Global Liquid Biopsy Tests Market

Размер рынка в млрд долларов США

CAGR :

%

USD

673.20 Million

USD

2,347.79 Million

2025

2033

USD

673.20 Million

USD

2,347.79 Million

2025

2033

| 2026 –2033 | |

| USD 673.20 Million | |

| USD 2,347.79 Million | |

| % | |

|

Сегментация мирового рынка жидкостной биопсии по типу (тесты на циркулирующие опухолевые клетки (ЦОК), тесты на циркулирующую опухолевую ДНК (цДНК), тесты на основе экзосом, тесты на основе микроРНК и другие), применению (диагностика рака, мониторинг лечения, раннее выявление и скрининг, прогностическая оценка и персонализированная медицина) — тенденции отрасли и прогноз до 2033 года.

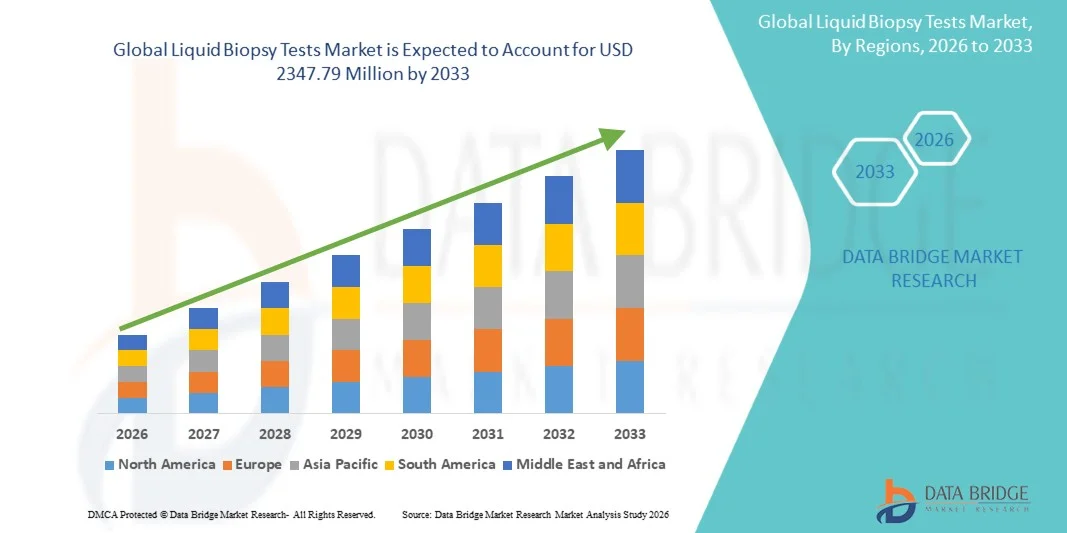

Размер рынка тестов жидкостной биопсии

- Объем мирового рынка жидкостной биопсии в 2025 году оценивался в 673,2 млн долларов США и, как ожидается, достигнет 2347,79 млн долларов США к 2033 году , демонстрируя среднегодовой темп роста в 16,90% в течение прогнозируемого периода.

- Рост рынка в значительной степени обусловлен расширением внедрения малоинвазивных диагностических методов, растущей распространенностью рака и увеличением спроса на персонализированную медицину и раннюю диагностику заболеваний.

- Кроме того, растущая осведомленность медицинских работников и пациентов о преимуществах жидкостной биопсии — таких как мониторинг заболевания в режиме реального времени, раннее выявление рецидива опухоли и снижение необходимости в инвазивной биопсии тканей — ускоряет внедрение решений на основе жидкостной биопсии, что значительно стимулирует рост отрасли.

Анализ рынка тестов жидкостной биопсии

- Жидкостная биопсия, предлагающая малоинвазивные диагностические решения для выявления и мониторинга рака и других генетических заболеваний, становится все более важной составляющей современного здравоохранения благодаря своей способности предоставлять информацию в режиме реального времени, обеспечивать раннюю диагностику и снижать необходимость в традиционной биопсии тканей.

- Растущий спрос на жидкостную биопсию обусловлен прежде всего увеличением распространенности рака, расширением применения персонализированной медицины и повышением осведомленности медицинских работников и пациентов о преимуществах неинвазивных диагностических методов.

- Северная Америка доминировала на рынке жидкостной биопсии, занимая наибольшую долю выручки в 46% в 2025 году, чему способствовали развитая инфраструктура здравоохранения, широкое внедрение прецизионной медицины, активная клиническая исследовательская деятельность и растущие инвестиции ключевых игроков рынка. США лидируют в регионе по значительному росту использования жидкостной биопсии в онкологических центрах, больницах и диагностических лабораториях.

- Ожидается, что Азиатско-Тихоокеанский регион станет самым быстрорастущим регионом на рынке жидкостной биопсии в течение прогнозируемого периода, прогнозируемый рост которого составит 11% в год с 2026 по 2033 год. Это обусловлено ростом заболеваемости раком, улучшением инфраструктуры здравоохранения, повышением осведомленности о передовых методах диагностики и расширением инициатив в области медицинских исследований в таких странах, как Китай, Индия, Япония и Южная Корея.

- Сегмент тестов на циркулирующую опухолевую ДНК (цДНК) занимал наибольшую долю рынка, составляющую 45,8% выручки в 2025 году, благодаря высокой чувствительности, неинвазивному характеру и доказанной клинической эффективности в выявлении мутаций, поддающихся лечению, для персонализированной терапии.

Обзор отчета и сегментация рынка жидкостной биопсии

|

Атрибуты |

Ключевые рыночные тенденции в области жидкостной биопсии. |

|

Охваченные сегменты |

|

|

Охваченные страны |

Северная Америка

Европа

Азиатско-Тихоокеанский регион

Ближний Восток и Африка

Южная Америка

|

|

Ключевые игроки рынка |

|

|

Рыночные возможности |

|

|

Информационные наборы данных, представляющие добавленную стоимость |

Помимо анализа рыночных сценариев, таких как рыночная стоимость, темпы роста, сегментация, географический охват и основные игроки, отчеты о рынке, подготовленные Data Bridge Market Research, также включают углубленный экспертный анализ, эпидемиологию пациентов, анализ перспективных разработок, анализ ценообразования и нормативно-правовую базу. |

Тенденции рынка тестов жидкостной биопсии

« Растущее внедрение малоинвазивных методов диагностики рака »

- Ключевой тенденцией на мировом рынке жидкостной биопсии является растущее внедрение малоинвазивных диагностических методов, позволяющих выявлять рак на ранних стадиях, отслеживать течение заболевания и оценивать эффективность лечения без необходимости проведения традиционной биопсии тканей.

- Например, в 2024 году компания Guardant Health запустила тест жидкостной биопсии Guardant360, позволяющий врачам выявлять множество потенциально значимых мутаций по одному образцу крови, что подчеркивает переход к минимально инвазивной диагностике.

- Жидкостная биопсия позволяет быстро и точно получить молекулярную информацию из простого образца крови, снижая дискомфорт и риски для пациента по сравнению с хирургической биопсией.

- Достижения в области секвенирования нового поколения (NGS), цифровой ПЦР и микрофлюидики позволяют проводить высокочувствительное и точное обнаружение циркулирующей опухолевой ДНК (ctDNA), экзосом и циркулирующих опухолевых клеток (CTC).

- Эта тенденция дополнительно подпитывается растущим предпочтением пациентов к менее инвазивным процедурам и сокращению сроков пребывания в больнице.

- Больницы и онкологические центры все чаще интегрируют жидкостную биопсию в стандартные рабочие процессы в дополнение к результатам визуализации и биопсии тканей. Фармацевтические компании используют технологии жидкостной биопсии в клинических испытаниях для идентификации биомаркеров и мониторинга терапии.

- Растущая доступность сопутствующих диагностических наборов для таргетной терапии стимулирует их внедрение среди врачей. Развивающиеся страны быстро внедряют жидкостную биопсию благодаря расширению онкологических центров и улучшению инфраструктуры здравоохранения.

- Технологические инновации, такие как многогенные панели и цифровые индикаторы, повышают надежность и скорость тестирования.

Динамика рынка тестов жидкостной биопсии

Водитель

«Рост заболеваемости раком и необходимость персонализированной медицины»

- Растущее глобальное бремя онкологических заболеваний является одним из основных факторов, стимулирующих рынок жидкостной биопсии, поскольку врачам необходимы точные, быстрые и неинвазивные диагностические решения для раннего выявления и мониторинга заболеваний.

- Например, в марте 2025 года компания Roche объявила о расширении своего теста Cobas EGFR Mutation Test, решения для жидкостной биопсии, которое помогает отбирать пациентов для таргетной терапии, что является примером растущего спроса на персонализированную медицину.

- Растущее внедрение подходов персонализированной и прецизионной медицины еще больше стимулирует спрос, поскольку жидкостная биопсия может помочь в выборе таргетной терапии и мониторинге ответа на лечение.

- Фармацевтические компании все чаще используют жидкостную биопсию для разработки лекарств на основе биомаркеров, мониторинга клинических испытаний и сопутствующей диагностики, что способствует расширению рынка.

- Расширение инфраструктуры здравоохранения на развивающихся рынках в сочетании с улучшенным доступом к передовой диагностике стимулирует внедрение новых методов. Государственные инициативы, направленные на продвижение программ раннего выявления рака, поддержку возмещения затрат и кампании по скринингу онкологических заболеваний, способствуют росту рынка.

- Технологические достижения в области высокопроизводительного секвенирования, цифровой ПЦР и биоинформатики повышают точность, надежность и скорость выполнения анализов. Повышение осведомленности врачей и их предпочтение менее инвазивным процедурам способствуют расширению использования жидкостной биопсии по сравнению с традиционной биопсией.

- Инвестиции ключевых игроков рынка в исследования и разработки новых панелей жидкостной биопсии стимулируют инновации и их внедрение. Возможность мультиплексного тестирования нескольких типов рака в рамках одного анализа повышает клиническую полезность и рыночный спрос.

- Предпочтение пациентов к малоинвазивным процедурам способствует росту их внедрения. Сотрудничество между диагностическими лабораториями, больницами и биотехнологическими компаниями облегчает проникновение на рынок.

Сдержанность/Вызов

« Высокая стоимость и проблемы технической стандартизации »

- Высокая стоимость жидкостной биопсии по сравнению с традиционными методами диагностики препятствует ее широкому внедрению, особенно в регионах с высокой чувствительностью к ценам и в развивающихся странах.

- Например, в 2023 году исследование, опубликованное в журнале The Lancet Oncology, показало, что средняя стоимость многогенных панелей жидкостной биопсии превышает 1000 долларов США за тест, что ограничивает доступность и внедрение этого метода врачами во многих регионах.

- Кроме того, отсутствие стандартизации в сборе, обработке образцов и интерпретации данных может приводить к вариабельности результатов, вызывая сомнения у врачей. Различия в чувствительности обнаружения и специфичности анализа у разных поставщиков услуг могут снижать уверенность в результатах тестирования.

- В некоторых регионах нормативные и финансовые барьеры замедляют расширение рынка и усложняют операционную деятельность производителей. В развивающихся странах ограничена доступность квалифицированного персонала и сертифицированных лабораторий, что препятствует внедрению новых технологий.

- Высокие инвестиционные требования к созданию современных платформ секвенирования в больницах и исследовательских центрах являются препятствием. Необходимы клинические валидационные исследования для обеспечения точности тестов и соответствия нормативным требованиям, что замедляет вывод продукции на рынок.

- Некоторые пациенты и врачи по-прежнему скептически относятся к надежности результатов жидкостной биопсии по сравнению с биопсией тканей, что влияет на ее эффективность. Технические ограничения в обнаружении мутаций с низкой частотой встречаемости на ранних стадиях рака создают проблемы.

- Компании преодолевают эти ограничения, предлагая экономически эффективные решения, повышая чувствительность анализов и предоставляя лабораториям обучение и поддержку.

Обзор рынка жидкостной биопсии

Рынок сегментирован по типу, технологии, применению и конечному пользователю.

• По типу

В зависимости от типа, рынок жидкостной биопсии сегментируется на тесты на циркулирующие опухолевые клетки (ЦОК), тесты на циркулирующую опухолевую ДНК (цДНК), тесты на основе экзосом, тесты на основе микроРНК и другие. Сегмент тестов на циркулирующую опухолевую ДНК (цДНК) занимал наибольшую долю рынка (45,8%) в 2025 году благодаря высокой чувствительности, неинвазивному характеру и доказанной клинической эффективности в выявлении мутаций, поддающихся лечению, для персонализированной терапии. Тесты на цДНК широко используются в онкологии для выбора лечения, мониторинга заболевания и выявления рецидивов. Этот сегмент пользуется популярностью как в больничных лабораториях, так и в коммерческих диагностических центрах благодаря надежным результатам, широкому охвату онкологических заболеваний и интеграции с платформами секвенирования нового поколения (NGS). Клиницисты часто предпочитают тесты на цДНК для мониторинга ответа на терапию и минимальной остаточной болезни (МОБ). Постоянные технологические достижения в области чувствительности анализов, мультиплексного обнаружения и биоинформатики укрепляют лидерство цДНК на рынке. Растущая распространенность рака во всем мире и спрос на прецизионную медицину еще больше способствуют росту этого сегмента. Участники рынка все чаще предлагают экономически эффективные панели циркулирующей ДНК (ctDNA), расширяя доступность в развитых и развивающихся регионах. Стратегическое сотрудничество между диагностическими компаниями и онкологическими центрами способствует быстрому внедрению. Кроме того, наличие одобренных FDA тестов на ctDNA повысило клиническую уверенность. Повышение осведомленности пациентов и медицинских работников о малоинвазивных методах лечения стимулирует их внедрение. В целом, тесты на ctDNA считаются золотым стандартом молекулярного профилирования на основе жидкостной биопсии, сохраняя лидирующие позиции по доходам и клиническому предпочтению.

Ожидается, что сегмент тестов на циркулирующие опухолевые клетки (ЦОК) продемонстрирует самый быстрый среднегодовой темп роста в 22,4% в период с 2026 по 2033 год, чему способствует их растущее использование для ранней диагностики рака, прогнозирования и мониторинга метастазов. Тесты на ЦОК позволяют отслеживать динамику опухоли в режиме реального времени и предоставляют информацию о гетерогенности опухоли, что делает их чрезвычайно ценными для планирования персонализированной терапии. Увеличение числа клинических исследований новых методов обогащения и обнаружения ЦОК способствует их внедрению. Повышение осведомленности пациентов и онкологов о неинвазивной диагностике ускоряет рост спроса. Технологии ЦОК интегрируются в клинические испытания для мониторинга эффективности терапии и механизмов резистентности. Новые приложения в мониторинге ответа на иммунотерапию еще больше стимулируют рост рынка. Стратегические партнерства и инвестиции в НИОКР позволяют создавать инновационные платформы ЦОК с более высокой чувствительностью и меньшими требованиями к объему образцов. Расширение сети диагностических лабораторий, специализирующихся на онкологии, в Северной Америке, Европе и Азиатско-Тихоокеанском регионе способствует быстрому проникновению на рынок. Государственные инициативы и поддержка возмещения затрат в некоторых регионах способствуют более широкому внедрению. Постоянное совершенствование точности, воспроизводимости и экономической эффективности анализов обеспечивает широкое признание среди врачей. Тесты на циркулирующие опухолевые клетки (ЦОК) дополняют анализы на циркулирующую ДНК (цДНК), создавая синергетический подход в диагностике с помощью жидкостной биопсии. Рост рынка усиливается за счет расширения программ скрининга онкологических заболеваний и сотрудничества с академическими исследовательскими центрами. В целом, ожидается, что тесты на ЦОК продемонстрируют самый быстрый рост доходов благодаря растущей клинической значимости и технологическим достижениям.

• По заявлению

В зависимости от области применения рынок жидкостной биопсии сегментирован на диагностику рака, мониторинг лечения, раннее выявление и скрининг, прогностическую оценку и персонализированную медицину. Сегмент диагностики рака занимал наибольшую долю рынка в 42,6% в 2025 году, что обусловлено растущим глобальным бременем онкологических заболеваний и острой необходимостью в точных, малоинвазивных диагностических инструментах. Врачи все чаще используют жидкостную биопсию для выявления мутаций, требующих лечения, мониторинга прогрессирования заболевания и дополнения результатов биопсии тканей. Внедрение тестов на циркулирующую ДНК (ctDNA) и циркулирующие опухолевые клетки (CTC) для различных солидных опухолей, включая рак легких, колоректальный рак, рак молочной железы и предстательной железы, укрепляет лидерство сегмента на рынке. Сегмент выигрывает от технологических достижений, таких как мультиплексные панели и высокопроизводительное секвенирование, которые позволяют одновременно обнаруживать множество биомаркеров. Расширение сотрудничества между больницами, исследовательскими центрами и диагностическими компаниями способствует широкому внедрению. Предпочтение пациентов к менее инвазивным процедурам еще больше усиливает спрос. Инициативы правительств и НПО, направленные на раннее выявление рака, создают благоприятные рыночные условия. Рост инвестиций в исследования и разработки в области онкологии в сочетании с развитием инфраструктуры здравоохранения в развивающихся странах еще больше стимулирует рост. В развитых регионах приоритет отдается применению методов диагностики рака благодаря поддержке в области возмещения затрат и широкому клиническому применению. Академические публикации и клинические рекомендации все чаще одобряют жидкостную биопсию для диагностики, что повышает ее авторитет. В целом, этот сегмент сохраняет доминирующее положение благодаря своей критической клинической значимости, внедрению технологий и широкой применимости для различных типов рака.

Ожидается, что сегмент мониторинга лечения продемонстрирует самый быстрый среднегодовой темп роста в 23,1% в период с 2026 по 2033 год, чему способствует растущая потребность в оценке эффективности терапии в режиме реального времени и раннем выявлении лекарственной устойчивости. Тесты жидкостной биопсии позволяют врачам неинвазивно отслеживать динамику опухоли, что дает возможность корректировать терапию без повторных биопсий тканей. Растущее использование таргетной терапии и иммунотерапии требует непрерывного мониторинга, что стимулирует спрос. Технологические достижения в количественном определении циркулирующей опухолевой ДНК (ctDNA) и характеристике циркулирующих опухолевых клеток (CTC) повышают точность и надежность. Фармацевтические компании все чаще включают жидкостную биопсию в клинические исследования для мониторинга результатов лечения. Расширение сети молекулярно-диагностических лабораторий при больницах в Северной Америке, Европе и Азиатско-Тихоокеанском регионе ускоряет внедрение. Повышение осведомленности пациентов о преимуществах персонализированного лечения способствует росту рынка. Расширение сотрудничества между биотехнологическими компаниями и онкологическими центрами поддерживает инновации в методах мониторинга. Развивающиеся экономики внедряют мониторинг лечения для оптимизации ограниченных ресурсов здравоохранения. Улучшенная политика возмещения затрат в развитых регионах способствует более широкому клиническому применению. Непрерывные исследования прогностических биомаркеров укрепляют доверие к этому сегменту. В целом, приложения для мониторинга лечения демонстрируют самый быстрый рост благодаря клинической необходимости, технологическому прогрессу и переходу к персонализированной онкологической помощи.

Региональный анализ рынка тестов жидкостной биопсии

- Северная Америка доминировала на рынке жидкостной биопсии, занимая наибольшую долю выручки в 46% в 2025 году.

- Поддержка со стороны развитой инфраструктуры здравоохранения.

- Широкое внедрение методов прецизионной медицины, активная клиническая исследовательская деятельность и растущие инвестиции со стороны ключевых игроков рынка.

Анализ рынка жидкостной биопсии в США

В 2025 году рынок жидкостной биопсии в США занял наибольшую долю выручки в Северной Америке, чему способствовал существенный рост объемов проведения жидкостной биопсии в онкологических центрах, больницах и диагностических лабораториях. Расширение рынка обусловлено технологическими достижениями в обнаружении циркулирующей опухолевой ДНК (цДНК) и циркулирующих опухолевых клеток (ЦОК), а также расширением применения методов ранней диагностики рака, мониторинга ответа на лечение и оценки минимальной остаточной болезни. Сильная регуляторная поддержка в стране, растущие инвестиции в прецизионную медицину и расширяющееся сотрудничество между диагностическими компаниями и исследовательскими институтами еще больше способствуют росту рынка.

Анализ рынка жидкостной биопсии в Европе

Прогнозируется, что европейский рынок тестов жидкостной биопсии будет расти значительными среднегодовыми темпами в течение прогнозируемого периода, чему способствуют растущая распространенность рака, внедрение прецизионной медицины и поддерживающая политика здравоохранения, направленная на раннюю диагностику. Сотрудничество между диагностическими компаниями и научно-исследовательскими институтами, а также расширение сети клинических лабораторий, предлагающих передовые решения в области молекулярной диагностики, еще больше способствуют росту.

Анализ рынка жидкостной биопсии в Великобритании

Ожидается, что рынок жидкостной биопсии в Великобритании будет расти значительными темпами, чему способствуют рост заболеваемости раком, все более широкое внедрение неинвазивных методов диагностики и увеличение инвестиций в клинические исследования. Развитая инфраструктура здравоохранения страны и акцент на раннем выявлении и персонализированном лечении продолжают стимулировать внедрение технологий жидкостной биопсии.

Анализ рынка жидкостной биопсии в Германии

Ожидается, что рынок жидкостной биопсии в Германии будет стабильно расти благодаря развитой системе здравоохранения, высокой активности в области клинических исследований и растущему внедрению передовых платформ молекулярной диагностики. Спрос на малоинвазивную диагностику рака и мониторинг прогрессирования заболевания в режиме реального времени также способствует росту рынка.

Анализ рынка жидкостной биопсии в Азиатско-Тихоокеанском регионе

Ожидается, что рынок жидкостной биопсии в Азиатско-Тихоокеанском регионе станет самым быстрорастущим регионом на этом рынке в течение прогнозируемого периода, прогнозируемый рост составит 11% в год с 2026 по 2033 год. Рост обусловлен увеличением заболеваемости раком, улучшением инфраструктуры здравоохранения, повышением осведомленности о передовых методах диагностики и расширением инициатив в области медицинских исследований в таких странах, как Китай, Индия, Япония и Южная Корея. Ключевыми факторами роста являются государственные инициативы, поддерживающие прецизионную медицину, растущее внедрение платформ секвенирования нового поколения (NGS) и расширение сети онкологических диагностических центров.

Анализ рынка жидкостной биопсии в Японии

Рынок жидкостной биопсии в Японии набирает обороты благодаря высокой распространенности рака в стране, технологически развитой системе здравоохранения и растущему использованию неинвазивных диагностических тестов. Продолжающиеся инвестиции в НИОКР и внедрение передовых молекулярно-диагностических инструментов дополнительно поддерживают рост рынка, особенно в области онкологии и персонализированной медицины.

Анализ рынка жидкостной биопсии в Китае

В 2025 году китайский рынок жидкостной биопсии занимал наибольшую долю выручки в Азиатско-Тихоокеанском регионе, чему способствовали рост распространенности рака, расширение инфраструктуры здравоохранения, государственные инициативы по ранней диагностике рака и растущее внедрение технологий молекулярной диагностики. Наличие отечественных диагностических компаний, предлагающих экономически эффективные решения, и быстрый технологический прогресс в области платформ жидкостной биопсии являются ключевыми факторами, способствующими расширению рынка.

Доля рынка тестов жидкостной биопсии

В отрасли жидкостной биопсии лидируют преимущественно хорошо зарекомендовавшие себя компании, в том числе:

- Guardant Health (США)

- Рош (Швейцария)

- Иллюмина (США)

- Точные науки (США)

- Thermo Fisher Scientific (США)

- Фонд медицины (США)

- Корпорация Sysmex (Япония)

- Натера (США)

- Ф. Хоффманн-Ла Рош (Швейцария)

- Sophia Genetics (Швейцария)

- Компания Cancer Genetics, Inc. (США)

- Singlera Genomics (Китай)

- Персональная геномная диагностика (США)

- Freenome (США)

- ArcherDX (США)

- Chronix Biomedical (Германия)

- Guardant Health (США)

- Bio-Rad Laboratories (США)

- Burning Rock Biotech (Китай)

Последние разработки на мировом рынке жидкостной биопсии.

- В июле 2024 года компания Guardant Health, Inc. объявила о запуске масштабного обновления своего ведущего на рынке теста жидкостной биопсии Guardant360, включающего расширенную панель из 739 генов, что позволяет проводить более широкую оценку биомаркеров и повышает чувствительность для характеристики запущенных форм рака, укрепляя тем самым свои позиции в области прецизионной онкологической диагностики.

- В октябре 2024 года компания Guardant Health получила одобрение Управления по санитарному надзору за качеством пищевых продуктов и медикаментов США (FDA) на свой тест жидкостной биопсии Guardant360 CDx в качестве сопутствующей диагностической системы для выявления мутаций EGFR при немелкоклеточном раке легких (НМРЛ). Это стало одним из первых одобрений FDA для сопутствующей диагностической системы жидкостной биопсии на основе NGS при солидных опухолях.

- В мае 2024 года компания Mercy BioAnalytics, Inc. получила от Управления по санитарному надзору за качеством пищевых продуктов и медикаментов США (FDA) статус «прорывного медицинского устройства» для своего теста Mercy Halo Ovarian Cancer Screening Test — жидкостной биопсии на основе внеклеточных везикул, предназначенной для раннего выявления рака у бессимптомных женщин в постменопаузе, — что подчеркивает поддержку регулирующих органов инновационным неинвазивным диагностическим методам.

- В августе 2024 года компания Labcorp объявила о получении разрешения на продажу от Управления по санитарному надзору за качеством пищевых продуктов и медикаментов США (FDA) для PGDx elio plasma focus Dx — первого одобренного FDA набора для жидкостной биопсии при различных солидных опухолях, позволяющего врачам определять возможность применения таргетной терапии при различных типах рака.

- В марте 2025 года компания Belay Diagnostics заключила партнерское соглашение с GenomOncology для интеграции GO Pathology Workbench в анализ результатов жидкостной биопсии «Summit», оптимизировав рабочие процессы интерпретации вариантов и поддержав высокопроизводительную обработку образцов для принятия клинических решений в онкологической помощи.

- В мае 2025 года Национальная служба здравоохранения Англии (NHS) внедрила новаторский тест на циркулирующую ДНК опухоли (ctDNA) на основе жидкостной биопсии в качестве диагностического инструмента первой линии для пациентов с подозрением на рак легких и запущенным раком молочной железы. Этот тест обеспечивает неинвазивное геномное профилирование для выбора персонализированной терапии и снижения необходимости в инвазивной биопсии тканей.

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.