Global Gastric Cancer Diagnostics Market, By Product Type (Instruments, Reagents & Consumables, Services), Diagnostics Type (Confirmatory Test, Gastric Cancer Screening Tests/Physical Exam), Age Group (Adult, Pediatric, and Geriatrics), Disease Type (Intestinal Or Diffuse Adenocarcinoma, Carcinoid Tumor, Gastrointestinal Stromal Tumor (GIST), Gastric Lymphoma and Others), Stage (Stage 0, Stage I, Stage II, Stage III), Gender (Male and Female), Sample Type (Blood, Tissue, Urine, and Stool), End Users (Diagnostic Laboratories, Hospitals, Cancer Research Institutes, Oncology Specialty Clinics, and Others), Distribution Channel (Direct Tenders and Retail Sales) - Industry Trends and Forecast to 2030.

Gastric Cancer Diagnostics Market Analysis and Insights

The increase in the global geriatric population is driving the growth of the gastric cancer diagnostics industry. The prevalence of gastrointestinal tumors and lymphomas has also fueled the demand for gastric cancer diagnostics. The key market constraint is the need to lower the high prices associated with cancer diagnostic testing so that even developing countries may benefit from it.

Large numbers of market players are offering gastric cancer diagnostics products with innovations that pave the way for the growth of the global gastric cancer diagnostics market.

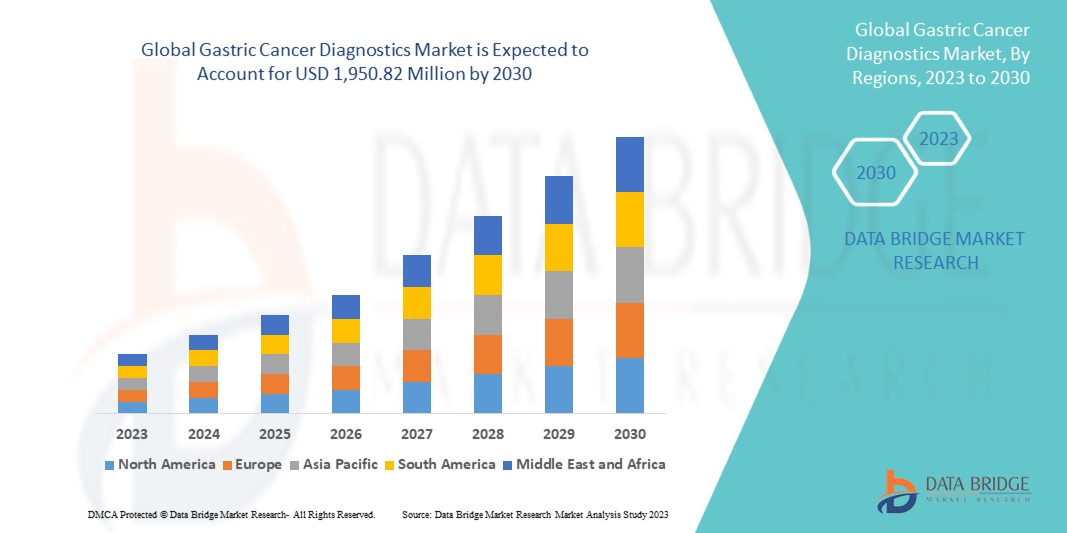

Data Bridge Market Research analyzes that the global gastric cancer diagnostics market is expected to reach a value of USD 1,950.82 million by 2030, at a CAGR of 8.% during the forecast period. Reagents and consumables account for the largest product type segment in the market due to rising demand for kits and reagents, and increasing health expenditures have accelerated the demand for smart medical devices.

|

Report Metric |

Details |

|

Forecast Period |

2023 to 2030 |

|

Base Year |

2022 |

|

Historic Years |

2021 (Customisable to 2015-2020) |

|

Quantitative Units |

Revenue in USD Million, Volumes in Units, Pricing in USD |

|

Segments Covered |

By Product Type (Instruments, Reagents & Consumables, Services), Diagnostics Type (Confirmatory Test, Gastric Cancer Screening Tests/Physical Exam), Age Group (Adult, Pediatric, and Geriatrics), Disease Type (Intestinal Or Diffuse Adenocarcinoma, Carcinoid Tumor, Gastrointestinal Stromal Tumor (GIST), Gastric Lymphoma and Others), Stage (Stage 0, Stage I, Stage II, Stage III), Gender (Male and Female), Sample Type (Blood, Tissue, Urine, and Stool), End Users (Diagnostic Laboratories, Hospitals, Cancer Research Institutes, Oncology Specialty Clinics, and Others), Distribution Channel (Direct Tenders and Retail Sales) |

|

Countries Covered |

U.S., Canada, and Mexico, Germany, U.K., France, Italy, Spain, Netherlands, Russia, Switzerland, Turkey, Belgium, rest of Europe, Japan, China, Australia, India, South Korea, Singapore, Indonesia, Thailand, Malaysia, Philippines, rest of Asia-Pacific, Brazil, Argentina, rest of South America, Saudi Arabia, South Africa, U.A.E, Israel, Egypt, and rest of Middle East and Africa |

|

Market Players Covered |

Myriad Genetics, Inc., ACON Laboratories, Inc., Teco Diagnostics., Vela Diagnostics, Abbott, AdvaCare Pharma, Fujirebio ( An H.U. Group company), Thermo Fisher Scientific Inc., F. Hoffmann-La Roche Ltd, General Electric, Agilent Technologies, Inc., Endofotonics Pte Ltd, Biohit Oyj, BIOCEPT, INC., FOUNDATION MEDICINE, INC., DiaSorin S.p.A, Paragon Genomics, Inc., BIOMÉRIEUX, and QIAGEN among others. |

Market Definition

Stomach cancer is a type of cancer that starts in the stomach and spreads throughout the body. The stomach is a muscular pouch that lies immediately below the ribs in the upper part of the abdomen. The stomach takes in and holds the food we eat before breaking it down and digesting it. Stomach cancer, commonly referred to as gastric cancer, can occur in any section of the stomach. Stomach cancers develop in the major section of the stomach in most parts of the world (stomach body). Various diagnostic tests used for the diagnosis of cancer include prescreening tests, biopsy, biomarkers, imaging tests, PET/CT scans, and ultrasound among others.

Cancer is caused by uncontrolled, abnormal cell proliferation that has the ability to spread and invade other sections of the body. Changes in the gene cause a single cell or a few cells to expand and replicate, which is when cancer begins. This could lead to the growth of a tumor, which is an abnormal mass of tissue. The creation of cancer cells in the stomach lining is known as gastric cancer or stomach cancer. Diet and stomach disorders are both risk factors for gastric cancer.

Global Gastric Cancer Diagnostics Market Dynamics

This section deals with understanding the market drivers, advantages, opportunities, restraints, and challenges. All of this is discussed in detail below:

Drivers

- Increase in incidence of gastrointestinal tumors, lymphoma, and adenocarcinoma

According to a report published in Clinical Medicine, gastric cancer is the fifth most common cancer and the fourth leading cause of cancer death worldwide in 2020. In 2020, an estimated 1.1 million cases (720,000 males and 370,000 females) of gastric cancer were diagnosed worldwide. Gastric cancer is responsible for about 1 in every 12 oncological fatalities. Every year, about a million new instances of stomach cancer are diagnosed around the world.

It is projected that the incidence of gastric cancer will rise, due to to aging and increasing population, lifestyle, and socioeconomic change. Striking variations in race, sociocultural norms, behaviors, and dietary trends are reflected in the burden and distribution of cancer in different regions across the globe.

Thus, the rising incidence of cancers across the globe is expected to accelerate the demand for gastric cancer diagnostics. Thus the increased incidence rates of gastrointestinal tumors, lymphoma, and adenocarcinoma are expected to drive the growth of the global gastric cancer diagnostics market.

- Rise in alcohol consumption and surge in smoking

Epidemiological, clinical, and laboratory evidence point to a behavioral relationship between cigarette smoking and alcohol consumption. The combined use of cigarettes and alcohol poses health concerns in addition to those posed by smoking alone and so represents a severe public health issue that warrants further investigation.

A chemical chain reaction occurs every time a smoker inhales a lit cigarette, producing dozens of hazardous chemicals. Cigarette smoke contains substances that are inhaled through the lips, through the tongue and mouth, down the throat, and into the lungs, producing inflammation and exposing those bodily parts to cancer-causing chemicals.

Thus, the rise in alcohol consumption and surge in smoking is expected to drive the global gastric cancer market growth.

Opportunity

- Rise in adoption of automated systems

Cancer is a system and network illness. This indicates that in a cancer cell, certain network-related genes stop working properly. Complex interactions in such gene networks should be addressed in cancer treatment. Artificial intelligence (AI) algorithms, in particular, have been rapidly evolving, which is reflected in oncology's progress.

Machine learning and neural networks are becoming increasingly significant in precision oncology and system medicine. The combination of imaging data with clinical and molecular data opens up a world of possibilities. Radiogenomics, for instance, is a new field focused on multidimensional data processing. It can also benefit from AI advancements.

Thus, the increased adoption of automated systems acts as an opportunity for the growth of this market.

Restraint/Challenge

- Lack of sufficient financial support from health insurance policies

To achieve their objectives, health systems require financial resources. Human resources, hospital care, and medications are the most expensive aspects of most healthcare systems. In most tropical countries, health care is funded through a combination of government, private (mainly out-of-pocket) spending, and international help.

Healthcare finance remains a key concern for low- and lower-middle-income countries. Many upper-middle-income countries in Latin America, Africa, and Asia have been able to establish health finance arrangements that cover large segments of their populations. These measures enable access to health care while also protecting individuals from catastrophic debt incurred as a result of that access. Finance, on the other hand, is a major obstacle to health care delivery in low-income countries (the bulk of which are in Sub-Saharan Africa).

Thus, the lack of sufficient financial support from health insurance policies acts as a restraint to market's growth.

Recent Developments

- In October 2022, General Electric Company collaborated with several research institutes such as the University of Cambridge Hospitals, Sophia Genetics, and earlier with Optellum to use imaging data in collaboration with Artificial intelligence. This will help to reduce the diagnosing time of several cancers and help to provide personalized care to patients. This has helped the company to widen its horizons in cancer diagnostics

- In March 2020, Thermo Fisher Scientific Inc. announced that it would be acquiring QIAGEN, a Netherland-based molecular diagnostics and healthcare company. This acquisition by the company will increase its product portfolio in the market, leading to increased revenue in future

Global Gastric Cancer Diagnostics Market Scope

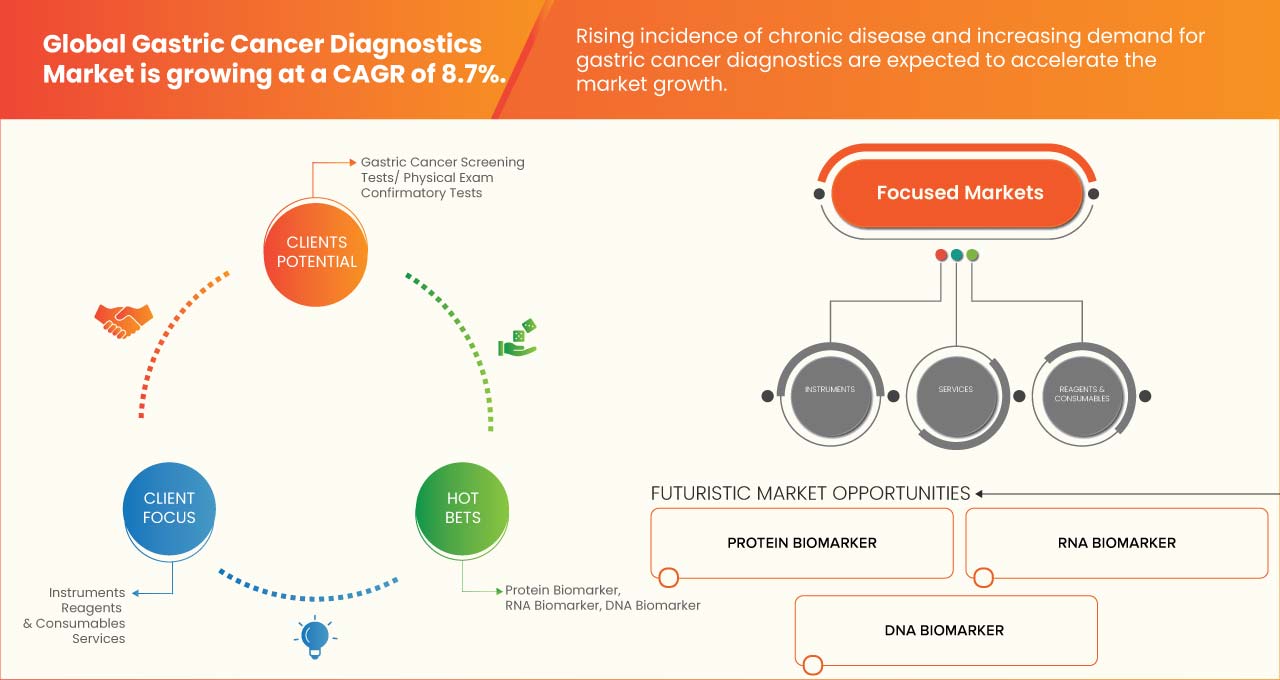

The global gastric cancer diagnostics market is segmented into nine notable segments based on product type, diagnostic type, age group, disease type, stage, gender, sample, end user, and distribution channel. The growth among segments helps you analyze niche pockets of growth and strategies to approach the market and determine your core application areas and the difference in your target markets.

PRODUCT TYPE

- Instruments

- Reagents & Consumables

- Services

On the basis of product type, the market is segmented into instruments, reagents & consumables, and services.

DIAGNOSTIC TYPE

- Confirmatory Test

- Gastric Cancer Screening Tests/Physical Exam

On the basis of diagnostics type, the market is segmented into gastric cancer screening tests/physical exam and confirmatory tests.

AGE GROUP

- Adult

- Pediatric

- Geriatrics

On the basis of age group, the market is segmented into adult, pediatric, and geriatrics.

TYPE

- Intestinal Or Diffuse Adenocarcinoma

- Carcinoid Tumor

- Gastrointestinal Stromal Tumor (GIST)

- Gastric Lymphoma

- Others

On the basis of type, the market is segmented into intestinal or diffuse adenocarcinoma, carcinoid tumor, gastrointestinal stromal tumor (GIST), gastric lymphoma, and others.

STAGE

- Stage 0

- Stage I

- Stage II

- Stage III

On the basis of stage, the market is segmented into stage 0, stage I, stage II, and stage III.

GENDER

- Male

- Female

On the basis of gender, the market is segmented into male and female.

SAMPLE TYPE

- Blood

- Tissue

- Urine

- Stool

On the basis of sample type, the market is segmented into blood, tissue, urine, and stool.

END USER

- Diagnostic Laboratories

- Hospitals

- Cancer Research Institutes

- Oncology Specialty Clinics

- Others

On the basis of end users, the market is segmented into diagnostic laboratories, hospitals, cancer research institutes, oncology specialty clinics, and others.

DISTRIBUTION CHANNEL

- Direct Tenders

- Retail Sales

On the basis of distribution channel, the market is segmented into direct tender and retail sales.

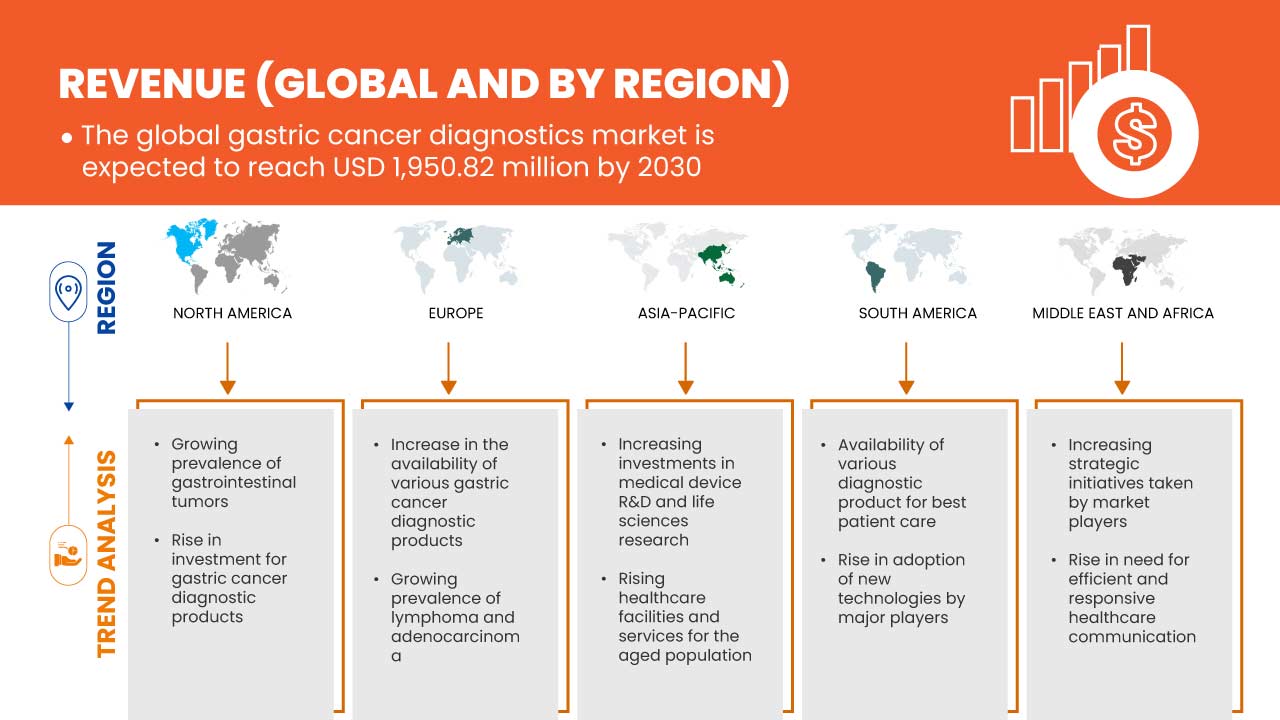

Global Gastric Cancer Diagnostics Market Regional Analysis/Insights

The global gastric cancer diagnostics market is segmented into nine notable segments based on product type, diagnostic type, age group, disease type, stage, gender, sample, end user, and distribution channel.

The countries covered in this market report are the U.S., Canada, and Mexico, Germany, U.K., France, Italy, Spain, Netherlands, Russia, Switzerland, Turkey, Belgium, rest of Europe, Japan, China, Australia, India, South Korea, Singapore, Indonesia, Thailand, Malaysia, Philippines, rest of Asia-Pacific, Brazil, Argentina, rest of South America, Saudi Arabia, South Africa, U.A.E, Israel, Egypt, and rest of Middle East and Africa.

North America is expected to dominate the global gastric cancer diagnostics market due to growing prevalence of gastrointestinal tumors. The U.S. dominates the North America region due to the strong presence of key players. Germany dominates the Europe region due to the increasing demand from emerging markets and expansion.

The country section of the report also provides individual market impacting factors and changes in regulation in the market domestically that impact the current and future trends of the market. Data points such as new sales, replacement sales, country demographics, regulatory acts, and import-export tariffs are some of the major pointers used to forecast the market scenario for individual countries. Also, the presence and availability of global brands and their challenges faced due to large or scarce competition from local and domestic brands, and the impact of sales channels are considered while providing forecast analysis of the country data.

Competitive Landscape and Gastric Cancer Diagnostics Market Share Analysis

The global gastric cancer diagnostics market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in R&D, new market initiatives, production sites and facilities, company strengths and weaknesses, product launch, product approvals, product width and breadth, application dominance, and product type lifeline curve. The above data points provided are only related to the company's focus on the Gastric Cancer Diagnostics market.

Some of the major players operating in the global gastric cancer diagnostics market are Myriad Genetics, Inc., ACON Laboratories, Inc., Teco Diagnostics., Vela Diagnostics, Abbott, AdvaCare Pharma, Fujirebio (An H.U. Group company), Thermo Fisher Scientific Inc., F. Hoffmann-La Roche Ltd, General Electric, Agilent Technologies, Inc., Endofotonics Pte Ltd, Biohit Oyj, BIOCEPT, INC., FOUNDATION MEDICINE, INC., DiaSorin S.p.A, Paragon Genomics, Inc., BIOMÉRIEUX, and QIAGEN among others.

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.