Asia Pacific Angioplasty Balloons Market

Market Size in USD Million

USD

758.66 Million

USD

1,087.17 Million

2025

2033

USD

758.66 Million

USD

1,087.17 Million

2025

2033

| 2026 - 2033 | |

| USD 758.66 Million | |

| USD 1,087.17 Million | |

| % | |

|

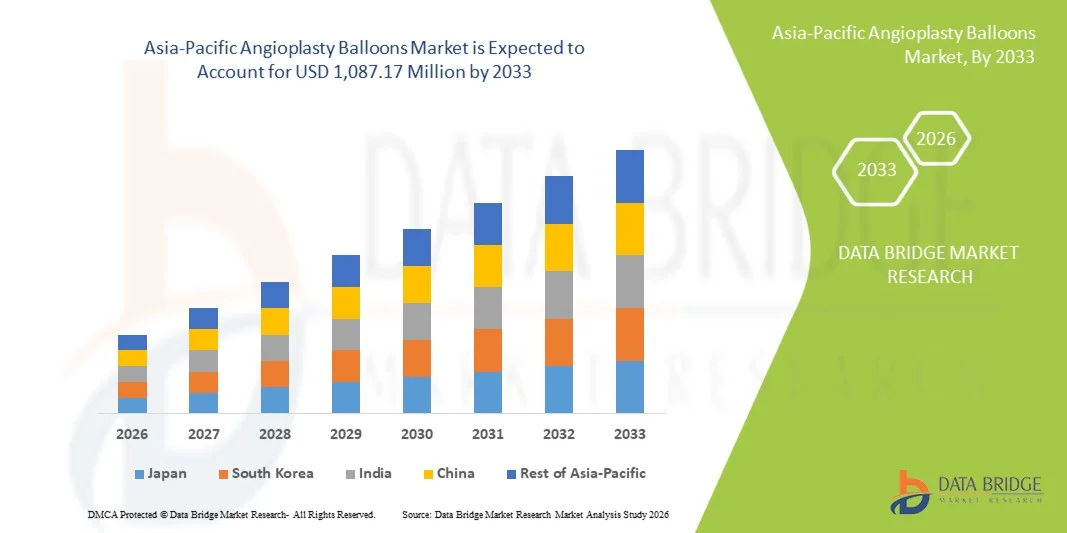

Asia-Pacific Angioplasty Balloons Market Size

- The Asia-Pacific angioplasty balloons market size was valued at USD 758.66 million in 2025 and is expected to reach USD 1,087.17 million by 2033, at a CAGR of 4.6% during the forecast period

- The market growth is largely fueled by the rising burden of cardiovascular disorders in the Asia‑Pacific region, technological advances in balloon catheter design, and improved access to advanced treatments in both developed and emerging economies

- Furthermore, growing awareness of early diagnosis and intervention, coupled with expanding healthcare expenditures and supportive government initiatives, is accelerating demand for angioplasty balloons as effective interventional devices, thereby significantly boosting industry growth

Asia-Pacific Angioplasty Balloons Market Analysis

- Angioplasty balloons, used in percutaneous coronary interventions to treat narrowed or blocked arteries, are increasingly vital components of modern cardiovascular care in both hospitals and specialized cardiac centers due to their minimally invasive nature, precision in dilation, and improved patient outcomes

- The escalating demand for angioplasty balloons is primarily fueled by the rising prevalence of cardiovascular diseases, increasing awareness of early intervention, and growing adoption of minimally invasive procedures over traditional surgeries

- Japan dominated the Asia‑Pacific angioplasty balloons market with the largest revenue share of 32.5% in 2025, characterized by advanced healthcare infrastructure, early adoption of innovative devices, and a strong presence of key industry players

- China is expected to be the fastest-growing country in the Asia‑Pacific angioplasty balloons market during the forecast period due to expanding healthcare infrastructure, increasing hospital investments, rising disposable incomes, and a growing patient population requiring cardiovascular interventions

- Drug-Coated Balloon (DCB) Angioplasty segment is expected to dominate the Asia‑Pacific angioplasty balloons market with a market share of 45.2%, driven by its proven efficacy in reducing restenosis rates, improving long-term outcomes, and increasing adoption in complex coronary and peripheral artery disease treatments

Report Scope and Asia-Pacific Angioplasty Balloons Market Segmentation

|

Attributes |

Asia-Pacific Angioplasty Balloons Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Asia-Pacific Angioplasty Balloons Market Trends

“Advancements in Drug-Coated and Specialty Balloons”

- A significant and accelerating trend in the Asia‑Pacific angioplasty balloons market is the rising adoption of drug-coated balloons (DCBs) and specialty balloons, which improve procedural outcomes and reduce restenosis rates

- For instance, the SeQuent Please Neo DCB has been increasingly adopted in Japan and China for treating in-stent restenosis and small vessel disease, offering improved efficacy over conventional balloons

- Innovations in balloon materials and coatings enable higher precision, enhanced deliverability, and reduced arterial injury, which are driving clinical preference among interventional cardiologists

- Integration with advanced imaging techniques, such as intravascular ultrasound (IVUS) and optical coherence tomography (OCT), facilitates optimized balloon sizing and placement, improving patient outcomes and procedural safety

- Rising adoption of minimally invasive procedures and outpatient cardiac interventions is encouraging hospitals to prefer angioplasty balloons over surgical alternatives

- This trend towards more advanced, targeted, and clinically effective balloons is fundamentally reshaping treatment approaches for coronary and peripheral artery disease in Asia‑Pacific

- The demand for balloons with improved clinical profiles and specialty functionalities is growing rapidly across hospitals and cardiac centers, as healthcare providers increasingly prioritize patient outcomes and procedural efficiency

Asia-Pacific Angioplasty Balloons Market Dynamics

Driver

“Rising Cardiovascular Disease Prevalence and Minimally Invasive Procedures”

- The increasing burden of cardiovascular diseases across Asia‑Pacific, coupled with growing awareness of early intervention, is a significant driver for the heightened demand for angioplasty balloons

- For instance, in 2025, Japan’s Ministry of Health reported rising rates of coronary artery disease, prompting hospitals to adopt advanced balloon technologies to improve patient outcomes

- Angioplasty balloons enable minimally invasive coronary and peripheral interventions, reducing hospitalization time and procedural risks compared with open-heart surgeries, driving clinical preference

- Expanding healthcare infrastructure, increasing investments in cardiac catheterization labs, and government initiatives to improve access to cardiovascular care are further boosting market growth

- The convenience of percutaneous procedures, higher patient acceptance, and improved recovery times are key factors propelling the adoption of angioplasty balloons in both established and emerging economies

- Rising healthcare insurance coverage and reimbursement schemes in countries such as South Korea and Singapore are supporting wider adoption of angioplasty balloons

- Growing physician training programs and workshops on advanced interventional cardiology techniques are improving familiarity and confidence in using drug-coated and specialty balloons

Restraint/Challenge

“High Device Costs and Regulatory Approval Hurdles”

- The relatively high cost of advanced angioplasty balloons, including drug-coated and specialty balloons, poses a challenge to widespread adoption, particularly in price-sensitive markets across Asia‑Pacific

- For instance, smaller hospitals in China and India may delay adoption of new DCBs due to budget constraints, limiting market penetration despite clinical advantages

- Stringent regulatory requirements and lengthy approval processes across multiple countries in the region can slow the introduction of innovative balloon technologies

- Addressing cost barriers through local manufacturing, strategic partnerships, and reimbursement support is crucial for broader adoption and market expansion

- Overcoming these challenges through pricing strategies, streamlined regulatory pathways, and clinician education on clinical benefits will be vital for sustained market growth

- Limited awareness among patients and some clinicians regarding the benefits of newer balloon technologies can delay adoption, especially in rural or smaller hospitals

- Competition from alternative devices, such as stents and atherectomy systems, may also restrain market growth in certain segments and applications

Asia-Pacific Angioplasty Balloons Market Scope

The market is segmented on the basis of type, material, balloon type, disease indication, and end user.

- By Type

On the basis of type, the Asia‑Pacific angioplasty balloons market is segmented into Plain Old Balloon Angioplasty (POBA), Drug-Coated Balloon (DCB) Angioplasty, Cutting Balloons, Scoring Balloons, and Stent Graft Balloon Catheters. The Drug-Coated Balloon (DCB) segment dominated the market with the largest revenue share of 45.2% in 2025, driven by its ability to reduce restenosis rates and improve long-term patient outcomes. Hospitals and cardiac centers in Japan, China, and South Korea increasingly prefer DCBs for coronary and peripheral interventions due to clinical evidence supporting their efficacy. DCBs are also being used in complex lesions and in-stent restenosis cases where conventional balloons may not be effective. Their growing adoption is further fueled by clinical guidelines recommending drug-eluting therapies for high-risk patients. Manufacturers are continuously innovating with improved coatings and delivery systems, enhancing procedural success rates. The combination of proven clinical benefits and growing cardiologist confidence makes DCBs the primary choice in Asia-Pacific interventional procedures.

The Plain Old Balloon Angioplasty (POBA) segment is expected to witness the fastest growth with a CAGR of 8.2% from 2026 to 2033, particularly in emerging markets such as India and Vietnam. POBA balloons are still widely used for initial interventions and smaller hospitals due to their cost-effectiveness and simplicity. Ongoing education programs and procedural training are increasing physician familiarity with POBA devices, while hospitals continue to expand capacity for interventional cardiology. The ease of use, quick procedural times, and accessibility in tier-2 cities support the adoption of POBA. Moreover, increasing peripheral angioplasty procedures in rural and semi-urban healthcare facilities are boosting POBA demand.

- By Material

On the basis of material, the market is segmented into nylon, polyurethane, silicone urethane co-polymers, and others. The Nylon segment dominated the market with a revenue share of 38.7% in 2025, due to its widespread availability, reliability, and proven clinical performance across multiple coronary and peripheral interventions. Nylon balloons offer predictable expansion properties, high burst pressure tolerance, and are suitable for both semi-compliant and non-compliant applications. Cardiologists in Japan and South Korea prefer nylon for standard procedures due to its cost-effectiveness and procedural safety. Manufacturers continue to supply enhanced nylon balloons with better coating compatibility for drug delivery. The strong clinical track record and established supply chains make nylon the most widely used balloon material in Asia‑Pacific.

The Polyurethane segment is expected to witness the fastest CAGR from 2026 to 2033 due to its superior flexibility, improved tracking ability in tortuous vessels, and compatibility with specialty drug coatings. Hospitals adopting advanced procedures increasingly choose polyurethane for complex lesion interventions. Its elasticity reduces arterial trauma and enhances procedural success. The rise in peripheral artery interventions, particularly in China and India, further supports polyurethane adoption. Continuous R&D on polyurethane balloons is expected to expand their use in high-risk patients and niche indications.

- By Balloon Type

On the basis of balloon type, the market is segmented into semi-compliant and non-compliant balloons. The Semi-Compliant segment dominated the Asia‑Pacific market in 2025 with a share of 51.4%, due to its versatility in expanding at varying pressures and suitability for a wide range of lesion types. Semi-compliant balloons are preferred for standard coronary interventions where some flexibility is needed to reduce arterial injury. Cardiologists rely on semi-compliant balloons for tortuous vessels and small arteries, making them highly adopted in Japan and South Korea. The combination of affordability, procedural safety, and availability in multiple diameters supports the segment’s dominance. Semi-compliant balloons are also often used in peripheral and renal artery angioplasty, increasing market penetration. Continuous innovation, such as low-profile designs, further enhances clinical adoption.

The Non-Compliant segment is expected to witness the fastest growth with a CAGR of 7.9% from 2026 to 2033 due to its precision in high-pressure dilations and use in complex lesions. Non-compliant balloons are essential for post-dilatation after stent placement and treating resistant or calcified lesions. Their predictable expansion helps reduce vessel injury and improve procedural outcomes. Increasing complex PCI procedures in China, India, and Australia drive demand. The segment also benefits from technological advancements in high-pressure resistant polymers and improved catheter design.

- By Disease Indication

On the basis of disease indication, the market is segmented into coronary angioplasty, venous angioplasty, carotid angioplasty, renal artery angioplasty, and peripheral angioplasty. The Coronary Angioplasty segment dominated the market with a revenue share of 58.6% in 2025, driven by the high prevalence of coronary artery disease in Asia‑Pacific countries such as Japan, China, and South Korea. Hospitals and specialized cardiac centers increasingly adopt angioplasty balloons as first-line treatment for arterial blockages. Coronary interventions benefit from both drug-coated and semi-compliant balloon technologies. Government initiatives promoting cardiovascular awareness and early intervention programs support market growth. Training programs and workshops for cardiologists further enhance adoption rates. Clinical evidence favoring minimally invasive approaches for coronary lesions ensures this segment remains dominant.

The Peripheral Angioplasty segment is expected to witness the fastest growth with a CAGR of 8.5% from 2026 to 2033 due to increasing prevalence of peripheral artery disease and rising adoption of minimally invasive treatments in India, China, and Southeast Asia. Peripheral interventions require specialized balloons such as scoring or drug-coated devices. Growing awareness about PAD among patients and clinicians, combined with expansion of cath labs in tier-2 cities, supports growth. Advancements in device flexibility and deliverability enable treatment of complex peripheral lesions.

- By End User

On the basis of end user, the market is segmented into cath labs, hospitals, specialty clinics, ambulatory surgery centers, and diagnostic centers. The Hospitals segment dominated the market with a share of 62.3% in 2025, owing to their comprehensive infrastructure, presence of experienced cardiologists, and ability to perform high-volume angioplasty procedures. Hospitals in Japan, China, and South Korea are equipped with state-of-the-art cath labs and offer both coronary and peripheral interventions. Hospitals prefer advanced balloons, including DCBs and non-compliant types, to treat complex cases. Government and private hospital initiatives supporting cardiac care further drive adoption. Hospitals also facilitate clinical trials, training, and R&D collaborations, consolidating their market dominance.

The Specialty Clinics segment is expected to witness the fastest growth with a CAGR of 9.1% from 2026 to 2033, particularly in emerging countries such as India and Vietnam, due to increasing investment in outpatient cardiac centers and minimally invasive procedures. Specialty clinics provide cost-effective, targeted interventions with shorter hospital stays. Expansion of diagnostic and treatment centers in urban areas supports higher procedure volumes. Adoption of advanced balloon technologies in these clinics is rising due to improved procedural efficiency and patient demand for less invasive treatments.

Asia-Pacific Angioplasty Balloons Market Regional Analysis

- Japan dominated the Asia‑Pacific angioplasty balloons market with the largest revenue share of 32.5% in 2025, characterized by advanced healthcare infrastructure, early adoption of innovative devices, and a strong presence of key industry players

- Cardiologists and hospitals in Japan highly value the clinical efficacy, procedural safety, and precision offered by drug-coated and specialty balloons, making them the preferred choice for both coronary and peripheral interventions

- This widespread adoption is further supported by supportive government healthcare initiatives, increasing investment in cardiac catheterization labs, and a technologically advanced medical ecosystem, establishing angioplasty balloons as a primary interventional tool for cardiovascular care in the country

The Japan Angioplasty Balloons Market Insight

The Japan angioplasty balloons market continues to expand due to its advanced healthcare system, widespread adoption of innovative balloon technologies, and strong clinical emphasis on cardiovascular interventions. Japanese hospitals and cath labs prioritize precision, safety, and patient outcomes, favoring drug-coated and specialty balloons for both coronary and peripheral artery procedures. Moreover, Japan’s aging population is likely to increase demand for minimally invasive treatments, including angioplasty balloons, across residential cardiac care centers and hospital settings. Continuous R&D and collaborations with global device manufacturers are also boosting adoption of the latest balloon technologies.

China Angioplasty Balloons Market Insight

The China angioplasty balloons market is expected to witness rapid growth due to increasing prevalence of coronary artery disease and peripheral vascular disorders, expanding hospital networks, and rising government support for minimally invasive interventions. Leading hospitals in urban centers are increasingly adopting drug-coated and non-compliant balloons for complex coronary and peripheral procedures. Patient awareness campaigns and the establishment of state-of-the-art cardiac catheterization labs are further boosting the adoption of advanced balloon technologies. The market is also benefiting from domestic production of balloons, reducing costs and improving accessibility in tier-2 and tier-3 cities.

India Angioplasty Balloons Market Insight

The India angioplasty balloons market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the rapid expansion of healthcare infrastructure, a growing patient population with cardiovascular conditions, and increased adoption of interventional cardiology procedures. Hospitals, specialty clinics, and diagnostic centers are increasingly deploying drug-coated and semi-compliant balloons for coronary and peripheral artery disease management. Government initiatives supporting smart hospitals, medical insurance coverage, and training programs for interventional cardiologists are key factors propelling market growth. Additionally, rising disposable incomes and increased awareness of minimally invasive procedures are encouraging wider adoption across urban and semi-urban regions.

Australia Angioplasty Balloons Market Insight

The Australia angioplasty balloons market is growing steadily, driven by advanced healthcare facilities, high awareness of cardiovascular health, and adoption of innovative balloon technologies in both public and private hospitals. The prevalence of coronary artery disease and government initiatives promoting early detection and treatment of heart conditions are fueling demand. Hospitals are increasingly using specialty balloons, including cutting and scoring types, for complex procedures, supporting market expansion. Furthermore, clinical collaborations and training programs for cardiologists enhance the adoption of advanced balloon technologies, reinforcing Australia’s role as a significant contributor to the regional market.

Asia-Pacific Angioplasty Balloons Market Share

The Asia-Pacific Angioplasty Balloons industry is primarily led by well-established companies, including:

- Abbott (U.S.)

- Boston Scientific Corporation (U.S.)

- Medtronic (Ireland)

- Terumo Corporation (Japan)

- Cook (U.S.)

- BIOTRONIK (Germany)

- MicroPort Scientific (China)

- Lepu Medical Technology (China)

- Nipro Medical Corporation (Japan)

- Philips (Netherlands)

- B. Braun SE (Germany)

- Stryker (U.S.)

- AngioDynamics, Inc. (U.S.)

- Hexacath (France)

- Jotec AG (Germany)

- Panmed US (U.S.)

- Terumo Aortic (Japan)

- Teleflex Medical (U.S.)

- Angioslide (Brazil)

- Atrium Medical (U.S.)

What are the Recent Developments in Asia-Pacific Angioplasty Balloons Market?

- In October 2025, three‑year follow‑up results from the REC‑CAGEFREE I multicenter randomized trial were presented at the Transcatheter Cardiovascular Therapeutics (TCT) meeting, evaluating paclitaxel‑coated balloon (DCB) angioplasty with rescue stenting versus up‑front sirolimus‑eluting stent implantation for de novo coronary artery lesions in China. The data showed that DCB angioplasty did not meet noninferiority criteria compared with traditional DES at three years, although outcomes continue to be monitored

- In June 2025, the Asia‑Pacific Consensus Group released its second consensus report outlining practical guidelines for drug‑coated balloon (DCB)‑based interventions in coronary artery disease, aimed at standardizing and expanding effective use of DCB therapies in real‑world clinical settings across Asia‑Pacific

- In January 2025, Concept Medical enrolled the first patient in the MAGICAL BTK IDE trial, a key clinical investigation testing its MagicTouch sirolimus‑coated balloon for below‑the‑knee peripheral artery disease (PAD), marking an important step toward expanding advanced balloon technology in clinical practice across Asia‑Pacific and beyond

- In July 2023, Boston Scientific Corporation received FDA approval for its Veritas™ Prime Plus Balloon Catheter, featuring a low‑profile design and improved pushability for complex lesions a development that often influences device adoption and regulatory strategies in Asia‑Pacific markets as global devices extend presence to these regions

- In June 2023, a research survey published in the Journal of Asian Pacific Society of Cardiology reported increasing awareness and use of drug‑coated balloons (DCBs) among interventional cardiologists across the Asia‑Pacific region. The study found that although usage varied by country, increased operator experience and expanding evidence of DCB effectiveness in specific lesion types (e.g., small‑vessel disease and high bleeding risk) were positively correlated with more frequent clinical adoption.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.