Global Spine Surgery Robots Market

Размер рынка в млрд долларов США

CAGR :

%

USD

230.00 Million

USD

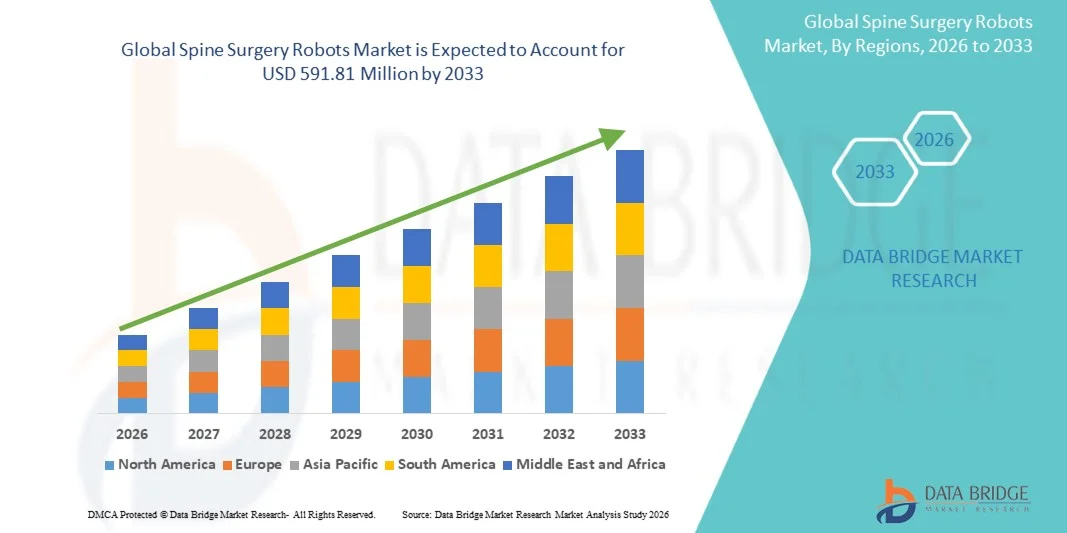

591.81 Million

2025

2033

USD

230.00 Million

USD

591.81 Million

2025

2033

| 2026 –2033 | |

| USD 230.00 Million | |

| USD 591.81 Million | |

| % | |

|

Global Spine Surgery Robots Market Segmentation, By Method (Minimally Invasive Surgery and Open Surgery), Product (Systems, Accessories and Consumables), End User (Hospitals and Ambulatory Surgical Centers), Approach (Anterior Approach, Posterior Approach, and Lateral Approach), Condition (Degenerative Disc Disease, Disc Herniation , Fractures, Tumors, Infections, and Instability, Deformity), Application (Laminectomy, Spinal Fusion, Forminatomy, Interlaminar Implant, Artificial Disc Replacement, Anterior Cervical Discectomy, Epidural lysis of adhesions, Laminotomy, OLLIF, Percutaneous Vetrebroplasty, Chronic Back Pain, and Spinal Stenosis)- Industry Trends and Forecast to 2033

Каков размер рынка роботов для хирургии позвоночника и темпы роста

- Согласно анализу Data Bridge Market Research, глобальный размер рынка роботов для хирургии позвоночника был оценен как230,00 млн долларов США в 2025 годуОжидается, что он достигнет591,81 млн долларов США к 2033 году, вCAGR 12,54%в течение прогнозируемого периода

- Рост рынка в значительной степени обусловлен растущим внедрением роботизированных хирургических систем и непрерывными технологическими достижениями в минимально инвазивных процедурах позвоночника, улучшая хирургическую точность и результаты лечения пациентов.

- Кроме того, растущий спрос на точное размещение имплантатов, снижение хирургических осложнений и более быстрое восстановление пациентов создает роботизированные системы в качестве передового решения для современной хирургии позвоночника. Эти сходящиеся факторы ускоряют внедрение роботов для хирургии позвоночника, тем самым значительно повышая рост отрасли.

Размер рынка и прогноз

Глобальная рыночная стоимость(2025) USD 230,00 млн.

Ожидаемая рыночная стоимость(2033) USD 591,81 млн.

Прогноз CAGR(2026–2033): 12,54%

Роботы хирургии позвоночника анализ рынка

- Роботы для хирургии позвоночника, предназначенные для оказания помощи хирургам в выполнении сложных спинальных процедур с повышенной точностью и контролем, становятся все более важными в современных хирургических средах в больницах и специализированных центрах позвоночника из-за их способности поддерживать минимально инвазивные процедуры, повышать точность имплантатов и улучшать хирургические результаты.

- Растущий спрос на роботов для хирургии позвоночника в первую очередь подпитывается растущей распространенностью заболеваний позвоночника, растущим предпочтением минимально инвазивных хирургических методов и непрерывными технологическими достижениями в роботизированных хирургических системах.

- Северная Америка доминировала на рынке роботов для хирургии позвоночника с самой большой долей дохода в 41,3% в 2025 году, характеризующейся передовой инфраструктурой здравоохранения, высоким внедрением роботизированной хирургии и сильным присутствием ведущих медицинских технологических компаний, при этом в США наблюдался значительный рост роботизированных процедур позвоночника, обусловленный увеличением инвестиций в хирургические инновации и внедрение передовых роботизированных платформ в больницах.

- Ожидается, что Азиатско-Тихоокеанский регион станет самым быстрорастущим регионом на рынке роботов для хирургии позвоночника в течение прогнозируемого периода из-за расширения инфраструктуры здравоохранения, роста расходов на здравоохранение и растущего внедрения передовых хирургических технологий в странах с развивающейся экономикой.

- Сегмент минимально инвазивной хирургии доминировал на рынке роботов для хирургии позвоночника с долей рынка 44,8% в 2025 году, что обусловлено его способностью улучшать хирургическую точность, уменьшать осложнения и поддерживать более быстрое восстановление пациентов по сравнению с обычными методами хирургии позвоночника.

Сегментация рынка роботов для хирургии позвоночника

|

Атрибуты |

Роботы хирургии позвоночника — ключевые рыночные идеи |

|

Сегменты покрыты |

|

|

Страны, охваченные |

Северная Америка

Европа

Азиатско-Тихоокеанский регион

Ближний Восток и Африка

Южная Америка

|

|

Ключевые игроки рынка |

|

|

Рыночные возможности |

|

|

Информационные наборы данных с добавленной стоимостью |

В дополнение к информации о рыночных сценариях, таких как рыночная стоимость, темпы роста, сегментация, географический охват и основные игроки, рыночные отчеты, курируемые Data Bridge Market Research, также включают углубленный экспертный анализ, эпидемиологию пациентов, анализ трубопроводов, анализ цен и нормативную базу. |

Каковы основные тенденции на рынке роботов для хирургии позвоночника

«Интеграция навигационных систем с искусственным интеллектом и систем визуализации в реальном времени»

- Значительной и ускоряющейся тенденцией на мировом рынке роботов для хирургии позвоночника является интеграцияискусственный интеллект- управляемые навигационные системы и технологии интраоперационной визуализации в режиме реального времени. Эта комбинация значительно улучшает хирургическую точность, точность планирования и общие клинические результаты в сложных процедурах позвоночника.

- Например, Medtronic plc предлагает роботизированную систему наведения Mazor X Stealth Edition, которая объединяет передовые технологии навигации и визуализации, чтобы помочь хирургам с точным размещением имплантатов и хирургическим планированием во время спинальных процедур.

- Интеграция ИИ в роботах для хирургии позвоночника обеспечивает такие функции, как автоматизированное хирургическое планирование, анатомическое картирование в реальном времени иПрогнозная аналитикаЭто помогает хирургам оптимизировать стратегии процедуры и повысить точность операции. Например, некоторые роботизированные платформы используют алгоритмы машинного обучения для анализа данных визуализации пациентов и рекомендуют оптимальные траектории для размещения винта. Кроме того, расширенные возможности визуализации позволяют хирургам непрерывно контролировать хирургический прогресс и вносить корректировки, основанные на данных, во время процедур.

- Бесшовная интеграция роботизированных платформ с хирургическим навигационным программным обеспечением и системами визуализации облегчает скоординированное управление несколькими хирургическими инструментами в среде операционной. Благодаря единому цифровому интерфейсу хирурги могут управлять роботизированным руководством, обратной связью с изображениями и данными хирургического планирования, создавая более эффективный и технологически продвинутый хирургический рабочий процесс.

- Эта тенденция к более интеллектуальным, точным и взаимосвязанным роботизированным хирургическим системам коренным образом меняет ожидания в отношении технологий хирургии позвоночника. Следовательно, такие компании, как Globus Medical, Inc. разрабатывают роботизированные системы, такие как ExcelsiusGPS, которые сочетают робототехнику, навигацию и технологии визуализации для повышения хирургической точности и эффективности рабочего процесса.

- Спрос на роботов для хирургии позвоночника с интегрированными возможностями навигации и визуализации на основе ИИ быстро растет в больницах и специализированных центрах позвоночника, поскольку поставщики медицинских услуг все чаще отдают приоритет улучшенной хирургической точности, безопасности пациентов и минимально инвазивным подходам к лечению.

- Растущие инвестиции в исследования и разработки для роботизированных платформ следующего поколения способствуют внедрению более точных, компактных и удобных для пользователя роботизированных хирургических систем.

Роботы спинной хирургии Динамика рынка

водитель

«Увеличение спроса на минимально инвазивные и точные операции на позвоночнике»

- Растущая распространенность заболеваний позвоночника, таких как дегенеративные заболевания дисков и деформации позвоночника, наряду с растущим предпочтением минимально инвазивных хирургических процедур, является значительным фактором для растущего внедрения роботов для хирургии позвоночника.

- Например, в июне 2024 года Stryker Corporation расширила возможности своей платформы Mako Spine Platform, стремясь улучшить роботизированные решения для хирургии позвоночника с улучшенными функциями навигации и планирования. Ожидается, что такие стратегии ключевых компаний будут стимулировать рост индустрии роботов для хирургии позвоночника в прогнозируемый период.

- Поскольку медицинские работники все больше сосредотачиваются на улучшении хирургической точности и результатов лечения пациентов, роботизированные системы позволяют хирургам выполнять сложные спинальные процедуры с повышенной точностью, стабильностью и визуализацией по сравнению с обычными хирургическими методами.

- Кроме того, растущие инвестиции в передовые технологии здравоохранения и расширение программ роботизированной хирургии в больницах делают роботов-хирургов позвоночника важным компонентом современной хирургической инфраструктуры.

- Способность роботизированных платформ поддерживать точное позиционирование имплантатов, уменьшать хирургические осложнения и минимизировать повреждение тканей способствует их внедрению как в академических медицинских центрах, так и в специализированных ортопедических больницах. Тенденция к технологически продвинутым операционным и растущая доступность программ подготовки хирургов способствуют росту рынка.

- Кроме того, повышение осведомленности среди хирургов о преимуществах роботизированной хирургии позвоночника способствует более высокому уровню внедрения в передовых медицинских учреждениях.

- Растущее число операций на позвоночнике во всем мире из-за старения населения и связанных с образом жизни заболеваний позвоночника еще больше ускоряет спрос на хирургические технологии с роботизированной помощью.

Сдержанность/вызов

«Высокие системные затраты и операционная сложность, ограничивающая принятие»

- Опасения, связанные с высокими капитальными вложениями, необходимыми для роботизированных хирургических систем, наряду с операционными сложностями, связанными с их внедрением, представляют собой серьезную проблему для более широкого проникновения на рынок. Поскольку роботы для хирургии позвоночника используют сложное оборудование, системы визуализации и специализированные требования к обучению, больницы могут столкнуться с финансовыми и операционными барьерами для внедрения.

- Например, поставщики медицинских услуг в чувствительных к затратам регионах могут отложить инвестиции в роботизированные хирургические платформы из-за значительных затрат на приобретение и обслуживание, связанных с передовыми роботизированными системами.

- Решение этих финансовых и операционных проблем с помощью экономически эффективных систем, гибких моделей финансирования и расширенных программ обучения хирургов имеет решающее значение для поощрения более широкого внедрения. Такие компании, как Zimmer Biomet Holdings, Inc., уделяют особое внимание обучению хирургов и оптимизации рабочих процессов в своих программах роботизированной хирургии для поддержки поставщиков медицинских услуг в эффективной интеграции роботизированных технологий. Кроме того, кривая обучения, связанная с роботизированными процедурами позвоночника, может первоначально замедлить хирургические рабочие процессы, особенно в учреждениях с ограниченным опытом роботизированной хирургии.

- В то время как технологические достижения продолжают улучшать удобство использования и эффективность, сложность роботизированных платформ все еще может ограничить внедрение в небольших больницах или медицинских учреждениях с ограниченными ресурсами.

- Преодоление этих проблем с помощью технологических инноваций, комплексных учебных инициатив и стратегий снижения затрат будет иметь важное значение для обеспечения устойчивого роста на мировом рынке роботов для хирургии позвоночника.

- Ограниченная политика возмещения расходов на хирургические процедуры с роботизированной поддержкой в некоторых системах здравоохранения может помешать больницам инвестировать в дорогие роботизированные платформы.

- Кроме того, потребность в специализированной подготовке и квалифицированных хирургических командах для эффективного управления роботизированными системами может создать рабочие и операционные проблемы для поставщиков медицинских услуг.

Роботы хирургии позвоночника рыночный охват

Рынок сегментируется на основе метода, продукта, конечного пользователя, подхода, состояния и применения.

- По методу

На основе метода рынок роботов для хирургии позвоночника сегментирован на минимально инвазивную хирургию и открытую хирургию. Сегмент минимально инвазивной хирургии доминировал на рынке с самой большой долей выручки в 44,8% в 2025 году, что обусловлено растущим внедрением хирургических систем с роботизированной поддержкой, которые обеспечивают меньшие разрезы, улучшенную точность и снижение кровопотери во время спинальных процедур. Больницы и центры позвоночника все чаще используют роботизированные платформы для выполнения минимально инвазивных процедур из-за их способности улучшать точность операции и сокращать время восстановления пациентов. Роботизированные системы также поддерживают точное размещение имплантатов и навигацию в режиме реального времени, что особенно ценно при минимально инвазивных подходах. Кроме того, предпочтение пациентов процедурам, связанным с более коротким пребыванием в больнице и более быстрой реабилитацией, ускоряет принятие. Интеграция роботизированных систем наведения с технологиями визуализации и навигации также усиливает рост минимально инвазивных операций на позвоночнике.

Сегмент открытой хирургии, как ожидается, будет наблюдать самый быстрый рост в течение прогнозируемого периода, в первую очередь из-за его постоянной важности в лечении очень сложных спинальных состояний, таких как серьезные деформации, опухоли и многоуровневые спинальные расстройства. Некоторые продвинутые процедуры позвоночника по-прежнему требуют открытых хирургических методов, где хирурги должны иметь прямой доступ к позвоночнику. Роботизированная помощь в открытых операциях помогает повысить точность размещения винта и хирургического планирования даже в сложных процедурах. Кроме того, достижения в области роботизированной навигации и интраоперационных технологий визуализации улучшают результаты в открытых спинальных процедурах. Растущее число сложных операций на позвоночнике во всем мире еще больше поддерживает спрос на роботизированные системы в открытых хирургических приложениях. Поскольку поставщики медицинских услуг продолжают внедрять роботизированные системы в различных хирургических процедурах, ожидается, что роль роботизированной помощи в операциях на открытом позвоночнике будет неуклонно расширяться.

- По продукту

На основе продукта рынок роботов для хирургии позвоночника сегментирован на системы и аксессуары и расходные материалы. Сегмент систем доминировал на рынке с наибольшей долей выручки в 2025 году, чему способствовала растущая установка роботизированных хирургических платформ в больницах и специализированных центрах позвоночника. Эти роботизированные системы обеспечивают интегрированные возможности, такие как хирургическое планирование, навигация и роботизированное руководство руками, которые помогают хирургам во время спинальных процедур. Больницы вкладывают значительные средства в передовые роботизированные системы для повышения хирургической точности и улучшения результатов лечения пациентов. Растущее внедрение технологически продвинутых операционных комнат и программ роботизированной хирургии также способствует росту этого сегмента. Кроме того, инновации в роботизированном оборудовании и навигационном программном обеспечении постоянно улучшают возможности этих систем. Расширение инфраструктуры здравоохранения в развитых странах также способствует внедрению передовых роботизированных систем.

Ожидается, что сегмент аксессуаров и расходных материалов станет свидетелем самого быстрого роста в течение прогнозируемого периода, чему будет способствовать постоянный спрос на хирургические инструменты, одноразовые компоненты и вспомогательные аксессуары, используемые с роботизированными платформами. Эти продукты включают хирургические инструменты, роботизированные инструменты и специализированные компоненты, необходимые во время каждой процедуры. Поскольку число операций на позвоночнике с помощью роботов растет во всем мире, спрос на расходные материалы и аксессуары продолжает расти. Больницы также требуют периодической замены роботизированных инструментов и компонентов для поддержания хирургических характеристик и стандартов безопасности. Повторяющийся характер этих продуктов создает постоянный поток доходов для производителей. Кроме того, ожидается, что расширение программ роботизированной хирургии в медицинских учреждениях значительно увеличит спрос на аксессуары и расходные материалы.

- Конечный пользователь

На базе конечного пользователя рынок роботов для хирургии позвоночника сегментирован на больницы и амбулаторные хирургические центры. Сегмент больниц доминировал на рынке с наибольшей долей выручки в 2025 году, в первую очередь из-за наличия передовой хирургической инфраструктуры и более высокой инвестиционной емкости для роботизированных систем. Больницы являются основными приверженцами роботизированных технологий, поскольку они выполняют большое количество сложных операций на позвоночнике, требующих точности и передового хирургического оборудования. Кроме того, больницы часто имеют многопрофильные хирургические команды и специализированные отделы, которые поддерживают роботизированные процедуры. Наличие опытных хирургов и комплексных учреждений послеоперационного ухода также укрепляет доминирование больниц на рынке. Многие медицинские учреждения активно интегрируют программы роботизированной хирургии для улучшения хирургических результатов и привлечения пациентов, ищущих передовые варианты лечения. Государственное финансирование и институциональные инвестиции способствуют внедрению роботизированных систем в больницах.

Ожидается, что в сегменте амбулаторных хирургических центров будет наблюдаться самый быстрый рост в течение прогнозируемого периода, обусловленный растущим сдвигом в сторону амбулаторных хирургических процедур и экономически эффективных моделей оказания медицинской помощи. Эти центры становятся популярными для минимально инвазивных операций на позвоночнике из-за более короткого времени процедуры и более быстрого выздоровления пациентов. Роботизированные технологии позволяют амбулаторным центрам выполнять точные и эффективные процедуры при сохранении высоких стандартов хирургической безопасности. Кроме того, растущее предпочтение амбулаторных процедур среди пациентов и поставщиков медицинских услуг способствует внедрению роботизированных систем в этих учреждениях. Более низкие эксплуатационные расходы амбулаторных центров по сравнению с больницами также делают их привлекательными как для пациентов, так и для медицинских работников. Поскольку роботизированные системы становятся более компактными и экономичными, их внедрение в амбулаторных хирургических центрах, как ожидается, значительно расширится.

- По подходу

На основе подхода рынок роботов для хирургии позвоночника сегментируется на передний подход, задний подход и боковой подход. Сегмент заднего подхода доминировал на рынке с самой большой долей дохода в 2025 году, что обусловлено его широким использованием в различных спинальных процедурах, таких как слияние позвоночника и декомпрессионные операции. Хирурги обычно используют задний подход, потому что он обеспечивает прямой доступ к важным спинномозговым структурам, позволяя точно размещать винты и имплантаты. Роботизированная помощь дополнительно повышает точность этих процедур, направляя позиционирование имплантата и хирургическую навигацию. Задний подход широко используется как в минимально инвазивных, так и в открытых операциях на позвоночнике. Кроме того, технологические достижения в роботизированных навигационных системах улучшают хирургические результаты с использованием этого подхода. Большой объем спинальных процедур, выполняемых с использованием задних методов, значительно способствует доминированию сегмента.

Ожидается, что сегмент бокового подхода будет наблюдать самый быстрый рост в течение прогнозируемого периода, чему способствует растущее внедрение минимально инвазивных хирургических методов в хирургии позвоночника. Такой подход позволяет хирургам получить доступ к позвоночнику со стороны тела, уменьшая мышечные нарушения и сводя к минимуму хирургическую травму. Роботизированные системы наведения помогают улучшить хирургическую точность и уменьшить осложнения, связанные со сложными боковыми процедурами. Пациенты, перенесшие операции бокового подхода, часто испытывают более короткое время восстановления и снижение послеоперационной боли. Поскольку хирурги продолжают применять минимально инвазивные методы для улучшения результатов лечения пациентов, латеральный подход получает большее клиническое признание. Кроме того, достижения в области роботизированных хирургических технологий позволяют проводить более точные и безопасные процедуры бокового отдела позвоночника.

- По условиям

Исходя из состояния, рынок роботов для хирургии позвоночника сегментирован на дегенеративное заболевание диска, грыжу диска, переломы, опухоли, инфекции, нестабильность и деформацию. Сегмент дегенеративных заболеваний дисков доминировал на рынке с самой большой долей доходов в 2025 году, в первую очередь из-за высокой глобальной распространенности возрастной дегенерации позвоночника. Дегенеративное заболевание диска часто требует хирургического вмешательства, когда консервативные методы лечения не могут облегчить симптомы. Роботизированные системы помогают хирургам выполнять точные процедуры спинального слияния и имплантации, необходимые для лечения этого состояния. Рост стареющего населения во всем мире способствует более высокой заболеваемости дегенеративными нарушениями позвоночника. Кроме того, роботизированные технологии помогают улучшить хирургические результаты и уменьшить осложнения при этих процедурах. Поскольку число пациентов, нуждающихся в лечении дегенеративных заболеваний дисков, продолжает расти, спрос на роботизированную хирургию позвоночника также растет.

Ожидается, что сегмент деформации позвоночника будет наблюдать самый быстрый рост в течение прогнозируемого периода, обусловленный увеличением диагностики и хирургического лечения таких состояний, как сколиоз и кифоз. Эти сложные условия часто требуют очень точной хирургической коррекции с участием нескольких уровней позвонков. Роботизированная помощь позволяет хирургам планировать и выполнять эти процедуры с улучшенной точностью и стабильностью. Использование роботизированных систем помогает снизить риск неправильного размещения имплантатов и улучшает общие хирургические результаты. Кроме того, достижения в области роботизированной навигации и технологий визуализации поддерживают лечение сложных деформаций позвоночника. Повышение осведомленности и доступность передовых вариантов лечения также способствуют росту этого сегмента.

- С помощью приложения

На основе применения рынок роботов для хирургии позвоночника сегментирован на ламинэктомию, спинномозговое слияние, фораминотомию, интерламинарный имплантат, замену искусственного диска, переднюю шейную дискэктомию, эпидуральный лизис спаек, ламинотомию, ОЛЛИФ, чрескожную вертебропластику, хроническую боль в спине и спинальный стеноз. Сегмент спинального синтеза доминировал на рынке с самой большой долей дохода в 2025 году, что обусловлено широким использованием процедур спинального синтеза при лечении различных заболеваний позвоночника, таких как дегенеративное заболевание диска и нестабильность позвоночника. Роботизированные системы позволяют хирургам достичь точного позиционирования имплантата и улучшения выравнивания во время процедур спинального слияния. Эти технологии также снижают риск осложнений и улучшают хирургическую точность. Растущее число операций по слиянию позвоночника, выполняемых во всем мире, также способствует доминированию этого сегмента. Кроме того, роботизированные платформы позволяют улучшить хирургическое планирование и навигацию во время сложных многоуровневых термоядерных процедур. Поскольку больницы продолжают внедрять технологии роботизированной хирургии, применение спинального синтеза остается основным фактором роста рынка.

Ожидается, что сегмент замены искусственного диска будет наблюдать самый быстрый рост в течение прогнозируемого периода, чему способствует растущий спрос на лечение позвоночника, сохраняющее движение. Процедуры замены искусственного диска направлены на поддержание подвижности позвоночника при решении дегенеративных условий диска. Роботизированные хирургические системы помогают хирургам точно позиционировать искусственные диски и обеспечивать оптимальное выравнивание. Эти процедуры набирают популярность в качестве альтернативы традиционным операциям по слиянию позвоночника у подходящих пациентов. Достижения в области технологий имплантации и роботизированного хирургического руководства улучшают клинические результаты в процедурах замены диска. По мере роста осведомленности пациентов о передовых вариантах лечения, ожидается, что спрос на роботизированную замену искусственного диска значительно возрастет.

Спинная хирургия роботы рынок региональный анализ

- Северная Америка доминировала на рынке роботов для хирургии позвоночника с самой большой долей дохода в 41,3% в 2025 году, характеризующейся передовой инфраструктурой здравоохранения, высоким внедрением роботизированной хирургии и сильным присутствием ведущих медицинских технологических компаний.

- Медицинские работники в регионе высоко ценят хирургическую точность, улучшенные клинические результаты и расширенные возможности навигации, предлагаемые роботизированными системами позвоночника, интегрированными с платформами визуализации и цифрового хирургического планирования.

- Это широкое внедрение дополнительно поддерживается передовой инфраструктурой здравоохранения, высокими расходами на здравоохранение, сильным присутствием ведущих производителей медицинских устройств и растущим предпочтением технологически продвинутых хирургических процедур, устанавливая роботов для хирургии позвоночника в качестве важного решения для современного лечения позвоночника в больницах и специализированных хирургических центрах.

Американский рынок роботов для хирургии позвоночника Insight

Рынок роботов для хирургии позвоночника в США занял самую большую долю дохода в 79% в 2025 году в Северной Америке, чему способствовало быстрое внедрение хирургических технологий с роботизированной помощью и растущее число минимально инвазивных процедур позвоночника, выполняемых в больницах и специализированных центрах позвоночника. Медицинские работники все чаще отдают приоритет передовым роботизированным платформам для улучшения хирургической точности и результатов лечения пациентов. Растущее предпочтение хирургических процедур, основанных на технологиях, в сочетании с сильными инвестициями в инновации в области здравоохранения и медицинскую робототехнику, еще больше продвигает индустрию роботов для хирургии позвоночника. Более того, растущая интеграция роботизированных систем с передовыми технологиями визуализации, навигации и цифровыми платформами хирургического планирования вносит значительный вклад в расширение рынка.

Европейский рынок роботов для хирургии позвоночника

Прогнозируется, что рынок роботов для хирургии позвоночника в Европе будет расширяться при существенном CAGR в течение прогнозируемого периода, в первую очередь из-за растущего спроса на передовые хирургические технологии и растущей распространенности заболеваний позвоночника в регионе. Рост стареющих популяций в сочетании с необходимостью минимально инвазивных хирургических процедур способствует внедрению роботизированных систем хирургии позвоночника. Европейские поставщики медицинских услуг также стремятся повысить точность хирургического вмешательства и улучшить результаты лечения пациентов, предлагаемые роботизированными процедурами. Регион переживает значительный рост в больницах и специализированных хирургических центрах, причем роботизированные системы позвоночника включаются как в недавно созданные объекты, так и в существующую инфраструктуру здравоохранения.

Британский рынок роботов для хирургии позвоночника

Ожидается, что в течение прогнозируемого периода рынок роботов для хирургии позвоночника в Великобритании будет расти с заметным CAGR, что обусловлено растущим спросом на технологически продвинутые хирургические процедуры и улучшением результатов лечения пациентов. Кроме того, растущая распространенность заболеваний позвоночника и опорно-двигательного аппарата побуждает учреждения здравоохранения внедрять технологии роботизированной хирургии позвоночника. Ожидается, что растущее внимание страны к инновациям в области цифрового здравоохранения наряду с поддерживающей инфраструктурой здравоохранения и исследовательскими инициативами будет продолжать стимулировать рост рынка.

Немецкий рынок роботов для хирургии позвоночника

Ожидается, что в течение прогнозируемого периода рынок роботов для хирургии позвоночника в Германии будет расширяться на значительном CAGR, чему будет способствовать сильный сектор медицинских технологий в стране и увеличение инвестиций в современное хирургическое оборудование. Хорошо развитая инфраструктура здравоохранения Германии в сочетании с ее акцентом на инновации и точную медицину способствует внедрению роботизированных систем хирургии позвоночника в больницах и специализированных клиниках. Интеграция роботизированных платформ с передовыми технологиями хирургической навигации и визуализации также становится все более распространенной, при этом предпочтение отдается высокоточным и технологически продвинутым хирургическим решениям, соответствующим ожиданиям поставщиков медицинских услуг.

Азиатско-Тихоокеанский рынок роботов для хирургии позвоночника

Рынок роботов для хирургии позвоночника в Азиатско-Тихоокеанском регионе будет расти самыми быстрыми темпами в период с 2026 по 2033 год, что обусловлено расширением инфраструктуры здравоохранения, увеличением расходов на здравоохранение и технологическими достижениями в таких странах, как Китай, Япония и Индия. Растущее внимание региона к улучшению хирургических результатов и расширению доступа к передовым технологиям здравоохранения стимулирует внедрение систем роботизированной хирургии позвоночника. Кроме того, по мере того, как Азиатско-Тихоокеанский регион становится быстро растущим рынком медицинских технологий, доступность передовых роботизированных хирургических платформ расширяется до более широкого круга больниц и медицинских учреждений.

Японский рынок роботов для хирургии позвоночника

Японский рынок роботов для хирургии позвоночника набирает обороты благодаря сильной индустрии медицинских технологий в стране, старению населения и растущему спросу на передовые хирургические процедуры. Японская система здравоохранения уделяет значительное внимание точной медицине и инновационным хирургическим технологиям, стимулируя внедрение роботизированных платформ для хирургии позвоночника. Интеграция роботизированных систем с технологиями визуализации и навигации обеспечивает более точные и эффективные хирургические процедуры. Кроме того, быстро стареющее население Японии, вероятно, будет стимулировать спрос на передовые хирургические решения для лечения возрастных заболеваний позвоночника как в больницах, так и в специализированных хирургических условиях.

Индийский рынок роботов для хирургии позвоночника

Рынок роботов для хирургии позвоночника в Индии составил самую большую долю рынка в Азиатско-Тихоокеанском регионе в 2025 году, что объясняется расширением инфраструктуры здравоохранения страны, ростом численности пациентов и растущим внедрением передовых медицинских технологий. Индия является одним из самых быстрорастущих рынков здравоохранения, и роботизированные системы хирургии позвоночника постепенно набирают обороты в крупных больницах и специализированных ортопедических центрах. Стремление к модернизации медицинских учреждений и улучшению хирургических результатов наряду с ростом инвестиций в медицинские технологии являются ключевыми факторами, стимулирующими рынок роботов для хирургии позвоночника в Индии.

Доля рынка роботов для хирургии позвоночника

Индустрия роботов для хирургии позвоночника в основном возглавляется хорошо зарекомендовавшими себя компаниями, в том числе:

- Medtronic (Ирландия)

- Globus Medical, Inc. (США)

- Zimmer Biomet (США)

- Страйкер (США)

- NuVasive, Inc. (США)

- Intuitive Surgical, Inc. (США)

- Brainlab AG (Германия)

- Smith & Nephew plc (Великобритания)

- Johnson & Johnson Services, Inc. (США)

- Renishaw plc (Великобритания)

- Siemens Healthineers AG (Германия)

- Orthofix Medical Inc. (США)

- Fusion Robotics, LLC (США)

- TINAVI Medical Technologies Co., Ltd. (Китай)

- Medacta International SA (Швейцария)

- Робокат (Франция)

- Aurora Spine Corporation (США)

- SpineGuard SA (Франция)

- Think Surgical, Inc. (США)

- CUREXO, Inc. (Южная Корея)

Каковы последние события на мировом рынке роботов для хирургии позвоночника

- В декабре 2025 года Providence Medical Technology объявила о совместимости своей системы CORUS-GLX с роботизированной навигационной платформой ExcelsiusGPS, разработанной Globus Medical, Inc., что позволяет хирургам интегрировать роботизированное руководство и навигацию во время процедур заднего поясничного слияния. Разработка улучшает хирургическую визуализацию, улучшает точность размещения имплантатов и поддерживает минимально инвазивные методы спинального синтеза.

- В июне 2025 года Johnson & Johnson через свое ортопедическое подразделение DePuy Synthes объявила о разработке и предстоящем коммерческом развертывании роботизированной системы VELYS Spine для процедур спинального синтеза. Платформа сочетает в себе роботизированную помощь с передовыми хирургическими навигационными технологиями для повышения точности и эффективности спинальных процедур. Новая система предназначена для поддержки хирургов с оптимизацией рабочего процесса и передовой интеграцией изображений, что представляет собой значительный шаг к расширению роботизированных решений для хирургии позвоночника во всем мире.

- В ноябре 2024 года Globus Medical, Inc. представила ExcelsiusHub, передовую хирургическую навигационную платформу, предназначенную для поддержки роботизированных спинальных процедур. Система расширяет возможности платформ роботизированной хирургии позвоночника путем интеграции технологий визуализации, навигации и роботизированного руководства в единый хирургический рабочий процесс. Разработка направлена на улучшение хирургической точности и рационализацию процедур для хирургов, выполняющих сложные операции на позвоночнике. Запуск подчеркивает возрастающую роль интегрированных цифровых технологий в роботизированных системах хирургии позвоночника.

- В июле 2021 года Globus Medical, Inc. объявила, что более 20 000 хирургических процедур были выполнены по всему миру с использованием роботизированной навигационной системы ExcelsiusGPS. Эта веха продемонстрировала растущее внедрение технологий роботизированной хирургии позвоночника в больницах и центрах позвоночника. Роботизированная система помогает хирургам повысить точность установки имплантатов, уменьшить радиационное воздействие во время операции и повысить эффективность операционной, подчеркивая расширяющуюся роль робототехники в современных спинальных процедурах.

- В апреле 2021 года отраслевой анализ сообщил, что такие компании, как Medtronic plc и Globus Medical, Inc., лидируют на быстро развивающемся рынке роботизированной хирургии позвоночника, а больницы все чаще внедряют роботизированные платформы для повышения хирургической точности и обеспечения минимально инвазивных процедур. Растущая конкуренция среди компаний, производящих медицинские устройства, за разработку передовых роботизированных систем наведения отражает растущий спрос на высокоточные операции на позвоночнике и расширение роботизированных технологий в ортопедических и нейрохирургических приложениях.

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.