Global Automotive Plastics Market

市场规模(十亿美元)

CAGR :

%

USD

33.84 Billion

USD

79.13 Billion

2024

2032

USD

33.84 Billion

USD

79.13 Billion

2024

2032

| 2025 –2032 | |

| USD 33.84 Billion | |

| USD 79.13 Billion | |

| % | |

|

Global Automotive Plastics Market Segmentation, By Product Type (Polypropylene, Polyurethane,Polyvinyl ChlorideAcrylonitrile-Butadiene-Styrene(ABS), Polyamide,High-Density Polyethylene (HDPE), Polycarbonate, Polybutylene Terephthalate (PBT), and Others), Vehicle Type (Conventional Cars and Electric Cars), Application (Powertrain, Electrical Components, Interior Furnishings, Under-The-Hood Components, Chassis, and Others) - Industry Trends and Forecast to 2032

Automotive Plastics Market Size

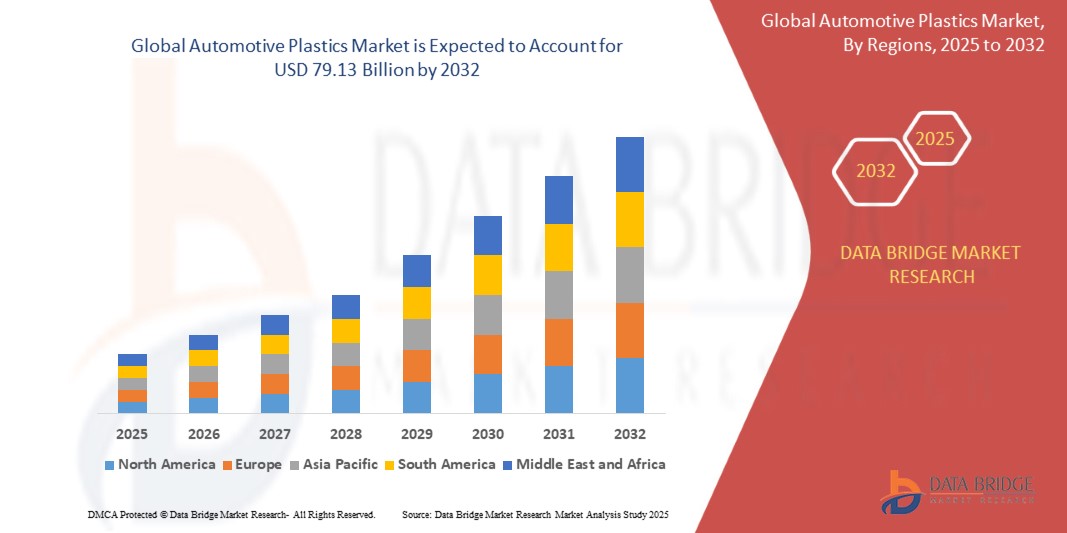

- The global automotive plastics market was valued atUSD 33.84 billion in 2024and is expected to reachUSD 79.13 billion by 2032

- During the forecast period of 2025 to 2032 the market is likely to grow at aCAGR of 11.20%,primarily driven by increasing demand for lightweight vehicles

- This growth is driven by the stringent government regulations on sustainability and the growing adoption of electric vehicles (EVs)

Automotive Plastics Market Analysis

- Automotive plastics has gained widespread acceptance due to its lightweight, durability, and high-performance characteristics, driving demand in vehicle manufacturing, electric vehicles (EVs), and sustainability initiatives. Its proven ability to enhance fuel efficiency, reduce carbon emissions, and improve crash safety has solidified its role in modern automotive engineering

- The market is primarily driven by increasing demand for lightweight materials, stringent government regulations on emissions, and the rising adoption of EVs. In addition, advancements in bio-based plastics and investments in automotive interiors are further accelerating market growth

- Asia-Pacific dominates the automotive plastics market due to its strong automotive manufacturing base, increasing vehicle production, and rapid adoption of sustainable materials

- For instance, inChina and India, the demand forlightweight plasticshas surged due to stringentfuel efficiencynorms and growingEV production, contributing to sustained market expansion

- Globally,automotive plasticscontinues to be acornerstoneinvehicle designandsustainability, with innovations such asrecyclable polymers,composite materials, andadvanced manufacturing techniquesdriving industry transformation and ensuring long-term market sustainability

Report Scope and Automotive Plastics Market Segmentation

|

Attributes |

Automotive Plastics Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Automotive Plastics Market Trends

“Rising Integration of Automotive Plastics in Sustainable Vehicle Manufacturing”

- The increasing focus onsustainabilityis driving demand forautomotive plastics, widely recognized for its role inlightweight vehicle designandfuel efficiencyimprovement

- Automakersare expanding the use ofhigh-performance plasticsinelectric vehicles (EVs),interior components, andstructural applicationsto enhance durability and reduce overallcarbon footprint

- The rising adoption ofbio-based polymersandrecyclable materialsis accelerating the shift towardseco-friendly vehicle production, aligning with stringentgovernment regulationson emissions

For instance,

- InFebruary 2024,Teslaincorporatedadvanced polymer compositesin its latest EV model, enhancingbattery efficiencyand overallvehicle weight reduction

- InOctober 2023,Toyotaintroduced a newrecyclable plasticdashboard, reinforcing its commitment tosustainable automotive manufacturing

- InJuly 2023,BASFpartnered withleading automakersto developbio-based plasticsfor next-generationEV interiors, ensuring higher durability and lowerenvironmental impact

- As theautomotive industrycontinues to prioritizesustainability,automotive plasticswill play a crucial role invehicle innovation, driving efficiency, durability, and compliance with globalemission standards

Automotive Plastics Market Dynamics

Driver

“Growing Demand for Lightweight Vehicles”

- Increasingfuel efficiencyand reducingcarbon emissionsare key priorities for theautomotive industry, driving the adoption oflightweight plasticsas an alternative to metals.

- Automakersare incorporatinghigh-performance polymersinvehicle interiors, exteriors, and under-the-hood componentsto enhance durability, safety, and design flexibility

- The rising penetration ofelectric vehicles (EVs)further accelerates the need forlightweight materials, as reducing vehicle weight directly improvesbattery performance and driving range

For instance,

- InMarch 2024,Fordintegratedpolycarbonate-based componentsinto its new EV lineup to reduce vehicle weight and enhanceenergy efficiency

- InNovember 2023,General Motorspartnered withBASFto develophigh-strength plastic compositesfor structural applications, replacing traditional metal parts.

- InAugust 2023,Hyundaiannounced the use ofbio-based plasticsin its next-gen vehicle interiors, reinforcing its commitment tosustainable mobility

- With strictergovernment regulationsonfuel efficiencyandemissions, the demand forautomotive plasticswill continue to grow, driving innovation inlightweight vehicle designand sustainable manufacturing

Opportunity

“Expansion of Bio-Based and Recyclable Automotive Plastics”

- Growing environmental concerns and stringentgovernment regulationsare creating opportunities forbio-basedandrecyclable plastics, reducing reliance on fossil fuel-derived materials

- Automakersare investing insustainable plastic alternativesto meetcarbon neutrality goals, improveend-of-life recyclability, and enhancebrand sustainability efforts

- The increasing adoption ofcircular economy principlesinautomotive manufacturingis driving demand forrecycled polymers, minimizing waste and lowering production costs

For instance,

- InJanuary 2024,BMWlaunched a new initiative to incorporateocean-recycled plasticsinto its vehicle interiors, supporting itssustainability strategy

- InSeptember 2023,Volkswagenpartnered withbiopolymer manufacturersto integrateplant-based plasticsinto its upcoming EV models

- InJune 2023,Stellantiscommitted to using at least50% recycled plasticsin its next-generation vehicle components to reduceenvironmental impact

- As theautomotive industryaccelerates its shift towardseco-friendly materials,bio-based and recyclable plasticswill unlock new growth avenues, enhancingsustainability, innovation, and regulatory compliance

Restraint/Challenge

“Recycling Complexities in Automotive Plastics”

- Themulti-layered compositionofautomotive plastics, combined withadditives and reinforcements, makesrecycling difficultand limits the feasibility of acircular economyin the sector

- Automakersface challenges inseparating, sorting, and reprocessingplastic components fromend-of-life vehicles, increasingwaste management costs

- Strictergovernment regulationsonplastic waste disposalare pushing companies to invest inadvanced recycling technologies, further raisingoperational expenses

For instance,

- InMarch 2024,Renaultreported difficulties in recoveringcomposite plasticsfrom scrapped vehicles, impacting itssustainability goals

- Addressingrecycling inefficiencieswill be critical for theautomotive industry, ensuringcost-effective plastic reusewhile meetingglobal environmental regulations

Automotive Plastics Market Scope

The market is segmented on the basis of product type, vehicle type, and application.

|

Segmentation |

Sub-Segmentation |

|

By Product Type |

|

|

By Vehicle Type |

|

|

By Application |

|

Automotive Plastics Market Regional Analysis

“Asia-Pacific is the Dominant Region in the Automotive Plastics Market”

- Asia-Pacificleads the globalAutomotive Plasticsmarket, driven by rapidindustrialization, increasingautomobile production, and strong demand forlightweight materials

- ChinaandIndiadominate the region due to their expandingautomotive manufacturing, risingvehicle sales, and strong government incentives forfuel efficiency

- Advancements inpolymer technology, increasing adoption ofelectric vehicles (EVs), and rising consumer preference forsustainable materialshave further accelerated market growth

- In addition, the presence of majorautomotive suppliers, expandingOEM production, and growing investments inresearch & developmentcontribute to the region’s market leadership

“Asia-Pacific is projected to register the Highest Growth Rate”

- Asia-Pacificis expected to witness the highest growth rate in theautomotive plasticsmarket, driven by rapidurbanization, increasingvehicle production, and growing demand forlightweight components

- ChinaandIndiaare emerging as key markets due to strongautomotive manufacturing, supportive government policies, and rising investments inelectric mobility

- Chinaleads the region inautomotive plasticsproduction, with advancedpolymer processingtechnologies and increasing adoption ofsustainable materialsfor vehicle components

- Indiais experiencing strong market growth due to risingautomobile exports, expandingEV infrastructure, and growing consumer preference forfuel-efficient vehicles

- Stringentemission regulations, increasing R&D inbioplastics, and strategic collaborations betweenautomotive OEMsfurther contribute to Asia-Pacific’s market expansion

Automotive Plastics Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- Magna International Inc. (Canada)

- Lear (U.S.)

- Adient plc (Ireland)

- BASF (Germany)

- Borealis AG (Austria)

- Covestro AG (Germany)

- Evonik Industries AG (Germany)

- SABIC (Saudi Arabia)

- Antolin (Spain)

- TOYOTA BOSHOKU CORPORATION (Japan)

- FORVIA HELLA (Germany)

- TOYODA GOSEI Co., Ltd. (Japan)

- Sage Automotive Interiors, Inc. (U.S.)

- DSM (Netherlands)

- Dow (U.S.)

- Momentive Performance Materials (U.S.)

- TEIJIN LIMITED (Japan)

- Solvay (Belgium)

- Akzo Nobel N.V. (Netherlands)

- CNR Group, LLC (U.S.)

Latest Developments in Global Automotive Plastics Market

- In June 2023,Borealis AGacquiredRialti S.p.A., a leadingpolypropylene (PP)compounding company specializing in recyclates in Italy’s Varese region. This acquisition strengthensBorealis'expertise and production capacity inPP compounding, particularly in increasing the volume of mechanically recycledPP compoundsto enhance its specialized and circular portfolios

- In May 2023,Learannounced plans to establish aconnection systems facilityin Morocco, aimed at manufacturing components for automakers, suppliers, and itsE-systemsandseating unitsto expand its automotive technology capabilities

- In November 2022,Covestro AGcollaborated withHASCO Visionto recyclepost-industrial plastics. Through this partnership,Covestrocollects used plastics fromHASCO'sproduction facilities, converts them into high-qualitypost-industrial recycled polycarbonatesandpolycarbonate blends, and supplies them back for manufacturing newautomotive components

- In June 2021,Lyondellbasellentered a long-term agreement withNesteto sourceNeste RE, a feedstock made entirely from renewable sources such as residue oils, fats, and waste. This material is processed atLyondellbasell'sWesseling, Germany, plant into polymers sold under theCirculenRenewbrand

- In May 2021,Lyondellbasellcommenced production ofvirgin-quality polymersusing raw materials derived from plastic waste at its Wesseling, Germany, facility. These raw materials are converted intopropyleneandethylene, which are further processed intopolypropylene (PP)andpolyethylene (PE)for plastics manufacturing

- In May 2021,ARKEMAcompleted the acquisition ofAgiplast, a company specializing in the regeneration ofhigh-performance polymers. This acquisition enablesARKEMAto become a fully integratedhigh-performance polymermanufacturer, focusing on bothrecycledandbio-based materialsto drive sustainability and circular economy initiatives

SKU-

研究方法

数据收集和基准年分析是使用具有大样本量的数据收集模块完成的。该阶段包括通过各种来源和策略获取市场信息或相关数据。它包括提前检查和规划从过去获得的所有数据。它同样包括检查不同信息源中出现的信息不一致。使用市场统计和连贯模型分析和估计市场数据。此外,市场份额分析和关键趋势分析是市场报告中的主要成功因素。要了解更多信息,请请求分析师致电或下拉您的询问。

DBMR 研究团队使用的关键研究方法是数据三角测量,其中包括数据挖掘、数据变量对市场影响的分析和主要(行业专家)验证。数据模型包括供应商定位网格、市场时间线分析、市场概览和指南、公司定位网格、专利分析、定价分析、公司市场份额分析、测量标准、全球与区域和供应商份额分析。要了解有关研究方法的更多信息,请向我们的行业专家咨询。

可定制

Data Bridge Market Research 是高级形成性研究领域的领导者。我们为向现有和新客户提供符合其目标的数据和分析而感到自豪。报告可定制,包括目标品牌的价格趋势分析、了解其他国家的市场(索取国家列表)、临床试验结果数据、文献综述、翻新市场和产品基础分析。目标竞争对手的市场分析可以从基于技术的分析到市场组合策略进行分析。我们可以按照您所需的格式和数据样式添加您需要的任意数量的竞争对手数据。我们的分析师团队还可以为您提供原始 Excel 文件数据透视表(事实手册)中的数据,或者可以帮助您根据报告中的数据集创建演示文稿。