Middle East And Africa Antiblock Additive Market

Размер рынка в млрд долларов США

CAGR :

%

USD

409.69 Million

USD

620.06 Million

2024

2032

USD

409.69 Million

USD

620.06 Million

2024

2032

| 2025 –2032 | |

| USD 409.69 Million | |

| USD 620.06 Million | |

| % | |

|

Сегментация антиблокировочного рынка на Ближнем Востоке и в Африке по форме (неорганический и органический), целевой полимер (полиэтилен (PE), поливинилхлорид (PVC), биаксиально-ориентированный полипропилен (BOPP), полиэтилентерефталат (PET), полистирол (PS) и другие), индустрия конечного использования (упаковка, промышленность, сельское хозяйство, медицина и здравоохранение, электроника и солнечная, печать и оптика и другие), страны (Саудовская Аравия, ОАЭ, Южная Африка, Египет, Израиль, остальная часть Ближнего Востока и Африки) - тенденции и прогноз на 2032 год

Ближневосточный и африканский антиблокировочный анализ рынка

На рынке антиблокировочных добавок на Ближнем Востоке и в Африке наблюдается устойчивый рост, обусловленный растущим спросом на пластиковую упаковку. По мере того, как глобальная индустрия антиблокировочных добавок продолжает расширяться, всплеск инноваций и достижений в области полимерной упаковки увеличился. Растущий спрос на разработку антиблокировочных добавок на биологической основе создает возможности для рынка. На динамику рынка также влияют колебания цен на сырье. В целом ожидается, что рынок продолжит расширяться, уделяя особое внимание инновациям и устойчивости для удовлетворения меняющихся промышленных потребностей.

Ближний Восток и Африка Размер антиблокировочного рынка

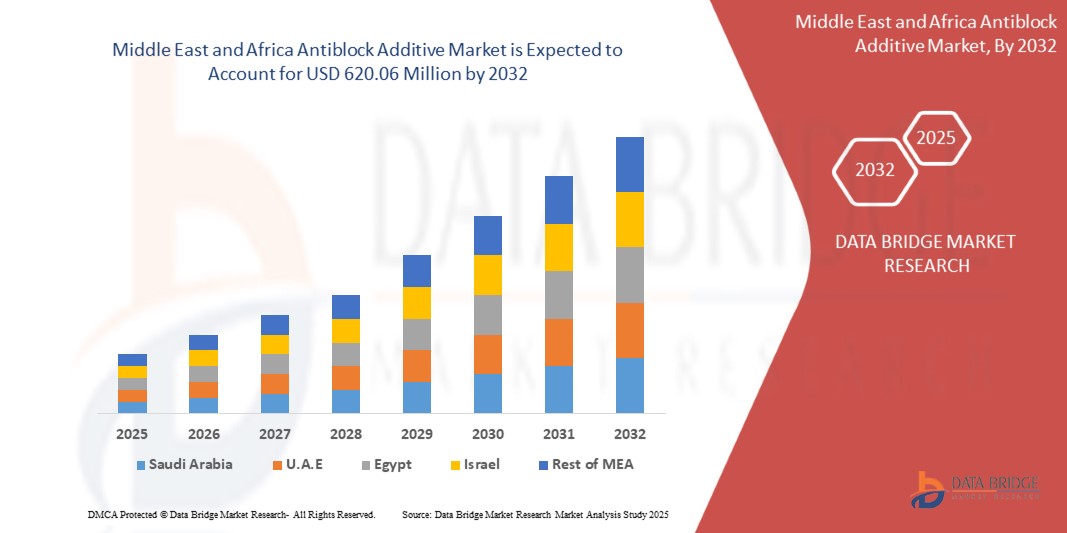

Размер рынка антиблокировочных добавок на Ближнем Востоке и в Африке был оценен в 409,69 млн долларов США в 2024 году и, по прогнозам, достигнет 620,06 млн долларов США к 2032 году с CAGR 5,33% в течение прогнозируемого периода 2025-2032 годов. В дополнение к информации о рыночных сценариях, таких как рыночная стоимость, темпы роста, сегментация, географическое покрытие и основные игроки, рыночные отчеты, курируемые Data Bridge Market Research, также включают углубленный экспертный анализ, анализ цен, анализ доли бренда, опрос потребителей, анализ демографии, анализ цепочки поставок, анализ цепочки создания стоимости, обзор сырья / расходных материалов, критерии выбора поставщиков, анализ PESTLE, анализ Porter и нормативную базу.

Ближний Восток и Африка Антиблокировочный рыноктенденции

«Рост спроса на пластиковую упаковку»

Растущий спрос на пластиковую упаковку является значительным драйвером для глобального рынка антиблокировочных добавок. По мере расширения таких отраслей, как пищевые продукты и напитки, фармацевтика, потребительские товары и электронная коммерция, возрастает потребность в эффективных, долговечных и функциональных упаковочных решениях. Пластиковая упаковка, будучи легкой, экономичной и универсальной, стала предпочтительным выбором в различных секторах. Эта повышенная зависимость от пластиковой упаковки стимулирует спрос на добавки, которые повышают производительность пластиковых материалов. Антиблокировочные добавки играют важную роль в улучшении обработки и производительности пластиковых пленок, используемых в упаковке. Эти добавки предотвращают слипание слоев пластиковых пленок во время производства, обработки и хранения. Без антиблокировочных агентов пластиковые пленки будут прилипать друг к другу, что приведет к производственным проблемам, нарушению целостности упаковки и неэффективности. Уменьшая такие проблемы, антиблокировочные добавки обеспечивают плавные производственные процессы, более высокое качество продукции и более эффективные системы упаковки.

Рост спроса на гибкую пластиковую упаковку, особенно в пищевой промышленности, способствует росту рынка антиблокировочных добавок. Поскольку потребители требуют более длительного срока хранения, лучшего сохранения продукта и удобной упаковки, антиблокировочные добавки способствуют улучшению функциональности и привлекательности пластиковой упаковки. Кроме того, поскольку устойчивость становится все более серьезной проблемой, разработка экологически чистых антиблокировочных добавок еще больше поддерживает эту тенденцию, предоставляя возможности для инноваций в упаковочном секторе.

Сфера охвата и сегментация рынка

| Атрибуты | Ближний Восток и Африка Антиблокировочная добавкаКлючОбзор рынка |

| Сегменты покрыты |

|

| Страны, охваченные | Саудовская Аравия, ОАЭ, Южная Африка, Египет, Израиль и остальной Ближний Восток и Африка |

| Ключевые игроки рынка | Imerys (Франция), Ampacet CORPORATION (США), ALTANA (Германия), Dow (США), Lyondellbasell Industries Holdings B.V. (Нидерланды), Astra Polymers (Саудовская Аравия), Avient Corporation (США), Cargill, Incorporated (США), Covia Holdings LLC. (США), Evonik (Германия), Fine Organic Industries Limited (Индия), Honeywell International Inc. (США), Inerals Technologies Inc. (США), National Plastics Color, Inc. (США), SABIC (Саудовская Аравия), Sukano AG (Швейцария), W.R. Grace & Co.-Conn (США), Wells Plastics (Великобритания). |

| Рыночные возможности |

|

| Информационные наборы данных с добавленной стоимостью | В дополнение к информации о рыночных сценариях, таких как рыночная стоимость, темпы роста, сегментация, географическое покрытие и основные игроки, рыночные отчеты, курируемые Data Bridge Market Research, также включают углубленный экспертный анализ, анализ цен, анализ доли бренда, опрос потребителей, анализ демографии, анализ цепочки поставок, анализ цепочки создания стоимости, обзор сырья / расходных материалов, критерии выбора поставщиков, анализ PESTLE, анализ Porter и нормативную базу. |

Ближний Восток и Африка Антиблокировочная добавкарынокОпределение

Антиблокировочные добавки представляют собой химические соединения, используемые в полимерных пленках, особенно в полиэтилене и полипропилене, для уменьшения адгезии между слоями пленки. Эти добавки работают путем создания микроскопических шероховатых поверхностей, которые минимизируют площадь контакта между слоями, предотвращая их слипание. Общие антиблокировочные агенты включают кремнезем, тальк и синтетические силикаты. Они широко используются в упаковочных пленках, сельскохозяйственных пленках и промышленных приложениях для улучшения обработки, обработки и обработки. Уменьшая блокировку, эти добавки повышают производительность, облегчают разделение пленки и обеспечивают эффективную упаковку без ущерба для прозрачности, механических свойств или печати конечного продукта из пластиковой пленки.

Ближний Восток и Африка Антиблокировочная добавкарынокдинамика

Водители

- Бум автомобильного и промышленного секторов

Антиблокировочные добавки, которые в основном используются в пластиковых пленках для предотвращения их склеивания во время обработки, становятся все более важными, поскольку такие отрасли, как автомобилестроение и производство, расширяются. В автомобильном секторе растет спрос на легкие, долговечные и экономически эффективные материалы для упаковки, интерьеров и автомобильных компонентов. Антиблокировочные добавки используются в производстве пластиковых пленок, которые находят применение в автомобильной упаковке, защитных покрытиях и композитных материалах. С ростом производства транспортных средств во всем мире производители сосредотачиваются на улучшении производительности и внешнего вида автомобильных пластмасс, что еще больше увеличивает потребность в антиблокировочных добавках. Спрос автомобильной промышленности на более эффективные, перерабатываемые и функциональные материалы напрямую способствует росту рынка.

Аналогичным образом, промышленный сектор, который охватывает широкий спектр применений, включая упаковку, строительство и оборудование, является важным фактором. Поскольку отрасли промышленности требуют высококачественные пластиковые пленки для упаковки и оборудования, потребность в антиблокировочных добавках возросла. В упаковочной промышленности антиблокировочные добавки необходимы для предотвращения склеивания слоев пленки, повышения простоты обработки и улучшения качества конечного продукта. Кроме того, антиблокировочные добавки являются неотъемлемой частью промышленных упаковочных решений, особенно в секторах, связанных с сыпучими товарами и чувствительными материалами.

Например,

- В мае 2022 года, согласно статье, опубликованной Squarespace, блог исследует использование пластмасс в автомобильных приложениях, подчеркивая как преимущества, так и экологические проблемы. Пластмассы делают транспортные средства легкими, экономичными и настраиваемыми, но такие проблемы, как токсичный ПВХ и плохая перерабатываемость, могут нанести вред окружающей среде. В статье содержится призыв к более устойчивым полимерам для решения этих проблем.

- В мае 2023 года, согласно статье, опубликованной American Chemistry Council, Inc. В докладе Американского химического совета за 2023 год подчеркивается, что с 2012 по 2021 год количество пластмасс в автомобилях увеличилось на 16%. Пластмассы повышают топливную экономичность, безопасность и производительность, особенно в электромобилях (EV), компенсируя вес батарей. В докладе подчеркивается роль пластмасс в устойчивом развитии и усилиях по переработке.

Акцент обоих секторов на снижении затрат, улучшении свойств материалов и обеспечении устойчивости приводит к более широкому внедрению антиблокировочных добавок. Поскольку мировое автомобильное и промышленное производство продолжает расти, спрос на эти добавки, как ожидается, последует этому примеру, усиливая положительную траекторию роста рынка антиблокировочных добавок в ближайшие годы.

- Инновации и достижения в полимерной упаковке

Инновации в полимерной упаковке значительно повлияли на рост рынка антиблокировочных добавок, стимулируя новые разработки в упаковочных материалах и повышая производительность продукта. Антиблокировочные добавки, в основном используемые в упаковке для повышения долговечности, стабильности и производительности полимеров, пользуются повышенным спросом из-за меняющихся потребностей упаковочной промышленности. По мере того, как требования к упаковке смещаются в сторону более устойчивых, эффективных и высокопроизводительных материалов, антиблокировочные добавки играют ключевую роль в улучшении полимерных составов. Одним из основных факторов является растущий спрос на полимеры, которые более устойчивы к трению и износу. Антиблокировочные добавки помогают уменьшить трение между полимерными поверхностями, минимизируя риск повреждения во время процесса упаковки, особенно в таких отраслях, как пищевая промышленность и фармацевтика, где целостность продукта имеет решающее значение. Эти добавки также улучшают характеристики обработки полимеров, обеспечивая более плавные производственные процессы и продлевая срок службы упаковочных материалов.

По мере того, как устойчивость становится критическим направлением, растет спрос на биоразлагаемые или перерабатываемые упаковочные материалы. Антиблокировочные добавки помогают сделать эти экологически чистые полимеры более эффективными и долговечными, гарантируя, что они хорошо работают без ущерба для окружающей среды. Этот переход к более экологичным упаковочным решениям привел к инновациям в разработке антиблокировочных добавок, которые не только эффективны в снижении трения, но и безопасны для окружающей среды. Кроме того, рост электронной коммерции увеличил потребность в надежных упаковочных решениях, которые могут противостоять суровым условиям глобального судоходства. Антиблокировочные добавки способствуют этому, улучшая производительность полимерной упаковки, гарантируя, что продукты остаются неповрежденными во время транзита, одновременно снижая риск отказа упаковки.

Например,

- Согласно статье, опубликованной CarePac., руководство по упаковочным полимерам предоставляет подробную информацию о различных типах полимерных упаковочных материалов, включая синтетические и биоразлагаемые пластмассы. Он исследует распространенные полимеры, такие как полиэтилен, ПЭТ и биопластик, их применение, преимущества, риски и воздействие на окружающую среду, подчеркивая переход к устойчивым, экологически чистым альтернативам в упаковочной промышленности.

- В 2020 году, согласно статье, опубликованной Elsevier B.V., В этой главе рассматриваются пищевые упаковочные материалы, уделяя особое внимание обычным полимерам, биопластикам и нанополимерам. В нем освещаются преимущества биопластиков, такие как возобновляемость и биоразлагаемость, при решении таких проблем, как невозобновляемость в традиционных полимерах. Исследование направлено на улучшение упаковочных решений за счет технологических достижений, таких как нанотехнологии, для повышения производительности материалов.

- В феврале 2024 года, согласно статье, опубликованной Мичиганским государственным университетом, эта статья из Мичиганского государственного университета рассматривает пластиковую и полимерную упаковку, подчеркивая ее преимущества, такие как защита, экономичность и универсальность. В нем рассматриваются проблемы, связанные с потенциальными рисками для здоровья, микропластиком и воздействием на окружающую среду, при этом особое внимание уделяется текущим исследованиям по улучшению упаковочных материалов, устойчивости и безопасности потребителей.

- В январе 2024 года, согласно статье, опубликованной Polymart, PolyMart предоставляет полный обзор полимеров, используемых в упаковке пищевых продуктов, выделяя их типы, свойства и преимущества, такие как защита продуктов питания, продление срока хранения и рентабельность. Платформа предлагает бесшовные варианты закупок через приложение Buyer App, связывая покупателей с надежными поставщиками и обеспечивая ценовые тенденции в режиме реального времени.

Инновации в полимерной упаковке, обусловленные достижениями в области антиблокировочных добавок, удовлетворяют растущий спрос на высокоэффективные, устойчивые и долговечные упаковочные решения, тем самым способствуя расширению рынка антиблокировочных добавок.

Возможности

- Достижения в био-основанных антиблокировочных добавках

Разработка антиблокировочных добавок на биологической основе представляет собой значительный прогресс в области обработки полимеров, особенно в решении проблем, связанных с адгезией пленки. Традиционно неорганические антиблокировочные добавки, такие как кремнезем или тальк, использовались для смягчения блокировки — нежелательного склеивания слоев полимерной пленки. Несмотря на свою эффективность, эти неорганические добавки могут нарушать оптическую четкость пленок, особенно при более высоких концентрациях. Напротив, биологические антиблокировочные добавки предлагают устойчивую и эффективную альтернативу, повышая производительность пленки без ущерба для ясности.

Антиблокировочные добавки на биологической основе, такие как те, которые получены из природных амидов, функционируют путем миграции на поверхность полимера, образуя смазочный слой, который снижает коэффициент трения между слоями пленки. Этот механизм не только предотвращает блокировку, но и поддерживает прозрачность пленки, что имеет решающее значение для таких приложений, как упаковка пищевых продуктов, где важна видимость продукта.

Переход к био-решениям также обусловлен экологическими соображениями. Поскольку отрасли стремятся уменьшить свой экологический след, спрос на устойчивые добавки увеличился. Биологические антиблокировочные добавки, полученные из возобновляемых ресурсов, соответствуют этим целям устойчивого развития. Такие компании, как Fine Organics, разработали такие продукты, как Finawax B, рафинированный растительный бенамид, который предлагает оптимальные антиблокирующие свойства в пленках на основе полиолефинов. При использовании в сочетании с неорганическими антиблокировщиками в подходящих дозировках он эффективно уравновешивает эффективность с экологической ответственностью.

Например,

- Согласно блогу, опубликованному Cargill, Incorporated, OptislipTM BR (бехенамид) представляет собой био-антиблокировочную добавку, предназначенную для полимерных пленок. Он уменьшает блокировку путем формирования смазочного поверхностного слоя при сохранении четкости пленки. Подходит для различных полимеров, предлагает устойчивую альтернативу неорганическим добавкам, в соответствии с отраслевыми требованиями для высокоэффективных и экологически чистых упаковочных решений.

- По данным Fine Organic Industries Limited, Finawax B, растительный бенамид, является эффективной антиблокировочной добавкой на биологической основе для полиолефиновых пленок. Он минимизирует адгезию пленки при сохранении прозрачности, уменьшая зависимость от неорганических антиблокировочных агентов. Это устойчивое решение повышает производительность упаковки и согласуется с переходом отрасли к экологически чистым полимерным добавкам.

Разработка антиблокировочных добавок на биооснове знаменует собой поворот в технологии полимерных добавок. Предоставляя эффективные антиблокировочные решения, которые не ставят под угрозу ясность пленки и поддерживают инициативы в области устойчивого развития, эти добавки будут играть решающую роль в будущем упаковки и других отраслей промышленности, зависящих от полимерных пленок.

- Рост онлайн-покупок и рост упаковки для электронной коммерции

Быстрое расширение электронной коммерции значительно изменило покупательское поведение потребителей, что привело к значительному увеличению онлайн-покупок. Этот всплеск требует эффективных и надежных упаковочных решений, чтобы гарантировать, что продукция поставляется неповрежденной и презентабельной. Следовательно, существует повышенный спрос на высококачественные упаковочные пленки, которые предотвращают такие проблемы, как блокировка, когда слои пленки слипаются, препятствуют процессам упаковки и подрывают целостность продукта.

Антиблокировочные добавки играют решающую роль в решении этих проблем, уменьшая адгезию между слоями пленки, тем самым повышая эффективность операций по упаковке. Эти добавки включаются в полимерные пленки для создания микрошероховатой поверхности, минимизируя точки контакта между слоями и облегчая более плавную обработку во время производства и упаковки продукта.

Этот рост связан с ростом потребления упакованных товаров, особенно в пищевой, пищевой и фармацевтической промышленности, которые являются неотъемлемыми компонентами экосистемы электронной коммерции. Поскольку потребители все больше полагаются на онлайн-платформы для своих покупок, спрос на упаковочные пленки, которые поддерживают качество и безопасность продукции во время транзита, стал первостепенным.

Например,

- Согласно Plastiblends, Polyaddit Anti-Block Masterbatches предотвращает адгезию пленки путем введения мелких частиц, которые создают микрошероховатую поверхность, уменьшая контакт между слоями. Это повышает эффективность обработки во время производства и упаковки, обеспечивая более плавную обработку и улучшенную производительность продукта в таких отраслях, как упаковка пищевых продуктов, фармацевтические препараты и потребительские товары.

- В марте 2024 года, согласно статье Flex-Pack Engineering, Inc., всплеск онлайн-покупок и рост электронной коммерции значительно увеличили спрос на эффективные и надежные упаковочные решения. Гибкие пластиковые пленки обычно используются в упаковке из-за их легких и защитных свойств. Тем не менее, эти пленки могут держаться вместе, что может препятствовать процессам упаковки и влиять на качество продукции. Чтобы решить эту проблему, антиблокировочные добавки включаются в пластиковые пленки для создания микрошероховатой поверхности, уменьшая адгезию между слоями пленки и облегчая более плавную обработку и обработку. Это улучшение имеет решающее значение для поддержания эффективности высокоскоростных упаковочных операций, которые характерны для электронной коммерции.

- В ноябре 2019 года, согласно статье, опубликованной Furion Analytics Research & Consulting LLP, растущий спрос на упаковочные пленки в таких секторах, как продукты питания и напитки, фармацевтические препараты и потребительские товары, стал основным фактором расширения рынка упаковочной пленки. Этот рост особенно увеличил спрос на антиблокировочные добавки, которые имеют решающее значение для обработки и производительности пленок, особенно полиолефиновых пленок, таких как полиэтилен (PE) и полипропилен (PP), которые склонны к проблемам блокировки.

В заключение, всплеск онлайн-покупок и последующий рост упаковки для электронной коммерции являются ключевыми возможностями для рынка антиблокировочных добавок. Поскольку сектор электронной коммерции продолжает расширяться, важность эффективных упаковочных решений, которые обеспечивают целостность продукта и удовлетворенность клиентов, будет только усиливаться, подчеркивая критическую роль антиблокировочных добавок в упаковочной промышленности.

Ограничения/проблемы

- Наличие альтернативных добавок и решений

Наличие альтернативных добавок и решений служит значительным сдерживающим фактором на мировом рынке антиблокировочных добавок. По мере появления новых технологий и материалов производители все чаще изучают альтернативы традиционным антиблокировочным добавкам, что часто обусловлено стремлением к экономической эффективности, устойчивости и повышению производительности. Эти альтернативные добавки, которые могут предложить аналогичные или улучшенные свойства, бросают вызов спросу на традиционные антиблокировочные решения, что приводит к усилению конкуренции и снижению доли рынка для традиционных продуктов.

Одним из ключевых сдерживающих факторов, обусловленных наличием альтернатив, является смещение предпочтения в сторону экологически чистых или биоразлагаемых добавок. По мере того, как устойчивость становится все более серьезной проблемой во многих отраслях, производители ищут решения, которые минимизируют воздействие на окружающую среду. В то время как традиционные антиблокировочные добавки эффективны, такие альтернативы, как натуральные или биопроизводные добавки, набирают обороты, создавая потенциальный сдвиг в рыночном спросе. Эти альтернативы часто воспринимаются как более экологически ответственные, отдавая предпочтение им перед обычными химическими добавками. Более того, достижения в области материаловедения привели к разработке инновационных решений на основе полимеров, которые обеспечивают улучшенные свойства снижения трения без необходимости традиционных антиблокировочных добавок. Эти новые решения могут обеспечить превосходную производительность, уменьшая зависимость от добавок и, в свою очередь, влияя на спрос на антиблокировочные продукты.

Кроме того, важную роль играют соображения стоимости. Производители могут выбрать альтернативные добавки, если они более рентабельны, особенно в регионах с высокой ценовой чувствительностью. Этот ценовой сдвиг может усугубиться, если альтернативные решения продемонстрируют сопоставимую или превосходную производительность при более низкой стоимости.

Например,

- В мае 2019 года, согласно статье, опубликованной Plastics Technology, DuPont запустила мастербатч Dow Corning AMB-12235, сочетающий антиблокировочные и пробуксовочные добавки для улучшения обработки пленки PE. Эта силиконовая композиция обеспечивает низкий коэффициент трения, предотвращает блокировку пленки и уменьшает миграцию при низких нагрузках (4-6%), оптимизируя производство, уменьшая сложность и экономя пространство в цепочке поставок.

- Согласно статье, опубликованной ChemPoint., силиконовые шарики Momentive Tospearl представляют собой усовершенствованные антиблокировочные и проскальзывающие добавки для полиолефиновых пленок, предназначенные для предотвращения адгезии между слоями и снижения коэффициента трения при экструзии. Эти добавки улучшают четкость пленки и эффективность обработки, а также сокращают время простоя, будучи одобренными FDA для приложений для контакта с пищевыми продуктами и термически стабильными до 400 ° C.

В целом, наличие альтернативных добавок и решений создает проблему для роста рынка антиблокировочных добавок, поскольку производители могут отдавать приоритет новым, более устойчивым или экономически эффективным вариантам, ограничивая рыночный потенциал для традиционных антиблокировочных продуктов.

- Нормативно-правовое соответствие и стандарты тестирования

Рынок антиблокировочных добавок подчиняется строгим нормативным требованиям и стандартам тестирования для обеспечения безопасности продукции и защиты окружающей среды. В Соединенных Штатах Управление по контролю за продуктами и лекарствами (FDA) контролирует вещества, предназначенные для контакта с пищевыми продуктами, включая антиблокировочные добавки, используемые в упаковочных материалах. Производители должны продемонстрировать, что эти добавки безопасны для их предполагаемого использования, что предполагает тщательную оценку сырья и потенциальную миграцию в пищевые продукты.

Европейское химическое агентство (ECHA) и Европейское агентство по безопасности пищевых продуктов (EFSA) играют ключевую роль в оценке безопасности химических веществ, включая антиблокировочные добавки. Регламент REACH предписывает производителям и импортерам регистрировать химические вещества, включая их предполагаемое использование и данные о безопасности. Эта строгая нормативная среда гарантирует, что все материалы, контактирующие с пищевыми продуктами, безопасны и не угрожают здоровью населения.

Регулятивная база, окружающая антиблокировочные добавки, имеет решающее значение для обеспечения безопасности продукции, защиты окружающей среды и соответствия отраслевым стандартам. Антиблокировочные добавки обычно используются в упаковочных материалах, особенно в полиэтиленовых пленках, чтобы предотвратить слипание листов, что может значительно улучшить удобство использования и качество продукции. Однако их широкое использование обусловило необходимость разработки всеобъемлющих руководящих принципов регулирования их использования.

Различные страны и регионы установили свои нормативные руководящие принципы. Например, в Соединенных Штатах Управление по контролю за продуктами и лекарствами (FDA) контролирует использование веществ, предназначенных для контакта с пищевыми продуктами, включая добавки, используемые в упаковке пищевых продуктов. FDA требует, чтобы все вещества, контактирующие с пищевыми продуктами, были безопасными для их предполагаемого использования, что включает тщательный анализ сырья и потенциальную миграцию добавок в пищевые продукты.

Например,

- В январе 2025 года, согласно блогу, опубликованному Европейским управлением по безопасности пищевых продуктов, EFSA предоставила подробную информацию о пищевых добавках, уделяя особое внимание оценке безопасности и нормативной базе в Европейском союзе. Их оценки помогают гарантировать, что добавки, используемые в упаковке пищевых продуктов, такие как антиблокировочные агенты, безопасны для потребителей и соответствуют строгим экологическим и медицинским стандартам для защиты общественного благополучия.

- Европейское химическое агентство (ECHA) предоставляет полный обзор законодательства для активных и интеллектуальных материалов, предназначенных для контакта с пищевыми продуктами. Это включает в себя правила, обеспечивающие безопасность материалов, таких как антиблокировочные агенты, используемые в упаковке. Структура ECHA помогает защитить здоровье потребителей и обеспечивает соответствие стандартам ЕС по безопасности пищевых продуктов.

Соблюдение нормативных требований и стандартов тестирования имеет важное значение для рынка антиблокировочных добавок для обеспечения безопасности продукции, экологической устойчивости и здоровья потребителей. Строгий надзор со стороны таких органов, как FDA, ECHA и EFSA, помогает поддерживать целостность отрасли, способствуя более безопасному и эффективному использованию добавок в упаковочных материалах.

Влияние и текущий рыночный сценарий дефицита сырья и задержек в доставке

Data Bridge Market Research предлагает высокоуровневый анализ рынка и предоставляет информацию, учитывая влияние и текущую рыночную среду нехватки сырья и задержек поставок. Это означает оценку стратегических возможностей, создание эффективных планов действий и оказание помощи предприятиям в принятии важных решений.

Помимо стандартного отчета, мы также предлагаем углубленный анализ уровня закупок от прогнозируемых задержек поставок, картирование дистрибьюторов по регионам, анализ сырьевых товаров, анализ производства, тенденции картирования цен, поиск источников, анализ эффективности категорий, решения по управлению рисками в цепочке поставок, расширенный бенчмаркинг и другие услуги для закупок и стратегической поддержки.

Ожидаемое влияние экономического спада на цены и доступность продукции

Когда экономическая активность замедляется, отрасли начинают страдать. Прогнозируемое влияние экономического спада на ценообразование и доступность продукции учитывается в отчетах и разведывательных службах, предоставляемых DBMR. При этом наши клиенты обычно могут на один шаг опережать своих конкурентов, прогнозировать свои продажи и доходы и оценивать свои расходы на прибыль и убытки.

Ближний Восток и Африка Антиблокировочный рынок

Рынок сегментирован на основе типа, целевого полимера и отрасли конечного использования. Рост среди этих сегментов поможет вам проанализировать скудные сегменты роста в отраслях и предоставить пользователям ценный обзор рынка и понимание рынка, чтобы помочь им принимать стратегические решения для определения основных рыночных приложений.

форма

- неорганический

- органический

Целевой полимер

- Полиэтилен (PE)

- Поливинилхлорид (ПВХ)

- Биаксиально-ориентированный полипропилен (BOPP)

- Полиэтилентерефталат (ПЭТ)

- Полистирол (PS)

- Другие

Конечная промышленность

- Упаковка

- промышленный

- Сельское хозяйство

- Медицина и здравоохранение

- Электроника и солнечная

- Печать и оптика

- Другие

Ближний Восток и Африка: региональный анализ антиблокировочного рынка

Рынок анализируется, и информация о размере рынка и тенденциях представлена по странам, типам, целевым полимерам и отрасли конечного использования, как указано выше.

Странами, охваченными рынком, являются Саудовская Аравия, ОАЭ, Южная Африка, Египет, Израиль и остальная часть Ближнего Востока и Африки.

Саудовская Аравия готова доминировать на рынке благодаря быстро растущему сельскохозяйственному сектору и растущему спросу на высокопроизводительные пленки. Правительственные инициативы, усилия по сохранению водных ресурсов и передовые сельскохозяйственные технологии стимулируют рост, обеспечивая повышение урожайности сельскохозяйственных культур, устойчивость и повышение эффективности сельского хозяйства.

Саудовская Аравия является самой быстрорастущей страной в регионе благодаря масштабным инвестициям в сельское хозяйство, инфраструктуру и промышленный сектор. Правительственные инициативы, такие как Vision 2030, технологические достижения и растущий спрос на высокопроизводительные материалы, стимулируют расширение рынка, стимулируя инновации и экономическую диверсификацию.

В страновом разделе отчета также представлены отдельные факторы, влияющие на рынок, и изменения в регулировании на внутреннем рынке, которые влияют на текущие и будущие тенденции рынка. Точки данных, такие как анализ цепочки создания стоимости, технические тенденции и анализ пяти сил Портера, тематические исследования, являются некоторыми из указателей, используемых для прогнозирования рыночного сценария для отдельных стран. Кроме того, рассматриваются наличие и доступность глобальных брендов и их проблемы, с которыми сталкиваются из-за большой или скудной конкуренции со стороны местных и отечественных брендов, влияние внутренних тарифов и торговых маршрутов при предоставлении прогнозного анализа данных по стране.

Ближневосточный и африканский антиблокировочный рынок

Конкурентный ландшафт рынка предоставляет детали конкурентам. Подробности включают в себя обзор компании, финансовые показатели компании, генерируемые доходы, рыночный потенциал, инвестиции в исследования и разработки, новые рыночные инициативы, глобальное присутствие, производственные площадки и объекты, производственные мощности, сильные и слабые стороны компании, запуск продукта, ширина и широта продукта, доминирование приложений. Приведенные выше данные касаются только фокуса компаний на рынке.

Ближний Восток и Африка Антиблокировочная добавкаЛидерами рынка, работающими на рынке, являются:

- Имерис (Франция)

- Ampacet CORPORATION (США)

- ALTANA (Германия)

- Dow (США)

- Lyondellbasell Industries Holdings BV (Нидерланды)

- Astra Polymers (Саудовская Аравия)

- Avient Corporation (США)

- BASF (Германия)

- Cargill, Incorporated (США)

- Covia Holdings LLC. (США)

- Эвоник (Германия)

- Компания Fine Organic Industries Limited (Индия)

- Honeywell International Inc (США)

- Inerals Technologies Inc. (США)

- Momentive Performance Materials (США)

- National Plastics Color, Inc. (США)

- plasmix pvt ltd (Индия)

- SABIC (Саудовская Аравия)

- Sukano AG (Швейцария)

- W. R. Grace & Co.-Conn (США)

- Wells Plastics (Великобритания)

Последние события на Ближнем Востоке и в Африке Антиблокировочный рынок

- В декабре 2024 года SABIC представила поликарбонатные сополимерные смолы LNP ELCRES CXL, предлагающие исключительную химическую стойкость, идеально подходящую для мобильности, электроники, промышленности и инфраструктуры. Эти материалы обеспечивают улучшенную долговечность, погодные условия и низкотемпературную ударопрочность. Доступные в биовозобновляемых версиях в рамках программы SABIC TRUCIRCLE, они способствуют устойчивости и повышению производительности деталей даже при резком химическом воздействии.

- В ноябре 2017 года SABIC возобновила свое почетное стратегическое партнерство с Боаоским форумом для Азии (BFA), отмечая 17 лет подряд спонсорства. Это партнерство подчеркивает приверженность SABIC устойчивому развитию посредством межрегионального сотрудничества. Компания продолжает использовать BFA в качестве платформы для усиления влияния и стимулирования инклюзивного развития во всем мире.

- В январе 2025 года Evonik Industries AG и Fuhua Tongda Chemicals Company создали совместное предприятие в Лешане, Китай, для производства специализированной перекиси водорода (H2O2) для таких применений, как солнечные батареи, полупроводники и упаковка пищевых продуктов. С Evonik 51% и Fuhua 49%, предприятие начнет поставлять на рынок в 2026 году. Это партнерство укрепляет присутствие Evonik в Азиатско-Тихоокеанском регионе.

- В июне 2024 года Covia Holdings LLC завершила разделение своего энергетического и промышленного бизнеса на два независимых предприятия: Covia Energy, LLC со штаб-квартирой в Вудлендсе, штат Техас, и Covia Solutions, базирующаяся в Независимости, штат Огайо. Этот стратегический шаг позволяет каждой компании сосредоточиться на своих рыночных возможностях.

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Содержание

1 Введение

1.1 Цели исследования

1.2 Маркетологическое определение

1.3 Просмотр

1.4 Ограничения

1.5 МАРКЕТЫ

2 МАРКЕТНАЯ СЕГМЕНТАЦИЯ

2.1 Приняты меры

2.2 ГЕОГРАФИЧЕСКАЯ СКОПА

2,3 года, присланные на обучение

2.4 КУРРЕНСИЯ И ПРИЧИНА

2.5 DBMR TRIPOD DATA VALIDATION

2.6 МУЛЬТИВАРИАТНОЕ МОДЕЛИРОВАНИЕ

2.7 Первичное Интервью с ключевыми лидерами

2.8 DBMR MARKET POSITION GRID

2.9 DBMR VENDOR SHARE ANALYSIS

2.1 МАРКЕТНАЯ ПРИМЕЧАНИЕ КОВЕРАГ ГРИД

2.11 Вторичные источники

2.12 Предложения

3 ИСПОЛНИТЕЛЬНАЯ РЕЗЮМЕ

4 Премиум Впечатления

4.1 ПЕСТЕЛЬНЫЙ АНАЛИЗ

4.1.1 Политические факторы

4.1.2 Экономические факторы

4.1.3 Социальные работники

4.1.4 Технические характеристики

4.1.5 ОБЩИЕ ФАКТОРЫ

4.1.6 Правовые факторы

4.2 АНАЛИЗ ПЯТИ СИЛ ПОРТЕРА

4.2.1 Угроза новых предпринимателей

4.2.2 СОСТОЯТЕЛЬНАЯ ВЛАСТЬ ПОСТОЯТЕЛЕЙ

4.2.3 СОБРАЩАЮЩАЯСЯ ВЛАСТЬ ПОКУПАТЕЛЕЙ

4.2.4 Угроза субститутов

4.2.5 Внутренняя конкуренция

4.3 Критерии отбора вендоров

4.3.1 КАЧЕСТВО И КОНСИСТЕМНОСТЬ

4.3.2 Технический опыт

4.3.3 Цепная надежность

4.3.4 СОСТОЯНИЕ И УСТАНОВЛЕНИЕ

4.3.5 Стоимость и ценовая структура

4.3.6 Финансовая стабильность

4.3.7 ПРЕДОСТАВЛЕНИЕ И КУСТОМИЗАЦИЯ

4.3.8 УПРАВЛЕНИЕ РИСКАМИ И ПЛАНЫ КОНТИНГЕНЦИИ

5 МАРКЕТНЫЙ ОБЗОР

5.1 Водители

5.1.1 Растущее требование к ПЛАСТИЧЕСКОЙ ПАКТАГИИ

5.1.2 АВТОМОТИВНЫЕ И ИНДУСТРИАЛЬНЫЕ СЕКТОРЫ

5.1.3 ИННОВАЦИИ И ПРИНЯТИЯ В ПОЛИМЕРНОЙ ПАКТАЖЕ

5.1.4 Быстрое расширение агрикультурного сектора и растущая потребность в высокопроизводительных фильмах

5.2 УВЕДОМЛЕНИЯ

5.2.1 ФЛЮКТУАЦИЯ РЕАЛЬНЫХ МАТЕРИАЛЬНЫХ ЦЕН

5.2.2 Доступность альтернативных подходов и решений

5.3 Положения

5.3.1 ПРЕДОСТАВЛЕНИЯ В БИО-БАСОВАННЫХ АНТИБЛОКОВ

5.3.2 ОБРАЩЕНИЕ В ОНЛАЙН-ШОППИНГЕ И РОСТ В ЭКОНОМИЧЕСКОМ ПАКЕ

5.4 Вызовы

5.4.1 СОСТОЯНИЕ ПРАВИТЕЛЬСТВА И СТАНДАРТЫ ИСПЫТАНИЯ

5.4.2 Переворачивание потребителю, содержащемуся в бумажной упаковке

6 МЕЖДУНАРОДНЫЙ ВОСТОК И АФРИКА АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ

6.1 Проверка

6.2 ИНОРГАНИЧЕСКИЙ

6.2.1 ИНОРГАНИЧЕСКИЙ, ПО ТИПУ

6.2.2 ИНОРГАНИЧЕСКИЙ, СТАТЬЯ

6.3 ОРГАНИЧЕСКИЙ

6.3.1 ОРГАНИЧЕСКИЙ, ПО ФОРМЕ

7 МЕДЛЯ И АФРИКА АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ, ТАРГЕТ ПОЛИМЕР

7.1 Проверка

7.2 Полиэтилен (ПЭ)

7.2.1 Полиэтилен (ПЭ), ПОЛИМЕР ТАРГЕТА

7.3 Поливинилхлорид (ПВХ)

7.4 Биаксилли-ориентированный полипропилен (BOPP)

7.5 Полиэтилентерефталат (ПЭТ)

7.6 Полистирол (ПС)

7.7 Другие

8 МЕДЛЯ И АФРИКА АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ, КОНЦЕ ИСПОЛЬЗОВАНИЯ ПРОМЫШЛЕНИЯ

8.1 Проверка

8.2 Упаковка

8.3 Промышленность

8.4 Агрикультура

8.5 Медицинская и медицинская помощь

8.6 Электроника и солнце

8.7 ПРИНИМАНИЕ И ОФТИКА

8.8 Другие

9 МЕДЛЯ И АФРИКА АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ, ПО РЕГИОНУ

9.1 Средний Восток и Африка

9.1.1 САУДИ АРАБИЯ

9.1.2 ЕАОС

9.1.3 Южная Африка

9.1.4 ЕГИПТ

9.1.5 Израиль

9.1.6 Продолжительность пребывания в Средние века и Африке

10 Средний Восток и АФРИКА АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ: КОМПАНИЯ ЛЭНДСКАП

10.1 КОМПАНИЯ ДОЛЖНА АНАЛИЗАЦИЯ: Средний Восток и Африка

11 СВОТ АНАЛИЗ

12 КОМИТЕТНЫХ ПРОФИЛ

12.1 ИМЕРИИ

12.1.1 КОМПАНИЯ СНАПШОТ

12.1.2 РЕВЕНУАЛЬНЫЙ АНАЛИЗ

12.1.3 КОМПАНИЯ ДЛЯ АНАЛИЗА

12.1.4 ПРОДУКТ ПОРТФОЛИО

12.1.5 ПРОЕКТ РАЗВИТИЯ

12.2 АМПЕЙСКАЯ КОРПОРАЦИЯ

12.2.1 КОМПАНИЯ СНАПШОТ

12.2.2 КОМПАНИЯ ДЛЯ АНАЛИЗА

12.2.3 ПРОДУКТ ПОРТФОЛИО

12.2.4 ТЕХНОЛОГИИ

12.3 Алтана

12.3.1 КОМПАНИЯ СНАПШОТ

12.3.2 КОМПАНИЯ ДЛЯ АНАЛИЗА

12.3.3 ПРОДУКТ ПОРТФОЛИО

12.3.4 РАЗВИТИЯ РЕЦЕНТОВ

12,4 Дау

12.4.1 КОМПАНИЯ СНАПШОТ

12.4.2 РЕВЕННЫЙ АНАЛИЗ

12.4.3 КОМПАНИЯ ДЛЯ АНАЛИЗА

12.4.4 ПРОДУКТ ПОРТФОЛИО

12.4.5 РАЗВИТИЯ РЕЦЕНТОВ

12.5 ИНДУСТРИИ ЛИОНДЕЛЬБАСЕЛЬНЫХ ХОЛДИНГОВ B.V.

12.5.1 КОМПАНИЯ СНАПШОТ

12.5.2 РЕВЕННЫЙ АНАЛИЗ

12.5.3 КОМПАНИЯ ДЛЯ АНАЛИЗА

12.5.4 ПРОДУКТ ПОРТФОЛИО

12.5.5 РАЗВИТИЕ РЕЦЕНТОВ

12.6 ПОЛИМЕРЫ АСТРА

12.6.1 КОМПАНИЯ СНАПШОТ

12.6.2 ПРОДУКТ/БРЭНД ПОРТФОЛИО

12.6.3 ТЕХНОЛОГИИ

12.7 Корпоративная деятельность

12.7.1 КОМПАНИЯ СНАПШОТ

12.7.2 РЕВЕННЫЙ АНАЛИЗ

12.7.3 ПРОДУКТ ПОРТФОЛИО

12.7.4 ПРОЕКТ РАЗВИТИЯ

12.8 BASF

12.8.1 КОМПАНИЯ СНАПШОТ

12.8.2 РЕВЕННЫЙ АНАЛИЗ

12.8.3 ПРОДУКТ ПОРТФОЛИО

12.8.4 ПРОЕКТ РАЗВИТИЯ

12.9 КАРГИЛЛ, ИНКОРПОРАТОР

12.9.1 КОМПАНИЯ СНАПШОТ

12.9.2 ПРОДУКТ ПОРТФОЛИО

12.9.3 ТЕХНОЛОГИИ

12.1 COVIA HOLDINGS LLC.

12.10.1 КОМПАНИЯ СНАПШОТ

12.10.2 ПРОДУКТ ПОРТФОЛИО

12.10.3 ПРОЕКТ РАЗВИТИЯ

12.11 Эвоник

12.11.1 КОМПАНИЯ СНАПШОТ

12.11.2 РЕВЕНУАЛЬНЫЙ АНАЛИЗ

12.11.3 ПРОДУКТ ПОРТФОЛИО

12.11.4 ТЕХНОЛОГИИ

12.12 ОГРАНИЧЕННЫЕ ОГРАНИЧЕННЫЕ ПРОМЫШЛЕНИЯ

12.12.1 КОМПАНИЯ СНАПШОТ

12.12.2 АНАЛИЗ РЕВЕНУА

12.12.3 ПРОДУКТ ПОРТФОЛИО

12.12.4 РАЗВИТИЯ РЕЦЕНТОВ

12.13 МЕЖДУНАРОДНЫЙ ИНК

12.13.1 КОМПАНИЯ СНАПШОТ

12.13.2 РЕВЕННЫЙ АНАЛИЗ

12.13.3 ПРОДУКТ ПОРТФОЛИО

12.13.4 ТЕХНОЛОГИИ

12.14 Инеральные технологии.

12.14.1 КОМПАНИЯ СНАПШОТ

12.14.2 РЕВЕННЫЙ АНАЛИЗ

12.14.3 ПРОДУКТ ПОРТФОЛИО

12.14.4 ПРОЕКТ РАЗВИТИЯ

12.15 МОМЕНТНЫЕ ПЕРФОРМАЦИИ

12.15.1 КОМПАНИЯ СНАПШОТ

12.15.2 ПРОДУКТ ПОРТФОЛИО

12.15.3 РАЗВИТИЯ РЕЦЕНТОВ

12.16 Национальный цвет пластики, INC.

12.16.1 КОМПАНИЯ СНАПШОТ

12.16.2 ПРОДУКТ ПОРТФОЛИО

12.16.3 ТЕХНОЛОГИИ

12.17 PLASMIX PVT LTD

12.17.1 КОМПАНИЯ СНАПШОТ

12.17.2 ПРОДУКТ ПОРТФОЛИО

12.17.3 ПРОЕКТ РАЗВИТИЯ

12.18 Сабик

12.18.1 КОМПАНИЯ СНАПШОТ

12.18.2 АНАЛИЗ РЕВЕНУА

12.18.3 ПРОДУКТ ПОРТФОЛИО

12.18.4 РАЗВИТИЯ РЕЦЕНТОВ

12.19 СУКАНО АГ

12.19.1 КОМПАНИЯ СНАПШОТ

12.19.2 ПРОДУКТ/БРЭНД ПОРТФОЛИО

12.19.3 РАЗВИТИЯ РЕЦЕНТОВ

12.2 W. R. GRACE & CO.-CONN

12.20.1 КОМПАНИЯ СНАПШОТ

12.20.2 ПРОДУКТ ПОРТФОЛИО

12.20.3 РАЗВИТИЯ РЕЦЕНТОВ

12.21 Уэллс Пластик

12.21.1 КОМПАНИЯ СНАПШОТ

12.21.2 ПРОДУКТ ПОРТФОЛИО

12.21.3 РАЗВИТИЯ РЕЦЕНТОВ

13 Вопросник

14 Связанные поправки

Список таблиц

Таблица 1 Средний Восток и АФРИКА АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (USD THOUSAND)

Таблица 2 Средний Восток и АФРИКА АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 3 МЕЖДУНАРОДНЫЙ ВОСТОК И АФРИКА ИНОРГАНИЧЕСКИЙ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ПО РЕГИОНУ, 2018-2032 (USD THOUSAND)

СТАТЬЯ 4 МИДЛЯ ВОСТОК И АФРИКА ИНОРГАНИЧЕСКАЯ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ПО РЕГИОНУ, 2018-2032, (ТОНС)

СТАТЬЯ 5 МЕЖДУНАРОДНЫЙ ВОСТОК И АФРИКА ИНОРГАНИЧЕСКИЙ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, В ТИПЕ, 2018-2032 (USD THOUSAND)

СТАТЬЯ 6 МЕЖДУНАРОДНЫЙ ВОСТОК И АФРИКА ИНОРГАНИЧЕСКИЙ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, В ТИПЕ, 2018-2032 (ТОНС)

СТАТЬЯ 7 МЕЖДУНАРОДНЫЙ ВОСТОК И АФРИКА ИНОРГАНИЧЕСКИЙ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, СТАТЬЯ, 2018-2032 (USD THOUSAND)

СТАТЬЯ 8 СРЕДСТВО И АФРИКА ИНОРГАНИЧЕСКИЙ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, СТАТЬЯ, 2018-2032 (ТОНС)

СТАТЬЯ 9 СРЕДСТВО И АФРИКА ОРГАНИЧЕСКИЙ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ПО РЕГИОНУ, 2018-2032 (USD THOUSAND)

СТАТЬЯ 10 МИДЛЯ ВОСТОК И АФРИКА ОРГАНИЧЕСКИЙ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ПО РЕГИОНУ, 2018-2032, (ТОНС)

СТАТЬЯ 11 МЕДЛЯ И АФРИКА ОРГАНИЧЕСКИЙ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 12 СРЕДСТВО И АФРИКА ОРГАНИЧЕСКАЯ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 13 ВОСТОК И АФРИКА АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ, ПОЛИМЕР ТАРГЕТА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 14 МЕДЛЯ И АФРИКА АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ, ТАРГЕТ ПОЛИМЕР, 2018-2032 (ТОНС)

СТАТЬЯ 15 МИДЛЯ ВОСТОК И ПОЛИТЕТИЛЕНА АФРИКИ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, РЕГИОН, 2018-2032 (USD THOUSAND)

Таблица 16 Средний Восток и Африка Полиэтилен (ПЭ) В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ПРИ РЕГИОНЕ, 2018-2032, (ТОНС)

TABLE 17 MIDDLE EAST and AFRICA POLYETHYLENE (PE) IN ANTIBLOCK ADDITIVE MARKET, BY TARGET POLYMER, 2018-2032 (USD THOUSAND)

Таблица 18 Средний Восток и Африка Полиэтилен (ПЭ) В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ТАРГЕТ ПОЛИМЕР, 2018-2032 (ТОНС)

СТАТЬЯ 19 МЕДЛЯ И АФРИКА ПОЛИВИНИЛ ХЛОРИД (ПВХ) В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ПО РЕГИОНУ, 2018-2032 (USD THOUSAND)

Таблица 20 Средний Восток и Африка Поливинил Хлорид (ПВХ) В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ПРИ РЕГИОНЕ, 2018-2032, (ТОНС)

СТАТЬЯ 21 СРЕДСТВО И АФРИКА БИАКСИАЛЬНО-ОРИЕНЦИАЛЬНЫЙ ПОЛИПРОПИЛЕН (БОПП) В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ПО РЕГИОНУ, 2018-2032 (USD THOUSAND)

СТАТЬЯ 22 СРЕДСТВО И АФРИКА БИАКСИАЛЬНО-ОРИЕНТНЫЙ ПОЛИПРОПИЛЕН (БОПП) В АНТИБЛОКСКОМ АДДИТИВНОМ МАРКЕ, ПРИ РЕГИОНЕ, 2018-2032, (ТОНС)

СТАТЬЯ 23 МЕДЛЯ И АФРИКА ПОЛИТЕТИЛЕННЫЙ ТЕРЕФТАЛАТ (ПЭТ) В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ПО РЕГИОНУ, 2018-2032 (USD THOUSAND)

СТАТЬЯ 24 МЕДЛЯ И АФРИКА ПОЛИТЕТИЛЕННЫЙ ТЕРЕФТАЛАТ (ПЭТ) В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ПО РЕГИОНУ, 2018-2032, (ТОНС)

СТАТЬЯ 25 МИДЛЯ ВОСТОК И ПОЛИСТИРЕНА АФРИКИ (PS) В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ПО РЕГИОНУ, 2018-2032 (USD THOUSAND)

СТАТЬЯ 26 ВОСТОК И ПОЛИСТИРЕНА АФРИКИ (PS) В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ПО РЕГИОНУ, 2018-2032, (ТОНС)

СТАТЬЯ 27 СРЕДСТВО И АФРИКА ДРУГИЕ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ПРИ РЕГИОНЕ, 2018-2032 (USD THOUSAND)

СТАТЬЯ 28 СРЕДСТВО И АФРИКА ДРУГИЕ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ПРИ РЕГИОНЕ, 2018-2032 (ТОНС)

СТАТЬЯ 29 МЕДЛЯ И АФРИКА АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ, К концу использования промышленности, 2018-2032 (USD THOUSAND)

СТАТЬЯ 30 СРЕДСТВО И АФРИКА АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ, К концу использования Индустрии, 2018-2032 (ТОНС)

СТАТЬЯ 31 ПОСЛЕДНИЙ И АФРИКА ПОДДЕРЖАЕТ В АНТИБЛОКСКОМ АДДИТИВНОМ МАРКЕ, ПО РЕГИОНУ, 2018-2032, (USD THOUSAND)

СТАТЬЯ 32 МЕДЛЯ ВОСТОК И АФРИКА ПАКАКУЮТСЯ В АНТИБЛОКСКОМ АДДИТИВНОМ МАРКЕ, ПРИ РЕГИОНЕ, 2018-2032 (ТОНС)

СТАТЬЯ 33 ПОСЛЕДНИЕ И АФРИКА ПАКАКУЕТСЯ В АНТИБЛОКСКОМ АДДИТИВНОМ МАРКЕТЕ, КИТАЙ, 2018-2032 (USD THOUSAND)

СТАТЬЯ 34 ПОСЛЕДНИЕ И АФРИКА ПАКАКУЕТСЯ В АНТИБЛОКСКОМ АДДИТИВНОМ МАРКЕТЕ, КИТАЙ, 2018-2032 (ТОНС)

СТАТЬЯ 35 МИДЛЯ ВОСТОК И АФРИКА ПАКАКУЮТ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 36 МЕДЛЯ ВОСТОК И АФРИКА ПАКАКУЮТ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 37 МЕДЛЯ ВОСТОК И АФРИКА ИНДУСТРИАЛЬНЫЙ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ПО РЕГИОНУ, 2018-2032, (USD THOUSAND)

СТАТЬЯ 38 МИДЛЯ ВОСТОК И АФРИКА ИНДУСТРИАЛЬНЫЙ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ПО РЕГИОНУ, 2018-2032 (ТОНС)

СТАТЬЯ 39 МИДЛЯ ВОСТОК И АФРИКА ИНДУСТРИАЛЬНЫЙ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, В ТИПЕ, 2018-2032 (USD THOUSAND)

СТАТЬЯ 40 МЕЖДУНАРОДНЫЙ ВОСТОК И АФРИКАНСКИЙ ИНДУСТРИАЛ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ВЫБОР, 2018-2032 (ТОНС)

TABLE 41 MIDDLE EAST and AFRICA INDUSTRIAL IN ANTIBLOCK ADDITIVE MARKET, BY FORM, 2018-2032 (USD THOUSAND)

СТАТЬЯ 42 МИДЛЯ ВОСТОК И АФРИКА ИНДУСТРИАЛ В АНТИБЛОКСКОМ АДДИТИВНОМ МАРКЕ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 43 МЕЖДУНАРОДНЫЙ ВОСТОК И АФРИКА АГРИКУЛЬТУРА В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ПРИ РЕГИОНЕ, 2018-2032, (USD THOUSAND)

СТАТЬЯ 44 ПОСЛЕДНИЙ ВОСТОК И АФРИКА АГРИКУЛЬТУРА В АНТИБЛОКСКОМ АДДИТИВНОМ МАРКЕ, ПО РЕГИОНУ, 2018-2032 (ТОНС)

СТАТЬЯ 45 МИДЛЯ ВОСТОК И АФРИКА АГРИКУЛЬТУРА В АНТИБЛОКСКОМ АДДИТИВНОМ МАРКЕ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 46 МЕЖДУНАРОДНЫЙ ВОСТОК И АФРИЧЕСКАЯ АГРИКУЛЬТУРА В АНТИБЛОКНОМ АДДИТИВНОМ МАРКЕ, ФОРМА, 2018-2032 (ТОНС)

TABLE 47 MIDDLE EAST AND AFRICA MEDICAL AND HEALTHCARE IN ANTIBLOCK ADDITIVE MARKET, BY REGION, 2018-2032, (USD THOUSAND)

СТАТЬЯ 48 МЕДЛЯ ВОСТОК И АФРИКА МЕДИЦИНАЛЬНАЯ И ЗДОРОВЬЯ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ПРИ РЕГИОНЕ, 2018-2032 (ТОНС)

СТАТЬЯ 49 МЕДЛЯ ВОСТОК И АФРИКА МЕДИЦИНСКАЯ И ЗДОРОВЬЯ В АНТИБЛОКСКОМ АДДИТИВНОМ МАРКЕ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 50 СРЕДСТВО И АФРИКА МЕДИЦИНСКИЕ И ЗДОРОВЬЯ В АНТИБЛОКСКОМ АДДИТИВНОМ МАРКЕ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 51 СРЕДСТВО И АФРИКА ЭЛЕКТРОНИКА И СОЛАР В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ПО РЕГИОНУ, 2018-2032, (USD THOUSAND)

СТАТЬЯ 52 СРЕДСТВО И АФРИКА ЭЛЕКТРОНИКА И СОЛАР В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ПО РЕГИОНУ, 2018-2032 (ТОНС)

СТАТЬЯ 53 СРЕДСТВО И АФРИКА ЭЛЕКТРОНИКА И СОЛАР В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, В ТИПЕ, 2018-2032 (USD THOUSAND)

СТАТЬЯ 54 СРЕДСТВО И АФРИКА ЭЛЕКТРОНИКА И СОЛАР В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, В ТИПЕ, 2018-2032 (ТОНС)

СТАТЬЯ 55 СРЕДСТВО И АФРИКА ЭЛЕКТРОНИКА И СОЛАР В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 56 СРЕДСТВО И АФРИКА ЭЛЕКТРОНИКА И СОЛАР В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 57 СРЕДСТВО И АФРИКА ПРИНИМАЮЩИЕСЯ И ОФТИКИ В АНТИБЛОКНОМ АДДИТИВНОМ МАРКЕ, ПО РЕГИОНУ, 2018-2032, (USD THOUSAND)

СТАТЬЯ 58 СРЕДСТВО И АФРИКА ПРИНИМАЯ И ОФТИКА В АНТИБЛОКНОМ АДДИТИВНОМ МАРКЕ, ПО РЕГИОНУ, 2018-2032 (ТОНС)

СТАТЬЯ 59 МИДЛЯ ВОСТОК И АФРИКА ПРИНТИРОВАНИЕ И ОФТИКА В АНТИБЛОКНОМ АДДИТИВНОМ МАРКЕ, ВЫБОР, 2018-2032 (USD THOUSAND)

СТАТЬЯ 60 МИДЛЯ ВОСТОК И АФРИКА ПРИНТИРОВАНИЕ И ОФТИКА В АНТИБЛОКНОМ АДДИТИВНОМ МАРКЕТЕ, ТИП, 2018-2032 (ТОНС)

СТАТЬЯ 61 МИДЛЯ ВОСТОК И АФРИКА ПРИНТИНГ И ОФТИКА В АНТИБЛОКСКОМ АДДИТИВНОМ МАРКЕ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 62 МЕЖДУНАРОДНЫЙ ВОСТОК И ПРИНИМАНИЕ АФРИКИ И ОФТИКА В АНТИБЛОКНОМ АДДИТИВНОМ МАРКЕ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 63 МЕЖДУНАРОДНЫЙ ВОСТОК И ДРУГИЕ АФРИКИ В АНТИБЛОКНОМ АДДИТИВНОМ МАРКЕ, ПРИ РЕГИОНЕ, 2018-2032, (USD THOUSAND)

СТАТЬЯ 64 МЕЖДУНАРОДНЫЙ ВОСТОК И ДРУГИЕ АФРИКА В АНТИБЛОКНОМ АДДИТИВНОМ МАРКЕ, ПРИ РЕГИОНЕ, 2018-2032 (ТОНС)

СТАТЬЯ 65 СРЕДСТВО И ДРУГИЕ АФРИКА В АНТИБЛОКНОМ АДДИТИВНОМ МАРКЕ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 66 СРЕДСТВО И АФРИКА ДРУГИЕ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 67 ВОСТОК И АФРИКА АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ, СТРАНА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 68 ВОСТОК И АФРИКА АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ, СТРАНА, 2018-2032 (ТОНС)

Таблица 69 Средний Восток и АФРИКА АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (USD THOUSAND)

Таблица 70 Средний Восток и АФРИКА АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 71 МИДЛЯ ВОСТОК И АФРИКА ИНОРГАНИЧЕСКАЯ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, В ТИПЕ, 2018-2032 (USD THOUSAND)

СТАТЬЯ 72 МИДЛЯ ВОСТОК И АФРИКА ИНОРГАНИЧЕСКАЯ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, В ТИПЕ, 2018-2032 (ТОНС)

СТАТЬЯ 73 МЕДЛЯ ВОСТОК И АФРИКА ИНОРГАНИЧЕСКАЯ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ПО СТАРТИЧЕСКОЙ ФОРМЕ, 2018-2032 (USD THOUSAND)

СТАТЬЯ 74 МЕЖДУНАРОДНЫЙ ВОСТОК И АФРИКА ИНОРГАНИЧЕСКИЙ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, СТАТЬЯ, 2018-2032 (ТОНС)

СТАТЬЯ 75 МИДЛЯ ВОСТОК И АФРИКА ОРГАНИЧЕСКИЙ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 76 ВОСТОК И АФРИКА ОРГАНИЧЕСКИЙ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (ТОНС)

Таблица 77 Средний Восток и АФРИКА АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ, ТАРГЕТ ПОЛИМЕР, 2018-2032 (USD THOUSAND)

Таблица 78 ВОСТОК И АФРИКА АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ, ТАРГЕТ ПОЛИМЕР, 2018-2032 (ТОНС)

Таблица 79 Средний Восток и Африка Полиэтилен (PE) В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ТАРГЕТ ПОЛИМЕР, 2018-2032 (USD THOUSAND)

Таблица 80 Средний Восток и Африка Полиэтилен (ПЭ) В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ТАРГЕТ ПОЛИМЕР, 2018-2032 (ТОНС)

СТАТЬЯ 81 ВОСТОК И АФРИКА АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ, К концу использования промышленности, 2018-2032 (USD THOUSAND)

СТАТЬЯ 82 ВОСТОК И АФРИКА АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ, К концу использования промышленности, 2018-2032 (ТОНС)

СТАТЬЯ 83 МИДЛЯ ВОСТОК И АФРИКА ПАКАКУЮТСЯ В АНТИБЛОКСКОМ АДДИТИВНОМ МАРКЕТЕ, КИТАЙ, 2018-2032 (USD THOUSAND)

СТАТЬЯ 84 МЕЖДУНАРОДНЫЙ ВОСТОК И АФРИКА ПАКАКУЮТСЯ В АНТИБЛОКСКОМ АДДИТИВНОМ МАРКЕТЕ, ВЫБОР, 2018-2032 (ТОНС)

СТАТЬЯ 85 МЕДЛЯ ВОСТОК И АФРИКА ПАКАКУЕТ В АНТИБЛОКСКОМ ДОПОЛНИТЕЛЬНОМ МАРКЕ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 86 МИДЛЯ ВОСТОК И АФРИКА ПАКАКУЮТСЯ В АНТИБЛОКСКОМ АДДИТИВНОМ МАРКЕ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 87 ПОСЛЕДНИЙ И АФРИКАНСКИЙ ИНДУСТРИАЛ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ВЫБОР, 2018-2032 (USD THOUSAND)

СТАТЬЯ 88 МЕЖДУНАРОДНЫЙ ВОСТОК И АФРИКАНСКИЙ ИНДУСТРИАЛ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ВЫБОР, 2018-2032 (ТОНС)

СТАТЬЯ 89 МИДЛЯ ВОСТОК И АФРИКА ИНДУСТРИАЛ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 90 МЕЖДУНАРОДНЫЙ ВОСТОК И АФРИКАНСКИЙ ИНДУСТРИАЛ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 91 МЕДЛЯ И АФРИКА АГРИКУЛЬТУРА В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 92 МЕЖДУНАРОДНЫЙ ВОСТОК И АФРИКА АГРИКУЛЬТУРА В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 93 МИДЛЯ ВОСТОК И АФРИКА МЕДИЦИНСКАЯ И ЗДОРОВЬЯ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 94 МЕДЛЯ ВОСТОК И АФРИКА МЕДИЦИНСКАЯ И ЗДОРОВЬЯ В АНТИБЛОКСКОМ АДДИТИВНОМ МАРКЕ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 95 МИДЛЯ ВОСТОК И АФРИКА ЭЛЕКТРОНИКА И СОЛАР В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ТИП, 2018-2032 (USD THOUSAND)

СТАТЬЯ 96 МИДЛЯ ВОСТОК И АФРИКА ЭЛЕКТРОНИКИ И СОЛАР В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, В ТИПЕ, 2018-2032 (ТОНС)

СТАТЬЯ 97 МЕДЛЯ И АФРИКА ЭЛЕКТРОНИКА И СОЛАР В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 98 МИДЛЯ ВОСТОК И АФРИКА ЭЛЕКТРОНИКА И СОЛАР В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 99 МИДЛЯ ВОСТОК И АФРИКА ПРИНТИРОВАНИЕ И ОФТИКА В АНТИБЛОКНОМ АДДИТИВНОМ МАРКЕ, ВЫБОР, 2018-2032 (USD THOUSAND)

СТАТЬЯ 100 МИДЛЯ ВОСТОК И АФРИКА ПРИНТИРОВАНИЕ И ОФТИКА В АНТИБЛОКНОМ АДДИТИВНОМ МАРКЕТЕ, ВЫБОР, 2018-2032 (ТОНС)

СТАТЬЯ 101 СРЕДСТВО И ПРИНИМАНИЕ АФРИКИ И ОФТИКА В АНТИБЛОКНОМ АДДИТИВНОМ МАРКЕ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 102 СРЕДСТВО И ПРИНИМАНИЕ АФРИКИ И ОФТИКА В АНТИБЛОКНОМ АДДИТИВНОМ МАРКЕ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 103 ПОСЛЕДНИЕ И АФРИКА ДРУГИЕ В АНТИБЛОКНОМ АДДИТИВНОМ МАРКЕ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 104 СРЕДСТВО И АФРИКА ДРУГИЕ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (ТОНС)

Таблица 105 SAUDI ARABIA ANTIBLOCK ADDITIVE MARKET, ФОРМА, 2018-2032 (USD THOUSAND)

Таблица 106 SAUDI ARABIA ANTIBLOCK ADDITIVE MARKET, ФОРМА, 2018-2032 (ТОНС)

Таблица 107 SAUDI ARABIA INORGANIC IN ANTIBLOCK ADDITIVE MARKET, BYPE, 2018-2032 (USD THOUSAND)

Таблица 108 SAUDI ARABIA INORGANIC IN ANTIBLOCK ADDITIVE MARKET, BYPE, 2018-2032

СТАТЬЯ 109 SAUDI ARABIA INORGANIC IN ANTIBLOCK ADDITIVE MARKET, BY PARTICLE SHAPE, 2018-2032 (USD THOUSAND)

СТАТЬЯ 110 SAUDI ARABIA INORGANIC IN ANTIBLOCK ADDITIVE MARKET, BY PARTICLE SHAPE, 2018-2032 (TONS)

СТАТЬЯ 111 SAUDI ARABIA ORGANIC IN ANTIBLOCK ADDITIVE MARKET, BY FORM, 2018-2032 (USD THOUSAND)

СТАТЬЯ 112 SAUDI ARABIA ORGANIC IN ANTIBLOCK ADDITIVE MARKET, BY FORM, 2018-2032

Таблица 113 САУДИ АРАБИЯ АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ, ПОЛИМЕР ТАРГЕТА, 2018-2032 (USD THOUSAND)

Таблица 114 SAUDI ARABIA ANTIBLOCK ADDITIVE MARKET, BY TARGET POLYMER, 2018-2032

Таблица 115 SAUDI ARABIA POLYETHYLENE (PE) IN ANTIBLOCK ADDITIVE MARKET, BY TARGET POLYMER, 2018-2032 (USD THOUSAND)

Таблица 116 SAUDI ARABIA POLYETHYLENE (PE) IN ANTIBLOCK ADDITIVE MARKET, BY TARGET POLYMER, 2018-2032 (TONS)

СТАТЬЯ 117 САУДИ АРАБИЯ АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ, К концу использования промышленности, 2018-2032 (USD THOUSAND)

СТАТЬЯ 118 САУДИ АРАБИЯ АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ, К концу использования промышленности, 2018-2032 (ТОНС)

Таблица 119 SAUDI ARABIA PACKAGING IN ANTIBLOCK ADDITIVE MARKET, BYPE, 2018-2032 (USD THOUSAND)

Таблица 120 SAUDI ARABIA PACKAGING IN ANTIBLOCK ADDITIVE MARKET, BYPE, 2018-2032

СТАТЬЯ 121 SAUDI ARABIA PACKAGING IN ANTIBLOCK ADDITIVE MARKET, BY FORM, 2018-2032 (USD THOUSAND)

СТАТЬЯ 122 САУДИ АРАБИЯ ПАКАКУЕТ В АНТИБЛОКСКОМ АДДИТИВНОМ МАРКЕ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 123 SAUDI ARABIA INDUSTRIAL IN ANTIBLOCK ADDITIVE MARKET, BYPE, 2018-2032 (USD THOUSAND)

Таблица 124 SAUDI ARABIA INDUSTRIAL IN ANTIBLOCK ADDITIVE MARKET, BYPE, 2018-2032

Таблица 125 SAUDI ARABIA INDUSTRIAL IN ANTIBLOCK ADDITIVE MARKET, BY FORM, 2018-2032 (USD THOUSAND)

СТАТЬЯ 126 SAUDI ARABIA INDUSTRIAL IN ANTIBLOCK ADDITIVE MARKET, BY FORM, 2018-2032 (TONS)

СТАТЬЯ 127 SAUDI ARABIA AGRICULTURE IN ANTIBLOCK ADDITIVE MARKET, BY FORM, 2018-2032

СТАТЬЯ 128 SAUDI ARABIA AGRICULTURE IN ANTIBLOCK ADDITIVE MARKET, BY FORM, 2018-2032

Таблица 129 SAUDI ARABIA MEDICAL AND HEALTHCARE IN ANTIBLOCK ADDITIVE MARKET, BY FORM, 2018-2032 (USD THOUSAND)

Таблица 130 SAUDI ARABIA MEDICAL AND HEALTHCARE IN ANTIBLOCK ADDITIVE MARKET, BY FORM, 2018-2032

СТАТЬЯ 131 SAUDI ARABIA ELECTRONICS AND SOLAR IN ANTIBLOCK ADDITIVE MARKET, BYPE, 2018-2032 (USD THOUSAND)

СТАТЬЯ 132 SAUDI ARABIA ELECTRONICS AND SOLAR IN ANTIBLOCK ADDITIVE MARKET, BYPE, 2018-2032 (TONS)

Таблица 133 SAUDI ARABIA ELECTRONICS AND SOLAR IN ANTIBLOCK ADDITIVE MARKET, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 134 SAUDI ARABIA ELECTRONICS AND SOLAR IN ANTIBLOCK ADDITIVE MARKET, BY FORM, 2018-2032 (TONS)

СТАТЬЯ 135 САУДИ АРАБИЯ ПРИНИМАНИЕ И ОПТИКА В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, КИТАЙ, 2018-2032 (USD THOUSAND)

СТАТЬЯ 136 САУДИ АРАБИЯ ПРИНТИНГ И ОФТИКА В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, КИТАЙ, 2018-2032 (ТОНС)

СТАТЬЯ 137 САУДИ АРАБИЯ ПРИНИМАНИЕ И ОФТИКА В АНТИБЛОКСКОМ АДДИТИВНОМ МАРКЕ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 138 САУДИ АРАБИЯ ПРИНИМАНИЕ И ОФТИКА В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 139 САУДИ АРАБИЯ ДРУГИЕ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (USD THOUSAND)

Таблица 140 SAUDI ARABIA OTHERS IN ANTIBLOCK ADDITIVE MARKET, BY FORM, 2018-2032

СТАТЬЯ 141 АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 142 АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (ТОНС)

143 U.A.E INORGANIC IN ANTIBLOCK ADDITIVE MARKET, BYPE, 2018-2032 (USD THOUSAND)

СТАТЬЯ 144 ИНОРГАНИЧЕСКАЯ В АНТИБЛОКЕ АДДИТИВНАЯ МАРКЕТКА, ВЫБОР, 2018-2032 (ТОНС)

145 U.A.E INORGANIC IN ANTIBLOCK ADDITIVE MARKET, BY PARTICLE SHAPE, 2018-2032 (USD THOUSAND)

СТАТЬЯ 146 МЕЖДУНАРОДНЫЙ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ПО СТАРТИЧЕСКОЙ ФОРМЕ, 2018-2032 (ТОНС)

147 U.A.E. ORGANIC IN ANTIBLOCK ADDITIVE MARKET, BY FORM, 2018-2032 (USD THOUSAND)

СТАТЬЯ 148 У.А.Е. ОРГАНИЧЕСКИЙ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 149 АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ, ТАРГЕТ ПОЛИМЕР, 2018-2032 (USD THOUSAND)

СТАТЬЯ 150 АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ, ПОЛИМЕР ТАРГЕТА, 2018-2032 (ТОНС)

Таблица 151 U.A.E. POLYETHYLENE (PE) IN ANTIBLOCK ADDITIVE MARKET, BY TARGET POLYMER, 2018-2032 (USD THOUSAND)

Таблица 152 U.A.E. POLYETHYLENE (PE) IN ANTIBLOCK ADDITIVE MARKET, BY TARGET POLYMER, 2018-2032 (TONS)

СТАТЬЯ 153 АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ, К концу использования промышленности, 2018-2032 (USD THOUSAND)

СТАТЬЯ 154 АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ, К концу использования промышленности, 2018-2032 (ТОНС)

Таблица 155 U.A.E. PACKAGING IN ANTIBLOCK ADDITIVE MARKET, BYPE, 2018-2032 (USD THOUSAND)

Таблица 156 U.A.E. PACKAGING IN ANTIBLOCK ADDITIVE MARKET, BYPE, 2018-2032

157 U.A.E. PACKAGING IN ANTIBLOCK ADDITIVE MARKET, BY FORM, 2018-2032 (USD THOUSAND)

Таблица 158 U.A.E. PACKAGING IN ANTIBLOCK ADDITIVE MARKET, BY FORM, 2018-2032

СТАТЬЯ 159 ПРОМЫШЛЕННЫЙ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, В ТИПЕ, 2018-2032 (USD THOUSAND)

СТАТЬЯ 160 ИНДУСТРИАЛЬНЫЙ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, В ТИПЕ, 2018-2032 (ТОНС)

СТАТЬЯ 161 ПРОМЫШЛЕННЫЙ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 162 ПРОМЫШЛЕННЫЙ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 163 АГРИКУЛЬТУРА У.А.Е. В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 164 АГРИКУЛЬТУРА У.А.Е. В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 165 U.A.E. MEDICAL AND HEALTHCARE IN ANTIBLOCK ADDITIVE MARKET, BY FORM, 2018-2032

СТАТЬЯ 166 U.A.E. MEDICAL AND HEALTHCARE IN ANTIBLOCK ADDITIVE MARKET, BY FORM, 2018-2032 (TONS)

Таблица 167 U.A.E. ELECTRONICS AND SOLAR IN ANTIBLOCK ADDITIVE MARKET, BYPE, 2018-2032 (USD THOUSAND)

СТАТЬЯ 168 ЕЛЕКТРОНИКА И СОЛАР В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, В ТИПЕ, 2018-2032 (ТОНС)

СТАТЬЯ 169 ЕЛЕКТРОНИКА И СОЛАР В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (USD THOUSAND)

Таблица 170 ЕЛЕКТРОНИКА И СОЛАР В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 171 U.A.E. ПРИНИМАНИЕ И ОФТИКА В АНТИБЛОКНОМ АДДИТИВНОМ МАРКЕ, КИТАЙ, 2018-2032 (USD THOUSAND)

СТАТЬЯ 172 U.A.E. ПРИНИМАНИЕ И ОПТИКА В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ВЫБОР, 2018-2032 (ТОНС)

СТАТЬЯ 173 U.A.E. ПРИНИМАНИЕ И ОФТИКА В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 174 U.A.E. ПРИНИМАНИЕ И ОФТИКА В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 175 ДРУГИЕ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 176 ДРУГИЕ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 177 АФРИКА АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 178 АФРИКА АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 179 ЮЖНАЯ АФРИКА ИНОРГАНИЧЕСКАЯ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, В ТИПЕ, 2018-2032 (USD THOUSAND)

СТАТЬЯ 180 ЮЖНАЯ АФРИКА ИНОРГАНИЧЕСКАЯ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, В ТИПЕ, 2018-2032 (ТОНС)

СТАТЬЯ 181 ЮЖНАЯ АФРИКА ИНОРГАНИЧЕСКАЯ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ПО СТАТЬИ, 2018-2032 (USD THOUSAND)

СТАТЬЯ 182 ЮЖНАЯ АФРИКА ИНОРГАНИЧЕСКАЯ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, СТАТЬЯ ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 183 ЮЖНАЯ АФРИКА ОРГАНИЧЕСКАЯ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 184 ЮЖНАЯ АФРИКА ОРГАНИЧЕСКАЯ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 185 АФРИКА АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ, ПОЛИМЕР ТАРГЕТА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 186 АФРИКА АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ, ПОЛИМЕР ТАРГЕТА, 2018-2032 (ТОНС)

СТАТЬЯ 187 ПОЛИТИЛЕНА ЮЖНОЙ АФРИКИ (ПЭ) В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ПОЛИМЕР ТАРГЕТ, 2018-2032 (USD THOUSAND)

СТАТЬЯ 188 ПОЛИТИЛЕНА ЮЖНОЙ АФРИКИ (ПЭ) В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ПОЛИМЕР ТАРГЕТ, 2018-2032 (ТОНС)

СТАТЬЯ 189 ЮАР АФРИКА АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ, К концу использования промышленности, 2018-2032 (USD THOUSAND)

СТАТЬЯ 190 ЮАР АФРИКА АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ, К концу использования промышленности, 2018-2032 (ТОНС)

Таблица 191 Южная Африка, ПАККУЮЩАЯ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ТИП, 2018-2032 (USD THOUSAND)

СТАТЬЯ 192 Южная Африка, ПАКАЮЩАЯ В АНТИБЛОКСКИЙ АДДИТИВНЫЙ МАРКЕТ, ТИП, 2018-2032 (ТОНС)

СТАТЬЯ 193 ЮЖНАЯ АФРИКА ПАКАКУЕТСЯ В АНТИБЛОКСКОМ АДДИТИВНОМ МАРКЕ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 194 Южная Африка ПАКАКУЕТСЯ В АНТИБЛОКСКОМ АДДИТИВНОМ МАРКЕ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 195 ЮЖНО-АФРИКАНСКИЙ ИНДУСТРИАЛ В АНТИБЛОКСКОМ АДДИТИВНОМ МАРКЕТЕ, ТИП, 2018-2032 (USD THOUSAND)

СТАТЬЯ 196 ЮЖНО-АФРИКАНСКИЙ ИНДУСТРИАЛ В АНТИБЛОКСКОМ АДДИТИВНОМ МАРКЕТЕ, КИТАЙ, 2018-2032 (ТОНС)

СТАТЬЯ 197 ЮЖНО-АФРИКАНСКИЙ ИНДУСТРИАЛ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 198 ЮЖНО-АФРИКАНСКИЙ ИНДУСТРИАЛ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 199 АГРИКУЛЬТУРА ЮЖНОЙ АФРИКИ В АНТИБЛОКНОМ АДДИТИВНОМ МАРКЕ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 200 АГРИКУЛЬТУРА ЮЖНОЙ АФРИКИ В АНТИБЛОКНОМ АДДИТИВНОМ МАРКЕ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 201 ЮЖНАЯ АФРИКА МЕДИЦИНСКАЯ И ЗДОРОВЬЯ В АНТИБЛОКСКОЙ АДДИТИВНОЙ МАРКЕ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 202 ЮЖНАЯ АФРИКА МЕДИЦИНСКАЯ И ЗДОРОВЬЯ В АНТИБЛОКСКОЙ АДДИТИВНОЙ МАРКЕ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 203 ЮЖНАЯ АФРИКА ЭЛЕКТРОНИКА И СОЛАР В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, КИТАЙ, 2018-2032 (USD THOUSAND)

СТАТЬЯ 204 ЮЖНАЯ АФРИКА ЭЛЕКТРОНИКА И СОЛАР В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, КИТАЙ, 2018-2032 (ТОНС)

СТАТЬЯ 205 ЮЖНАЯ АФРИКА ЭЛЕКТРОНИКА И СОЛАР В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 206 ЮЖНАЯ АФРИКА ЭЛЕКТРОНИКА И СОЛАР В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 207 ПРИНИМАНИЕ И ОПТИКА ЮЖНОЙ АФРИКИ В АНТИБЛОКНОМ АДДИТИВНОМ МАРКЕТЕ, КИТАЙ, 2018-2032 (USD THOUSAND)

СТАТЬЯ 208 ПРИНИМАНИЕ И ОФТИКА ЮЖНОЙ АФРИКИ В АНТИБЛОКНОМ АДДИТИВНОМ МАРКЕТЕ, КИТАЙ, 2018-2032 (ТОНС)

СТАТЬЯ 209 ПРИНИМАНИЕ И ОПТИКА ЮЖНОЙ АФРИКИ В АНТИБЛОКНОМ АДДИТИВНОМ МАРКЕ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 210 ПРИНИМАНИЕ И ОФТИКА ЮЖНОЙ АФРИКИ В АНТИБЛОКНОМ АДДИТИВНОМ МАРКЕ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 211 ЮЖНАЯ АФРИКА ДРУГИЕ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 212 ЮЖНАЯ АФРИКА ДРУГИЕ В АНТИБЛОКНОМ АДДИТИВНОМ МАРКЕ, ФОРМА, 2018-2032 (ТОНС)

Таблица 213 ЭГИПТ АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (USD THOUSAND)

Таблица 214 ЭГИПТ АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 215 ЭГИПТИЧЕСКАЯ ИНОРГАНИЧЕСКАЯ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ВЫБОР, 2018-2032 (USD THOUSAND)

СТАТЬЯ 216 ЭГИПТ ИНОРГАНИЧЕСКИЙ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, В ТИПЕ, 2018-2032 (ТОНС)

СТАТЬЯ 217 ЭГИПТ ИНОРГАНИЧЕСКИЙ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ПО СТАТЬИ, 2018-2032 (USD THOUSAND)

СТАТЬЯ 218 ЭГИПТИЧЕСКАЯ ИНОРГАНИЧЕСКАЯ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ПО СТАРТИЧЕСКОЙ ФОРМЕ, 2018-2032 (ТОНС)

СТАТЬЯ 219 ЕГИПТОВЫЙ ОРГАНИЧЕСКИЙ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 220 ЭГИПТ ОРГАНИЧЕСКИЙ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 221 ЭГИПТ АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ, ПОЛИМЕР ТАРГЕТА, 2018-2032 (USD THOUSAND)

Таблица 222 ЭГИПТ АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ, ТАРГЕТ ПОЛИМЕР, 2018-2032 (ТОНС)

Таблица 223 ЭГИПТ ПОЛИЭТИЛЕН (ПЭ) В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ТАРГЕТ ПОЛИМЕР, 2018-2032 (USD THOUSAND)

Таблица 224 ЭГИПТ ПОЛИЭТИЛЕН (ПЭ) В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ТАРГЕТ ПОЛИМЕР, 2018-2032 (ТОНС)

СТАТЬЯ 225 ЭГИПТ АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ, К концу использования промышленности, 2018-2032 (USD THOUSAND)

Таблица 226 ЭГИПТ АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ, К концу использования Индустрии, 2018-2032 (ТОНС)

СТАТЬЯ 227 ЕГИПТ ПАККУЮЩИЙ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, В ТИПЕ, 2018-2032 (USD THOUSAND)

СТАТЬЯ 228 ЕГИПТЫ, ПУТИВЫЕ В АНТИБЛОКСКОМ АДДИТИВНОМ МАРКЕТЕ, В ТИПЕ, 2018-2032 (ТОНС)

СТАТЬЯ 229 ЕГИПТОВЫЙ ПАКТАЖ В АНТИБЛОКСКОМ АДДИТИВНОМ МАРКЕ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 230 ЕГИПТ ПАКАГИРОВАНИЯ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 231 ЭГИПТИЧЕСКИЙ ИНДУСТРИАЛ В АНТИБЛОКСКОМ АДДИТИВНОМ МАРКЕ, В ТИПЕ, 2018-2032 (USD THOUSAND)

СТАТЬЯ 232 ЭГИПТИЧЕСКИЙ ИНДУСТРИАЛ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, В ТИПЕ, 2018-2032 (ТОНС)

СТАТЬЯ 233 ЭГИПТНЫЙ ИНДУСТРИАЛ В АНТИБЛОКСКОМ АДДИТИВНОМ МАРКЕ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 234 ЭГИПТНЫЙ ИНДУСТРИАЛ В АНТИБЛОКСКОМ АДДИТИВНОМ МАРКЕ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 235 ЭГИПТНАЯ АГРИКУЛЬТУРА В АНТИБЛОКНОМ АДДИТИВНОМ МАРКЕ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 236 ЭГИПТНАЯ АГРИКУЛЬТУРА В АНТИБЛОКНОМ АДДИТИВНОМ МАРКЕ, ФОРМА, 2018-2032 (ТОНС)

Таблица 237 ЭГИПТ МЕДИЦИНСКАЯ И ЗДОРОВЬЯ В АНТИБЛОКСКОМ АДДИТИВНОМ МАРКЕ, ФОРМА, 2018-2032 (USD THOUSAND)

Таблица 238 ЭГИПТ МЕДИЦИНСКАЯ И ЗДОРОВЬЯ В АНТИБЛОКСКОМ АДДИТИВНОМ МАРКЕ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 239 ЭГИПТ ЭЛЕКТРОНИКА И СОЛАР В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, В ТИПЕ, 2018-2032 (USD THOUSAND)

СТАТЬЯ 240 ЭГИПТ ЭЛЕКТРОНИКА И СОЛАР В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, В ТИПЕ, 2018-2032 (ТОНС)

СТАТЬЯ 241 ЭГИПТ ЭЛЕКТРОНИКА И СОЛАР В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 242 ЭГИПТ ЭЛЕКТРОНИКА И СОЛАР В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 243 ЕГИПТ ПРИНИМАНИЕ И ОПТИКА В АНТИБЛОКНОМ АДДИТИВНОМ МАРКЕ, В ТИПЕ, 2018-2032 (USD THOUSAND)

СТАТЬЯ 244 ЕГИПТ ПРИНИМАНИЕ И ОФТИКА В АНТИБЛОКНОМ АДДИТИВНОМ МАРКЕТЕ, В ТИПЕ, 2018-2032 (ТОНС)

СТАТЬЯ 245 ЕГИПТ ПРИНИМАНИЕ И ОФТИКА В АНТИБЛОКНОМ АДДИТИВНОМ МАРКЕ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 246 ЕГИПТ ПРИНИМАНИЕ И ОФТИКА В АНТИБЛОКНОМ АДДИТИВНОМ МАРКЕ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 247 ЭГИПТ ДРУГИХ В АНТИБЛОКНОМ АДДИТИВНОМ МАРКЕ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 248 ЕГИПТ ДРУГИХ В АНТИБЛОКНОМ АДДИТИВНОМ МАРКЕ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 249 ИЗРАИЛЬСКИЙ АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 250 ИЗРАИЛЬСКИЙ АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 251 ИЗРАИЛЬСКАЯ ИНОРГАНИЧЕСКАЯ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ВЫБОР, 2018-2032 (USD THOUSAND)

СТАТЬЯ 252 ИЗРАИЛЬСКИЙ ИНОРГАНИЧЕСКИЙ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, В ТИПЕ, 2018-2032 (ТОНС)

СТАТЬЯ 253 ИЗРАИЛЬСКАЯ ИНОРГАНИЧЕСКАЯ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ПО СТАРТИЧЕСКОЙ ФОРМЕ, 2018-2032 (USD THOUSAND)

СТАТЬЯ 254 ИЗРАИЛЬСКАЯ ИНОНОРГАНИЧЕСКАЯ В АНТИБЛОКСКОМ АДДИТИВНОМ МАРКЕТЕ, СТАТЬЯ, 2018-2032 (ТОНС)

СТАТЬЯ 255 ИЗРАИЛЬСКИЙ ОРГАНИЧЕСКИЙ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 256 ИЗРАИЛЬСКАЯ ОРГАНИЧЕСКАЯ В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 257 ИЗРАИЛЬСКИЙ АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ, ПОЛИМЕР ТАРГЕТА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 258 ИЗРАИЛЬСКИЙ АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ, ПОЛИМЕР ТАРГЕТА, 2018-2032 (ТОНС)

СТАТЬЯ 259 ИЗРАИЛЬСКАЯ ПОЛИТЕТИЛЕНА (ПЭ) В АНТИБЛОКСКОМ АДДИТИВНОМ МАРКЕ, ПОЛИМЕР ТАРГЕТ, 2018-2032 (USD THOUSAND)

СТАТЬЯ 260 ИЗРАИЛЬСКАЯ ПОЛИТЕТИЛЕНА (ПЭ) В АНТИБЛОКСКОМ АДДИТИВНОМ МАРКЕ, ПОЛИМЕР ТАРГЕТ, 2018-2032 (ТОНС)

СТАТЬЯ 261 ИЗРАИЛЬСКИЙ АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ, К концу использования Индустрии, 2018-2032 (USD THOUSAND)

СТАТЬЯ 262 ИЗРАИЛЬСКИЙ АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ, К концу использования Индустрии, 2018-2032 (ТОНС)

СТАТЬЯ 263 ИЗРАИЛЬСКИЙ ПАККАГ В АНТИБЛОКСКОМ АДДИТИВНОМ МАРКЕТЕ, ВЫБОР, 2018-2032 (USD THOUSAND)

СТАТЬЯ 264 ИЗРАИЛЬСКИЙ ПАКАГ В АНТИБЛОКСКОМ АДДИТИВНОМ МАРКЕТЕ, ВЫБОР, 2018-2032 (ТОНС)

СТАТЬЯ 265 ИЗРАИЛЬСКИЙ ПАКАГ В АНТИБЛОКСКОМ АДДИТИВНОМ МАРКЕ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 266 ИЗРАИЛЬ ПАККИНГ В АНТИБЛОКСКОМ АДДИТИВНОМ МАРКЕ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 267 ИСРАИЛЬСКИЙ ИНДУСТРИАЛ В АНТИБЛОКСКОМ АДДИТИВНОМ МАРКЕТЕ, ВЫБОР, 2018-2032 (USD THOUSAND)

СТАТЬЯ 268 ИСРАИЛЬСКИЙ ИНДУСТРИАЛ В АНТИБЛОКСКОМ АДДИТИВНОМ МАРКЕТЕ, ВЫБОР, 2018-2032 (ТОНС)

СТАТЬЯ 269 ИСРАИЛЬСКИЙ ИНДУСТРИАЛ В АНТИБЛОКСКОМ АДДИТИВНОМ МАРКЕ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 270 ИСРАИЛЬСКИЙ ИНДУСТРИАЛ В АНТИБЛОКСКОМ АДДИТИВНОМ МАРКЕ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 271 ИСРАЕЛЬСКАЯ АГРИКУЛЬТУРА В АНТИБЛОКСКОМ АДДИТИВНОМ МАРКЕ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 272 ИСРАЕЛЬСКАЯ АГРИКУЛЬТУРА В АНТИБЛОКНОМ АДДИТИВНОМ МАРКЕ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 273 ИСРАИЛЬСКАЯ МЕДИЦИНСКАЯ И ЗДОРОВЬЯ В АНТИБЛОКСКОЙ АДДИТИВНОЙ МАРКЕТ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 274 ИСРАИЛЬСКАЯ МЕДИЦИНСКАЯ И ЗДОРОВЬЯ В АНТИБЛОКСКОМ АДДИТИВНОМ МАРКЕ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 275 ИСРАЕЛЬСКАЯ ЭЛЕКТРОНИКА И СОЛАР В АНТИБЛОКСКОМ АДДИТИВНОМ МАРКЕТЕ, КИТАЙ, 2018-2032 (USD THOUSAND)

СТАТЬЯ 276 ИСРАЕЛЬСКАЯ ЭЛЕКТРОНИКА И СОЛАР В АНТИБЛОКСКОМ АДДИТИВНОМ МАРКЕТЕ, КИТАЙ, 2018-2032 (ТОНС)

СТАТЬЯ 277 ИСРАЕЛЬСКАЯ ЭЛЕКТРОНИКА И СОЛАР В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 278 ИСРАЕЛЬСКАЯ ЭЛЕКТРОНИКА И СОЛАР В АНТИБЛОКЕ АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 279 ИЗРАИЛЬСКОЕ ПРИНИМАНИЕ И ОФТИКА В АНТИБЛОКНОМ АДДИТИВНОМ МАРКЕ, ВЫБОР, 2018-2032 (USD THOUSAND)

СТАТЬЯ 280 ИЗРАИЛЬСКОЕ ПРИНИМАНИЕ И ОФТИКА В АНТИБЛОКНОМ АДДИТИВНОМ МАРКЕТЕ, ВЫБОР, 2018-2032 (ТОНС)

СТАТЬЯ 281 ИЗРАИЛЬСКОЕ ПРИНИМАНИЕ И ОФТИКА В АНТИБЛОКНОМ АДДИТИВНОМ МАРКЕ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 282 ИЗРАИЛЬСКОЕ ПРИНИМАНИЕ И ОФТИКА В АНТИБЛОКНОМ АДДИТИВНОМ МАРКЕ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 283 ИЗРАИЛЬСКИЕ ДРУГИЕ В АНТИБЛОКНОМ АДДИТИВНОМ МАРКЕ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 284 ИЗРАИЛЬСКИЕ ДРУГИЕ В АНТИБЛОКНОМ АДДИТИВНОМ МАРКЕ, ФОРМА, 2018-2032 (ТОНС)

СТАТЬЯ 285 ПЕРЕДАЧА ВОСТОКА СРЕДСТВА И АФРИКА АНТИБЛОКА АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (USD THOUSAND)

СТАТЬЯ 286 ПОСТАНОВЛЕНИЕ ВОСТОКА СРЕДСТВА И АФРИКА АНТИБЛОКА АДДИТИВНЫЙ МАРКЕТ, ФОРМА, 2018-2032 (ТОНС)

Список рисунков

ФИГРАЛЬ 1 МЕДЛЯ И АФРИКА АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ

ФИГРА 2 СРЕДСТВО И АФРИКА АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ: ТРИАНГУЛЯЦИЯ ДАННЫХ

ФИГРА 3 СРЕДСТВО И АФРИКА АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ: ДРОК АНАЛИЗИС

ФИГРА 4 СРЕДСТВО И АФРИКА АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ: РЕГИОНАЛЬНЫЙ МАРКЕТ АНАЛИЗ

ФИГРА 5 СРЕДСТВО И АФРИКА АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ: КОМПАНИЯ ИССЛЕДОВАНИЕ АНАЛИЗА

ФИГРА 6 СРЕДСТВО И АФРИКА АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ: МУЛЬТИВАРИАТНЫЙ МОДЕЛЛИНГ

ФИГРА 7 МЕДЛЯ И АФРИКА АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ: МЕЖДУНАРОДНАЯ ДЕМОГРАФИКА

ФИГРАЛЬ 8 СРЕДСТВО И АФРИКА АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ: DBMR МАРКЕТ ПОСИЦИОННЫЙ ГРИД

ФИГРА 9 МЕДЛЯ И АФРИКА АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ: ВЕНДОР ШАРЕ АНАЛИЗИС

ФИГРА 10 МИДЛЯ ВОСТОК И АФРИКА АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ: СЕГМЕНТАЦИЯ

ФИГРА 11 ДВА СЕГМЕНТА КОМПРИЗАЦИИ Средний Восток и АФРИКА АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ, ФОРМА (2024)

ФИГРАЛЬ 12 МИДЛЯ ВОСТОК И АФРИКА АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ: ИСПОЛНИТЕЛЬНАЯ РЕЗЮМЕ

ФИГРА 13 МЕДЛЯ И АФРИКА АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ: СТРАТЕГИЧЕСКИЕ РЕШЕНИЯ

ФИГРА 14 Растущее требование к ПЛАСТИЧЕСКОЙ ПАКТИЧЕСКОЙ СЕРДЦЕ И АФРИКА ОЖИДАЕТСЯ ДВИГАТЬ СЕРДЦЕ И АФРИКА АНТИБЛОКОВАННЫЙ МАРКЕТ В ПЕРИОДЕ ФОРЕКАСТА (2025-2032)

ФИГРА 15 ИНОРСКОЕ ОБЪЯВЛЕНИЕ ОЖИДАЕТСЯ ПОСТАНОВЛЯТЬ НАСТОЯЩЕЕ РАЗВИТИЕ СРЕДСТВА И АФРИКАНСКОЙ АНТИБЛОКНОЙ АДДИТИВНОЙ МАРКЕТ В 2025 И 2032 годах

ФИГРА 16 ПЕСТЕЛЬНЫЙ АНАЛИЗ

Рисунок 17 Пять сил Портера Аналитика

Рисунок 18 Критерии выбора вендора

Рисунок 19 Водители, УВЕДОМЛЕНИЯ, ПОСЛЕДОВАТЕЛЬСТВА И ЗАЯВЛЕНИЯ НА Средний Восток И АФРИКА АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ

ФИГРА 20 СРЕДСТВО И АФРИКА АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ: ФОРМА, 2024

ФИГРА 21 МИДЛЯ И АФРИКА АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ: ТАРГЕТ ПОЛИМЕР, 2024

ФИГРА 22 СРЕДСТВО И АФРИКА АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ: К концу использования промышленности, 2024

ФИГРАЛЬ 23 СРЕДСТВО И АФРИКА АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ: СНАПШОТ (2024)

ФИГРА 24 МИДЛЯ ВОСТОК И АФРИКА АНТИБЛОК АДДИТИВНЫЙ МАРКЕТ: КОМПАНИЯ ДЛЯ 2024 (%)

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.