Global Needle Free Injection System Market

Размер рынка в млрд долларов США

CAGR :

%

USD

240.40 Million

USD

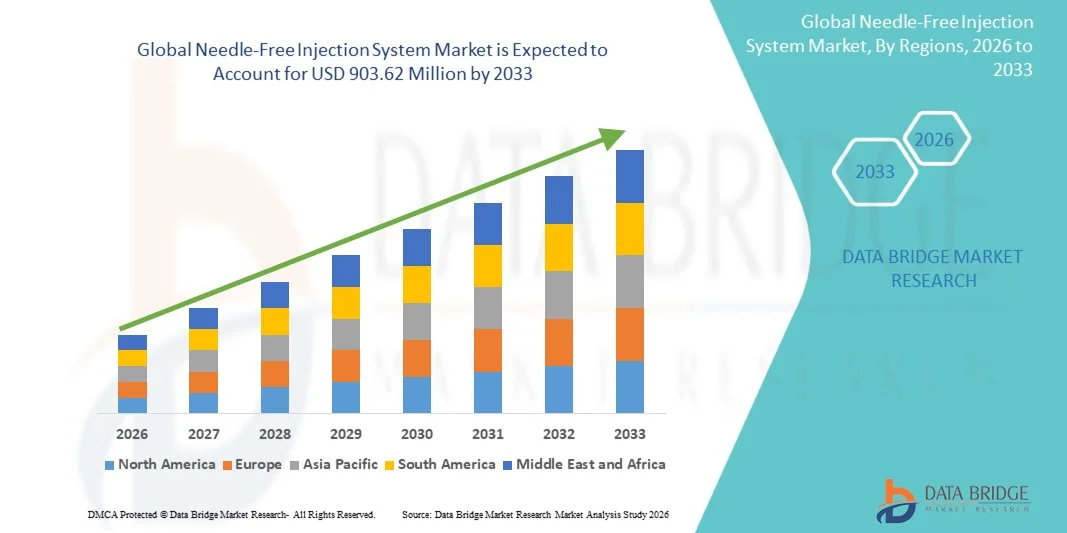

903.62 Million

2025

2033

USD

240.40 Million

USD

903.62 Million

2025

2033

| 2026 –2033 | |

| USD 240.40 Million | |

| USD 903.62 Million | |

| % | |

|

Global Needle-Free Injection System Market Segmentation, By Type (Liquid-Based Needle-Free Injectors, Projectile/Depot-Based Needle-Free Injectors, and Powder-Based Needle-Free Injectors), Product (Fillable Needle-Free Injectors and Prefilled Needle-Free Injectors), Technology (Jet-Based Needle-Free Injectors, Spring-Based Needle-Free Injectors, Laser-Powered Needle-Free Injectors, and Vibration-Based Needle-Free Injectors), Source of Power (Spring-Based Needle-Free Injectors, Gas Propelled/ Air Forced Injector Systems), Usability (Disposable Needle-Free Injectors, and Reusable Needle-Free Injectors), Delivery Site (Subcutaneous Injectors, Intramuscular Injectors, and Intradermal Injectors), Application (Vaccine Delivery, Insulin Delivery, Oncology, Pain Management, and Others), End-User (Hospitals, Clinics, Home Care Settings, Research Laboratories, Pharmaceutical and Biotechnological Companies, and Others) - Industry Trends and Forecast to 2033

Needle-Free Injection System Market Size

- The global needle-free injection system market size was valued at USD 240.40 Million in 2025 and is expected to reach USD 903.62 Million by 2033, at a CAGR of 18.00% during the forecast period

- The market growth is largely fueled by the increasing adoption of advanced drug delivery technologies and the rising need for safe, convenient, and pain-free injection solutions in both clinical and home care settings

- Furthermore, growing awareness about the benefits of needle-free systems, such as reduced risk of needle-stick injuries, enhanced patient compliance, and suitability for mass vaccination programs, is driving the uptake of Needle-Free Injection System solutions, thereby significantly boosting the industry's growth

Needle-Free Injection System Market Analysis

- Needle-free injection systems, offering pain-free and safe drug delivery without traditional needles, are increasingly vital in both clinical and home care settings due to their enhanced convenience, reduced risk of needle-stick injuries, and improved patient compliance

- The escalating demand for needle-free injection systems is primarily fueled by rising awareness of their benefits, increasing adoption in vaccination programs, chronic disease management, and preference for user-friendly, minimally invasive solutions

- North America dominated the needle-free injection system market with the largest revenue share of 38.5% in 2025, driven by the high prevalence of chronic diseases, early adoption of advanced medical devices, and the presence of leading market players, with the U.S. experiencing significant growth in needle-free system usage across hospitals, clinics, and home care

- Asia Pacific is expected to be the fastest-growing region in the needle-free injection system market during the forecast period with a projected CAGR of 9.3%, fueled by increasing healthcare awareness, government initiatives promoting vaccination, and growing adoption of advanced drug delivery technologies

- Disposable injectors dominated with a 55% revenue share in 2025, owing to hygiene, infection control, and suitability for large-scale immunization programs

Report Scope and Needle-Free Injection System Market Segmentation

|

Attributes |

Needle-Free Injection System Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• PharmaJet (U.S.) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Needle-Free Injection System Market Trends

“Enhanced Adoption of Minimally Invasive Drug Delivery”

- A significant trend in the global needle-free injection system market is the rising adoption of devices for patient-friendly and pain-reducing drug delivery, particularly in chronic disease management, vaccination campaigns, and biologic therapies

- For instance, in 2024, PharmaJet’s needle-free injectors were deployed by the U.S. Centers for Disease Control and Prevention (CDC) for mass vaccination campaigns, enabling rapid and safe administration without traditional needles

- The increased focus on patient comfort and adherence is encouraging hospitals and clinics to switch from conventional syringes to needle-free systems, reducing fear and stress associated with injections

- Growing awareness about needle-stick injury prevention among healthcare professionals is motivating the adoption of these systems in clinical environments

- Needle-free devices support accurate dosing and minimize drug wastage, making them highly efficient for large-scale vaccination programs

- Home healthcare providers are increasingly recommending needle-free injectors for self-administration of insulin, vaccines, and other biologics

- Needle-free injection is gaining traction in pediatrics, as children are more likely to comply with pain-free drug delivery methods

- Pharmaceutical companies are partnering with device manufacturers to integrate needle-free technology into new drug formulations, improving patient experience

- The technology is also being incorporated into mobile health programs, allowing rapid and convenient administration during community health drives

- Regulatory bodies in Europe and North America are increasingly recognizing needle-free injectors as safe and effective alternatives, boosting market confidence and adoption

Needle-Free Injection System Market Dynamics

Driver

“Rising Demand for Safe and Efficient Drug Delivery”

- The prevalence of chronic diseases such as diabetes, autoimmune disorders, and infectious diseases is increasing the demand for painless and hygienic drug delivery systems

- For instance, in 2023, Becton Dickinson launched its BD Physioject needle-free injector for insulin delivery, allowing diabetic patients to self-administer medication with minimal discomfort and improved adherence

- Growing mass vaccination programs for influenza, COVID-19, and other preventable diseases are driving large-scale adoption of needle-free systems

- Hospitals and clinics prefer needle-free devices to minimize biohazard waste and reduce cross-contamination risks in high-volume settings

- Needle-free injection systems improve patient compliance and retention in long-term therapy, particularly for injectable biologics

- The convenience of faster administration allows healthcare staff to treat more patients in less time, improving operational efficiency

- Needle-free injectors are increasingly used in military and humanitarian health programs for rapid immunization campaigns

- Pharmaceutical firms are developing combination devices with integrated monitoring to track dosage history, enhancing patient safety

- Government initiatives to promote immunization and reduce injection-related injuries are directly supporting market growth

- The market is also benefiting from technological advances such as spring-powered and gas-powered injectors, which enhance precision, safety, and usability

Restraint/Challenge

“High Initial Costs and Regulatory Barriers”

- The high upfront cost of advanced needle-free injection devices compared to traditional syringes limits adoption, especially in emerging markets

- For instance, regulatory delays in India and Brazil in 2023 slowed the rollout of PharmaJet needle-free injectors despite high demand for mass vaccination programs

- Regulatory compliance with international standards such as ISO 11608 and local approvals adds complexity and increases time-to-market

- Limited reimbursement policies in certain regions make needle-free injectors less accessible to price-sensitive healthcare providers and patients

- Price sensitivity for biologics and vaccines in developing countries continues to pose adoption challenges

- Training healthcare personnel to operate needle-free injectors effectively is required to ensure proper administration and safety

- Some patients are initially hesitant to switch from conventional syringes due to lack of awareness or familiarity with the devices

- Distribution and supply chain challenges, particularly in rural and remote areas, can limit device accessibility

- Maintenance and calibration requirements for advanced devices can increase operational costs for clinics and hospitals

- Overcoming these barriers requires cost optimization, education for healthcare providers and patients, and faster regulatory approvals to facilitate widespread adoption of needle-free injection systems

Needle-Free Injection System Market Scope

The market is segmented on the basis of type, product, technology, source of power, usability, delivery site, application, and end-user.

• By Type

On the basis of type, the Needle-Free Injection System market is segmented into liquid-based needle-free injectors, projectile/depot-based needle-free injectors, and powder-based needle-free injectors. The liquid-based segment dominated the largest market revenue share of 45% in 2025, driven by its widespread use in hospitals and clinics for vaccine administration, insulin delivery, and biologics. Its high accuracy, safety, and patient comfort make it the preferred choice for healthcare providers. The segment benefits from regulatory approvals, proven efficacy, and compatibility with multiple drug formulations. Hospitals and specialty clinics favor liquid-based injectors due to their reliability and reduced risk of cross-contamination. Government immunization programs and global vaccination campaigns further strengthen market dominance. The liquid-based segment also gains momentum in research laboratories, where precise dosing is critical. Pharmaceutical companies prefer liquid-based systems for high-volume production, streamlined supply chains, and integration with automated dispensing technologies. Overall, the segment’s combination of clinical effectiveness, patient comfort, and scalability drives its leading position in the market.

The projectile/depot-based segment is expected to witness the fastest CAGR of 11.2% from 2026 to 2033, fueled by precision therapy applications in oncology, insulin delivery, and dermatology. Its benefits include controlled-dose administration, minimal pain, and targeted drug delivery. The segment is gaining traction in specialty clinics and research laboratories that require advanced delivery mechanisms. Rising adoption in emerging markets and increased investment in R&D are accelerating growth. Healthcare providers are increasingly adopting depot-based injectors for chronic disease management and biologic drugs. Ongoing clinical trials and technological innovation also support expansion. The segment’s versatility allows compatibility with multiple formulations, including vaccines, biologics, and small-molecule drugs. Pharmaceutical companies are developing portable depot-based systems for home-use patients, further driving market adoption. With rising awareness of non-invasive drug delivery, the segment is poised for rapid growth in the forecast period.

• By Product

On the basis of product, the Needle-Free Injection System market is segmented into fillable needle-free injectors and prefilled needle-free injectors. The prefilled segment accounted for the largest market revenue share of 50% in 2025, due to ease of use, accuracy, and minimized preparation errors. Prefilled injectors are preferred in hospitals and immunization centers for high-volume vaccination campaigns. They ensure consistency, reduce risk of dosing errors, and improve workflow efficiency. Pre-filled systems also provide enhanced patient safety, making them ideal for mass immunization programs. The segment is supported by government procurement programs, hospital supply agreements, and strong partnerships with pharmaceutical companies. Prefilled injectors are increasingly integrated with digital monitoring systems to track doses and administration records. The segment’s reliability, convenience, and regulatory compliance drive its market dominance. Prefilled injectors are also widely adopted in home-care settings for chronic conditions like diabetes. High awareness among clinicians about safety and workflow efficiency contributes to growth.

The fillable segment is projected to witness the fastest CAGR of 10.5% from 2026 to 2033, driven by demand for reusable, customizable dosing systems. Fillable injectors offer flexibility in drug volume, dosage customization, and cost-effectiveness, particularly in emerging markets. Adoption is increasing in research laboratories, hospitals, and specialty clinics. Technological innovations, such as automated refill mechanisms and smart dose monitoring, further boost growth. Fillable injectors are preferred in applications where multiple drug types or volumes are required. Rising awareness of environmental sustainability and reusable devices supports expansion. Healthcare providers are adopting fillable injectors for specialized therapies requiring precise dosing. Ongoing product development by manufacturers for ease of use and durability is accelerating adoption. The segment’s cost-effectiveness, adaptability, and technological innovations make it the fastest-growing product segment.

• By Technology

On the basis of technology, the market is segmented into jet-based, spring-based, laser-powered, and vibration-based needle-free injectors. Jet-based injectors dominated with a revenue share of 47% in 2025 due to high clinical adoption, proven dosing accuracy, and patient comfort. Jet injectors allow rapid, needle-free delivery of liquids into subcutaneous or intramuscular tissue. Hospitals and clinics prefer them for vaccines, insulin, and biologics due to their consistency and reliability. Jet-based systems are integrated with digital monitoring for dose tracking. Adoption in immunization campaigns and chronic care drives growth. They are widely manufactured and supported by regulatory approvals. Jet-based injectors reduce cross-contamination risk and enhance patient compliance. Their ease of use supports hospital workflows and high-volume administration. Pharmaceutical companies rely on jet-based systems for scalable drug delivery. The segment continues to dominate due to efficacy, reliability, and clinical acceptance.

Laser-powered injectors are expected to grow at the fastest CAGR of 12% from 2026 to 2033, fueled by innovations in pain-free drug delivery, precision dosing, and oncology applications. Laser-based systems offer minimally invasive administration with high patient comfort. Adoption is increasing in dermatology, oncology, and research laboratories. Technological improvements, clinical studies demonstrating safety, and rising demand for non-invasive delivery drive growth. Laser-powered injectors are increasingly supported by hospitals and specialty clinics. Manufacturers are developing portable, home-use laser injectors to expand applications. Integration with smart monitoring enhances usability. Regulatory approvals for new laser-based devices support market expansion. Laser technology’s accuracy, patient-centric design, and applicability across multiple therapies contribute to rapid growth.

• By Source of Power

On the basis of source of power, the market is segmented into spring-based and gas-propelled/air-forced injectors. The spring-based injectors segment dominated the largest revenue share of 42% in 2025, due to its simplicity, portability, and cost-effectiveness. Hospitals and clinics widely adopt spring-based systems for routine vaccination, insulin delivery, and biologic administration. These injectors are easy to operate, require minimal training, and are reliable in high-volume clinical environments. Their widespread availability and established supply chains ensure timely access across hospitals, clinics, and outpatient centers. Spring-based injectors are particularly favored for immunization campaigns and government vaccination programs. Their mechanical design eliminates dependency on electricity or compressed gas, enhancing usability in low-resource settings. Hospitals also prefer them for their consistent dose accuracy and low maintenance requirements. In addition, spring-based systems are compatible with a variety of drug formulations, making them versatile for multiple applications. Their affordability and robustness contribute to strong adoption in emerging markets as well. Pharmaceutical companies support spring-based injectors through bulk supply and service agreements. Overall, these factors establish spring-based systems as the preferred choice for clinical and institutional settings.

Gas-propelled/air-forced injectors are expected to witness the fastest CAGR of 11% from 2026 to 2033, driven by increasing demand for automated, high-pressure delivery systems in hospitals, research laboratories, and specialty clinics. These injectors enable precise drug targeting and rapid administration, making them ideal for vaccines, oncology treatments, and biologics. Technological innovations, including smart pressure control and adjustable dosing, enhance performance and expand clinical applications. Adoption is rising in emerging markets due to growing healthcare infrastructure and investments in advanced drug delivery solutions. Gas-propelled systems are increasingly used in home-care settings for chronic disease management, providing patients with efficient, non-invasive administration. The ability to deliver multiple drug formulations with high accuracy supports adoption in specialized therapies. Manufacturers are introducing portable, lightweight models to improve accessibility and ease of use. Regulatory approvals for automated and high-pressure systems further bolster market confidence. The combination of precision, versatility, and innovation ensures rapid growth of this segment throughout the forecast period.

• By Usability

On the basis of usability, the market is segmented into disposable and reusable needle-free injectors. Disposable injectors dominated with a 55% revenue share in 2025, owing to hygiene, infection control, and suitability for large-scale immunization programs. Hospitals, clinics, and home-care providers prefer disposable injectors for their convenience, ease of handling, and reduced cross-contamination risks. They are particularly popular in vaccination campaigns, outpatient procedures, and chronic disease management. Disposable systems eliminate cleaning and sterilization requirements, saving time and reducing operational costs. They are widely used in pediatric, geriatric, and home-care applications due to safety and convenience. Pharmaceutical companies favor disposable injectors for prefilled systems, which enhance dosing accuracy and patient compliance. The segment benefits from regulatory approvals and strong partnerships with healthcare institutions. Rising awareness of single-use medical devices also supports growth. Disposable injectors are available in multiple configurations and delivery mechanisms, meeting diverse clinical needs. Overall, hygiene, reliability, and convenience position disposable injectors as the market leader.

Reusable injectors are expected to witness the fastest CAGR of 9.8% from 2026 to 2033, driven by cost efficiency, sustainability, and adoption in chronic care and specialty treatments. Reusable systems are preferred in hospitals and research laboratories where multiple doses are administered with the same device, reducing long-term costs. Technological advancements, such as modular design, durable materials, and ease of sterilization, are accelerating adoption. Reusable injectors are compatible with various drug formulations, supporting flexibility in clinical applications. They are increasingly integrated with smart dose-tracking systems, ensuring accuracy and compliance. Manufacturers are focusing on ergonomics and portability to enhance usability. Home-care settings are adopting reusable injectors for insulin and biologics management, enabling self-administration. Rising awareness of environmental sustainability further drives growth. The segment is projected to expand in emerging markets as hospitals and clinics aim to reduce medical waste. Overall, durability, adaptability, and cost-effectiveness fuel rapid growth in reusable injectors.

• By Delivery Site

On the basis of delivery site, the market is segmented into subcutaneous, intramuscular, and intradermal injectors. Subcutaneous injectors held the largest revenue share of 48% in 2025, owing to their extensive use in insulin delivery, biologics, and vaccines. Hospitals and clinics adopt subcutaneous systems for chronic disease management and high-volume immunization campaigns. Subcutaneous injectors are preferred due to accuracy, minimal pain, and patient comfort. They support a wide range of drug formulations and dosing volumes. Adoption is reinforced by regulatory approvals and standard clinical protocols. Hospitals, specialty clinics, and home-care providers rely on these injectors for reliable and safe administration. They are particularly effective for repeated dosing and self-administration scenarios. The segment benefits from technological innovations such as prefilled, spring-based, and jet-based subcutaneous systems. Pharmaceutical companies actively promote subcutaneous injectors for high-volume delivery and patient compliance. Government vaccination initiatives and chronic care programs further strengthen demand. Overall, subcutaneous injectors maintain a dominant position due to versatility, safety, and clinical acceptance.

Intradermal injectors are expected to witness the fastest CAGR of 11.5% from 2026 to 2033, supported by innovations such as microneedles, precision dosing, and targeted vaccine delivery. Adoption is rising in specialty clinics, research laboratories, and home-care applications requiring minimal invasiveness. Intradermal injectors enable reduced drug volumes while achieving effective immunization or therapy outcomes. Rising demand for minimally invasive, patient-friendly devices is driving growth. Regulatory approvals for microneedle and intradermal technologies support adoption. Hospitals and clinics are incorporating these systems into vaccination campaigns and therapeutic applications. Pharmaceutical companies are investing in intradermal injectors for biologics and specialty drugs. Emerging markets are increasingly adopting intradermal delivery due to cost efficiency and targeted efficacy. Ongoing product innovations, such as adjustable depth and automated dose control, further accelerate growth. The segment’s precision, patient comfort, and clinical effectiveness ensure rapid adoption.

• By Application

On the basis of application, the market is segmented into vaccine delivery, insulin delivery, oncology, pain management, and others. Vaccine delivery dominated with 50% revenue share in 2025, driven by global immunization programs, high adoption in hospitals and clinics, and government initiatives. Vaccine injectors are preferred for their safety, accuracy, and patient compliance. Hospitals, research laboratories, and home-care providers rely on these systems for large-scale vaccination campaigns. Prefilled and disposable injectors enhance dosing accuracy, reduce contamination risk, and support workflow efficiency. Rising awareness of preventive healthcare and immunization programs further strengthens demand. The segment benefits from well-established supply chains, regulatory support, and integration with hospital protocols. Vaccine delivery systems are widely used in pediatric and adult populations across both developed and emerging markets. Technological improvements in automated, needle-free, and jet-based delivery systems increase adoption. Pharmaceutical companies actively develop prefilled vaccine injectors to meet growing global demand. Overall, vaccine delivery injectors maintain a stronghold due to high volume, regulatory support, and clinical necessity.

Oncology applications are expected to witness the fastest CAGR of 12.2% from 2026 to 2033, driven by targeted drug delivery, precision medicine, and minimally invasive administration. Needle-free injectors are increasingly used for biologics, chemotherapy, and immunotherapy in specialty clinics and hospitals. Adoption is supported by innovations in delivery mechanisms, such as jet-based, gas-propelled, and laser-powered systems. Home-care oncology applications are expanding due to patient convenience and reduced hospital visits. Pharmaceutical companies are developing oncology-specific injectors for safer and more efficient drug administration. Regulatory approvals and clinical trials demonstrate efficacy and safety, boosting adoption. Emerging markets are increasingly investing in oncology treatments, increasing injector demand. Intradermal and intramuscular delivery systems are particularly suitable for oncology therapies. Healthcare providers prioritize precision, dosing accuracy, and patient comfort. Ongoing R&D and integration with smart monitoring systems enhance usability. The combination of clinical necessity, patient-centric design, and technological advancement ensures rapid market growth.

• By End-User

On the basis of end-user, the market is segmented into hospitals, clinics, home-care settings, research laboratories, pharmaceutical and biotechnological companies, and others. Hospitals dominated with 46% revenue share in 2025, due to high patient volume, integration into clinical protocols, and large-scale immunization and therapy programs. Hospitals benefit from reliable supply chains, high-quality devices, and strong after-sales support. Adoption is reinforced by prefilled, disposable, and jet-based systems that support high-volume workflows. Hospitals also rely on needle-free systems for chronic care, oncology, and vaccine delivery. Compliance, accuracy, and patient safety make hospitals the preferred setting. The segment benefits from regulatory approvals, healthcare initiatives, and partnerships with pharmaceutical companies. In addition, hospitals often implement automated and connected devices to improve efficiency. The segment remains dominant due to established procurement processes and clinical trust.

Home-care settings are expected to witness the fastest CAGR of 10.8% from 2026 to 2033, driven by remote healthcare adoption, chronic disease management, and self-administration of insulin, vaccines, and biologics. Increasing awareness of patient autonomy, ease of use, and minimally invasive administration fuels growth. Prefilled, disposable, and portable systems support usability in home settings. Emerging markets are increasingly adopting home-care injectors due to affordability and accessibility. Integration with digital health applications for dose tracking enhances adoption. Technological innovations improve safety, dosing accuracy, and comfort. Government programs and telemedicine initiatives further support expansion. Rising chronic disease prevalence and aging populations boost demand. Convenience, safety, and technological support are driving rapid adoption in home-care applications.

Needle-Free Injection System Market Regional Analysis

- North America dominated the needle-free injection system market with the largest revenue share of 38.5% in 2025, driven by the high prevalence of chronic diseases, early adoption of advanced medical devices, and the presence of leading market players. For instance, in 2024, PharmaJet’s needle-free injectors were widely deployed across U.S. hospitals and clinics for influenza and COVID-19 vaccination campaigns, enabling faster and safer drug administration

- The widespread adoption is further supported by well-established healthcare infrastructure, high disposable incomes, and increasing patient preference for pain-free and hygienic drug delivery solutions. The availability of trained healthcare professionals skilled in needle-free system usage enhances market penetration across hospitals, outpatient centers, and home care. Continuous investment by leading players in R&D for advanced needle-free devices with improved accuracy and usability is further boosting the market. Government programs promoting immunization and chronic disease management are accelerating the adoption of needle-free systems

- Growing awareness of needle-stick injury prevention among healthcare workers is motivating hospitals to switch to needle-free injectors. Increasing integration of needle-free systems into clinical protocols ensures higher patient compliance and reduced medication errors. Expansion of home healthcare and self-administration programs for insulin and other biologics supports sustained growth. North America’s robust regulatory framework for medical devices ensures safety, reliability, and trust, further driving market expansion

U.S. Needle-Free Injection System Market Insight

The U.S. needle-free injection system market captured the largest revenue share within North America in 2025, fueled by increasing prevalence of chronic diseases, rising patient awareness, and growing adoption of advanced drug delivery devices. The market is supported by hospitals, clinics, and home care programs emphasizing patient-friendly and efficient medication administration. For instance, in 2023, Becton Dickinson launched its BD Physioject needle-free injector for self-administration of insulin, which gained rapid acceptance among diabetic patients due to its ease of use and reduced pain.

Europe Needle-Free Injection System Market Insight

The Europe needle-free injection system market is projected to expand at a substantial CAGR during the forecast period, driven by stringent healthcare regulations, increasing vaccination programs, and growing demand for minimally invasive drug delivery. For instance, in 2022, the French Ministry of Health initiated pilot programs using Bioject needle-free injectors for mass immunization campaigns, demonstrating improved efficiency and reduced medical waste. Urbanization and well-established healthcare infrastructure in Western Europe support broader adoption of needle-free systems. Hospitals and multi-specialty clinics increasingly prefer needle-free injectors to enhance patient comfort and reduce risk of cross-contamination. European governments are encouraging adoption through subsidies and public health programs targeting chronic disease management. The market is bolstered by partnerships between pharmaceutical companies and device manufacturers for new drug formulations compatible with needle-free delivery. Increasing awareness among patients regarding needle-stick injuries and hygiene drives the preference for needle-free systems. The convenience of self-administration for vaccines and biologics at home is further boosting market uptake. Training programs for healthcare professionals ensure correct use, safety, and compliance with local guidelines. Expansion in outpatient clinics, long-term care facilities, and vaccination centers is driving regional growth.

U.K. Needle-Free Injection System Market Insight

The U.K. needle-free injection system market is anticipated to grow at a noteworthy CAGR, driven by rising awareness of pain-free drug delivery, vaccination programs, and chronic disease management initiatives. For instance, in 2023, NHS pilot programs employed PharmaJet needle-free systems for school vaccination drives, ensuring faster coverage and minimizing needle-related anxiety among children. Adoption is supported by high patient acceptance and healthcare infrastructure that favors advanced drug delivery methods. Hospitals and home healthcare providers are integrating needle-free injectors for insulin and biologic therapies. Government programs emphasizing vaccination and safety are enhancing the market’s reach. Growing patient preference for minimally invasive therapies is motivating healthcare providers to shift from traditional syringes. Training programs for nurses and home care providers improve confidence and proper usage. Partnerships between pharmaceutical companies and needle-free system manufacturers expand product availability. High demand in pediatric care and chronic disease management further drives market growth. The trend toward self-administration and remote healthcare delivery supports long-term adoption.

Germany Needle-Free Injection System Market Insight

The Germany needle-free injection system market is expected to expand at a considerable CAGR due to a strong focus on innovative healthcare solutions and preventive medicine. For instance, in 2022, clinics in Berlin and Munich adopted Zogenix needle-free systems for biologics and vaccines, increasing patient throughput while reducing needle-related injuries. High patient awareness and preference for pain-free injections support market growth. Well-developed healthcare infrastructure and advanced hospital networks encourage adoption. Government support for vaccination and chronic disease initiatives strengthens market demand. Collaborations between pharmaceutical and device manufacturers enhance product offerings. Increasing use of needle-free systems in outpatient care and home healthcare settings drives penetration. Professional training and education programs for healthcare workers facilitate proper device use. Rising investments in research and development of advanced needle-free technologies improve device efficacy. Regulatory frameworks ensuring safety and quality boost market confidence.

Asia-Pacific Needle-Free Injection System Market Insight

The Asia-Pacific needle-free injection system market is poised to grow at the fastest CAGR of 9.3% during the forecast period (2026–2033), fueled by increasing healthcare awareness, government vaccination initiatives, and growing adoption of advanced drug delivery technologies. For instance, in 2023, India’s Ministry of Health launched pilot programs deploying PharmaJet needle-free injectors in rural vaccination drives, significantly reducing needle-associated injuries and enhancing coverage. Rapid urbanization and rising disposable incomes increase patient access to advanced healthcare devices. Expansion of hospitals, clinics, and home healthcare networks supports widespread adoption. Government campaigns for vaccination, particularly for influenza and COVID-19, encourage needle-free device usage. Pharmaceutical companies are increasingly collaborating with local device manufacturers to enhance distribution and affordability. Patient awareness campaigns emphasizing safety, hygiene, and pain reduction improve acceptance. The growing prevalence of chronic diseases, such as diabetes, boosts demand for insulin-compatible needle-free systems. Integration of devices into mobile health programs and community health initiatives expands market reach. APAC’s emerging manufacturing capabilities reduce costs and improve accessibility for wider populations.

Japan Needle-Free Injection System Market Insight

The Japan needle-free injection system market is gaining momentum due to high-tech healthcare infrastructure, aging population, and preference for convenient, minimally invasive drug delivery. For instance, in 2022, Japanese hospitals implemented PharmaJet needle-free injectors for routine influenza vaccination, improving patient compliance and throughput in urban clinics. Patient awareness about pain-free injections encourages adoption in hospitals and home care. Government health initiatives targeting chronic disease management drive usage. Integration with home healthcare programs enhances convenience for elderly patients. Pharmaceutical collaborations ensure compatible formulations for needle-free devices. Training programs for nurses and caregivers enhance correct device administration. Hospitals are adopting needle-free injectors to reduce biohazard waste and needle-stick incidents. Increased use in pediatrics and geriatric care supports market growth. Regulatory approvals for safety and efficacy bolster market confidence.

China Needle-Free Injection System Market Insight

The China needle-free injection system market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to rapid urbanization, rising middle-class healthcare spending, and high rates of technological adoption. For instance, in 2023, China CDC deployed PharmaJet needle-free injectors for influenza vaccination campaigns in multiple provinces, achieving faster administration and reduced medical waste. Growing patient preference for pain-free injections is driving hospital adoption. Government programs promoting mass immunization and preventive care support market expansion. Advanced hospital networks and clinics are increasing integration of needle-free injectors. Collaborations between global and domestic device manufacturers improve distribution and affordability. Rising incidence of chronic diseases like diabetes boosts the demand for needle-free insulin delivery. Adoption in outpatient care, community health programs, and school vaccination drives is increasing. Awareness campaigns on safe, hygienic drug delivery encourage self-administration. China’s position as a manufacturing hub ensures cost-effective production and broad accessibility.

Needle-Free Injection System Market Share

The Needle-Free Injection System industry is primarily led by well-established companies, including:

• PharmaJet (U.S.)

• Antares Pharma (U.S.)

• Zogenix (U.S.)

• Portal Instruments (U.S.)

• Bioject (U.S.)

• Crossject (France)

• Nanopass Technologies (Israel)

• Injex Pharma (Germany)

• Enable Injections (U.S.)

• Bespak (U.K.)

• West Pharmaceutical Services (U.S.)

• Vaxess Technologies (U.S.)

• RPS Pharma (U.S.)

• Medimetrics (France)

• ApiJect Systems (U.S.)

• Ferrosan Medical Devices (Denmark)

• MicronJet (Israel)

• PharmaJet Europe (Netherlands)

• Kindeva Drug Delivery (U.S.)

• Elcam Medical (Israel)

Latest Developments in Global Needle-Free Injection System Market

- In May 2022, Pulse NeedleFree Systems launched its first disposable needle‑free injector, aimed at livestock vaccination, offering a safe and effective alternative to traditional needles for animal health applications and expanding the use of needle‑free technology beyond human healthcare

- In August 2024, the U.S. Food and Drug Administration (FDA) approved Neffy, a needle‑free nasal spray epinephrine product developed by ARS Pharmaceuticals as an alternative to traditional epinephrine auto‑injectors, providing a user‑friendly needle‑free option for emergency anaphylaxis treatment

- In September 2023, PharmaJet formed strategic partnerships with more than 12 vaccine developers to deploy its needle‑free injection systems in mass vaccination trials, improving public acceptance and expanding adoption in regions with high needle phobia concerns

- In 2023, INJEX Pharma AG received pediatric certification for its needle‑free device line, enabling inclusion in European child immunization programs and helping reduce vaccination‑related distress among children in several pilot regions

- In January 2025, FlowBeams showcased its BoldJet needle‑free injection technology at CES 2025, a novel approach using controlled laser‑generated pressure to deliver medications and vaccines through the skin, recognized as an Innovation Awards honoree and demonstrating innovation toward painless, needle‑free drug delivery

- In May 2025, Crossject enhanced its production capabilities by implementing a new manufacturing module at its ZENEO Factory, preparing to scale up production of prefilled needle‑free injectors for emergency and chronic care applications

- In August 2025, NuGen Medical Devices Inc. announced development of a next‑generation needle‑free injection system with integrated internal cartridge technology, designed to improve patient safety and dosing precision while reducing contamination risk, with full commercialization anticipated after 2026 tooling investment

- In October 2025, PharmaJet initiated development of needle‑free self‑injector pens for home use, targeting chronic diseases and metabolic peptide therapies to improve patient compliance and reduce injection‑related anxiety and discomfort

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.