North America Inflation Device Market

Размер рынка в млрд долларов США

CAGR :

%

USD

353.62 Million

USD

524.79 Million

2025

2033

USD

353.62 Million

USD

524.79 Million

2025

2033

| 2026 –2033 | |

| USD 353.62 Million | |

| USD 524.79 Million | |

| % | |

|

Сегментация рынка устройств для накачивания баллонов в Северной Америке по типу (аналоговые и цифровые устройства), объему (20 мл, 25 мл, 30 мл и 60 мл), применению (интервенционная кардиология, периферические сосудистые процедуры, интервенционная радиология, урологические процедуры, гастроэнтерологические процедуры и другие), давлению (30 атм, 40 атм, 55 атм и другие), функциям (установка стента и подача жидкости), конечным пользователям (больницы, интервенционные лаборатории и клиники), каналам сбыта (прямые закупки, розничные продажи и сторонние дистрибьюторы) — тенденции отрасли и прогноз до 2033 года.

Размер рынка устройств для искусственного нагнетания воздуха в Северной Америке

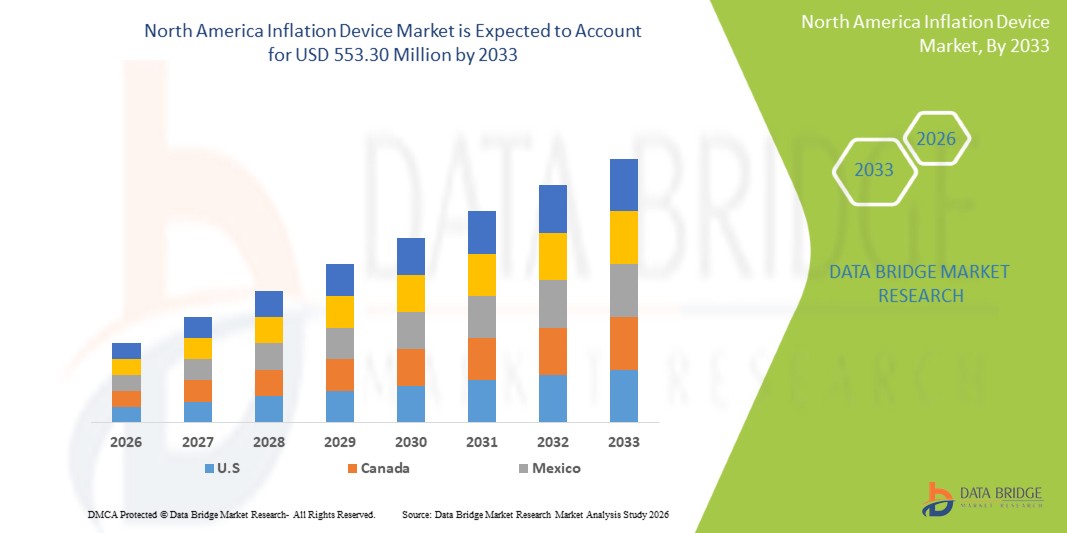

- Объем рынка устройств для искусственного надувания в Северной Америке в 2025 году оценивался в 371,65 млн долларов США и, как ожидается, достигнет 553,30 млн долларов США к 2033 году , демонстрируя среднегодовой темп роста в 5,10% в течение прогнозируемого периода.

- Расширение рынка обусловлено прежде всего увеличением объема интервенционных кардиологических и радиологических процедур, где устройства для надувания баллонов необходимы для точного контроля давления в баллонных катетерах как в больницах, так и в амбулаторных хирургических центрах.

- Кроме того, регион выигрывает от развитой инфраструктуры здравоохранения, широкого внедрения малоинвазивных хирургических вмешательств и постоянного совершенствования медицинских устройств, что ускоряет спрос на продукцию.

Анализ рынка устройств для надувания в Северной Америке

- Устройства для надувания баллонов, используемые для обеспечения контролируемого давления в баллонных катетерах во время интервенционных кардиологических, радиологических и сосудистых процедур, становятся все более важными компонентами современных малоинвазивных хирургических систем как в стационарных, так и в амбулаторных условиях благодаря своей точности, простоте использования и важной роли в катетерном лечении.

- Растущий спрос на устройства для создания избыточного давления в первую очередь обусловлен увеличением распространенности сердечно-сосудистых заболеваний и заболеваний периферических артерий, расширением применения малоинвазивных процедур и растущим предпочтением среди врачей точных, надежных и стерильных инструментов для создания избыточного давления.

- США доминировали на североамериканском рынке устройств для искусственной вентиляции легких, занимая наибольшую долю выручки в 84,7% в 2025 году. Этому способствовали развитая инфраструктура здравоохранения, большой объем интервенционных процедур и присутствие крупных производителей медицинского оборудования. В стране наблюдается существенный рост использования устройств для искусственной вентиляции легких, особенно в катетеризационных лабораториях и кардиологических центрах с высокой пропускной способностью, обусловленный постоянными инновациями в продукции и улучшением эргономичного дизайна.

- Ожидается, что Канада станет самой быстрорастущей страной на рынке устройств для искусственной вентиляции легких в Северной Америке в течение прогнозируемого периода благодаря увеличению инвестиций в отделения интервенционной кардиологии, расширению возможностей малоинвазивной хирургии и растущему спросу на одноразовые устройства для искусственной вентиляции легких, повышающие эффективность процедур и безопасность пациентов.

- Сегмент аналоговых устройств для нагнетания воздуха доминировал на рынке устройств для нагнетания воздуха в Северной Америке, занимая 65,2% рынка в 2025 году, благодаря своей экономической эффективности, доказанной клинической надежности и широкой совместимости с существующими катетерными системами.

Обзор отчета и сегментация рынка устройств для надувания в Северной Америке

|

Атрибуты |

Основные тенденции рынка устройств для искусственного надувания в Северной Америке: анализ рынка |

|

Охваченные сегменты |

|

|

Охваченные страны |

Северная Америка

|

|

Ключевые игроки рынка |

|

|

Рыночные возможности |

|

|

Информационные наборы данных, представляющие добавленную стоимость |

Помимо анализа рыночных сценариев, таких как рыночная стоимость, темпы роста, сегментация, географический охват и основные игроки, отчеты о рынке, подготовленные Data Bridge Market Research, также включают углубленный экспертный анализ, эпидемиологию пациентов, анализ перспективных разработок, анализ ценообразования и нормативно-правовую базу. |

Тенденции рынка устройств для надувания в Северной Америке

«Достижения в области точности, автоматизации и цифровой интеграции»

- Значительной и быстро набирающей обороты тенденцией на рынке устройств для нагнетания воздуха в Северной Америке является растущий переход к цифровым и автоматизированным системам нагнетания воздуха, которые повышают точность измерения давления, снижают количество ошибок при ручном управлении и поддерживают передовые рабочие процессы интервенционной кардиологии в больницах и катетеризационных лабораториях.

- Например, несколько ведущих производителей представляют устройства для накачивания воздуха со встроенными цифровыми манометрами и эргономичным дизайном, позволяющие врачам контролировать давление в режиме реального времени с большей точностью и меньшей нагрузкой во время процедур ангиопластики или установки стентов.

- Цифровая интеграция в устройства для накачивания воздуха обеспечивает такие функции, как автоматическое спускание воздуха, улучшенная стабилизация давления и расширенные оповещения пользователя о ненормальных показаниях. Например, в новых моделях от Merit Medical используются цифровые дисплеи, которые обеспечивают лучшую визуализацию, эффективность рабочего процесса и согласованность процедур во время критически важных вмешательств.

- Бесшовная интеграция устройств для надувания катетеров с более широким спектром платформ интервенционной визуализации и системами мониторинга в катетеризационных лабораториях обеспечивает централизованное управление, позволяя врачам координировать работу устройств с результатами визуализации и данными о процедуре для оптимизации процесса лечения.

- Тенденция к созданию более интеллектуальных, автоматизированных и поддерживаемых цифровыми технологиями решений для нагнетания воздуха коренным образом меняет представления о процедурах с использованием катетеров. Вследствие этого такие компании, как Teleflex и Boston Scientific, разрабатывают системы нагнетания воздуха с расширенными функциями создания дополнительного давления и улучшенной функциональностью, адаптированные для сложных интервенционных процедур.

- В отделениях интервенционной кардиологии и радиологии быстро растет спрос на устройства для нагнетания воздуха, обеспечивающие точную подачу давления, эргономичное управление и совместимость с цифровыми рабочими процессами, поскольку медицинские работники все чаще отдают приоритет эффективности, точности и улучшению клинических результатов.

Динамика рынка устройств для надувания в Северной Америке

Водитель

«Растущая потребность обусловлена увеличением сердечно-сосудистой нагрузки и предпочтением малоинвазивных процедур».

- Растущая распространенность сердечно-сосудистых и периферических артериальных заболеваний в США и Канаде, в сочетании с ускоренным внедрением малоинвазивных интервенционных процедур, является существенным фактором, обуславливающим повышенный спрос на устройства для искусственной вентиляции легких.

- Например, в 2025 году ряд медицинских учреждений расширили свои программы интервенционной кардиологии, модернизировав технологии катетеризационных лабораторий и улучшив возможности лечения с помощью катетеров, что способствовало более широкому использованию устройств для нагнетания воздуха в диагностических и терапевтических процедурах.

- Поскольку врачи уделяют первостепенное внимание точности и безопасности при проведении критически важных вмешательств, устройства для надувания баллонов обеспечивают точный контроль давления, мониторинг в режиме реального времени и повышенную надежность процедуры, представляя собой существенный шаг вперед по сравнению с базовыми ручными решениями.

- Кроме того, растущая популярность катетерных методов лечения и все большее предпочтение сокращению времени восстановления делают устройства для надувания катетеров неотъемлемым компонентом интервенционных систем, обеспечивая бесшовную интеграцию с современным хирургическим и диагностическим оборудованием.

- Удобство контролируемой подачи давления, улучшенная эргономика устройства и возможность проведения сложных процедур, таких как ангиопластика и стентирование сосудов, являются ключевыми факторами, способствующими внедрению устройств для нагнетания давления в крупных медицинских центрах.

- Тенденция к расширению амбулаторных интервенционных услуг и растущая доступность современных систем нагнетания воздуха, разработанных специально для учреждений с большим потоком пациентов, дополнительно способствуют росту рынка.

Сдержанность/Вызов

«Процедурные риски, барьеры, связанные с затратами, и препятствия на пути соблюдения нормативных требований»

- Опасения, связанные с неточностями, рисками, связанными с подачей давления, и изменчивостью характеристик некоторых ручных устройств для нагнетания воздуха, создают серьезные препятствия для более широкого проникновения на рынок, особенно в высокорискованных сердечно-сосудистых процедурах.

- Например, сообщения об осложнениях, возникающих из-за неправильного регулирования давления или неисправности оборудования во время надувания баллона, заставили некоторых медицинских работников с осторожностью относиться к использованию недорогих или нецифровых решений для надувания баллонов.

- Решение этих эксплуатационных проблем за счет улучшенной калибровки устройств, усовершенствованных механизмов контроля давления и более строгой проверки качества имеет решающее значение для повышения доверия врачей. Такие компании, как Cook Medical и Zimmer, делают акцент на точности проектирования и функциях безопасности, чтобы заверить пользователей в надежности устройств.

- Кроме того, относительно более высокая стоимость современных цифровых систем измерения давления по сравнению с традиционными ручными устройствами может стать препятствием для их внедрения в небольших больницах и учреждениях с ограниченным бюджетом, особенно в регионах с ограниченными капитальными средствами.

- Хотя цены постепенно стабилизируются, предполагаемая надбавка, связанная с расширенными цифровыми функциями, может препятствовать их широкому внедрению, особенно среди поставщиков, которые полагаются на устоявшиеся аналоговые системы и не нуждаются в немедленном переходе на цифровые технологии.

- Преодоление этих проблем за счет усиления стандартизации продукции, повышения квалификации врачей и разработки экономически эффективных, но высокоточных устройств для надувания баллонов будет иметь решающее значение для поддержания долгосрочного роста рынка.

Обзор рынка устройств для искусственного надувания в Северной Америке

Рынок сегментирован по типу, мощности, применению, давлению, функциям, конечному пользователю и каналу сбыта.

- По типу

В зависимости от типа, рынок устройств для раздувания баллонов в Северной Америке сегментируется на аналоговые и цифровые устройства. Сегмент аналоговых устройств доминировал на рынке, занимая наибольшую долю выручки в 65,2% в 2025 году, благодаря широкой клинической распространенности, экономической эффективности и надежности в рутинных интервенционных кардиологических и периферических сосудистых процедурах. Аналоговые устройства широко используются в крупных больницах и катетеризационных лабораториях благодаря простоте эксплуатации, быстрой настройке и надежной работе при раздувании баллонов. Их совместимость с широким спектром катетерных систем и стандартизированными рабочими процессами также способствует их доминированию. Кроме того, аналоговые устройства остаются ведущим выбором для учреждений, отдающих приоритет закупкам с контролем затрат.

Ожидается, что сегмент цифровых устройств для нагнетания давления продемонстрирует самый быстрый темп роста в период с 2026 по 2033 год, чему способствует растущий спрос на мониторинг давления в режиме реального времени и повышение точности при сложных сердечно-сосудистых и радиологических вмешательствах. Цифровые устройства для нагнетания давления предлагают расширенные функции, такие как цифровое отображение давления, улучшенная эргономика и автоматизированные функции управления, которые помогают снизить количество процедурных ошибок. Их растущее внедрение поддерживается модернизацией больниц, которые переходят на цифровые системы в своих катетеризационных лабораториях и интервенционных кабинетах. Увеличение инвестиций в малоинвазивные технологии и улучшение клинических результатов, связанных с цифровыми устройствами, также способствуют быстрому расширению рынка.

- По вместимости

По объему баллонов рынок сегментирован на устройства для надувания баллонов объемом 20 мл, 25 мл, 30 мл и 60 мл. Сегмент устройств для надувания баллонов объемом 30 мл доминировал на рынке в 2025 году благодаря идеальному балансу объема и давления, необходимого для большинства процедур ангиопластики и установки стентов. Больницы и интервенционные центры часто выбирают устройства объемом 30 мл из-за их универсальности в коронарных, периферических и радиологических приложениях. Эргономичный дизайн и точный контроль давления делают их предпочтительным выбором для врачей, выполняющих рутинные процедуры надувания баллонов. Сильное присутствие ведущих производителей, предлагающих оптимизированные модели объемом 30 мл, еще больше стимулирует спрос в этом сегменте.

Ожидается, что сегмент устройств с объемом нагнетания 60 мл продемонстрирует самый быстрый рост в период с 2026 по 2033 год, чему способствует растущее применение в периферических сосудистых и гастроэнтерологических процедурах, требующих большего объема. Более крупные баллоны, используемые при лечении заболеваний периферических артерий и в некоторых областях интервенционной радиологии, выигрывают от расширенного диапазона объемов, обеспечиваемого устройствами с объемом нагнетания 60 мл. Растущий спрос на сложные вмешательства и увеличение распространенности заболеваний периферических артерий в Северной Америке поддерживают ускоренный рост этого сегмента. Расширение использования устройств большой емкости в специализированных центрах дополнительно способствует сильным перспективам сегмента.

- По заявлению

В зависимости от области применения рынок сегментируется на интервенционную кардиологию, периферические сосудистые процедуры, интервенционную радиологию, урологические процедуры, гастроэнтерологические процедуры и другие. Интервенционная кардиология доминировала на рынке в 2025 году, чему способствовал большой объем ангиопластики, баллонной дилатации и установки стентов в США и Канаде. Растущая распространенность ишемической болезни сердца и растущая предпочтение малоинвазивным вмешательствам значительно способствуют увеличению спроса на устройства для инфляции, ориентированные на кардиологию. Больницы и катетеризационные лаборатории отдают приоритет прецизионным инструментам для инфляции, чтобы обеспечить оптимальное расширение стента и безопасность процедуры. Кроме того, постоянные инвестиции в кардиологическую инфраструктуру и быстрое внедрение передовых катетерных технологий укрепляют доминирование этого сегмента.

Ожидается, что интервенционная радиология станет самым быстрорастущим сегментом применения в период с 2026 по 2033 год, чему будет способствовать растущее внедрение процедур под контролем изображений как для сосудистых, так и для неваскулярных вмешательств. Устройства для надувания баллонов играют ключевую роль в ангиопластике, баллонной дилатации и установке устройств в рентгенологических кабинетах, где точность и видимость имеют решающее значение. Расширение сети амбулаторных рентгенологических центров и более широкое использование малоинвазивных методов лечения при заболеваниях брюшной полости, почек и печени способствуют быстрому росту сегмента. Улучшенная интеграция методов визуализации и технологические достижения еще больше увеличивают спрос на высокопроизводительные системы надувания баллонов в рентгенологических условиях.

- Под давлением

В зависимости от номинального давления рынок сегментируется на 30 атм, 40 атм, 55 атм и другие. Сегмент 30 атм доминировал на рынке в 2025 году благодаря своей пригодности для большинства стандартных процедур раздувания баллонов в коронарных и периферических артериях. Этот сегмент пользуется широким клиническим применением как в небольших, так и в крупных медицинских учреждениях благодаря доказанной надежности и безопасности при стандартных ангиопластических процедурах. Устройства 30 атм также широко доступны, экономически эффективны и совместимы с распространенными катетерными системами. Их способность соответствовать требованиям процедур при большом объеме вмешательств вносит значительный вклад в их лидирующие позиции.

Ожидается, что сегмент баллонов высокого давления (55 атм) продемонстрирует самый быстрый рост в течение прогнозируемого периода, главным образом благодаря расширению их использования в условиях высокого давления, таких как лечение кальцинированных поражений, вмешательства при хронических окклюзиях коронарных артерий и сложные процедуры расширения стентов. Поскольку врачи все чаще сталкиваются со сложными сосудистыми случаями, устройства для надувания баллонов под более высоким давлением обеспечивают улучшенное расширение просвета и контроль процедуры. Растущее внедрение специализированных баллонов высокого давления в интервенционной кардиологии и радиологии еще больше ускоряет рост. Постоянные инновации в материалах для баллонов и безопасности устройств также поддерживают растущий спрос на этот сегмент баллонов высокого давления.

- По функциям

По функциональному назначению рынок сегментируется на установку стентов и доставку жидкостей. В 2025 году установка стентов доминировала на рынке, что обусловлено центральной ролью устройств для нагнетания давления, обеспечивающих точное и контролируемое расширение коронарных и периферических стентов. Высокий объем процедур ангиопластики и стентирования в США значительно повышает спрос на инструменты для нагнетания давления, предназначенные для точной подачи давления. Необходимость в надежности при критически важных сердечно-сосудистых вмешательствах гарантирует, что установка стентов останется ведущей функцией устройств для нагнетания давления. Растущая распространенность сердечно-сосудистых заболеваний еще больше укрепляет доминирование этого сегмента.

Ожидается, что в период с 2026 по 2033 год наиболее быстрорастущей функцией станет система доставки жидкостей, чему способствует растущее использование устройств для нагнетания жидкости в неваскулярных и диагностических процедурах, требующих точного введения жидкости. По мере того, как врачи внедряют малоинвазивные подходы в различных областях медицины, таких как урология и гастроэнтерология, спрос на системы контролируемой доставки жидкостей возрастает. Технологические усовершенствования, обеспечивающие более плавное и эффективное управление жидкостями, еще больше способствуют быстрому росту этого сегмента. Расширение применения в амбулаторных условиях также укрепляет перспективы этого сегмента.

- Конечным пользователем

В зависимости от конечного пользователя рынок сегментируется на больницы, интервенционные лаборатории и клиники. В 2025 году больницы доминировали на рынке благодаря большому объему коронарных и периферических вмешательств, проводимых в больничных катетеризационных лабораториях и хирургических центрах. Их мощные возможности по закупкам и наличие развитой интервенционной инфраструктуры способствуют широкому внедрению как аналоговых, так и цифровых устройств для нагнетания давления. На больницы также приходится большинство сложных случаев, требующих расширенного контроля давления и специализированной совместимости устройств. Постоянные инвестиции в кардиоваскулярные и радиологические отделения укрепляют лидерство этого сегмента.

Ожидается, что в период с 2026 по 2033 год наиболее быстрый рост продемонстрируют интервенционные лаборатории, чему способствует растущее число специализированных катетеризационных лабораторий и отдельных интервенционных центров по всей Северной Америке. Эти учреждения отдают приоритет передовым инструментам для раздувания баллонов, обеспечивающим высокоточные процедуры и эффективное управление рабочим процессом. Растущий спрос на амбулаторную ангиопластику и сосудистые вмешательства в кабинетах врачей также способствует быстрому расширению сегмента. Технологические усовершенствования и переход к цифровым интервенционным системам еще больше ускоряют внедрение в этом сегменте.

- По каналам сбыта

По каналам сбыта рынок сегментируется на прямые закупки, розничные продажи и сторонних дистрибьюторов. В 2025 году сегмент прямых закупок доминировал на рынке благодаря крупным закупкам больницами, интегрированными системами здравоохранения и государственными учреждениями. Прямые закупки обеспечивают стабильные поставки оборудования, конкурентоспособные цены и доступ к передовым системам инфляции для центров с большими объемами закупок. Прочные связи между производителями и медицинскими учреждениями еще больше поддерживают доминирование этого сегмента в Северной Америке.

Ожидается, что сегмент розничных продаж продемонстрирует самый быстрый рост в период с 2026 по 2033 год, чему способствует растущее внедрение устройств для искусственной вентиляции легких клиниками, амбулаторными центрами и небольшими интервенционными учреждениями, которые полагаются на гибкие варианты закупок. Розничная дистрибуция также выигрывает от растущей доступности современных устройств для искусственной вентиляции легких через специализированных поставщиков медицинского оборудования и онлайн-платформы для профессионалов. Растущий спрос со стороны независимых практикующих врачей и амбулаторных учреждений вносит значительный вклад в быстрый рост этого сегмента.

Региональный анализ рынка устройств для надувания в Северной Америке

- США доминировали на североамериканском рынке устройств для искусственной вентиляции легких, занимая наибольшую долю выручки в 84,7% в 2025 году. Этому способствовали развитая инфраструктура здравоохранения, большой объем интервенционных процедур и присутствие крупных производителей медицинского оборудования. В стране наблюдается существенный рост использования устройств для искусственной вентиляции легких, особенно в катетеризационных лабораториях и кардиологических центрах с высокой пропускной способностью, обусловленный постоянными инновациями в продукции и улучшением эргономичного дизайна.

- Больницы и хирургические центры региона уделяют особое внимание высоким стандартам клинических результатов, что обуславливает постоянный спрос на современные устройства для надувания дыхательных путей с повышенной точностью, эргономичным дизайном и возможностями цифрового мониторинга.

- Внедрение новых технологий дополнительно стимулируется хорошо развитой в регионе индустрией медицинских изделий, высокими расходами на здравоохранение и быстрой интеграцией малоинвазивных процедур в кардиологию, гастроэнтерологию и урологию.

Анализ рынка устройств для искусственного надувания в США

В 2025 году рынок устройств для искусственной вентиляции легких в США занял наибольшую долю выручки в Северной Америке – 84,7%, чему способствовал большой объем интервенционных кардиологических и периферических сосудистых процедур. Больницы и катетеризационные лаборатории все чаще отдают приоритет устройствам для точной искусственной вентиляции легких с контролем давления, чтобы повысить безопасность процедур и улучшить клинические результаты. Растущая популярность цифровых систем искусственной вентиляции легких с мониторингом давления в реальном времени и эргономичным дизайном еще больше способствует росту рынка. Кроме того, внедрение малоинвазивных процедур и интеграция с передовыми катетерными технологиями вносят значительный вклад в расширение рынка. Развитая инфраструктура здравоохранения и большой объем процедур также поддерживают постоянный спрос как на аналоговые, так и на цифровые устройства.

Анализ рынка устройств для искусственного надувания в Канаде

Ожидается, что рынок устройств для искусственной вентиляции легких в Канаде будет расти значительными темпами в течение прогнозируемого периода, в основном за счет увеличения инвестиций в программы интервенционной кардиологии и модернизации катетеризационных лабораторий. Повышение осведомленности о здоровье сердечно-сосудистой системы в сочетании с ростом объемов процедур способствует внедрению современных устройств для искусственной вентиляции легких. Канадские медицинские учреждения заинтересованы в устройствах, обеспечивающих повышенную точность, надежность и интеграцию с системами визуализации. В регионе наблюдается заметный рост в больницах, интервенционных лабораториях и специализированных центрах, при этом как аналоговые, так и цифровые устройства внедряются в новые и модернизированные учреждения.

Анализ рынка устройств для искусственного нагнетания воздуха в Мексике

Ожидается, что рынок устройств для искусственной вентиляции легких в Мексике будет расти значительными темпами в течение прогнозируемого периода, чему способствуют растущий спрос на малоинвазивные процедуры и увеличение заболеваемости сердечно-сосудистыми заболеваниями. Больницы и частные клиники внедряют устройства для искусственной вентиляции легких, чтобы повысить безопасность пациентов и эффективность процедур. Кроме того, растущие инвестиции в инфраструктуру здравоохранения и расширение центров интервенционной кардиологии, как ожидается, будут и дальше стимулировать рост рынка. Внедрение удобных в использовании устройств, подходящих как для аналоговых, так и для цифровых рабочих процессов, также способствует росту спроса.

Доля рынка устройств для нагнетания воздуха в Северной Америке

В Северной Америке лидирующие позиции в отрасли устройств для надувания шин занимают, в основном, хорошо зарекомендовавшие себя компании, в том числе:

- Merit Medical Systems, Inc. (США)

- Бостонская научная корпорация (США)

- Б. Браун, США

- Корпорация CONMED (США)

- Teleflex Incorporated (США)

- US Endovascular, LLC (США)

- Корпорация Атрион (США)

- БД (США)

- Кук (США)

- Компания Argon Medical Devices, Inc. (США)

- TZ Medical, Inc. (США)

- Кардинал Хит (США)

- Корпорация «Олимпус» (Япония)

- Корпорация Терумо (Япония)

- Medtronic (Ирландия)

- Аккларент, Инк. (США)

- Johnson & Johnson Services, Inc. (США)

- Эббот (США)

- AngioDynamics, Inc. (США)

- Vygon SAS (Франция)

Какие последние тенденции наблюдаются на рынке устройств для надувания шин в Северной Америке?

- В январе 2025 года компания Olympus Latin America приобрела дистрибьюторский бизнес Sur Medical SpA в Чили, образовав компанию Olympus Corporation Chile. Это приобретение обеспечивает прямой доступ к растущему чилийскому рынку здравоохранения, оптимизирует дистрибуцию продукции Olympus и улучшает обслуживание и поддержку клиентов в регионе.

- В ноябре 2024 года компания Merit Medical Systems завершила приобретение портфеля решений Cook Medical по управлению электродами примерно за 210 миллионов долларов США. Это приобретение расширяет бизнес Merit в области электрофизиологии и управления сердечным ритмом, добавляя широкий спектр устройств, используемых при процедурах удаления и замены электродов кардиостимуляторов и имплантируемых кардиовертеров-дефибрилляторов.

- В мае 2024 года компания Merit Medical Systems объявила о начале коммерческого выпуска в США устройства для надувания баллона basixSKY. Это аналоговое устройство предназначено для эндоваскулярных вмешательств, таких как баллонная ангиопластика и установка стентов. Оно оснащено удобной рукояткой для подготовки баллона одной рукой и минимизирует крутящий момент и количество оборотов рукоятки для достижения необходимого давления. Устройство доступно как в виде автономного решения, так и в комплектах с наборами для ангиопластики Merit, которые дополняют гемостатические клапаны AccessPLUS, Honor и PhD.

- В апреле 2024 года компания Integra LifeSciences Corporation завершила приобретение Acclarent, Inc., компании, специализирующейся на решениях для ЛОР-заболеваний (заболевания уха, носа и горла). Это приобретение расширяет портфель Integra на рынке ЛОР-заболеваний, увеличивая ее возможности в области инновационных медицинских технологий для лечения синусита, заболеваний уха и носа, что будет способствовать дальнейшему росту в секторе здравоохранения.

- В январе 2022 года компания Medtronic приобрела Affera, компанию, специализирующуюся на кардиологических технологиях и системах картирования, навигации и абляции для лечения аритмий, таких как фибрилляция предсердий. Это приобретение знаменует собой выход Medtronic на рынок кардиологического картирования, расширяя ее портфель решений для абляции сердца.

SKU-

Получите онлайн-доступ к отчету на первой в мире облачной платформе рыночной аналитики

- Интерактивная панель анализа данных

- Панель анализа компании для возможностей с высоким потенциалом роста

- Доступ аналитика-исследователя для настройки и запросов

- Анализ конкурентов с помощью интерактивной панели

- Последние новости, обновления и анализ тенденций

- Используйте возможности сравнительного анализа для комплексного отслеживания конкурентов

Методология исследования

Сбор данных и анализ базового года выполняются с использованием модулей сбора данных с большими размерами выборки. Этап включает получение рыночной информации или связанных данных из различных источников и стратегий. Он включает изучение и планирование всех данных, полученных из прошлого заранее. Он также охватывает изучение несоответствий информации, наблюдаемых в различных источниках информации. Рыночные данные анализируются и оцениваются с использованием статистических и последовательных моделей рынка. Кроме того, анализ доли рынка и анализ ключевых тенденций являются основными факторами успеха в отчете о рынке. Чтобы узнать больше, пожалуйста, запросите звонок аналитика или оставьте свой запрос.

Ключевой методологией исследования, используемой исследовательской группой DBMR, является триангуляция данных, которая включает в себя интеллектуальный анализ данных, анализ влияния переменных данных на рынок и первичную (отраслевую экспертную) проверку. Модели данных включают сетку позиционирования поставщиков, анализ временной линии рынка, обзор рынка и руководство, сетку позиционирования компании, патентный анализ, анализ цен, анализ доли рынка компании, стандарты измерения, глобальный и региональный анализ и анализ доли поставщика. Чтобы узнать больше о методологии исследования, отправьте запрос, чтобы поговорить с нашими отраслевыми экспертами.

Доступна настройка

Data Bridge Market Research является лидером в области передовых формативных исследований. Мы гордимся тем, что предоставляем нашим существующим и новым клиентам данные и анализ, которые соответствуют и подходят их целям. Отчет можно настроить, включив в него анализ ценовых тенденций целевых брендов, понимание рынка для дополнительных стран (запросите список стран), данные о результатах клинических испытаний, обзор литературы, обновленный анализ рынка и продуктовой базы. Анализ рынка целевых конкурентов можно проанализировать от анализа на основе технологий до стратегий портфеля рынка. Мы можем добавить столько конкурентов, о которых вам нужны данные в нужном вам формате и стиле данных. Наша команда аналитиков также может предоставить вам данные в сырых файлах Excel, сводных таблицах (книга фактов) или помочь вам в создании презентаций из наборов данных, доступных в отчете.