Global Vomiting Treatment Market

市场规模(十亿美元)

CAGR :

%

USD

5.90 Million

USD

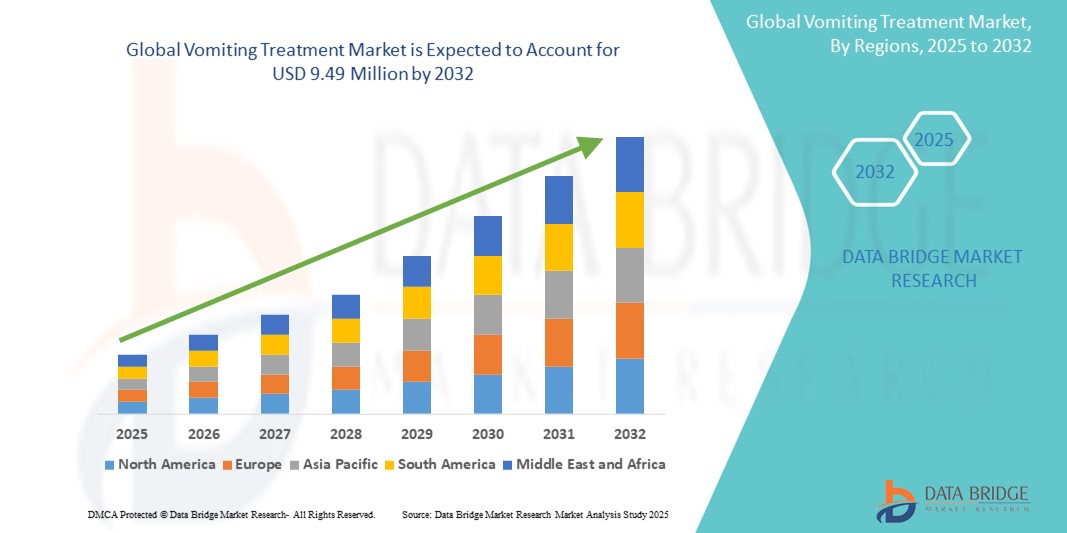

9.49 Million

2024

2032

USD

5.90 Million

USD

9.49 Million

2024

2032

| 2025 –2032 | |

| USD 5.90 Million | |

| USD 9.49 Million | |

| % | |

|

全球嘔吐治療市場細分,按類型(嘔吐、反流和噴射性嘔吐)、作用機制(血清素拮抗劑、抗組織胺藥、D2 受體拮抗劑、苯二氮平類、多巴胺拮抗劑等)、藥物(昂丹司瓊、異丙嗪、甲氧氯普胺、勞拉西泮等)、治療藥物(藥物、藥物、零售藥物、零售藥物通路、零售藥物、零售藥物、零售藥物、零售藥物、零售藥物、零售藥物、藥物和醫院)、藥物、零售藥物、零售藥物、零售藥物、零售藥物和醫院)、藥物、零售藥物、零售藥物、零售藥物和醫院)、藥物、藥物和醫院)、零售藥物、零售藥物、零售藥物、零售藥物、零售藥物、零售藥物和醫院)、藥物配送品(藥物及外產業趨勢和預測到 2032 年

嘔吐治療市場規模

- 2024 年全球嘔吐治療市場規模為590 萬美元 ,預計 到 2032 年將達到 949 萬美元,預測期內 複合年增長率為 6.10%。

- 市場成長主要受到胃腸道疾病、暈動病、術後恢復要求以及化療引起的噁心和嘔吐(CINV) 盛行率不斷上升的推動,所有這些都推動了對有效止吐藥物和療法的需求

- 此外,隨著癌症治療中支持性護理意識的不斷提升、非處方(OTC) 和處方止吐藥的可近性不斷提高,以及給藥方式的不斷進步,嘔吐治療已成為急性和慢性醫療管理中不可或缺的一部分。這些因素共同加速了嘔吐治療解決方案的普及,顯著促進了該行業的成長。

嘔吐治療市場分析

- 嘔吐治療方案涵蓋一系列藥物幹預措施,例如止吐藥和非藥物療法,在現代臨床實踐中,對於治療與胃腸道感染、化療、懷孕和術後恢復等情況相關的噁心和嘔吐,正變得越來越重要。

- 嘔吐治療需求的不斷增長,主要原因是癌症和胃腸道疾病等慢性疾病的發病率不斷上升,易患此類症狀的老年人口不斷擴大,以及人們對腫瘤學和姑息治療中支持性護理的認識不斷提高

- 北美在嘔吐治療市場佔據主導地位,2024 年其收入份額最大,為 39.2%,其特點是醫療基礎設施先進、新型止吐劑型採用率高,以及腫瘤治療支持藥物供應充足

- 由於患者人數不斷增加、醫療保健管道不斷擴大以及政府日益重視癌症治療和孕產婦健康,預計亞太地區將成為預測期內嘔吐治療市場成長最快的地區

- 血清素拮抗劑在嘔吐治療市場佔據主導地位,2024 年的市佔率為 42.1%,這得益於其在治療化療引起的噁心和嘔吐以及術後噁心和嘔吐方面的高效性,以及良好的安全性

報告範圍和嘔吐治療市場細分

|

屬性 |

嘔吐治療關鍵市場洞察 |

|

涵蓋的領域 |

|

|

覆蓋國家 |

北美洲

歐洲

亞太

中東和非洲

南美洲

|

|

主要市場參與者 |

|

|

市場機會 |

|

|

加值資料資訊集 |

除了對市場價值、成長率、細分、地理覆蓋範圍和主要參與者等市場情景的洞察之外,Data Bridge Market Research 策劃的市場報告還包括深入的專家分析、定價分析、品牌份額分析、消費者調查、人口統計分析、供應鏈分析、價值鏈分析、原材料/消耗品概述、供應商選擇標準、PESTLE 分析、波特分析和監管框架。 |

嘔吐治療市場趨勢

“標靶止吐療法和個人化護理的進展”

- 全球嘔吐治療市場的一個重要且加速發展的趨勢是針對性止吐療法的開發和應用,旨在有效管理化療、術後恢復、暈動病和其他疾病引起的噁心和嘔吐。這種對精準治療的關注正在改善患者的治療效果和舒適度。

- 例如,5-HT3受體拮抗劑和NK1受體拮抗劑的聯合療法正在成為癌症治療的標準,並且能夠更好地控制化療引起的噁心和嘔吐(CINV)。同樣,口腔崩解片(ODT)和透皮貼片的推出也為兒童和老年患者提供了更方便的給藥選擇。

- 個人化醫療方法也正在興起,根據患者的個人情況、遺傳因素和具體的嘔吐原因制定個人化治療方案,從而更有效地管理症狀。針灸和先進的補液技術等補充療法作為藥物治療的輔助手段,正日益受到關注,進一步提升患者的健康水平。

- 口服製劑和患者友善藥物傳遞系統的日益普及正在提高患者的依從性,尤其是在門診和家庭護理環境中。

- 這種個人化、多模式和以患者為中心的嘔吐治療趨勢正在從根本上重塑治療策略,製藥公司大力投資創新藥物配方和聯合療法,以滿足不同患者的需求

- 隨著醫療保健提供者優先考慮全面的症狀控制和支持性護理,腫瘤科、胃腸科和急診科對能夠提高療效和生活品質的先進嘔吐治療解決方案的需求正在迅速增長

嘔吐治療市場動態

司機

“慢性病發病率上升,支持性護理意識增強”

- 癌症、胃腸道疾病和病毒感染等慢性疾病的盛行率不斷上升,以及容易出現噁心和嘔吐的老年人口不斷增加,是推動嘔吐治療解決方案需求的重要驅動因素

- 例如,一家領先的製藥公司於2024年3月推出了一種新型複方止吐療法,旨在緩解化療引起的噁心,凸顯了其對加強腫瘤支持治療的重視。預計主要參與者的此類創新將在預測期內加速市場成長。

- 隨著患者和醫療保健提供者越來越意識到有效症狀管理的重要性,具有更高療效和安全性的嘔吐治療方法比傳統療法更受青睞

- 此外,大眾對未經治療的嘔吐併發症(如脫水和電解質失衡)的認識不斷提高,正在推動藥物和非藥物治療方案的採用

- The growing availability of oral antiemetics, rehydration therapies, and comprehensive treatment protocols across hospitals, clinics, and home care settings is facilitating wider access and better patient outcomes, supporting market expansion

- Increasing investments in research and development for targeted antiemetic drugs and personalized treatment approaches are also key factors propelling the vomiting treatment market growth globally

Restraint/Challenge

“Side Effects and Limited Access in Low-Income Regions”

- Despite advancements in antiemetic therapies, concerns regarding the side effects and tolerability of certain vomiting treatment drugs pose a significant challenge to broader market penetration. Common adverse effects such as sedation, extrapyramidal symptoms, or cardiac concerns associated with some medications, such as dopamine antagonists or serotonin antagonists, can limit their use in specific patient populations

- For instance, regulatory agencies have issued cautions about the use of certain antiemetics in pediatric and geriatric patients due to increased risk of adverse events, making clinicians more cautious in prescribing them. These safety-related concerns create barriers in achieving universal treatment protocols and necessitate ongoing drug monitoring and education

- Addressing these concerns through the development of better-tolerated formulations, patient-specific treatment strategies, and clearer dosing guidelines is crucial for expanding treatment coverage. Pharmaceutical companies are increasingly focusing on producing targeted antiemetics with improved safety profiles to alleviate these concerns

- In addition, limited access to effective vomiting treatments in low-income and rural regions remains a major barrier to market growth. The lack of availability of newer antiemetics, coupled with poor healthcare infrastructure and insufficient awareness, prevents timely diagnosis and management of vomiting symptoms in underserved populations

- While generic medications are helping to lower treatment costs, disparities in distribution, cold-chain logistics for certain formulations, and low prioritization of symptom control in primary care settings hinder widespread access

- Overcoming these challenges through drug safety enhancements, healthcare provider training, and global access initiatives will be critical to ensuring equitable and sustained growth in the global vomiting treatment market

Vomiting Treatment Market Scope

The market is segmented on the basis of type, mechanism of action, drugs, treatment, route of administration, and distribution channel.

-

By Type

On the basis of type, the vomiting treatment market is segmented into posseting, reflux, and projectile vomiting. The reflux segment dominates the largest market revenue share in 2024, driven by its high prevalence across both pediatric and adult populations, particularly in gastrointestinal conditions and post-operative settings. Reflux-associated vomiting is frequently treated due to its recurrent nature, prompting the widespread use of antiemetics and acid-suppressing agents. The increasing awareness about early diagnosis and the availability of effective pharmacological therapies further support the growth of this segment.

The projectile vomiting segment is anticipated to witness the fastest growth rate from 2025 to 2032, fueled by rising diagnostic rates of underlying causes such as pyloric stenosis and neurological disorders. The growing demand for accurate and prompt treatment protocols, along with improved pediatric healthcare infrastructure, is expected to drive this segment forward during the forecast period.

- By Mechanism Of Action

On the basis of mechanism of action, the vomiting treatment market is segmented into serotonin antagonists, antihistamines, D2 receptor antagonists, benzodiazepines, dopamine antagonists, and others. The serotonin antagonist segment dominates the largest market revenue share of 42.1% in 2024, driven by its proven effectiveness in treating acute, chemotherapy-induced, and post-operative vomiting. Widely used agents such as ondansetron are considered first-line treatment in various clinical scenarios due to their minimal side effects and rapid onset of action.

The D2 receptor antagonists segment is expected to witness the fastest growth rate from 2025 to 2032, driven by their expanding role in chronic nausea and gastrointestinal disorders. Their effectiveness in patients unresponsive to standard treatments and increasing use in hospital settings contribute to the rising demand.

- By Drugs

On the basis of drugs, the market is segmented into ondansetron, promethazine, metoclopramide, lorazepam, and others. The ondansetron segment holds the largest market revenue share in 2024, driven by its well-established efficacy across a wide range of vomiting etiologies, including chemotherapy-induced nausea, pregnancy-related vomiting, and post-operative nausea. Its inclusion in essential medicine lists and broad clinical acceptance further cement its market dominance.

The metoclopramide segment is anticipated to grow rapidly over the forecast period due to its dual prokinetic and antiemetic effects, especially in treating gastroparesis and functional dyspepsia-related vomiting. As awareness grows regarding the diverse utility of this medication, demand is expected to increase in both primary care and specialist settings.

- By Treatment

On the basis of treatment, the vomiting treatment market is segmented into medications, rehydration, and others. The medications segment dominates the largest market revenue share in 2024, driven by their immediate effectiveness in symptom relief and the availability of multiple drug classes targeting different mechanisms. As vomiting is often a secondary symptom to various underlying conditions, medications remain the frontline approach in both acute and chronic scenarios.

The rehydration segment is projected to register the fastest CAGR from 2025 to 2032, fueled by rising emphasis on supportive care, especially in pediatric and elderly populations where fluid loss poses greater health risks. Growing healthcare focus on holistic recovery and guidelines promoting fluid balance management further support segment growth

- By Route Of Administration

On the basis of route of administration, the vomiting treatment market is segmented into oral and parenteral. The oral segment dominates the largest market revenue share in 2024, attributed to the widespread availability of tablets, syrups, and dissolvable forms that offer convenience and compliance, especially in outpatient care. Oral antiemetics are often the first line of defense for mild to moderate cases, with rapid advancements improving bioavailability and onset time.

The parenteral segment is expected to witness strong growth during forecast period, driven by its importance in emergency and hospital settings where oral intake is not feasible. Intravenous formulations are especially favored in post-surgical recovery, oncology, and severe dehydration cases.

- By Distribution Channel

On the basis of distribution channel, the vomiting treatment market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The retail pharmacy segment dominates the largest market revenue share in 2024, driven by strong over-the-counter availability of key antiemetic drugs and wide accessibility to consumers across urban and rural settings. Pharmacist guidance and affordability also contribute to the popularity of this channel.

The online pharmacy segment is anticipated to witness the fastest growth rate from 2025 to 2032, supported by increasing consumer shift towards digital healthcare platforms, rising penetration of e-pharmacies in emerging markets, and the convenience of doorstep delivery. Enhanced regulatory clarity and growing trust in licensed online platforms further accelerate this trend.

Vomiting Treatment Market Regional Analysis

- North America dominates the vomiting treatment market with the largest revenue share of 39.2% in 2024, driven by advanced healthcare infrastructure, high adoption of novel antiemetic formulations, and a strong pipeline of supportive drugs in oncology care

- 該地區先進的醫療基礎設施,以及處方藥和非處方止吐藥的廣泛供應,極大地促進了其市場領先地位。患者和醫療保健提供者越來越依賴速效藥物和支持性護理來緩解症狀。

- 此外,強大的研發活動、優惠的報銷政策以及針對化療引起的噁心和暈動病等症狀的宣傳舉措支持了持續的需求,使北美成為嘔吐治療療法創新和消費的領先地區

美國嘔吐治療市場洞察

2024年,美國嘔吐治療市場佔據北美地區最大收入份額,達79.3%,這主要得益於化療引起的噁心、胃腸道疾病以及術後嘔吐等疾病的高發性。完善的醫療基礎設施,以及先進的止吐療法和支持性護理方案的普及,進一步增強了市場需求。此外,老齡人口的增長和處方藥的廣泛使用也推動了市場需求,醫生和患者的意識增強,促進了早期幹預和堅持治療方案。

歐洲嘔吐治療市場洞察

預計歐洲嘔吐治療市場在整個預測期內將以顯著的複合年增長率擴張,這主要歸因於該地區慢性病發病率的上升和住院人數的增加。對護理品質的日益重視、對噁心和嘔吐管理的嚴格治療指南,以及對有效且耐受性良好的止吐藥的日益青睞,都促進了市場的擴張。此外,歐洲醫療保健體系強調循證護理和嘔吐治療的報銷,從而推動了住院和門診患者對嘔吐治療的採用。

英國嘔吐治療市場洞察

英國嘔吐治療市場預計在預測期內將以顯著的複合年增長率增長,這得益於其強大的公共醫療基礎設施,以及止吐藥在癌症治療、妊娠相關噁心和急診環境中的使用日益增多。患者和全科醫生對及時治療嘔吐相關症狀的認識不斷提高,也推動了嘔吐治療市場的需求。此外,嚴格的監管標準和主要製藥公司的參與也促進了嘔吐治療領域的供應和創新。

德國嘔吐治療市場洞察

預計在預測期內,德國嘔吐治療市場將以可觀的複合年增長率擴張,這得益於胃腸道和神經系統疾病(這些疾病通常伴隨嘔吐)的負擔日益加重。德國先進的醫療基礎設施,加上以患者為中心的護理方法和早期診斷實踐,有助於提高治療的普及率。德國強大的製藥生產基礎和研發投入進一步推動了止吐藥領域的創新。

亞太嘔吐治療市場洞察

受傳染病、癌症以及妊娠相關併發症導致嘔吐的日益普及推動,亞太地區嘔吐治療市場在2025年至2032年的預測期內預計以23.2%的複合年增長率保持高速成長。印度、中國和日本等國家的醫療保健可近性、保險覆蓋率和醫療意識的提升,推動了嘔吐治療的普及。此外,醫療基礎設施和製藥業投資的不斷增長,使該地區成為止吐療法的重要成長中心。

日本嘔吐治療市場洞察

由於日本人口老化、慢性病盛行率上升以及醫療保健水平高,日本嘔吐治療市場發展勢頭強勁。對安全、速效止吐藥的需求日益增長,尤其是在腫瘤科、老年病科和外科治療領域。日本注重先進的藥理學研究和數位醫療工具的整合,確保了及時診斷和依從性治療,鞏固了其成熟且創新驅動的市場地位。

印度嘔吐治療市場洞察

2024年,印度嘔吐治療市場佔據亞太地區最大市場份額,這得益於人們意識的提升、快速的城市化進程以及醫療服務可及性的改善。胃腸道感染、瘧疾、懷孕相關噁心的高發生率以及癌症治療週期的延長,推動了止吐藥的需求。在政府健康計劃和國內藥品生產的支持下,非處方和處方嘔吐治療藥物的日益普及,是印度市場強勁表現的關鍵因素。

嘔吐治療市佔率

嘔吐治療產業主要由知名公司主導,包括:

- 輝瑞公司(美國)

- 葛蘭素史克公司(英國)

- 強生服務公司(美國)

- 諾華公司(瑞士)

- 賽諾菲(法國)

- 阿斯特捷利康(英國)

- F. Hoffmann-La Roche Ltd(瑞士)

- 拜耳公司(德國)

- 武田藥品工業株式會社(日本)

- 禮來(美國)

- 艾伯維公司(美國)

- 梯瓦製藥工業股份有限公司(以色列)

- 太陽製藥工業有限公司(印度)

- 雷迪博士實驗室有限公司(印度)

- Cipla Limited (India)

- Aurobindo Pharma Limited (India)

- Torrent Pharmaceuticals Ltd. (India)

- Perrigo Company plc (Ireland)

- Zydus Group (India)

- Lupin (India)

Latest Developments in Global Vomiting Treatment Market

- In April 2024, Pfizer Inc. announced positive overall survival results from its Phase III ECHELON-3 trial, evaluating ADCETRIS plus lenalidomide and rituximab versus lenalidomide and rituximab plus placebo in adult patients with relapsed/refractory diffuse large B-cell lymphoma. The study demonstrated a significant improvement in patient outcomes, positioning the combination as a potential advancement in oncology supportive care

- In March 2024, GlaxoSmithKline (GSK) launched a new over-the-counter (OTC) formulation of Dramamine XR, an extended-release antihistamine aimed at preventing motion sickness and associated vomiting. This product caters to travelers seeking long-lasting relief, reflecting GSK's commitment to expanding its consumer healthcare portfolio

- In February 2024, Johnson & Johnson's Janssen Pharmaceuticals received FDA approval for IMAAVY™ (nipocalimab), a novel FcRn blocker offering long-lasting disease control in the broadest population of people living with generalized myasthenia gravis (gMG). This approval underscores the company's commitment to developing treatments that address unmet medical needs

- In January 2024, Novartis AG entered into a strategic collaboration with Voyager Therapeutics to license novel capsids for use in gene therapy programs. This partnership aims to enhance the delivery of gene therapies, potentially benefiting various therapeutic areas, including those addressing vomiting and nausea

- In December 2023, Sanofi S.A. presented new data at the American Society of Hematology (ASH) 2023, highlighting its commitment to innovation in rare blood diseases and cancers. While not directly related to vomiting treatments, advancements in oncology can have implications for managing chemotherapy-induced nausea and vomiting

SKU-

研究方法

数据收集和基准年分析是使用具有大样本量的数据收集模块完成的。该阶段包括通过各种来源和策略获取市场信息或相关数据。它包括提前检查和规划从过去获得的所有数据。它同样包括检查不同信息源中出现的信息不一致。使用市场统计和连贯模型分析和估计市场数据。此外,市场份额分析和关键趋势分析是市场报告中的主要成功因素。要了解更多信息,请请求分析师致电或下拉您的询问。

DBMR 研究团队使用的关键研究方法是数据三角测量,其中包括数据挖掘、数据变量对市场影响的分析和主要(行业专家)验证。数据模型包括供应商定位网格、市场时间线分析、市场概览和指南、公司定位网格、专利分析、定价分析、公司市场份额分析、测量标准、全球与区域和供应商份额分析。要了解有关研究方法的更多信息,请向我们的行业专家咨询。

可定制

Data Bridge Market Research 是高级形成性研究领域的领导者。我们为向现有和新客户提供符合其目标的数据和分析而感到自豪。报告可定制,包括目标品牌的价格趋势分析、了解其他国家的市场(索取国家列表)、临床试验结果数据、文献综述、翻新市场和产品基础分析。目标竞争对手的市场分析可以从基于技术的分析到市场组合策略进行分析。我们可以按照您所需的格式和数据样式添加您需要的任意数量的竞争对手数据。我们的分析师团队还可以为您提供原始 Excel 文件数据透视表(事实手册)中的数据,或者可以帮助您根据报告中的数据集创建演示文稿。