Global Parallel Computing Market

Размер рынка в млрд долларов США

CAGR :

%

USD

179.93 Billion

USD

281.42 Billion

2025

2033

USD

179.93 Billion

USD

281.42 Billion

2025

2033

| 2026 –2033 | |

| USD 179.93 Billion | |

| USD 281.42 Billion | |

| % | |

|

Сегментация глобального параллельного вычислительного рынка, по компонентам (программное обеспечение, аппаратное обеспечение и услуги), развертывание (облако, on-Premieses и Hybrid), вертикаль (BFSI, здравоохранение и науки о жизни, правительство, производство и автомобилестроение, IT & Telecom и другие), технологии (программные модели и API, ускорительная микроархитектура / ISA, технологии межсоединения и ткани, оркестровка и промежуточное программное обеспечение, библиотеки и ядра и другие) - отраслевые тенденции и прогноз до 2033 года

Что такое параллельный размер рынка и темпы роста

- Согласно анализу Data Bridge Market Research, размер глобального рынка параллельных вычислений оценивался как179,93 млрд долларов в 2025 годуОжидается, что он достигнет281,42 млрд долларов к 2033 году, вCAGR 5,75%в течение прогнозируемого периода

- Рост рынка в значительной степени обусловлен растущим спросом на высокопроизводительные вычисления в приложениях, требующих больших объемов данных.искусственный интеллектМашинное обучение и аналитика больших данных

- Растущее внедрение облачных вычислений, ускорение графического процессора и многоядерных процессоров на предприятиях и в научно-исследовательских институтах стимулирует рынок параллельных вычислений.

Размер рынка и прогноз

- Глобальная рыночная стоимость (2025):179,93 млрд долларов в 2025 году

- Ожидаемая рыночная стоимость (2033):281,42 млрд долларов к 2033 году

- Прогноз CAGR (2026–2033):5.75%

Параллельный анализ рынка вычислений

- Рынок параллельных вычислений демонстрирует значительный рост благодаря технологическим достижениям в области аппаратного и программного обеспечения, что позволяет быстрее вычислять и повышать эффективность.

- Растущее внимание к обработке данных в реальном времени, прогнозной аналитике и сложному моделированию в различных секторах способствует внедрению параллельных вычислительных систем.

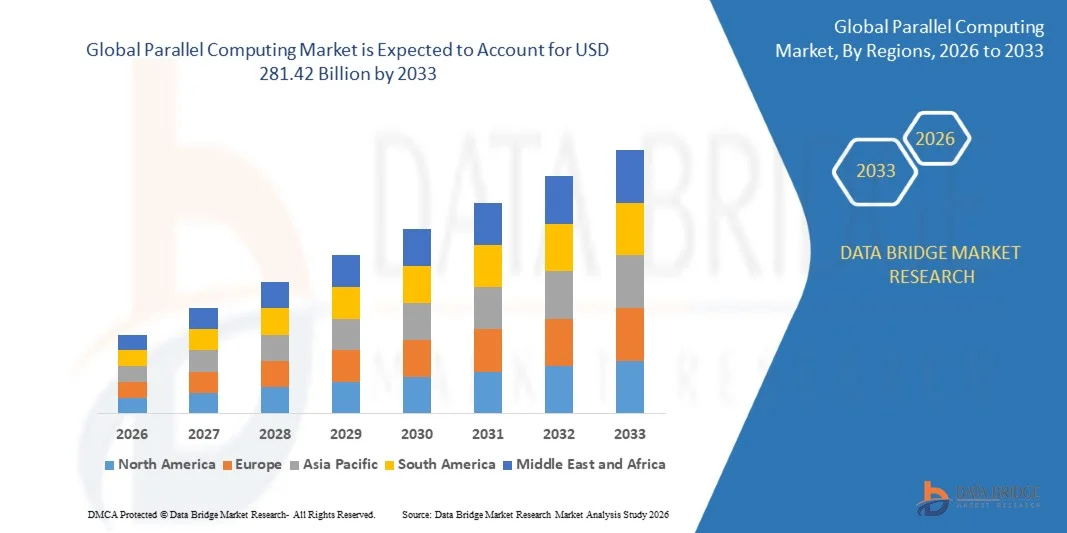

- Северная Америка доминировала на рынке параллельных вычислений с самой большой долей доходов в 28,3% в 2025 году, чему способствовало раннее внедрение высокопроизводительных вычислительных систем и увеличение инвестиций в ИИ, машинное обучение и аналитику данных на предприятиях.

- Ожидается, что в Азиатско-Тихоокеанском регионе будут наблюдаться самые высокие темпы роста в мире.параллельный компьютеррынок, обусловленный быстрой цифровизацией, растущими инвестициями в инфраструктуру ИИ и HPC, расширением облачных услуг и появлением технологических центров в Китае, Японии и Индии

- Сегмент аппаратного обеспечения занимал самую большую долю рынка в 57% в 2025 году, что обусловлено растущим спросом на высокопроизводительные вычислительные системы и специализированные процессоры, которые могут эффективно обрабатывать сложные вычисления. Аппаратные решения, включая GPU, CPU и FPGA, широко используются на предприятиях и в научно-исследовательских учреждениях для ускорения обработки данных и повышения общей производительности системы.

Сфера охвата отчетов и сегментация параллельного вычислительного рынка

|

Атрибуты |

Параллельные вычисления Key Market Insights |

|

Сегменты покрыты |

|

|

Страны, охваченные |

Северная Америка

Европа

Азиатско-Тихоокеанский регион

Ближний Восток и Африка

Южная Америка

|

|

Ключевые игроки рынка |

|

|

Рыночные возможности |

|

|

Информационные наборы данных с добавленной стоимостью |

В дополнение к рыночным идеям, таким как рыночная стоимость, темпы роста, сегменты рынка, географический охват, игроки рынка и рыночный сценарий, отчет о рынке, курируемый командой Data Bridge Market Research, включает углубленный экспертный анализ, анализ импорта / экспорта, анализ цен, анализ потребления продукции и анализ пестле. |

Каковы основные тенденции на рынке параллельных вычислений

«Растущее внедрение высокопроизводительных вычислений и аналитики больших данных»

- Растущая зависимость от высокопроизводительных вычислительных систем и аналитики больших данных значительно формирует рынок параллельных вычислений, поскольку организациям все чаще требуются более быстрые возможности обработки для сложных вычислений. Параллельные вычислительные архитектуры набирают обороты благодаря своей способности выполнять несколько задач одновременно, сокращая время обработки и повышая операционную эффективность. Эта тенденция усиливает их внедрение в ИТ, финансах, здравоохранении и научных исследованиях, побуждая поставщиков внедрять инновации с помощью новых масштабируемых и энергоэффективных решений.

- Повышение акцента на искусственный интеллект (ИИ), машинное обучение (ML) иоблачный сервисУскорил спрос на параллельные вычислительные системы. Предприятия и исследовательские учреждения используют параллельные вычисления для эффективной обработки больших наборов данных, что позволяет быстрее понять и улучшить процесс принятия решений. Растущая интеграция параллельных вычислений с ИИ-фреймворками также способствует развитию партнерских отношений между поставщиками аппаратного и программного обеспечения для повышения производительности и функциональности.

- Тенденции облачного развертывания и виртуализации влияют на решения о покупке, и компании ищут гибкие вычислительные ресурсы по требованию. Эти факторы помогают организациям оптимизировать затраты, повысить масштабируемость и ускорить выход на рынок, а также способствуют внедрению гибридных и многооблачных архитектур. Продавцы все чаще продвигают возможности параллельных вычислений, чтобы подчеркнуть эффективность и преимущества производительности, привлекая потребителей, ориентированных на технологии.

- Например, в 2024 году IBM в США и Fujitsu в Японии расширили свои суперкомпьютерные портфели, интегрировав передовые технологии параллельных вычислений для ИИ и научного моделирования. Эти обновления были введены для удовлетворения растущего спроса на более быструю обработку и более высокую вычислительную точность с развертыванием на корпоративных, исследовательских и облачных платформах. Продукты также продавались как энергоэффективные и высокопроизводительные решения, повышающие принятие клиентов и лояльность.

- В то время как спрос на параллельные вычисления растет, устойчивое расширение рынка зависит от непрерывных исследований и разработок, энергоэффективных проектов и экономически эффективного развертывания. Продавцы также сосредоточены на улучшении масштабируемости, интеграции программного обеспечения и разработке инновационных решений, которые уравновешивают производительность, стоимость и устойчивость для более широкого внедрения.

Параллельная динамика рынка вычислений

водитель

«Рост спроса на высокопроизводительные вычисления и аналитику больших данных»

- Растущие корпоративные и исследовательские требования к более быстрой обработке данных и высокопроизводительным вычислениям являются основным драйвером для рынка параллельных вычислений. Организации все чаще заменяют традиционные вычислительные системы параллельными архитектурами, чтобы повысить эффективность обработки и уменьшить задержку. Эта тенденция также поощряет исследования специализированных аппаратных ускорителей и оптимизированных параллельных алгоритмов, поддерживая диверсификацию рынка.

- Расширение приложений в области ИИ, машинного обучения, облачных вычислений, научного моделирования и финансового моделирования влияет на рост рынка. Параллельные вычисления позволяют одновременно выполнять задачи, сокращая время вычислений при сохранении точности и надежности. Растущее внедрение приложений с интенсивным использованием данных во всем мире еще больше усиливает эту тенденцию.

- Поставщики технологий активно продвигают решения параллельных вычислений посредством оптимизации программного обеспечения, аппаратных инноваций и партнерских отношений с экосистемами. Эти усилия поддерживаются растущим спросом предприятий на аналитику в реальном времени и прогнозное моделирование, а также поощряют сотрудничество между разработчиками программного обеспечения и производителями оборудования для повышения производительности системы и энергоэффективности.

- Например, в 2023 году NVIDIA в США и Atos во Франции сообщили об увеличении развертывания параллельных вычислительных рамок в обучении ИИ и высокопроизводительном моделировании. Это расширение последовало за более высоким спросом на более быструю обработку и вычислительную масштабируемость, что привело к принятию предприятия и конкурентной дифференциации. Обе компании также подчеркнули энергоэффективность и снижение операционных расходов в маркетинговых кампаниях для укрепления доверия и вовлеченности клиентов.

- Хотя растущие тенденции HPC и ИИ поддерживают рост, более широкое внедрение зависит от оптимизации затрат, энергоэффективных проектов и совместимости с существующей ИТ-инфраструктурой. Инвестиции в масштабируемые системы, передовую разработку программного обеспечения и интеграцию с облачными платформами будут иметь решающее значение для удовлетворения глобального спроса и сохранения конкурентных преимуществ.

Сдержанность/вызов

«Высокие затраты на внедрение и техническая сложность»

- Относительно высокая стоимость параллельного вычислительного оборудования и программного обеспечения по сравнению с обычными системами остается ключевой проблемой, ограничивая внедрение среди чувствительных к цене предприятий. Специализированные процессоры, межсоединения и программные фреймворки способствуют увеличению капитальных затрат, влияя на проникновение на рынок в развивающихся регионах. Организации могут отложить принятие из-за бюджетных ограничений и неопределенности ROI.

- Техническая сложность и ограниченность квалифицированной рабочей силы также влияют на рост рынка, поскольку параллельные вычисления требуют опыта в моделях программирования, оптимизации алгоритмов и системной интеграции. Ограниченная доступность подготовленных специалистов может замедлить развертывание, особенно в развивающихся странах, где ИТ-инфраструктура все еще развивается.

- Потребности в инфраструктуре и энергопотребление препятствуют дальнейшему внедрению, поскольку высокопроизводительные параллельные системы требуют значительных энергетических и охлаждающих ресурсов. Дата-центры должны оптимизировать физическое пространство, сети и управление тепловой энергией, увеличивая эксплуатационные расходы.

- Например, в 2024 году несколько исследовательских учреждений в Юго-Восточной Азии и Латинской Америке сообщили о замедлении развертывания кластеров параллельных вычислений из-за высоких затрат на оборудование, ограничений мощности и ограниченного технического опыта, что повлияло на общее использование системы и сроки реализации проекта.

- Преодоление этих проблем потребует инвестиций в экономичное оборудование, энергоэффективные конструкции и учебные программы для создания квалифицированных технических ресурсов. Сотрудничество с поставщиками облачных услуг, образовательными учреждениями и технологическими партнерами может помочь раскрыть долгосрочный потенциал роста глобального рынка параллельных вычислений. Кроме того, разработка гибридных решений и удобных для пользователя рамок будет иметь важное значение для широкого распространения.

Сфера параллельного вычислительного рынка

Рынок сегментирован на основе компонентов, развертывания, вертикали и технологий.

- Компонент

На основе компонента рынок параллельных вычислений сегментирован на программное обеспечение, аппаратное обеспечение и услуги. Сегмент аппаратного обеспечения занимал самую большую долю рынка в 57% в 2025 году, что обусловлено растущим спросом на высокопроизводительные вычислительные системы и специализированные процессоры, которые могут эффективно обрабатывать сложные вычисления. Аппаратные решения, включая GPU, CPU и FPGA, широко используются на предприятиях и в научно-исследовательских учреждениях для ускорения обработки данных и повышения общей производительности системы.

Ожидается, что в сегменте программного обеспечения будут наблюдаться самые быстрые темпы роста с 2026 по 2033 год, обусловленные растущей потребностью в оптимизированных параллельных вычислительных средах, моделях программирования и API, которые позволяют эффективно распределять рабочую нагрузку и выполнять задачи. Программные решения облегчают масштабируемость, сокращают время вычислений и обеспечивают бесшовную интеграцию с облачными платформами, что делает их очень ценными для ИИ, аналитики больших данных и научного моделирования.

- путем развертывания

На основе развертывания рынок сегментирован на облачный, локальный и гибридный. Облачный сегмент занимал самую большую долю в 2025 году благодаря своей гибкости, масштабируемости и экономической эффективности для предприятий, стремящихся к высокопроизводительным вычислительным возможностям, не вкладывая значительные средства в физическую инфраструктуру. Облачные параллельные вычисления позволяют организациям получать доступ к мощным ресурсам по требованию, поддерживая более быструю аналитику и рабочие нагрузки ИИ.

Ожидается, что в гибридном сегменте будет наблюдаться самый быстрый рост с 2026 по 2033 год, чему способствует растущая потребность организаций в балансе локальной инфраструктуры с облачными возможностями. Гибридное развертывание обеспечивает эффективное управление рабочей нагрузкой, улучшенную безопасность и лучшую оптимизацию затрат, что делает его предпочтительным выбором для предприятий со сложными вычислительными требованиями.

- Вертикальный

На основе вертикали рынок сегментирован на BFSI, здравоохранение и науки о жизни, правительство, производство и автомобилестроение, ИТ и телекоммуникации и другие. Вертикаль ИТ и телекоммуникаций занимала самую большую долю рынка в 23,2% в 2025 году, чему способствовало широкое внедрение параллельных вычислений для центров обработки данных, приложений на основе ИИ и крупномасштабного управления сетью. Параллельные вычисления позволяют этим секторам быстро обрабатывать массивные наборы данных и улучшать доставку услуг.

Ожидается, что вертикаль здравоохранения и наук о жизни будет наблюдать самый быстрый рост с 2026 по 2033 год из-за растущей потребности в параллельных вычислениях в геномике, открытии лекарств и медицинских приложениях для визуализации. Расширенные вычислительные возможности помогают ускорить исследования, сократить время анализа и поддерживать персонализированные решения в области здравоохранения.

- По технологии

На основе технологий рынок сегментирован на модели программирования и API, ускорительную микроархитектуру / ISA, технологии межсоединения и ткани, оркестровку и промежуточное ПО, библиотеки и ядра и другие. Сегмент ускорительной микроархитектуры / ISA занимал самую большую долю в 2025 году, чему способствовало растущее развертывание GPU, TPU и FPGA, которые значительно повышают скорость и эффективность вычислений.

Ожидается, что в сегменте моделей программирования и API будут наблюдаться самые быстрые темпы роста с 2026 по 2033 год, обусловленные потребностью в стандартизированных инструментах разработки и эффективном распределении рабочей нагрузки по архитектурам параллельных вычислений. Эти технологии упрощают разработку, повышают производительность и обеспечивают бесшовную интеграцию с облачными и локальными средами, поддерживая приложения AI, ML и HPC.

В каком регионе находится наибольшая доля рынка параллельных вычислений

- Северная Америка доминировала на рынке параллельных вычислений с самой большой долей доходов в 28,3% в 2025 году, чему способствовало раннее внедрение высокопроизводительных вычислительных систем и увеличение инвестиций в ИИ, машинное обучение и аналитику данных на предприятиях.

- Сильная ИТ-инфраструктура региона, присутствие крупных поставщиков технологий и высокий спрос на облачные услуги способствуют росту.

- Компании и исследовательские институты все больше полагаются на параллельные вычисления для сложных симуляций, обработки данных и научных исследований, что делает Северную Америку ключевым центром для расширения рынка.

Американский рынок параллельных вычислений Insight

Американский рынок параллельных вычислений занял самую большую долю доходов в 2025 году в Северной Америке, чему способствовало лидерство страны в облачных вычислениях, внедрении ИИ и суперкомпьютерной инфраструктуре. Организации в секторах BFSI, здравоохранения, производства и государственного управления интегрируют параллельные вычисления для повышения вычислительной эффективности, сокращения времени обработки и ускорения инноваций. Присутствие ведущих поставщиков оборудования и программного обеспечения наряду с постоянными инвестициями в исследования и разработки укрепляет позиции США на мировом рынке параллельных вычислений.

Европа Параллельное понимание рынка вычислений

Ожидается, что на европейском рынке параллельных вычислений будут наблюдаться самые быстрые темпы роста с 2026 по 2033 год, обусловленные ростом цифровизации, ростом внедрения ИИ и больших данных и правительственными инициативами, поддерживающими высокопроизводительные вычисления. Регион сосредоточен на модернизации ИТ-инфраструктуры в различных отраслях, включая автомобилестроение, здравоохранение и производство. Европейские предприятия все чаще используют параллельные вычислительные системы для расширения возможностей обработки данных, поддержки исследований и оптимизации промышленных операций.

Параллельное понимание рынка вычислений в Великобритании

Прогнозируется, что рынок параллельных вычислений в Великобритании будет быстро расти с 2026 по 2033 год, чему способствуют достижения в области искусственного интеллекта, машинного обучения и внедрения облачных вычислений. Увеличение инвестиций в финтех, аналитику здравоохранения и государственные исследовательские программы способствует расширению рынка. Интеграция решений параллельных вычислений повышает вычислительную скорость, точность и эффективность, удовлетворяя растущий спрос на принятие решений на основе данных и расширенное моделирование как в государственном, так и в частном секторах.

Германия Параллельное понимание рынка вычислений

Ожидается, что рынок параллельных вычислений в Германии будет значительно расти с 2026 по 2033 год, чему способствуют надежные инициативы в области НИОКР, промышленная автоматизация и спрос на высокопроизводительные вычисления в производственном и автомобильном секторах. Хорошо развитая технологическая экосистема Германии и акцент на инновации позволяют предприятиям использовать параллельные вычисления для оптимизации процессов, моделирования и прогнозной аналитики. Растущее внедрение облачных решений HPC еще больше ускоряет расширение рынка в стране.

Азиатско-Тихоокеанский параллельный расчетный рынок

Ожидается, что на Азиатско-Тихоокеанском рынке параллельных вычислений будут наблюдаться самые быстрые темпы роста с 2026 по 2033 год, чему способствует увеличение инвестиций в ИИ, облачную инфраструктуру и цифровую трансформацию в Китае, Японии, Индии и Южной Корее. Регион испытывает растущий спрос на высокопроизводительные вычисления в ИТ-услугах, научно-исследовательских институтах и промышленных приложениях. Кроме того, появление APAC в качестве производственного и технологического центра для вычислительного оборудования и программного обеспечения способствует доступности и принятию решений для параллельных вычислений.

Японский рынок параллельных вычислений

Японский рынок параллельных вычислений, по прогнозам, будет быстро расти с 2026 по 2033 год из-за сильного внимания страны к ИИ, робототехнике и суперкомпьютерным инициативам. Японские предприятия все чаще используют параллельные вычисления для передовых симуляций, научных исследований и приложений с интенсивным использованием данных. Ожидается, что инвестиции в инфраструктуру HPC, облачные вычисления и проекты в области НИОКР будут способствовать расширению рынка, особенно в секторах производства, здравоохранения и государственных исследований.

Китай Параллельное понимание рынка вычислений

Китайский рынок параллельных вычислений составил самую большую долю доходов в Азиатско-Тихоокеанском регионе в 2025 году, чему способствовали расширение ИТ-инфраструктуры страны, быстрая оцифровка и растущее внедрение облачных и высокопроизводительных вычислительных систем. Растущее внимание к ИИ, аналитике больших данных и промышленной автоматизации поддерживает рост рынка. Сильные правительственные инициативы, инвестиции в суперкомпьютерные центры и доступность экономически эффективного вычислительного оборудования способствуют дальнейшему развитию рынка в Китае.

Какие компании занимают лидирующие позиции на рынке параллельных вычислений

Индустрия параллельных вычислений в основном возглавляется хорошо зарекомендовавшими себя компаниями, в том числе:

- Amazon Web Services, Inc.(США)

- Apple Inc. (США)

- Atos SE(Великобритания)

- Dell Inc. (США)

- Фудзицу(Великобритания)

- Hewlett Packard Enterprise Development LP (США)

- Корпорация IBM (США)

- Intel Corporation (США)

- Microsoft (США)

- NVIDIA Corporation (США)

Каковы последние события на рынке параллельных вычислений

- В марте 2025 года Quantum Machines запустила программу NVIDIA DGX Quantum Early Customer Program, представив плотно интегрированную квантово-классическую вычислительную платформу. Решение сочетает модульную систему квантового управления OPX1000 от Quantum Machines с суперчипами GH200 Grace Hopper от NVIDIA, обеспечивая сверхнизкую задержку менее 4 микросекунд между квантовым управлением и суперкомпьютерами AI. Эта инновация повышает вычислительную эффективность для квантовых и ИИ-нагрузок, позиционируя компанию на переднем крае гибридных вычислительных решений и укрепляя ее присутствие на рынках высокопроизводительных вычислений.

- В ноябре 2024 года Eviden, входящая в группу Atos, представила BXI v3, европейскую технологию масштабирования третьего поколения, предназначенную для рабочих нагрузок ИИ и HPC. Разработанный совместно с Французской комиссией по атомной энергии (CEA), он интегрирует технологию SmartNIC и разгрузку протоколов приложений для оптимизации использования процессоров и графических процессоров, улучшая скорость выполнения приложений до 35% при одновременном снижении общей стоимости владения. Эта разработка устраняет сетевые узкие места, повышая производительность и эффективность для приложений ИИ и высокопроизводительных вычислений

- В ноябре 2023 года Fujitsu представила новую технологию для динамичной оптимизации использования CPU и GPU в режиме реального времени, уделяя приоритетное внимание процессам с более высокой эффективностью исполнения. Интегрированная в будущего брокера рабочей нагрузки на основе ИИ, эта инновация помогает распределять вычислительные ресурсы на основе таких факторов, как время вычислений, точность и стоимость. Технология направлена на облегчение глобального дефицита графических процессоров, вызванного растущим спросом на генеративный ИИ и глубокое обучение, повышение производительности и эффективности в рабочих нагрузках ИИ и HPC, а также обеспечение более экономичного управления ресурсами.

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.