Global Wet Pet Food Market

Размер рынка в млрд долларов США

CAGR :

%

USD

25.20 Billion

USD

37.50 Billion

2025

2033

USD

25.20 Billion

USD

37.50 Billion

2025

2033

| 2026 –2033 | |

| USD 25.20 Billion | |

| USD 37.50 Billion | |

| % | |

|

Сегментация глобального рынка кормов для мокрых домашних животных, по домашним животным (собаки и кошки), канал распространения (магазины специализации для домашних животных, супермаркеты / гипермаркеты, магазины удобств и онлайн), источник (животные, растительные производные и синтетические) - отраслевые тенденции и прогноз до 2033 года

Размер рынка кормов для домашних животных

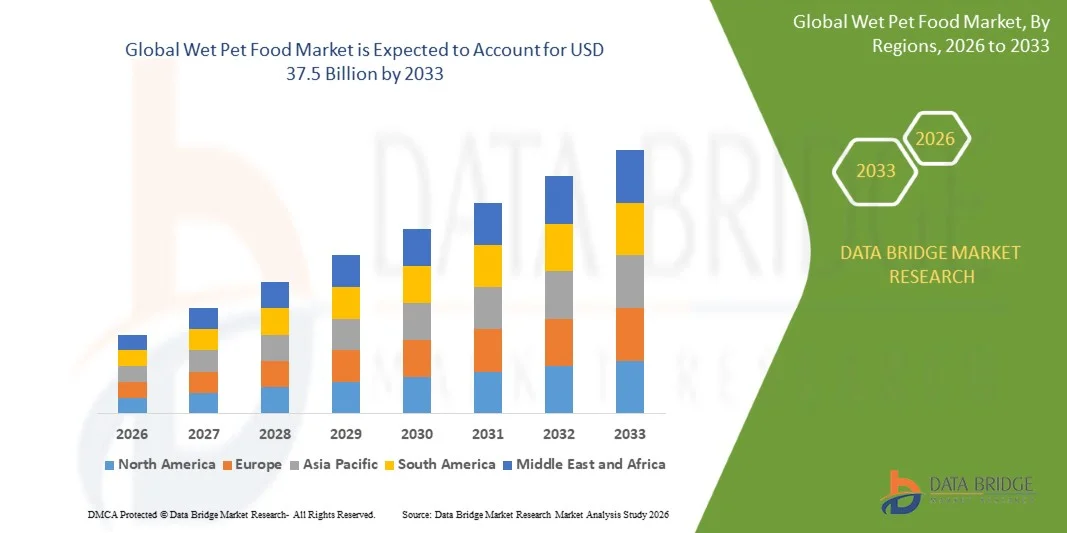

- Мировой рынок кормов для домашних животных оценили в25,2 млрд долларов в 2025 годуОжидается, что он достигнет37,5 млрд долларов к 2033 году, вCAGR 5.10%в течение прогнозируемого периода

- Рост рынка в значительной степени обусловлен ростом гуманизации домашних животных и повышением осведомленности о питании домашних животных, что заставляет владельцев уделять приоритетное внимание высококачественным, богатым влагой диетам для своих домашних животных как на развитых, так и на развивающихся рынках.

- Кроме того, растущий спрос на премиальные, функциональные и специфические для конкретных условий продукты питания для домашних животных, поддерживаемый более высокими располагаемыми доходами и расширением доступности розничной торговли и электронной коммерции, ускоряет принятие и укрепление общего расширения рынка.

Анализ рынка кормов для домашних животных

- Влажная корма для домашних животных, предлагающая высокую вкусоувлажняемость, улучшенную гидратацию и повышенную усвояемость, стала важным компонентом современного питания домашних животных как для собак, так и для кошек, особенно среди стареющих домашних животных и людей с особыми потребностями в области здравоохранения.

- Растущий спрос на влажные корма для домашних животных в первую очередь подпитывается увеличением владения домашними животными, сдвигом потребительских предпочтений в сторону премиальных и натуральных рецептур и постоянными инновациями продуктов ведущих производителей, ориентированных на здоровье, благополучие и удобство.

- Северная Америка доминирует на рынке кормов для домашних животных с долей 42,2%В 2025 году из-за высоких ставок владения домашними животными и высоких потребительских расходов на премиальное кормление домашних животных

- Ожидается, что Азиатско-Тихоокеанский регион станет самым быстрорастущим регионом на рынке кормов для домашних животных в течение прогнозируемого периода из-за быстрой урбанизации, роста располагаемых доходов и увеличения усыновления домашних животных в основных экономиках.

- Сегмент собак доминировал на рынке с долей рынка 62,5% в 2025 году из-за более высокой глобальной популяции собак и большего потребления продуктов на одного котенка по сравнению с кошками. Владельцы собак все чаще предпочитают влажную пищу из-за ее вкусности, более высокого содержания влаги и пригодности для домашних животных с проблемами зубов или пищеварения. Растущая тенденция премиализации и гуманизации корма для собак еще больше усиливает спрос на обогащенные питательными веществами влажные составы, адаптированные к различным породам и этапам жизни.

Сегментация рынка кормов для мокрых домашних животных

| Атрибуты | Влажная корма для домашних животных Ключевые идеи рынка |

| Сегменты покрыты |

|

| Страны, охваченные | Северная Америка

Европа

Азиатско-Тихоокеанский регион

Ближний Восток и Африка

Южная Америка

|

| Ключевые игроки рынка |

|

| Рыночные возможности |

|

| Информационные наборы данных с добавленной стоимостью | В дополнение к информации о рыночных сценариях, таких как рыночная стоимость, темпы роста, сегментация, географическое покрытие и основные игроки, рыночные отчеты, курируемые Data Bridge Market Research, также включают анализ экспорта импорта, обзор производственных мощностей, анализ потребления продукции, анализ ценового тренда, сценарий изменения климата, анализ цепочки поставок, анализ цепочки создания стоимости, обзор сырья / расходных материалов, критерии выбора поставщиков, анализ PESTLE, анализ Porter и нормативную базу. |

Тенденции рынка кормов для домашних животных

«Премиумизация продуктов питания для мокрых домашних животных»

- Ключевой тенденцией, формирующей рынок кормов для домашних животных, является растущая премиализация продуктов, обусловленная тем, что владельцы домашних животных все чаще относятся к домашним животным как к членам семьи и ищут высококачественное питание, сопоставимое с человеческими стандартами питания. Этот сдвиг побуждает производителей сосредоточиться на рецептах с высоким содержанием белка, натуральных ингредиентах и составах с чистой маркировкой, которые подчеркивают прозрачность и питательную ценность.

- Например, Nestlé Purina PetCare расширила свои портфели Pro Plan и Fancy Feast премиальными предложениями влажных продуктов питания, которые подчеркивают беззерновые составы и функциональные преимущества для здоровья. Эти запуски укрепляют доверие потребителей и укрепляют позиции бренда в премиум-сегменте.

- Ведущие игроки все чаще подчеркивают рецепты с высокой влажностью для улучшения вкуса и увлажнения, особенно для кошек и пожилых домашних животных. Эта тенденция поддерживает спрос на специализированные варианты влажной пищи, направленные на пищеварение, здоровье мочи и управление весом.

- Тенденция премиализации также проявляется в растущей доступности влажной корма для домашних животных в стиле гурманов с новыми белками и рецептами, ориентированными на текстуру. Эти продукты привлекательны для городских и более высокодоходных потребителей, ищущих дифференцированный опыт кормления для своих домашних животных.

- Инновации в упаковке, такие как одноразовые лотки и порционно-контролируемые пакеты, принимаются для повышения удобства и свежести восприятия. Эта эволюция в дизайне продуктов усиливает привлекательность премиального бренда и поощряет повторные покупки.

- В целом, премиализация меняет конкурентную динамику, увеличивая средние цены продажи и заставляя производителей инвестировать в инновации, обеспечение качества и рассказывание историй бренда, чтобы привлечь потребителей, ориентированных на стоимость.

Динамика рынка кормов для домашних животных

водитель

Растущая гуманизация домашних животных и акцент на здоровье домашних животных

- Растущая гуманизация домашних животных является основной движущей силой рынка кормов для влажных домашних животных, поскольку владельцы все чаще отдают приоритет питанию, здоровью и профилактическому уходу за своими питомцами. Этот сдвиг ускоряет спрос на влажную пищу из-за ее предполагаемой пользы для здоровья, включая более высокое содержание влаги и улучшенную усвояемость.

- Например, Mars Petcare расширила свой портфель продуктов питания для влажных домашних животных в таких брендах, как Royal Canin и Pedigree, для удовлетворения конкретных потребностей в породе, возрасте и здоровье. Эти предложения поддерживают индивидуальные стратегии питания в соответствии с ветеринарными рекомендациями.

- Растущая осведомленность об ожирении, стоматологических проблемах и проблемах со здоровьем мочи у домашних животных побуждает владельцев выбирать влажную пищу в рамках сбалансированных диет. Ветеринарные рекомендации и клинические исследования в области питания еще больше усиливают это предпочтение.

- Водитель усиливается за счет увеличения располагаемых доходов и готовности тратить на продукты по уходу за домашними животными, особенно в Северной Америке и Европе. Потребители активно ищут полноценные и функциональные решения для влажной пищи.

- В совокупности гуманизация домашних животных и осведомленность о здоровье трансформируют привычки кормления и позиционируют влажные корма для домашних животных как основной компонент современного питания домашних животных.

Сдержанность/вызов

«Высокие затраты на производство и упаковку мокрых кормов для домашних животных»

- Рынок кормов для домашних животных сталкивается с серьезными проблемами из-за высоких затрат на производство и упаковку, связанных с богатыми влагой составами и строгими стандартами безопасности. Влажные корма для домашних животных требуют передовых методов обработки, включая стерилизацию и контролируемое уплотнение, что увеличивает операционную сложность.

- Например, Freshpet полагается на холодильную производственную и распределительную инфраструктуру для поддержания свежести продукта, что значительно увеличивает производственные и логистические затраты. Эти требования ограничивают гибкость затрат и влияют на стратегии ценообразования.

- Упаковочные материалы, такие как банки, лотки и мешки, увеличивают общие расходы, особенно на фоне колебаний цен на металл и пластик. Соблюдение правил безопасности пищевых продуктов и сроков хранения еще больше повышает давление на стоимость для производителей.

- Меньшие производители сталкиваются с трудностями в масштабировании операций, сохраняя при этом качество и доступность, создавая барьеры для входа и расширения. Эта проблема более выражена на чувствительных к цене рынках, где потребители могут предпочесть альтернативы сухим продуктам питания.

- В целом, высокие затраты на производство и упаковку остаются ключевым сдерживающим фактором, влияющим на ценообразование, масштабируемость и долгосрочную прибыльность на рынке кормов для домашних животных.

Сфера рынка кормов для домашних животных

Рынок сегментируется на основе домашних животных, канала распределения и источника.

• Пет

На основе домашних животных рынок кормов для домашних животных сегментирован на собак и кошек. Сегмент собак доминировал на рынке с самой большой долей дохода в 62,5% в 2025 году, что обусловлено более высокой глобальной популяцией собак и большим потреблением корма на одного котенка по сравнению с кошками. Владельцы собак все чаще предпочитают влажную пищу из-за ее вкусности, более высокого содержания влаги и пригодности для домашних животных с проблемами зубов или пищеварения. Растущая тенденция премиализации и гуманизации корма для собак еще больше усиливает спрос на обогащенные питательными веществами влажные составы, адаптированные к различным породам и этапам жизни.

Сегмент кошек, как ожидается, станет свидетелем самого быстрого роста с 2026 по 2033 год, чему будет способствовать рост популярности кошек в городских домохозяйствах и небольших жилых помещениях. Влажная пища для домашних животных особенно предпочтительна для кошек из-за высокого содержания белка и уровня влаги, которые поддерживают здоровье мочевыводящих путей. Растущая осведомленность о специфичных для кошек потребностях в питании и запуск гурманов и функциональных вариантов корма для мокрых кошек продолжают ускорять рост сегмента.

• Распределительный канал

На основе канала распределения рынок кормов для домашних животных сегментирован на специализированные магазины для домашних животных, супермаркеты / гипермаркеты, магазины и онлайн. Специализированные магазины домашних животных доминировали на рынке в 2025 году благодаря широкому ассортименту премиальных и терапевтических брендов кормов для домашних животных, а также руководству экспертов. Эти магазины предпочитают владельцы домашних животных, которые ищут специализированное питание, рекомендованные ветеринарами продукты и надежные портфели брендов. Сильные отношения с поставщиками и рекламные акции в магазине еще больше укрепляют их лидирующие позиции.

Онлайн-сегмент, по прогнозам, зафиксирует самые быстрые темпы роста с 2026 по 2033 год, что обусловлено ростом проникновения электронной коммерции и удобством доставки на дом. Модели подписки, конкурентное ценообразование и доступ к более широкому спектру международных и нишевых брендов привлекают владельцев домашних животных. Расширение использования мобильных приложений и платформ прямого потребления производителями кормов для домашних животных также способствует быстрому расширению.

• Источник

На основе источника, рынок кормов для домашних животных сегментирован на животных, растительных производных и синтетических. Сегмент животного происхождения обеспечил наибольшую долю рынка в 2025 году благодаря высокому содержанию белка и более тесному согласованию с естественными диетическими предпочтениями собак и кошек. Потребители воспринимают влажную пищу животного происхождения как более питательную и вкусную, особенно для домашних животных с более высокими потребностями в энергии и поддержании мышц. Доминирование мясных, рыбных и птичьих рецептур в премиальных и массовых категориях поддерживает высокий спрос.

Ожидается, что сегмент производных растений будет расти самыми быстрыми темпами в течение прогнозируемого периода, чему будет способствовать растущий интерес к устойчивым и этическим вариантам кормов для домашних животных. Владельцы домашних животных постепенно принимают растительные препараты для конкретных диетических требований и управления аллергией. Инновации в переработке растительного белка и сбалансированном питании еще больше усиливают принятие этого сегмента.

Региональный анализ рынка кормов для домашних животных

- Северная Америка доминировала на рынке кормов для домашних животных с самой большой долей дохода 42,2% в 2025 году, что обусловлено высокими ставками владения домашними животными и сильными потребительскими расходами на премиальное питание для домашних животных.

- Владельцы домашних животных в регионе все чаще отдают приоритет высокобелковым, натуральным и функциональным продуктам питания для домашних животных, которые поддерживают здоровье пищеварения, гидратацию и общее самочувствие.

- Это сильное внедрение поддерживается хорошо зарекомендовавшей себя инфраструктурой ухода за домашними животными, высокой осведомленностью о тенденциях гуманизации домашних животных и присутствием ведущих мировых брендов кормов для домашних животных, позиционируя влажные корма для домашних животных как предпочтительный выбор среди домашних хозяйств.

Американский рынок кормов для домашних животных Insight

Американский рынок кормов для домашних животных составил самую большую долю дохода в Северной Америке в 2025 году, чему способствовала большая популяция собак и кошек и растущее предпочтение премиальных и специализированных диет. Потребители все чаще выбирают беззерновые, органические и рекомендованные ветеринарами влажные пищевые составы для удовлетворения конкретных потребностей в области здравоохранения. Сильное присутствие платформ электронной коммерции, моделей доставки на основе подписки и непрерывных инноваций в продуктах также поддерживает устойчивый рост рынка.

Европейский рынок кормов для домашних животных Insight

Ожидается, что европейский рынок кормов для домашних животных будет расти на стабильном CAGR в течение прогнозируемого периода, что обусловлено повышением осведомленности о питании домашних животных и увеличением принятия премиальных кормов для домашних животных. Европейские потребители проявляют большой интерес к экологически чистым, экологически чистым и этическим кормам для домашних животных. Рост поддерживается увеличением усыновления домашних животных, особенно среди молодых семей, и сильным присутствием в розничной торговле как в автономном режиме, так и в Интернете.

Великобритания Wet Pet Food Market Insight

Прогнозируется, что рынок кормов для домашних животных в Великобритании будет заметен рост в течение прогнозируемого периода, чему будет способствовать высокий уровень владения домашними животными и высокий спрос на натуральные корма с высоким содержанием мяса. Опасения, связанные с ожирением домашних животных и здоровьем пищеварения, побуждают владельцев переходить к сбалансированному питанию. Зрелая розничная экосистема страны и растущее проникновение премиальных брендов продолжают стимулировать расширение рынка.

Германия Wet Pet Food Market Insight

Ожидается, что рынок кормов для домашних животных в Германии будет расширяться при значительном CAGR, что обусловлено растущим вниманием к здоровью домашних животных, устойчивости и прозрачности продуктов. Немецкие потребители предпочитают высококачественные, без добавок влажные корма для домашних животных с четкой маркировкой ингредиентов. Рынок выигрывает от сильного спроса как на собак, так и на кошек, а также растущего признания функциональных и ветеринарных рецептур.

Азиатско-Тихоокеанский рынок кормов для домашних животных Insight

Ожидается, что Азиатско-Тихоокеанский рынок кормов для домашних животных зарегистрирует самый быстрый CAGR с 2026 по 2033 год, что обусловлено быстрой урбанизацией, ростом располагаемых доходов и увеличением усыновления домашних животных в основных экономиках. Изменение образа жизни и растущая осведомленность о питании домашних животных ускоряют переход от домашних продуктов питания к коммерческим влажным кормам для домашних животных. Расширение розничных сетей и растущее проникновение международных брендов кормов для домашних животных еще больше стимулируют региональный рост.

Японский рынок кормов для домашних животных Insight

Японский рынок кормов для домашних животных набирает обороты благодаря старению популяции домашних животных в стране и сильному акценту на удобство и качество питания. Влажная пища для домашних животных широко предпочтительна из-за ее простоты потребления и пригодности для старых домашних животных с проблемами со здоровьем. Высокий спрос на премиальные, частично контролируемые и функциональные влажные продукты питания продолжает стимулировать рынок.

Китайский рынок кормов для домашних животных Insight

Китайский рынок кормов для домашних животных занимал самую большую долю доходов в Азиатско-Тихоокеанском регионе в 2025 году, чему способствовал быстрый рост владения домашними животными и увеличение располагаемого дохода среди городских домохозяйств. Повышение осведомленности о здоровье домашних животных и сильное влияние западных тенденций ухода за домашними животными ускоряют принятие коммерческих влажных кормов для домашних животных. Наличие отечественных производителей, конкурентное ценообразование и быстрое расширение каналов онлайн-продаж существенно поддерживают рост рынка в Китае.

Доля рынка кормов для домашних животных

Влажная индустрия кормов для домашних животных в основном возглавляется хорошо зарекомендовавшими себя компаниями, в том числе:

- VAFO Group a.s. (Чешская Республика)

- Freshpet Inc. (США)

- Tiernahrung Deuerer GmbH (Германия)

- Blue Buffalo Co. Ltd. (США)

- Harringtons Pet Food (Великобритания)

- Darling Ingredients Inc. (США)

- Чемпион Petfoods Holding Inc. (Канада)

- Phelps Pet Products (США)

- Nestle SA (Швейцария)

- De Haan Petfood (Нидерланды)

- Mars Inc. (США)

- FirstMate Pet Foods (Канада)

- Schell and Kampeter Inc. (США)

- Beaphar Beheer BV (Нидерланды)

- Spectrum Brands Inc. (США)

- C and D Foods Ltd. (Ирландия)

- Simmons Foods Inc. (США)

- Evangers Dog and Cat Food Co. Inc. (США)

- Colgate Palmolive Co. (США)

- Clearlake Capital Group L.P. (США)

Последние события на мировом рынке кормов для мокрых домашних животных

- В феврале 2025 года Royal Canin завершила приобретение Aguas Frescas, мексиканского производителя кормов для мокрых домашних животных, значительно укрепив свое присутствие в Латинской Америке. Этот шаг позволяет Royal Canin локализовать производство, повысить эффективность цепочки поставок и лучше реагировать на растущий региональный спрос на влажные корма для домашних животных. Приобретение усиливает конкурентное позиционирование, расширяя доступ к новым потребительским базам и укрепляя свое лидерство в области премиального питания домашних животных на развивающихся рынках.

- В январе 2024 года Nestlé Purina PetCare запустила новый ассортимент беззерновой, влажной пищи для кошек с высоким содержанием белка под маркой Pro Plan, уделяя внимание растущему переходу к диетам для домашних животных, ориентированным на здоровье. Расширение этого продукта укрепляет присутствие Purina в сегменте кормов для домашних животных премиум-класса, привлекая владельцев домашних животных, ищущих решения для функционального питания. Запуск поддерживает рост рынка, стимулируя инновации и усиливая тенденции премиализации в категории влажных кормов для домашних животных.

- В июле 2023 года Champion Petfoods, под марсом Mars, Incorporated, представила линию кормов ACANA Premium Pâté для мокрых кошек, подчеркивая преимущества питания и гидратации на основе добычи. Этот запуск расширяет портфель продуктов питания компании и повышает ее привлекательность среди потребителей, уделяя приоритетное внимание естественным и биологически подходящим диетам. Это развитие укрепляет конкурентную позицию Champion Petfoods, расширяя выбор на рынке премиальных кормов для мокрых кошек и поддерживая долгосрочную дифференциацию бренда.

- В апреле 2023 года Mars Petcare расширила свой портфель продуктов SHEBA, представив улучшенную пищу для кошек, ориентированную на потребности в питании в раннем возрасте. Внедрение этого продукта позволяет компании захватывать спрос на разных этапах жизни кошек, укрепляя лояльность бренда среди новых владельцев домашних животных. Этот шаг поддерживает расширение рынка за счет увеличения глубины продукта в сегменте питания для котят и укрепления общего предложения кормов для домашних животных Mars Petcare.

- В марте 2023 года Hill’s Pet Nutrition, дочерняя компания Colgate-Palmolive, запустила специальную линию влажной пищи для домашних животных с диагнозом рак. Это развитие усиливает присутствие Хилла в терапевтическом и ветеринарном сегменте кормов для домашних животных, усиливая его роль в клиническом питании. Постепенное глобальное развертывание этого ассортимента укрепляет позиции компании на рынке, удовлетворяя неудовлетворенные потребности в медицинском питании и углубляя отношения с ветеринарными каналами по всему миру.

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.