers, as healthcare providers increasingly prioritize improved patient outcomes and reduced complication rates

- The development of miniaturized and low-profile embolic protection devices suitable for smaller vessels and complex anatomies is enabling expansion into previously challenging procedures, creating new clinical applications and market opportunities

Embolic Protection Devices Market Dynamics

Driver

“Growing Demand Due to Rising Cardiovascular Disease Burden and Minimally Invasive Procedures”

- The increasing prevalence of cardiovascular diseases and the growing adoption of minimally invasive interventional procedures are significant drivers for the heightened demand for embolic protection devices

- For instance, in March 2025, Medtronic highlighted advancements in embolic protection solutions designed for complex cardiovascular interventions, focusing on improving procedural safety and reducing embolic complications, which are expected to drive market growth during the forecast period

- As healthcare providers become more focused on reducing procedure-related complications, embolic protection devices offer advanced features such as efficient debris capture and continuous blood flow maintenance, providing a critical advantage over procedures without protection systems

- Furthermore, the increasing adoption of minimally invasive techniques and the growing number of catheter-based interventions are making embolic protection devices an integral component of modern cardiovascular treatments, ensuring safer and more effective procedures

- The rising awareness regarding complications such as distal embolization, combined with the need for improved patient outcomes and reduced hospital stays, are key factors propelling the adoption of embolic protection devices in both developed and emerging healthcare markets. The trend towards technologically advanced interventional solutions and the increasing availability of skilled professionals further contribute to market growth

- Expansion of structural heart disease interventions, including transcatheter mitral and tricuspid valve procedures, is driving additional demand for embolic protection devices to prevent procedural embolic events

- Increasing collaborations between device manufacturers and hospitals to provide training and procedural support are enhancing clinician confidence, accelerating adoption, and supporting the market’s overall growth

Restraint/Challenge

“High Cost and Procedural Complexity Limiting Adoption”

- Concerns surrounding the high cost of embolic protection devices and the complexity associated with their use pose a significant challenge to broader market penetration. As these devices require specialized training and expertise, their adoption may be limited in certain healthcare settings

- For instance, the requirement for additional procedural steps and device costs during interventions has made some healthcare providers hesitant to adopt embolic protection devices, particularly in cost-sensitive markets

- Addressing these challenges through cost-effective product development, simplified device designs, and enhanced training programs is crucial for wider adoption. Companies such as Abbott Laboratories emphasize ease-of-use and improved device efficiency in their product innovations to encourage adoption among clinicians

- In addition, reimbursement limitations and variability across different regions can act as a barrier to adoption, particularly in developing economies where healthcare budgets are constrained. While advanced embolic protection systems offer significant clinical benefits, their higher cost compared to standard interventional tools can limit accessibility

- While healthcare investments are gradually increasing, the perceived cost burden and procedural complexity can still hinder widespread adoption, especially in facilities with limited resources or lower procedural volumes

- Overcoming these challenges through improved reimbursement frameworks, clinician training, and the development of more affordable and user-friendly embolic protection solutions will be vital for sustained market growth

- Limited awareness and adoption among smaller hospitals and clinics, especially in emerging regions, restricts market penetration and highlights the need for broader educational initiatives

- Stringent regulatory approvals and the need for clinical validation can delay product launches and increase development costs, posing additional challenges to market expansion

Embolic Protection Devices Market Scope

The market is segmented on the basis of product, material, usage, application, indication, and end user.

- By Product

On the basis of product, the embolic protection devices market is segmented into distal filter devices, distal occlusion devices, and proximal occlusion devices. Distal Filter Devices dominated the market with the largest revenue share of 45.6% in 2025, driven by their wide adoption in carotid artery stenting and percutaneous coronary interventions. These devices allow continuous blood flow while capturing embolic debris, reducing the risk of stroke and other procedure-related complications. Cardiologists often prefer distal filter devices for their ease of deployment, established clinical efficacy, and compatibility with multiple catheter-based interventions. The demand is further supported by extensive clinical studies demonstrating their effectiveness in preventing distal embolization. Hospitals and specialty cardiac centers invest heavily in distal filter devices for high-risk patients, and innovations such as low-profile filters and enhanced mesh designs are enhancing capture efficiency and procedural safety.

Proximal Occlusion Devices are anticipated to witness the fastest growth rate of 9.8% from 2026 to 2033, fueled by their increasing use in complex interventions such as transcatheter aortic valve replacement (TAVR) and saphenous vein graft procedures. Proximal occlusion devices temporarily halt blood flow upstream to prevent embolic events during high-risk procedures, providing enhanced safety in patients with complex anatomies. Their growing adoption is driven by rising awareness among interventional cardiologists regarding distal embolization risks in high-risk populations. Advancements in device flexibility, deliverability, and ease of use are encouraging hospitals and surgical centers to integrate these systems into standard procedural protocols.

- By Material

On the basis of material, the embolic protection devices market is segmented into nitinol and polyurethane. Nitinol dominated the market with the largest share in 2025 due to its excellent shape-memory properties, flexibility, and biocompatibility. Nitinol devices allow easier navigation through tortuous vessels and ensure precise deployment, which is critical in neurovascular and coronary interventions. Cardiologists prefer nitinol-based devices because they conform to complex vessel anatomies without causing trauma or obstruction, thereby improving procedural outcomes. Furthermore, nitinol’s durability and resistance to fatigue make it suitable for both distal and proximal embolic protection applications. Continuous material innovations are enhancing device performance, increasing clinician confidence, and expanding its adoption in high-volume cardiac centers.

Polyurethane is expected to witness the fastest growth during the forecast period, driven by its cost-effectiveness and increasing use in disposable embolic protection devices. Polyurethane-based filters and occlusion devices are lightweight, flexible, and compatible with various delivery systems, making them attractive for both hospitals and ambulatory surgical centers. In addition, polyurethane devices support scalable manufacturing for emerging markets where affordability is a key factor, encouraging wider adoption. The material’s versatility also allows integration with innovative designs that enhance debris capture efficiency and procedural safety.

- By Usage

On the basis of usage, the market is segmented into disposable devices and reusable devices. Disposable Devices dominated the market with the largest revenue share of 52.3% in 2025, due to the growing preference for single-use devices that minimize infection risk and eliminate the need for sterilization between procedures. Hospitals increasingly rely on disposable embolic protection devices for high-risk interventions to ensure patient safety, procedural efficiency, and regulatory compliance. Clinicians value these devices for their consistent performance, ease of handling, and reduced maintenance requirements. The rising number of percutaneous coronary and carotid interventions is also contributing to the growing demand for disposable solutions in both developed and emerging markets.

Reusable Devices are expected to witness the fastest growth during the forecast period, driven by hospitals aiming to optimize procedural costs in high-volume centers. Reusable embolic protection devices can be sterilized and used across multiple procedures, offering cost advantages over disposable alternatives. Technological improvements in device durability, ease of cleaning, and safety compliance are further supporting the adoption of reusable systems. In addition, reusable devices are particularly attractive in emerging markets where healthcare providers balance cost efficiency with patient safety and clinical outcomes.

- By Application

On the basis of application, the embolic protection devices market is segmented into cardiovascular diseases, neurovascular diseases, and peripheral vascular diseases. Cardiovascular Diseases dominated the market with the largest share of 48.5% in 2025, driven by the high prevalence of coronary artery disease and increasing numbers of percutaneous coronary interventions. These devices are critical in preventing distal embolization during stenting and angioplasty procedures, reducing procedure-related complications such as myocardial infarction or stroke. Cardiologists rely on embolic protection devices for high-risk patients, particularly in complex lesion anatomies and saphenous vein graft interventions. Continuous technological advancements, such as smaller crossing profiles and improved capture efficiency, are further enhancing adoption in cardiovascular applications.

Neurovascular Diseases are expected to witness the fastest growth during the forecast period, driven by rising incidence of ischemic strokes and the increasing use of embolic protection devices during carotid artery stenting. The adoption of neurovascular protection systems is fueled by growing awareness among neurologists and interventional cardiologists regarding stroke prevention during high-risk neurovascular procedures. Miniaturized, low-profile devices designed for tortuous cerebral vessels are enabling broader clinical application, particularly in elderly and high-risk patients. Increasing hospital investments in neurointerventional facilities and government initiatives to reduce stroke-related morbidity and mortality are also contributing to rapid growth.

- By Indication

On the basis of indication, the embolic protection devices market is segmented into percutaneous coronary, carotid artery, saphenous vein graft diseases, transcatheter aortic valve replacement (TAVR), and others. Percutaneous Coronary dominated the market with the largest share of 44.7% in 2025, driven by the high volume of coronary interventions performed globally and the critical need to prevent distal embolization during these procedures. Cardiologists prefer embolic protection devices in percutaneous coronary interventions (PCI) involving saphenous vein grafts and complex lesions to reduce the risk of myocardial infarction and improve procedural outcomes. Continuous advancements in device design, such as improved crossing profiles and enhanced debris capture, are increasing adoption. The large patient pool, combined with favorable reimbursement policies in developed markets, further strengthens the dominance of this segment. For instance, high-risk PCI cases increasingly rely on distal filter devices to ensure patient safety and procedural efficacy.

Transcatheter Aortic Valve Replacement (TAVR) is expected to witness the fastest growth from 2026 to 2033, fueled by the rising prevalence of aortic stenosis and the increasing adoption of minimally invasive TAVR procedures, particularly in elderly patients. Embolic protection devices are crucial during TAVR to prevent cerebral embolization and stroke, making them an essential adjunct in high-risk interventions. Technological innovations such as compact, deliverable filters that can navigate tortuous vasculature are supporting rapid growth. The increasing number of structural heart programs in hospitals worldwide and clinical evidence demonstrating stroke reduction with embolic protection are further accelerating market adoption. For instance, hospitals in North America and Europe are increasingly implementing TAVR procedures with integrated embolic protection systems to improve patient outcomes.

- By End Users

On the basis of end users, the embolic protection devices market is segmented into hospitals, ambulatory surgical centers (ASCs), and others. Hospitals dominated the market with the largest share of 65.8% in 2025, due to the high volume of complex interventional procedures performed in these settings and the availability of advanced infrastructure. Hospitals prefer embolic protection devices for high-risk patients undergoing PCI, carotid stenting, and TAVR procedures, as these devices enhance procedural safety and clinical outcomes. The presence of skilled interventional cardiologists, robust procedural support systems, and access to cutting-edge imaging technologies further drives hospital adoption. For instance, tertiary cardiac centers in the U.S. and Europe extensively use distal filter and proximal occlusion devices in routine interventional practice. In addition, hospitals invest in training programs and technology upgrades to ensure optimal device usage and patient safety.

Ambulatory Surgical Centers (ASCs) are expected to witness the fastest growth during the forecast period, fueled by the rising trend of minimally invasive cardiovascular procedures being performed outside traditional hospital settings. ASCs offer cost-effective and efficient care for lower-risk patients while providing access to embolic protection devices for routine interventional procedures. The adoption of these devices in ASCs is supported by technological improvements that simplify deployment, reduce procedure time, and enhance safety. For instance, ASCs in emerging economies and developed regions are increasingly performing PCI and peripheral interventions with disposable distal filter devices, driving rapid segment growth. In addition, favorable regulatory frameworks and increasing patient preference for outpatient procedures contribute to the accelerated adoption of embolic protection devices in ASCs.

Embolic Protection Devices Market Regional Analysis

- North America dominated the embolic protection devices market with the largest revenue share of 41.2% in 2025, characterized by advanced healthcare infrastructure, high adoption of interventional cardiology procedures, and a strong presence of key market players

- Healthcare providers in the region highly prioritize patient safety and procedural efficacy, making embolic protection devices a standard component in high-risk interventions such as percutaneous coronary interventions (PCI), carotid artery stenting, and transcatheter aortic valve replacement (TAVR)

- This widespread adoption is further supported by favorable reimbursement policies, well-established hospital networks, and the presence of leading device manufacturers investing in continuous innovation and clinician training programs

U.S. Embolic Protection Devices Market Insight

The U.S. embolic protection devices market captured the largest revenue share of 79% in 2025 within North America, driven by the high prevalence of cardiovascular diseases and the increasing adoption of minimally invasive interventional procedures. Hospitals and specialty cardiac centers are prioritizing patient safety, making embolic protection devices a standard in percutaneous coronary interventions (PCI), carotid artery stenting, and transcatheter aortic valve replacement (TAVR). The growing focus on reducing procedure-related complications, combined with favorable reimbursement policies, advanced clinical infrastructure, and continuous innovation from leading manufacturers, further propels market expansion. Moreover, U.S. cardiologists are increasingly adopting next-generation devices with improved debris capture efficiency and low-profile designs, enhancing procedural outcomes and supporting broader adoption.

Europe Embolic Protection Devices Market Insight

The Europe embolic protection devices market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by a strong focus on cardiovascular disease management and an increasing number of interventional procedures. The adoption of embolic protection devices is fostered by well-equipped hospitals, early adoption of advanced interventional technologies, and growing awareness among cardiologists regarding procedural safety. Countries such as Germany, France, and Italy are witnessing increasing deployment in both new and complex cardiovascular procedures, supported by clinical evidence demonstrating reduced stroke and distal embolization risks. Furthermore, favorable healthcare policies and investments in cardiac care infrastructure are accelerating adoption across both hospital and ambulatory surgical settings.

U.K. Embolic Protection Devices Market Insight

The U.K. embolic protection devices market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the increasing number of percutaneous interventions and rising awareness of stroke and cardiovascular complication prevention. Hospitals and specialized cardiac centers are adopting embolic protection devices to reduce procedural risks during PCI and carotid interventions. The U.K.’s strong healthcare system, coupled with government initiatives to improve cardiovascular care and clinical outcomes, supports the growth of high-quality interventional devices. In addition, collaborations between device manufacturers and hospitals for training and procedural guidance are further stimulating market adoption.

Germany Embolic Protection Devices Market Insight

The Germany embolic protection devices market is expected to expand at a considerable CAGR during the forecast period, fueled by growing awareness of procedural safety and technological innovation in cardiovascular interventions. Germany’s well-developed hospital infrastructure and focus on advanced healthcare solutions promote the adoption of embolic protection devices, particularly for high-risk PCI and TAVR procedures. Clinical evidence demonstrating reduced distal embolization and stroke risk further encourages adoption among cardiologists. Integration with modern interventional platforms, emphasis on patient safety, and the presence of leading global and domestic device manufacturers contribute to steady market growth.

Asia-Pacific Embolic Protection Devices Market Insight

The Asia-Pacific embolic protection devices market is poised to grow at the fastest CAGR of 11.5% during the forecast period of 2026 to 2033, driven by rising cardiovascular disease prevalence, increasing healthcare expenditure, and expanding access to minimally invasive interventional procedures in countries such as China, India, and Japan. Government initiatives promoting advanced cardiac care, coupled with growing awareness among cardiologists regarding embolic protection, are encouraging adoption in hospitals and surgical centers. The emergence of regional manufacturing hubs for cardiovascular devices is improving accessibility and reducing costs, allowing broader utilization of embolic protection technologies. In addition, increasing procedural volumes and rising investments in cardiac infrastructure are propelling market growth across APAC.

Japan Embolic Protection Devices Market Insight

The Japan embolic protection devices market is gaining momentum due to the country’s advanced healthcare infrastructure, high prevalence of elderly patients with cardiovascular conditions, and rising demand for minimally invasive interventions. Japanese hospitals emphasize patient safety and reduced procedure-related complications, increasing reliance on embolic protection devices during PCI, carotid artery stenting, and TAVR procedures. The integration of these devices with imaging and catheter-based systems enhances procedural precision and clinical outcomes. Moreover, Japan’s aging population is likely to drive demand for safer and more efficient cardiovascular interventions in both hospital and outpatient settings, supporting market expansion.

India Embolic Protection Devices Market Insight

The India embolic protection devices market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to the country’s increasing burden of cardiovascular diseases, rapid urbanization, and improving healthcare infrastructure. Hospitals and specialty cardiac centers are adopting embolic protection devices to reduce distal embolization risks during PCI and TAVR procedures. The push towards establishing advanced cardiac care facilities, alongside the availability of cost-effective and locally manufactured devices, is accelerating market growth. In addition, increasing awareness among cardiologists and patients regarding procedural safety and improved clinical outcomes is driving widespread adoption in India’s residential and commercial healthcare settings.

Embolic Protection Devices Market Share

The Embolic Protection Devices industry is primarily led by well-established companies, including:

- Abbott (U.S.)

- Boston Scientific Corporation (U.S.)

- Medtronic (Ireland)

- Cardinal Health, Inc. (U.S.)

- Terumo Corporation (Japan)

- Contego Medical, LLC (U.S.)

- Cook. (U.S.)

- Cordis Corporation (U.S.)

- Edwards Lifesciences Corporation (U.S.)

- Emboline, Inc. (U.S.)

- InspireMD, Inc. (U.S.)

- Merit Medical Systems, Inc. (U.S.)

- MicroPort Scientific Corporation (China)

- Nipro Medical Corp. (Japan)

- Transverse Medical, Inc. (U.S.)

- W. L. Gore & Associates, Inc. (U.S.)

- Claret Medical, Inc. (U.S.)

- Innovative Cardiovascular Solutions, LLC (U.S.)

- Keystone Heart Ltd. (Switzerland)

- Allium Medical Solutions Ltd. (Israel)

What are the Recent Developments in Global Embolic Protection Devices Market?

- In October 2025, Emboline, Inc. announced completion of patient enrollment in its pivotal U.S. IDE clinical trial (ProtectH2H) evaluating the Emboliner® Embolic Protection Catheter in patients undergoing TAVR, underscoring the company’s advancement toward potential regulatory submission and expanded clinical evidence

- In March 2025, a major clinical study (BHF PROTECT‑TAVI) presented at the American College of Cardiology’s Annual Scientific Session revealed that a widely used cerebral embolic protection device did not significantly reduce stroke risk when used routinely during TAVR procedures, stimulating debate on clinical utility and design of future embolic protection technologies

- In October 2024, EMBLOK™ announced enrollment of the first 50 patients in its clinical trial for the Emblok™ Embolic Protection System, along with the appointment of a scientific and strategic advisory board to support the development of this next‑generation embolic protection device aimed at reducing stroke and other complications during TAVR

- In March 2024, Emboline, Inc. announced that the 100th patient had been treated in its Protect the Head to Head IDE trial of the Emboliner® embolic protection catheter, signifying progress in clinical evaluation of a device intended to capture embolic debris and reduce procedural stroke risk during transcatheter heart procedures

- In May 2023, Emboline, Inc. announced that the first patient was treated in the IDE clinical trial of its Emboliner® Full‑Body Embolic Protection Catheter designed to minimize stroke risk during transcatheter aortic valve replacement (TAVR), marking a key milestone in full‑body embolic protection research and paving the way for future safety data

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.