Global Glomerulonephritis Market

Размер рынка в млрд долларов США

CAGR :

%

USD

12.17 Billion

USD

17.57 Billion

2025

2033

USD

12.17 Billion

USD

17.57 Billion

2025

2033

| 2026 –2033 | |

| USD 12.17 Billion | |

| USD 17.57 Billion | |

| % | |

|

Global Glomerulonephritis Market Segmentation, By Type (Acute Glomerulonephritis, Chronic Glomerulonephritis, and Others), Diagnosis (Urine and Blood Test, Imaging Tests, Kidney Biopsy, and Others), Treatment (Medication, Surgery, Dialysis, and Others), Route of Administration (Oral, Parenteral, and Others), End-Users (Hospitals, Specialty Clinics, and Others), Distribution Channel (Hospital Pharmacy, Retail Pharmacy, and Others)- Industry Trends and Forecast to 2033

Glomerulonephritis Market Size

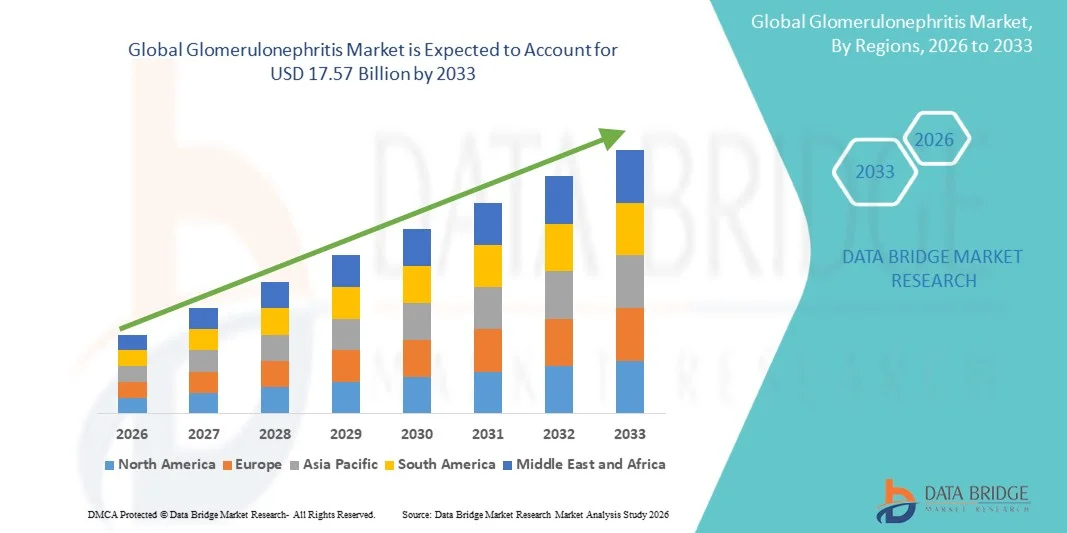

- The global glomerulonephritis market size was valued at USD 12.17 billion in 2025 and is expected to reach USD 17.57 billion by 2033, at a CAGR of 4.70% during the forecast period

- The market growth is largely driven by the increasing prevalence of chronic kidney diseases, rising awareness about early diagnosis, and advancements in diagnostic and therapeutic options for glomerular disorders

- Furthermore, growing demand for targeted therapies, improved treatment outcomes, and supportive care solutions is propelling the adoption of innovative treatment regimens. These converging factors are accelerating the uptake of glomerulonephritis management solutions, thereby significantly boosting the industry's growth

Glomerulonephritis Market Analysis

- Glomerulonephritis, a group of kidney disorders characterized by inflammation of the glomeruli, is increasingly recognized as a critical area in nephrology due to its impact on renal function, risk of progression to chronic kidney disease, and association with systemic conditions such as autoimmune disorders and infections

- The rising prevalence of chronic kidney diseases, growing awareness of early diagnosis, and advancements in diagnostic tools such as kidney biopsies, serological tests, and imaging technologies are key factors driving market growth

- North America dominated the glomerulonephritis market with the largest revenue share of 39.7% in 2025, supported by advanced healthcare infrastructure, high adoption of novel therapies, robust clinical research activities, and a strong presence of leading pharmaceutical and biotech companies offering targeted treatment options

- Asia-Pacific is expected to be the fastest growing region in the glomerulonephritis market during the forecast period, attributed to increasing healthcare access, rising patient awareness, and growing investments in nephrology-focused treatment centers

- Chronic Glomerulonephritis segment dominated the glomerulonephritis market with a market share of 44.3% in 2025, driven by the high prevalence of progressive renal conditions, long-term management needs, and increasing adoption of early intervention strategies to slow disease progression

Report Scope and Glomerulonephritis Market Segmentation

|

Attributes |

Glomerulonephritis Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Glomerulonephritis Market Trends

“Advancements in Targeted Therapies and Biologics”

- A significant and accelerating trend in the global glomerulonephritis market is the increasing development and adoption of targeted therapies, including biologics and monoclonal antibodies, which provide precision treatment for immune-mediated glomerular disorders

- For instance, the approval of sparsentan for focal segmental glomerulosclerosis (FSGS) allows clinicians to offer a therapy that specifically addresses the underlying pathophysiology while reducing proteinuria and preserving kidney function

- Targeted therapies enable more personalized treatment regimens, reducing systemic side effects compared to conventional immunosuppressants, and improving patient adherence and long-term outcomes

- Furthermore, integration of advanced therapeutics with ongoing clinical monitoring and biomarker-driven treatment adjustments facilitates more proactive disease management and early intervention to slow progression to end-stage renal disease

- This trend towards precision and biologic-based interventions is reshaping treatment paradigms and patient expectations for glomerulonephritis care

- The demand for innovative targeted therapies and biologics is rapidly growing across both chronic and acute glomerulonephritis cases, as clinicians prioritize effective and safer treatment options

- Growing investment in R&D collaborations between pharmaceutical companies and academic institutions is accelerating the development of novel therapies and combination treatments for complex glomerulonephritis cases

Glomerulonephritis Market Dynamics

Driver

“Rising Prevalence of Chronic Kidney Diseases and Early Diagnosis Awareness”

- The increasing prevalence of chronic kidney diseases and growing awareness of the importance of early diagnosis is a significant driver for the heightened demand for glomerulonephritis management solutions

- For instance, in March 2025, the National Kidney Foundation launched an awareness campaign to educate patients about early detection and timely treatment of glomerular disorders, highlighting the importance of preventive care

- As more patients undergo routine screening, early diagnosis allows timely intervention with appropriate medications, dialysis planning, or lifestyle modifications, thereby improving long-term outcomes

- Furthermore, expanding access to nephrology specialists and diagnostic facilities is making glomerulonephritis management more accessible to patients in both urban and semi-urban regions

- The increasing adoption of advanced diagnostic tools, including kidney biopsy and serological testing, combined with patient education initiatives, is propelling market growth

- Growing patient demand for effective disease management solutions and improved prognosis is driving the uptake of advanced treatment options and integrated care strategies

- Increasing awareness programs by global health organizations are promoting lifestyle modifications and preventive strategies to reduce the incidence of glomerular disorders

- Rising government initiatives and funding for kidney disease research are accelerating clinical trials and innovations, further driving market expansion

Restraint/Challenge

“High Treatment Costs and Limited Access in Emerging Regions”

- The relatively high cost of glomerulonephritis therapies, particularly biologics and advanced immunosuppressants, poses a significant challenge to broader market adoption, especially in developing countries

- For instance, limited reimbursement policies in regions such as Southeast Asia and Africa make it difficult for patients to access high-cost targeted therapies, restricting market penetration

- In addition, disparities in healthcare infrastructure, lack of specialized nephrology centers, and insufficient trained medical personnel limit the availability of timely diagnosis and treatment for glomerulonephritis

- While ongoing efforts to develop more affordable generics and biosimilars are underway, the perceived high cost of advanced therapies continues to be a barrier for price-sensitive patients and healthcare systems

- Furthermore, patient adherence to long-term treatment regimens can be affected by the financial burden and accessibility issues, slowing overall market growth

- Addressing these challenges through improved healthcare policies, expanded insurance coverage, and cost-effective therapeutic options will be crucial for sustained growth in the glomerulonephritis market

- Regulatory hurdles related to clinical trial approvals and stringent safety requirements can delay the launch of new therapies, affecting market expansion

- Limited public awareness in rural and underserved regions about kidney diseases and available treatment options continues to constrain the overall adoption of glomerulonephritis management solutions

Glomerulonephritis Market Scope

The market is segmented on the basis of type, diagnosis, treatment, route of administration, end-users, and distribution channel.

- By Type

On the basis of type, the glomerulonephritis market is segmented into acute glomerulonephritis, chronic glomerulonephritis, and others. The chronic glomerulonephritis segment dominated the market with the largest revenue share of 44.3% in 2025, driven by its higher prevalence and long-term management requirements. Chronic cases often require continuous monitoring, repeated laboratory assessments, and extended treatment regimens, creating steady demand for therapeutics and supportive care. The segment also benefits from the rising adoption of immunosuppressive medications, biologics, and patient education programs aimed at slowing disease progression. In addition, the increasing incidence of comorbidities such as diabetes and hypertension in chronic kidney disease patients fuels the growth of this segment. Growing investments in nephrology-focused healthcare infrastructure and specialized clinics further support market expansion. Steady research into chronic glomerulonephritis pathophysiology is also driving innovation in treatment options.

The acute glomerulonephritis segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing awareness and early diagnosis of post-infectious and rapidly progressive cases. Acute presentations often require immediate intervention through medications, supportive care, or dialysis, creating demand for quick-access diagnostic and therapeutic solutions. Improved availability of rapid diagnostic tools, including urine and blood tests, is accelerating early detection and treatment. In addition, rising patient education and physician awareness initiatives are increasing the identification of acute cases, particularly in pediatric and geriatric populations. Emerging healthcare facilities in developing regions are also expanding access to acute care services, driving adoption. Technological advancements in immunomodulatory treatments further support market growth.

- By Diagnosis

On the basis of diagnosis, the market is segmented into urine and blood tests, imaging tests, kidney biopsy, and others. The kidney biopsy segment dominated the market in 2025, owing to its critical role in accurately diagnosing glomerular disorders, guiding treatment strategies, and assessing disease severity. Biopsies provide precise histological insights that cannot be obtained from blood or imaging tests alone, making them the gold standard for clinical decision-making. Growing investments in pathology labs, advancements in biopsy techniques, and increasing physician preference for histopathological confirmation support this segment. The need for early and accurate diagnosis of complex glomerulonephritis cases ensures continued growth. In addition, integration of biopsy results with emerging biomarkers is enhancing personalized treatment planning. Hospital-based nephrology departments are further boosting segment adoption through specialist consultation.

The urine and blood test segment is expected to witness the fastest CAGR from 2026 to 2033, driven by its non-invasive nature, low cost, and ability to monitor disease progression. Regular monitoring of proteinuria, creatinine, and eGFR allows early detection and adjustment of therapy, reducing the risk of renal failure. Technological improvements in point-of-care testing and automation in laboratories are further accelerating adoption. Widespread screening programs and growing patient awareness are also contributing to rapid growth. The segment benefits from integration with telemedicine platforms for remote monitoring. Increased adoption in both hospitals and specialty clinics supports steady expansion.

- By Treatment

On the basis of treatment, the market is segmented into medication, surgery, dialysis, and others. The medication segment dominated the market with the largest revenue share in 2025, due to the widespread use of immunosuppressants, corticosteroids, and targeted therapies. Medications allow long-term disease management, reduce progression to end-stage renal disease, and are accessible across most healthcare settings. The segment benefits from increasing R&D in biologics and precision medicines designed to address specific glomerular pathologies. Patient adherence programs and clinical guidelines further support widespread use. Growth is also driven by expanding hospital and clinic formularies.

The dialysis segment is expected to witness the fastest growth rate from 2026 to 2033, owing to rising prevalence of severe glomerulonephritis cases progressing to kidney failure. Hemodialysis and peritoneal dialysis provide life-sustaining treatment and are increasingly accessible due to expanded dialysis centers in emerging markets. Improved awareness of renal replacement therapy and healthcare investments are supporting segment growth. Early intervention programs and governmental support for dialysis patients further drive adoption. Growing patient preference for home-based dialysis is expected to contribute to market expansion.

- By Route of Administration

On the basis of route of administration, the market is segmented into oral, parenteral, and others. The parenteral segment dominated the market in 2025, as many immunosuppressants, biologics, and monoclonal antibodies require intravenous or subcutaneous delivery for efficacy and controlled dosing. Parenteral administration ensures rapid therapeutic effects, better bioavailability, and suitability for hospital or clinic settings. The segment also benefits from advancements in infusion technology and reduced adverse events. Hospital-based nephrology centers support widespread adoption through trained personnel. Increasing R&D in parenteral biologics enhances treatment options.

The oral segment is expected to witness the fastest growth from 2026 to 2033, driven by patient preference for convenient, self-administered therapies. Innovations in oral formulations of immunosuppressants and adjunctive medications are increasing adoption. Growing awareness of adherence benefits and reduced hospital visits further propel segment growth. Expansion of retail pharmacy networks and prescription access supports market growth. Integration with digital health platforms for monitoring adherence enhances adoption. Development of combination oral therapies is expected to further accelerate this segment.

- By End-Users

On the basis of end-users, the market is segmented into hospitals, specialty clinics, and others. The hospital segment dominated the market in 2025, owing to availability of comprehensive diagnostic, therapeutic, and dialysis services under one roof. Hospitals also serve as referral centers for complex glomerulonephritis cases requiring multidisciplinary care. The segment benefits from government funding and advanced healthcare infrastructure. Availability of specialist nephrologists and trained personnel further supports market leadership. Hospitals act as key distribution points for parenteral medications. Established patient trust and integrated care models enhance adoption.

The specialty clinics segment is expected to witness the fastest growth from 2026 to 2033, fueled by expansion of nephrology-focused centers offering outpatient management, early intervention, and follow-up care. These clinics cater to chronic and early-stage patients, enhancing accessibility and convenience. Growing investments in clinic-based diagnostics and telemedicine solutions accelerate market penetration. Clinics often provide personalized care and patient education programs. Rising preference for decentralized treatment and reduced hospital visits is driving adoption. Integration with local pharmacies and diagnostic labs supports growth.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, and others. The hospital pharmacy segment dominated the market in 2025, due to in-hospital availability of critical medications, parenteral therapies, and dialysis support. Hospitals act as a primary source for advanced and specialized treatment options. Established procurement systems and direct access to physicians support market dominance. High patient inflow in hospitals ensures steady medication demand. Integration with electronic health records enhances inventory management. Hospital pharmacies often collaborate with specialty drug manufacturers to provide targeted therapies.

The retail pharmacy segment is expected to witness the fastest CAGR from 2026 to 2033, driven by the increasing availability of oral medications, growing patient preference for community-based access, and expansion of pharmacy networks in urban and semi-urban areas. Enhanced patient education and prescription adherence programs also support growth. Convenience of proximity to patients’ homes encourages regular refills. Partnerships with clinics and telemedicine providers further accelerate adoption. Growing awareness campaigns about chronic kidney disease medications increase retail demand. Online pharmacy integration provides additional avenues for market expansion.

Glomerulonephritis Market Regional Analysis

- North America dominated the glomerulonephritis market with the largest revenue share of 39.7% in 2025, supported by advanced healthcare infrastructure, high adoption of novel therapies, robust clinical research activities, and a strong presence of leading pharmaceutical and biotech companies offering targeted treatment options

- Patients and clinicians in the region highly value access to advanced diagnostics, targeted therapies, and integrated care programs that improve disease management and long-term outcomes for both acute and chronic glomerulonephritis cases

- This widespread adoption is further supported by high healthcare spending, robust clinical research activities, and strong government and private support for kidney disease awareness and early intervention initiatives, establishing North America as a leading market for glomerulonephritis management solutions

U.S. Glomerulonephritis Market Insight

The U.S. glomerulonephritis market captured the largest revenue share of 42% in 2025 within North America, fueled by the high prevalence of chronic kidney diseases and widespread adoption of advanced diagnostic and treatment solutions. Patients increasingly prioritize early detection through regular screening and timely intervention using immunosuppressive therapies and biologics. The growing availability of specialized nephrology centers, combined with robust healthcare spending and insurance coverage, further propels market growth. Moreover, ongoing research, clinical trials, and adoption of telemedicine for continuous disease monitoring are significantly contributing to the expansion of the U.S. market.

Europe Glomerulonephritis Market Insight

The Europe glomerulonephritis market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing awareness of kidney disorders and government initiatives promoting early diagnosis and treatment. Urbanization, rising healthcare expenditures, and improved access to specialty care foster adoption of glomerulonephritis management solutions. European patients and clinicians are also drawn to advanced therapies and integrated care programs that improve long-term outcomes. The region is experiencing significant growth across hospitals and specialty clinics, with treatment being incorporated into both acute care and chronic disease management programs.

U.K. Glomerulonephritis Market Insight

The U.K. glomerulonephritis market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising incidence of chronic kidney disease and increasing patient awareness of early detection strategies. Concerns regarding renal complications and long-term kidney health are encouraging both patients and healthcare providers to adopt advanced diagnostic and treatment solutions. In addition, the U.K.’s well-developed healthcare infrastructure and growing adoption of telemedicine and outpatient nephrology clinics are expected to continue to stimulate market growth.

Germany Glomerulonephritis Market Insight

The Germany glomerulonephritis market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of kidney health and the demand for advanced, precision-based therapies. Germany’s strong healthcare system, emphasis on medical innovation, and focus on patient-centric care promote the adoption of glomerulonephritis management solutions, particularly in hospitals and specialty clinics. Integration of early diagnosis programs with advanced therapeutic options is becoming increasingly prevalent, with a preference for evidence-based and guideline-directed treatments.

Asia-Pacific Glomerulonephritis Market Insight

The Asia-Pacific glomerulonephritis market is poised to grow at the fastest CAGR of 22% during the forecast period of 2026 to 2033, driven by increasing prevalence of kidney disorders, rising healthcare awareness, and expanding healthcare infrastructure in countries such as China, Japan, and India. The region's growing inclination towards preventive healthcare and early intervention is driving the adoption of diagnostic tools and treatment options. Furthermore, rising investments in nephrology-focused facilities and government initiatives supporting kidney disease management are expanding accessibility and affordability of therapies.

Japan Glomerulonephritis Market Insight

The Japan glomerulonephritis market is gaining momentum due to the country’s high awareness of chronic kidney diseases, aging population, and strong healthcare infrastructure. Japanese patients prioritize early diagnosis, continuous monitoring, and advanced treatment options including immunosuppressive therapies and biologics. The adoption of outpatient nephrology services and integration of telehealth platforms for disease management is fueling growth. Moreover, Japan’s focus on research, clinical trials, and technology-driven healthcare solutions is expected to further propel the market in both residential and institutional settings.

India Glomerulonephritis Market Insight

The India glomerulonephritis market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s increasing prevalence of kidney disorders, rising healthcare awareness, and expanding middle class. India stands as one of the largest emerging markets for advanced diagnostics and treatment solutions, and glomerulonephritis management is becoming increasingly accessible through hospitals, specialty clinics, and community healthcare programs. Government initiatives promoting early detection, combined with increasing availability of affordable therapies and rising telemedicine adoption, are key factors propelling the market in India.

Glomerulonephritis Market Share

The Glomerulonephritis industry is primarily led by well-established companies, including:

- F. Hoffmann La Roche Ltd (Switzerland)

- Pfizer Inc. (U.S.)

- Novartis AG (Switzerland)

- AstraZeneca (U.K.)

- Bristol Myers Squibb Company (U.S.)

- AbbVie Inc. (U.S.)

- Merck & Co., Inc. (U.S.)

- Sanofi (France)

- GSK plc (U.K.)

- Johnson & Johnson Services, Inc. (U.S.)

- Takeda Pharmaceutical Company Limited (Japan)

- Amgen Inc. (U.S.)

- Biogen Inc. (U.S.)

- Otsuka Pharmaceutical Co., Ltd. (Japan)

- Travere Therapeutics, Inc. (U.S.)

- Chinook Therapeutics, Inc. (U.S.)

- Vera Therapeutics, Inc. (U.S.)

- Ionis Pharmaceuticals, Inc. (U.S.)

- Alnylam Pharmaceuticals, Inc. (U.S.)

- Omeros Corporation (U.S.)

What are the Recent Developments in Global Glomerulonephritis Market?

- In November 2025, the U.S. FDA approved Voyxact (Otsuka’s injectable monoclonal antibody) for the treatment of primary immunoglobulin A nephropathy (IgAN), reducing proteinuria and offering a convenient at‑home treatment option

- In July 2025, the FDA approved EMPAVELI (pegcetacoplan) for patients aged 12 and older with C3 glomerulopathy (C3G) and primary immune complex membranoproliferative glomerulonephritis (IC‑MPGN), offering a new targeted therapy that significantly reduces proteinuria and stabilizes kidney function

- In April 2025, the U.S. FDA granted accelerated approval to Vanrafia® (atrasentan), a selective endothelin‑A receptor antagonist, for reducing proteinuria in adults with primary immunoglobulin A nephropathy (IgAN) at risk of rapid progression, expanding treatment options in IgAN management

- In March 2025, the U.S. FDA approved Fabhalta (iptacopan), the first oral treatment for adults with complement 3 glomerulopathy (C3G), marking a milestone as the only approved therapy targeting this rare form of glomerulonephritis to reduce proteinuria

- In March 2025, Novartis received third FDA approval for its oral drug Fabhalta (iptacopan), including a kidney disease indication for adults with complement 3 glomerulopathy (C3G), expanding its use beyond prior approvals and reinforcing its evolving role in glomerular disease therapy

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.