Global Hemodynamic Monitoring Systems Market

Размер рынка в млрд долларов США

CAGR :

%

USD

1.77 Billion

USD

2.67 Billion

2025

2033

USD

1.77 Billion

USD

2.67 Billion

2025

2033

| 2026 –2033 | |

| USD 1.77 Billion | |

| USD 2.67 Billion | |

| % | |

|

Global Hemodynamic Monitoring Systems Market Segmentation, By Type (Invasive, Minimally Invasive, and Non-Invasive), Product (Systems and Disposables), End User (Hospitals, Cath Labs and Home, and Ambulatory Care)- Industry Trends and Forecast to 2033

Hemodynamic Monitoring Systems Market Size

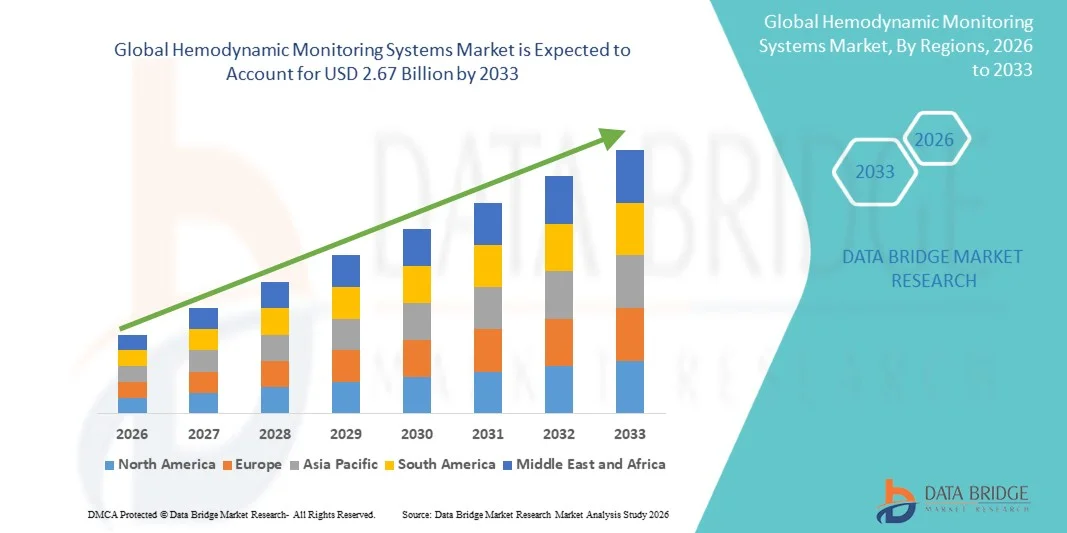

- The global hemodynamic monitoring systems market size was valued at USD 1.77 billion in 2025 and is expected to reach USD 2.67 billion by 2033, at a CAGR of 5.3% during the forecast period

- The market growth is largely fueled by the rising prevalence of cardiovascular diseases worldwide, increasing demand for real‑time and accurate cardiovascular status monitoring in critical care settings, and technological advancements in minimally invasive and non‑invasive monitoring solutions that enhance clinical decision‑making

- Furthermore, growing geriatric populations, expanding healthcare infrastructure in emerging regions, and a shift toward integrated, user‑friendly monitoring platforms with advanced sensors and data analytics are driving adoption across hospitals and ambulatory care centers, positioning hemodynamic monitoring systems as essential tools in modern patient management

Hemodynamic Monitoring Systems Market Analysis

- Hemodynamic monitoring systems, providing real-time measurement of cardiovascular parameters such as blood pressure, cardiac output, and oxygen delivery, are increasingly vital components of modern healthcare, particularly in intensive care units, operating rooms, and emergency care settings, due to their ability to support timely clinical decisions and improve patient outcomes

- The escalating demand for hemodynamic monitoring systems is primarily fueled by the increasing prevalence of cardiovascular diseases, growing geriatric populations, and rising adoption of minimally invasive and non-invasive monitoring technologies that enhance patient safety while reducing procedural risks

- North America dominated the hemodynamic monitoring systems market with the largest revenue share of 39.4% in 2025, driven by advanced healthcare infrastructure, early adoption of technologically advanced medical devices, and a strong presence of key industry players, with the U.S. leading in the deployment of both invasive and non-invasive monitoring solutions and innovations in wireless, integrated platforms

- Asia-Pacific is expected to be the fastest-growing region during the forecast period due to expanding healthcare infrastructure, rising healthcare expenditure, increasing cardiovascular disease prevalence, and growing awareness of advanced patient monitoring systems in countries such as China and India

- Minimally invasive segment dominated the market with a share of 42.7% in 2025, driven by its ability to provide accurate hemodynamic measurements with reduced patient risk, shorter recovery times, and lower chances of complications compared to fully invasive techniques, making it the preferred choice in critical care and perioperative monitoring

Report Scope and Hemodynamic Monitoring Systems Market Segmentation

|

Attributes |

Hemodynamic Monitoring Systems Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Hemodynamic Monitoring Systems Market Trends

“Advancements in Non-Invasive and Wireless Monitoring Technologies”

- A major and accelerating trend in the global hemodynamic monitoring systems market is the growing adoption of non-invasive and wireless monitoring devices that reduce patient risk while providing continuous real-time cardiovascular data

- For instance, the Clearsight Finger Cuff system enables non-invasive continuous blood pressure monitoring, eliminating the need for arterial catheterization in select ICU and perioperative settings

- Integration of wireless technologies with hospital information systems allows clinicians to remotely monitor patient parameters, receive alerts, and make timely interventions without being physically at the bedside

- Advanced sensor technologies and miniaturized wearable monitors facilitate patient mobility and comfort, while providing accurate hemodynamic measurements in critical care, step-down, and outpatient settings

- This trend toward more compact, intelligent, and connected monitoring solutions is reshaping clinical workflows, improving patient safety, and supporting hospital efforts to optimize critical care efficiency

- The demand for real-time, non-invasive, and wireless hemodynamic monitoring solutions is rapidly increasing across hospitals, ambulatory surgical centers, and telehealth applications, driven by efficiency, safety, and data-driven patient management

- Cloud-based monitoring systems are also gaining traction, enabling centralized data analysis across multiple hospital units and supporting tele-ICU programs

Hemodynamic Monitoring Systems Market Dynamics

Driver

“Rising Prevalence of Cardiovascular Diseases and Critical Care Needs”

- The increasing global incidence of cardiovascular diseases, coupled with higher demand for critical care monitoring, is a significant driver for the growing adoption of hemodynamic monitoring systems

- For instance, Philips Healthcare launched advanced IntelliVue monitoring platforms to provide integrated hemodynamic data for ICU patients, improving clinical decision-making and patient outcomes

- Clinicians increasingly prefer minimally invasive and non-invasive monitoring technologies to obtain real-time cardiovascular data while reducing procedural risks and complications

- The rising geriatric population and chronic disease prevalence are driving hospitals to adopt continuous hemodynamic monitoring for timely intervention and prevention of cardiac events

- Furthermore, growing awareness among healthcare providers about data-driven critical care and the integration of monitoring devices with electronic medical records is propelling adoption in both developed and emerging markets

- For instance, hospitals are implementing integrated monitoring solutions that combine hemodynamic, respiratory, and oxygenation data to streamline workflow and reduce manual errors

- Increasing government initiatives and funding programs to modernize hospital ICUs in emerging economies are creating additional opportunities for market expansion

Restraint/Challenge

“High Device Costs and Integration Complexities”

- The relatively high cost of advanced hemodynamic monitoring systems can limit adoption, particularly in smaller hospitals and developing regions, posing a significant market challenge

- For instance, some wireless and minimally invasive monitoring platforms require substantial upfront investment and staff training, making procurement difficult for resource-constrained facilities

- Integration of monitoring devices with existing hospital IT infrastructure can be complex, requiring software compatibility, cybersecurity measures, and interoperability standards compliance

- Maintenance, calibration, and disposable components further add to operational expenses, which can deter wider deployment in cost-sensitive healthcare settings

- Addressing these challenges through cost-effective device designs, modular system offerings, and simplified integration protocols will be critical to sustaining market growth

- For instance, lack of standardized protocols across devices can result in data inconsistencies, limiting clinician trust and slowing adoption

- Regulatory hurdles for approvals in multiple regions can delay product launches and increase development costs, further challenging market growth

Hemodynamic Monitoring Systems Market Scope

The market is segmented on the basis of type, product, end user.

- By Type

On the basis of type, the hemodynamic monitoring systems market is segmented into invasive, minimally invasive, and non-invasive systems. The minimally invasive segment dominated the market with a share of 42.7% in 2025, driven by its ability to provide accurate cardiovascular measurements while minimizing patient risk and procedural complications. Minimally invasive systems are widely adopted in ICUs and perioperative care due to their balance of reliability and safety, allowing clinicians to obtain real-time hemodynamic data without the need for fully invasive catheterization. The growing preference for minimally invasive monitoring is also supported by technological advancements in sensor design, integration with electronic medical records, and wireless connectivity, which enhance workflow efficiency and patient comfort. Hospitals increasingly rely on these systems to reduce the likelihood of infections and shorten patient recovery times, further strengthening market dominance.

The non-invasive segment is expected to witness the fastest growth rate of 7.2% CAGR from 2026 to 2033, fueled by increasing demand for remote patient monitoring and wearable hemodynamic devices. Non-invasive systems enable continuous monitoring of blood pressure, cardiac output, and other key parameters without surgical intervention, making them ideal for tele-ICU programs, outpatient care, and home-based monitoring. Advancements in AI-driven predictive analytics and wireless integration further support the adoption of non-invasive systems. Rising patient awareness, safety concerns, and hospitals’ emphasis on minimizing procedural risks contribute to the rapid uptake of non-invasive technologies, particularly in emerging markets.

- By Product

On the basis of product, the market is segmented into systems and disposables. Systems dominated the market with a share of 46% in 2025, as hospitals and critical care centers increasingly adopt comprehensive monitoring platforms capable of integrating multiple hemodynamic parameters. These systems allow clinicians to view real-time data, generate alerts for patient deterioration, and support decision-making in ICUs, operating rooms, and emergency care units. The dominance is also supported by the trend toward multi-parameter integration, connectivity with hospital IT infrastructure, and incorporation of AI-based analytics for predictive insights. Hospitals prioritize advanced systems due to their long-term clinical value and ability to streamline workflows across critical care departments.

The disposables segment is expected to witness the fastest growth rate of 6.8% CAGR from 2026 to 2033, driven by increased focus on hygiene, infection prevention, and single-use sensor applications. Disposables such as arterial pressure lines, disposable catheters, and single-use sensors reduce cross-contamination risks, ensuring patient safety in high-risk ICU and surgical environments. Rising awareness of hospital-acquired infections and regulatory requirements further propel demand for disposable components. In addition, technological advancements making disposables more accurate and compatible with systems are boosting adoption globally.

- By End User

On the basis of end user, the market is segmented into hospitals, cath labs & ambulatory care, and home care. Hospitals dominated the market in 2025 with the largest revenue share of 58%, driven by the high prevalence of critical care procedures, cardiac surgeries, and ICU admissions requiring continuous hemodynamic monitoring. Hospitals invest in integrated monitoring systems to improve patient outcomes, streamline workflows, and comply with regulatory standards for quality and safety. Large hospitals in North America and Europe lead adoption due to advanced healthcare infrastructure, trained staff, and budget allocation for high-value medical devices.

The home care and ambulatory care segment is expected to witness the fastest growth rate of ~8% CAGR from 2026 to 2033, fueled by increasing demand for remote monitoring solutions, wearable hemodynamic devices, and telehealth programs. Patients with chronic cardiovascular conditions or post-surgical care requirements increasingly rely on home monitoring to reduce hospital visits while maintaining real-time health tracking. Advancements in non-invasive and wireless technologies, along with smartphone and cloud-based monitoring applications, are accelerating adoption. Growing patient awareness, the shift toward decentralized healthcare, and healthcare reimbursement support for home monitoring devices contribute to rapid growth in this segment.

Hemodynamic Monitoring Systems Market Regional Analysis

- North America dominated the hemodynamic monitoring systems market with the largest revenue share of 39.4% in 2025, driven by advanced healthcare infrastructure, early adoption of technologically advanced medical devices

- Healthcare providers in the region highly value real-time monitoring, integration with electronic medical records, and advanced features such as AI-driven analytics and wireless connectivity, which improve patient outcomes and workflow efficiency

- This widespread adoption is further supported by a high prevalence of cardiovascular diseases, a growing geriatric population, strong healthcare spending, and a focus on critical care optimization, establishing hemodynamic monitoring systems as essential tools in modern hospital and surgical care

U.S. Hemodynamic Monitoring Systems Market Insight

The U.S. hemodynamic monitoring systems market captured the largest revenue share of 35% in 2025 within North America, fueled by the high prevalence of cardiovascular diseases and the extensive use of critical care monitoring in ICUs and surgical centers. Hospitals and healthcare providers increasingly prioritize real-time patient monitoring, integration with electronic medical records, and advanced minimally invasive and non-invasive technologies. The growing adoption of wireless and AI-enabled monitoring systems further propels market growth. Moreover, government initiatives supporting hospital modernization and tele-ICU programs are significantly contributing to the market's expansion.

Europe Hemodynamic Monitoring Systems Market Insight

The Europe hemodynamic monitoring systems market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by well-established healthcare infrastructure, increasing cardiovascular disease burden, and the rising need for critical care optimization. The adoption of advanced non-invasive and minimally invasive monitoring systems is growing across hospitals and surgical centers. European healthcare providers are also drawn to systems that enhance patient safety, workflow efficiency, and integration with hospital IT systems. The region is witnessing significant growth in both public and private hospital settings, with adoption in both new facilities and ICU upgrades.

U.K. Hemodynamic Monitoring Systems Market Insight

The U.K. hemodynamic monitoring systems market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing awareness of cardiovascular diseases and the growing trend of technology-driven patient care. Hospitals and specialty care centers are prioritizing non-invasive and wireless monitoring solutions to reduce procedural risks and improve real-time decision-making. The U.K.’s focus on digital health initiatives, robust healthcare infrastructure, and training programs for critical care staff is expected to continue stimulating market growth.

Germany Hemodynamic Monitoring Systems Market Insight

The Germany hemodynamic monitoring systems market is expected to expand at a considerable CAGR during the forecast period, fueled by advanced healthcare infrastructure, high adoption of minimally invasive monitoring systems, and emphasis on patient safety and clinical efficiency. German hospitals and ICUs are increasingly deploying integrated monitoring platforms that combine multiple hemodynamic parameters, supporting better patient outcomes. The country’s well-developed infrastructure and strong focus on healthcare innovation promote adoption in both public and private hospitals.

Asia-Pacific Hemodynamic Monitoring Systems Market Insight

The Asia-Pacific hemodynamic monitoring systems market is poised to grow at the fastest CAGR of 8% from 2026 to 2033, driven by rising healthcare expenditure, expanding hospital infrastructure, and increasing prevalence of cardiovascular disorders in countries such as China, India, and Japan. Government initiatives promoting hospital modernization and telehealth programs are also supporting market growth. In addition, increasing awareness of advanced patient monitoring solutions and growing demand for non-invasive and wearable devices are accelerating adoption.

Japan Hemodynamic Monitoring Systems Market Insight

The Japan hemodynamic monitoring systems market is gaining momentum due to the country’s high-tech healthcare environment, aging population, and emphasis on patient safety. Hospitals and cardiac care units increasingly adopt non-invasive and wireless monitoring systems to improve efficiency and reduce procedural risks. Integration with hospital IT systems and predictive analytics platforms is fueling growth, alongside demand for remote monitoring in home care and outpatient settings.

India Hemodynamic Monitoring Systems Market Insight

The India hemodynamic monitoring systems market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rapid hospital infrastructure expansion, rising cardiovascular disease prevalence, and growing awareness of advanced monitoring technologies. India is witnessing increased adoption of non-invasive and minimally invasive systems in both urban and semi-urban hospitals. Government programs for critical care development, tele-ICU initiatives, and cost-effective monitoring solutions are key factors propelling the market in India.

Hemodynamic Monitoring Systems Market Share

The Hemodynamic Monitoring Systems industry is primarily led by well-established companies, including:

- Edwards Lifesciences Corporation (U.S.)

- GE HealthCare (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- Medtronic (Ireland)

- Baxter (U.S.)

- NIHON KOHDEN CORPORATION (Japan)

- Drägerwerk AG & Co. KGaA (Germany)

- Getinge AB (Sweden)

- Mindray Medical International Limited (China)

- ICU Medical, Inc. (U.S.)

- CNSystems Medizintechnik GmbH (Austria)

- LiDCO Group Ltd. (U.K.)

- Deltex Medical Group PLC (U.K.)

- Osypka Medical GmbH (Germany)

- Schwarzer Cardiotek GmbH (Germany)

- Uscom Limited (Australia)

- Masimo Corporation (U.S.)

- CareTaker Medical LLC (U.S.)

- Tensys Medical Inc. (U.S.)

- NI Medical Ltd. (Israel)

What are the Recent Developments in Global Hemodynamic Monitoring Systems Market?

- In April 2025, BD (Becton, Dickinson and Company) launched the next‑generation HemoSphere Alta™ hemodynamic monitoring platform, integrating predictive artificial intelligence‑based algorithms including a Cerebral Autoregulation Index (CAI) and Hypotension Prediction Index to enhance real‑time clinical decision support for blood pressure instability and patient management

- In April 2025, Medtronic expanded its acute care and monitoring portfolio by entering into a distribution agreement with Retia Medical to offer the Argos™ cardiac output monitor in the U.S., providing clinicians with advanced multi‑beat hemodynamic data for critically ill and high‑risk surgical patients, aiming to enhance personalized care and improve ICU outcomes

- In October 2023, Masimo received the EU MDR CE Mark for its LiDCO® board‑in‑cable (BIC) module for hemodynamic monitoring, enabling dynamic beat‑by‑beat hemodynamic assessments directly from existing patient monitors without the need for a standalone monitor, thus expanding product offerings and interoperability in European clinical environments

- In July 2023, Retia Medical was awarded a national group purchasing agreement with Premier, Inc. for its Argos hemodynamic monitoring monitor, allowing Premier members access to negotiated pricing and terms for adoption of the Argos system in hospitals to support shock detection and resuscitation guidance for high‑risk patients

- In June 2023, Mindray Medical and Edwards Lifesciences collaborated to launch an advanced hemodynamic monitoring solution in Europe that integrates Edwards’s FloTrac™ sensor into Mindray’s BeneVision N‑Series patient monitors, enabling comprehensive hemodynamic assessment for acute care scenarios across multiple clinical settings

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.