Asia Pacific Orthopedic Braces And Supports Market

Marktgröße in Milliarden USD

CAGR :

%

USD

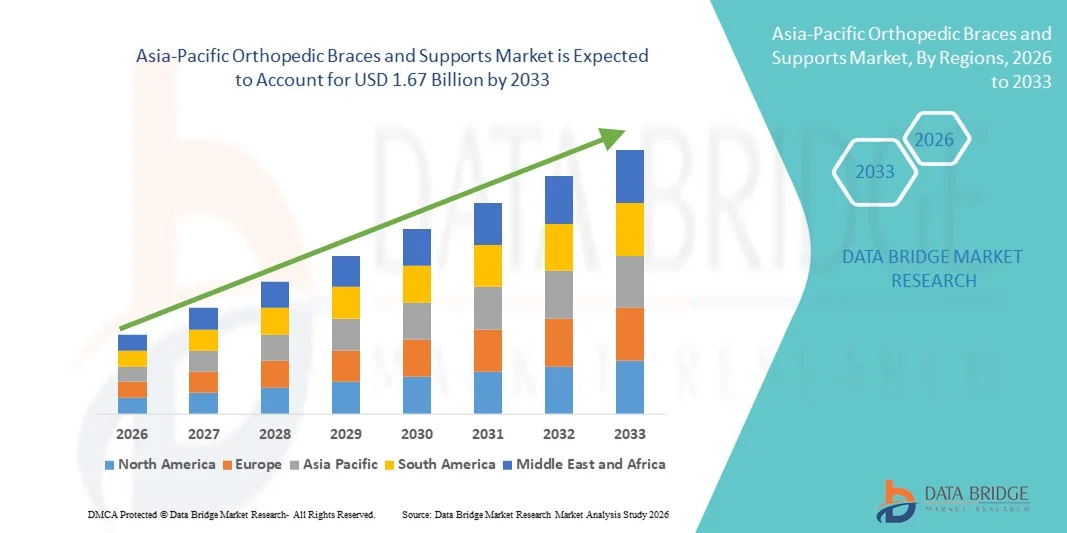

1.07 Billion

USD

1.67 Billion

2025

2033

USD

1.07 Billion

USD

1.67 Billion

2025

2033

| 2026 –2033 | |

| USD 1.07 Billion | |

| USD 1.67 Billion | |

| % | |

|

Marktsegmentierung für orthopädische Bandagen und Stützsysteme im asiatisch-pazifischen Raum nach Produkt (Knöchelbandagen und -stützen, Gehhilfen und Orthesen, Hüft-, Rücken- und Wirbelsäulenbandagen und -stützen, Kniebandagen und -stützen, Schulterbandagen und -stützen, Ellenbogenbandagen und -stützen, Hand-/Handgelenkbandagen und -stützen sowie Gesichtsbandagen und -stützen), Typ (weiche und elastische Bandagen und Stützsysteme, harte und starre Bandagen und Stützsysteme, Gelenkbandagen und -stützen), Anwendung (Prävention, Bänderverletzungen, postoperative Rehabilitation, Arthrose, Kompressionstherapie und Sonstiges), Endnutzer (Krankenhäuser, Kliniken, häusliche Pflege und Sonstiges) – Branchentrends und Prognose bis 2033

Was ist die asiatisch-pazifische orthopädische Klammern und unterstützt Marktgröße und Übersicht

- Die asiatisch-pazifischen orthopädischen Klammern und unterstützt die Marktgröße1,07 Milliarden USD in 2025und wird voraussichtlich erreichen1,67 Milliarden USD bis 2033, beiCAGR von 5,80%während des Prognosezeitraums

- Das Marktwachstum wird größtenteils von der steigenden Prävalenz derMuskel-Skelett-Erkrankungen,zunehmende sportbedingte Verletzungen und eine wachsende geriatrische Bevölkerung in großen Volkswirtschaften wie China, Indien und Japan, was zu einer höheren Nachfrage nach nicht-invasiven orthopädischen Support-Lösungen führt

- Darüber hinaus werden die Sensibilisierung für die vorbeugende Gesundheitsversorgung, die Verbesserung des Zugangs zu Rehabilitationsdiensten und die technologischen Fortschritte bei leichten, langlebigen und anpassbaren Strebenmaterialien orthopädische Streben und Unterstützungen als wesentliche Mobilitäts- und Erholungshilfen geschaffen. Diese konvergierenden Faktoren beschleunigen die Produktakzeptanz in Krankenhäusern, Kliniken und Heimpflege-Einstellungen, wodurch das Wachstum der Industrie deutlich erhöht wird

Asien-Pazifik Orthopädische Klammern und unterstützt Marktanalyse

- Orthopädische Stützen und Stützen, entwickelt, um verletzte oder geschwächte Gelenke und Muskeln zu stabilisieren, zu schützen und zu rehabilitieren, sind in Krankenhäusern, orthopädischen Kliniken, Sportmedizin Zentren und Heimpflege-Einstellungen in China aufgrund ihrer Wirksamkeit bei Schmerzlinderung, postoperativer Erholung und Verletzungsvorbeugung

- Die eskalierende Nachfrage nach orthopädischen Stützen und Stützen in China wird in erster Linie durch die steigende Prävalenz vonosteoarthritisund andere Muskel-Skelett-Erkrankungen, zunehmende Sportbeteiligung, eine schnell alternde Bevölkerung und wachsendes Bewusstsein für nicht-invasive Behandlungsalternativen

- China dominierte die asiatisch-pazifischen orthopädischen Klammern und unterstützt den Markt mit dem größten Umsatzanteil von 38,6% im Jahr 2025, unterstützt von seiner großen Patientenpopulation, Erweiterung der Gesundheitsinfrastruktur und steigenden Gesundheitsausgaben, mit einer starken Nachfrage in Tier-1- und Tier-2-Städten, wo der Zugang zu fortgeschrittenen orthopädischen Pflege- und Rehabilitationsdienstleistungen verbessert

- Indien wird voraussichtlich das am schnellsten wachsende Land in den orthopädischen Stämmen Asiens sein und unterstützt den Markt während der Prognosezeit durch steigende Gesundheitsinvestitionen, Ausweitung privater Krankenhausnetze, steigende Sportverletzungen und wachsendes Bewusstsein für erschwingliche orthopädische Rehabilitationslösungen

- Das Segment Kniestützen und Stützen dominierte die asiatisch-pazifischen orthopädischen Klammern und unterstützt den Markt mit einem Marktanteil von 41,3% im Jahr 2025, angetrieben durch die hohe Häufigkeit von Knie-Arthritis, sportbedingten Ligamentverletzungen und wachsende Nachfrage nach postchirurgischen Rehabilitations- und älteren Mobilitätsunterstützungslösungen

Report Scope und Asien-Pazifik Orthopädische Klammern und unterstützt Marktsegmentierung

|

Attribute |

Asia-Pazifische Orthopädische Klammern und unterstützt Schlüsselmarkt Einblicke |

|

Verdeckte Segmente |

|

|

Überarbeitete Länder |

Asien-Pazifik

|

|

Key Market Players |

|

|

Marktmöglichkeiten |

|

|

Daten Infos zum Wert hinzugefügt |

|

Was ist der Haupttrend im asiatisch-pazifischen Orthopädischen Braces and Supports Market

Technologische Entwicklung in Leicht- und Smart Rehabilitationslösungen

- Ein bedeutender und beschleunigender Trend in den asiatisch-pazifischen orthopädischen Klammern und unterstützt den Markt, ist die zunehmende Einführung von leichten, atmungsaktiven und ergonomisch gestalteten Materialien in Kombination mit aufstrebenden intelligenten Rehabilitationstechnologien. Diese Entwicklung verbessert den Patientenkomfort, die Compliance und die Behandlungsergebnisse in verschiedenen Pflegeeinstellungen deutlich.

- So stellen mehrere regionale und globale Hersteller 3D-gestrickte Knie- und Knöchelstützen vor, die eine gezielte Kompression bieten und gleichzeitig Flexibilität und Haltbarkeit verbessern. Ebenso gewinnen Funktionsstreben, die mit verstellbaren Stützsystemen integriert sind, in postchirurgischen und sportlichen Verletzungsrettungsprogrammen Traktion.

- Die Integration von sensorbasierten Überwachungssystemen in fortgeschrittenen orthopädischen Streben ermöglicht die Verfolgung von Gelenkbewegungen, Rehabilitationsfortschritten und Patientenhaftung an vorgeschriebener Therapie. Beispielsweise können bestimmte smarte Kniesträhnen Mobilitätsdaten an vernetzte mobile Anwendungen übertragen, so dass die Kliniker die Wiederherstellung remote bewerten und Behandlungspläne entsprechend anpassen können. Darüber hinaus reduzieren leichte Verbundwerkstoffe Beschwerden bei längerem Gebrauch und fördern eine bessere Patientenkonformität

- Die nahtlose Einbindung orthopädischer Unterstützungen in hausbasierte Rehabilitationsprogramme erleichtert die dezentrale Betreuung und reduziert Krankenhausbesuche. Durch digitale Plattformen können Patienten mit Physiotherapeuten koordinieren, während sie verschriebene Klammern verwenden, wodurch ein effizienteres und vernetztes Erholungs-Ökosystem entsteht

- Dieser Trend hin zu geduldig-zentrischen, technologieverfügbaren orthopädischen Lösungen macht die Erwartungen an die Muskelpflege grundlegend neu. Daher entwickeln Unternehmen, die in Asia-Pacific tätig sind, anpassbare Klammern mit verbesserter Haltbarkeit, atmungsaktiven Stoffen und intelligente Überwachungskompatibilität, um den wachsenden Anforderungen an klinische und Verbraucher gerecht zu werden

- Die Nachfrage nach technologisch fortschrittlichen, komfortablen und digital integrierten orthopädischen Stützen und Stützen wächst rasant in Krankenhäusern, Sportanlagen und Pflegeumgebungen, da Patienten zunehmend Mobilität, Komfort und schnellere Rehabilitationsergebnisse priorisieren

- Erweiterung von E-Commerce- und Direkt-to-Consumer-Vertriebskanälen in ganz Asien-Pazifik verbessert die Produktzuverlässigkeit und ermöglicht es Patienten, Features, Preise und klinische Vorteile effizienter zu vergleichen

Asien-Pazifik Orthopädische Klammern und unterstützt Marktdynamik

Fahrer

Musculoskeletale Disorder und die Ausweitung der Geriatric Bevölkerung

- Die zunehmende Prävalenz von Osteoarthritis, Ligamentverletzungen und anderen muskuloskeletalen Störungen, verbunden mit der schnellen Expansion der älteren Bevölkerung in Asien-Pazifik, ist ein bedeutender Treiber für die erhöhte Nachfrage nach orthopädischen Streben und Stützen

- So unterstützen z.B. steigende Gesundheitsinvestitionen in Ländern wie China und Indien einen verbesserten Zugang zu orthopädischen Verfahren und postoperativen Rehabilitationsprodukten, wodurch die Markterweiterung während der Prognosezeit angeregt wird.

- Da das Bewusstsein für nicht-invasive Behandlungsoptionen wächst, entscheiden sich die Patienten zunehmend für Klammern und Unterstützungen für Schmerzmanagement, gemeinsame Stabilisierung und Verletzungsprävention und bieten eine praktische Alternative zu chirurgischen Eingriffen in milden bis moderaten Fällen

- Die zunehmende Sportkultur, die Zunahme von Arbeitsplatzverletzungen und die stärkere Beteiligung an körperlichen Aktivitäten machen orthopädisch einen wesentlichen Bestandteil der präventiven und therapeutischen Betreuung in städtischen Bevölkerungsgruppen.

- Die Verfügbarkeit unterschiedlicher Produktkategorien, einschließlich Knie-, Knöchel-, Rücken- und Schulterstützen, sowie die Verteilung über Krankenhäuser, Apotheken und E-Commerce-Plattformen, ist die Förderung der Adoption in den entwickelten und Schwellenländern in der Region

- Regierungsinitiativen zur Stärkung des Inlandsmedizinisches GerätHerstellung unterstützen die lokale Produktion und reduzieren die Abhängigkeit von den Importen, wodurch die Zuverlässigkeit der Lieferkette erhöht

- Die Erhöhung der Durchdringung und Erstattung von Krankenversicherungen für orthopädische Rehabilitationsprodukte in ausgewählten Ländern Asien-Pazifik unterstützen das anhaltende Nachfragewachstum

Zurückhaltung/Challenge

Produkt-Affordability Constraints und Regulatory Compliance Hurdles

- Die hohen Kosten für fortgeschrittene orthopädische Streben und die unterschiedlichen Regulierungsstandards in Asien-Pazifik-Ländern stellen große Herausforderungen für eine breitere Marktdurchdringung dar. Prämien- und technologisch verstärkte Streben können für preisempfindliche Bevölkerungsgruppen in den Entwicklungsmärkten nicht beeinträchtigt werden

- So können z.B. strenge Medizingeräte-Zulassungsverfahren und unterschiedliche Rückerstattungsrahmen in Ländern Produkteinführungen verzögern und die Zugänglichkeit bestimmter Patientengruppen begrenzen

- Die Bewältigung von Erreichbarkeitsproblemen durch lokale Fertigungs-, Kostenoptimierungsstrategien und eine erweiterte Versicherungsabdeckung sind entscheidend für die Verbesserung der Produktverfügbarkeit. Unternehmen konzentrieren sich zunehmend auf wertbasierte Produktlinien, um die Bevölkerung mit mittlerem Einkommen unter Beibehaltung von Qualitäts- und Haltbarkeitsstandards zu versorgen. Darüber hinaus kann ein begrenztes Bewusstsein in ländlichen Gebieten in Bezug auf die ordnungsgemäße Verwendung der Klammern und Vorteile die Adoptionsraten trotz klinischer Notwendigkeit einschränken

- Während sich die Infrastruktur im Gesundheitswesen verbessert, können die Unterschiede zwischen städtischen und ländlichen Regionen den Zugang zu fortschrittlichen orthopädischen Rehabilitationsprodukten behindern. Veränderungen in Preis- und Vertriebsnetzen beeinflussen die Marktreichweite und die Patientenaufnahme weiter

- Die Überwindung dieser Herausforderungen durch eine vereinfachte Regulierungsharmonisierung, eine verstärkte Erstattungsunterstützung, Initiativen zur Ausbildung von Patienten und eine Erweiterung erschwinglicher Produktportfolios wird entscheidend sein, um das langfristige Marktwachstum in ganz Asien-Pazifik zu erhalten.

- Intensiver Preiswettbewerb unter den inländischen und internationalen Herstellern kann Gewinnmargen unter Druck setzen und Investitionen in Forschung und Produktinnovation begrenzen

- Das Risiko einer unsachgemäßen Leimung oder einer unsupervisierten Nutzung ohne professionelle Beratung kann die Produktwirksamkeit verringern, potenziell die Patientenergebnisse und die Markenglaubwürdigkeit beeinflussen

Asien-Pazifik Orthopädische Klammern und unterstützt Marktumfang

Der Markt wird auf Basis von Produkt, Typ, Anwendung und Endbenutzer segmentiert.

- Nach Produkt

Auf Basis des Produkts wird der asiatisch-pazifische orthopädische Stützen- und Stützenmarkt zu Knöchelstützen, Fußspazierern und Kiefern, Hüft-, Rücken- und Rückenstützen, Kniestützen und Stützen, Schulterstützen und Stützen, Ellbogenstützen und Stützen, Hand- und Handgelenksstützen und Gesichtsstützen segmentiert. Das Segment Kniestützen und Stützen dominierte den Markt mit dem größten Umsatzanteil von 41,3% im Jahr 2025, vor allem durch die hohe Prävalenz von Knie-Osteoarthritis, Bänderrissen und sportbedingten Verletzungen in China, Japan und Indien. Die alternde Bevölkerung und steigende Fettleibigkeitsraten haben deutlich erhöhte kniebedingte muskuloskeletale Bedingungen, die Segmentnachfrage stärken. Darüber hinaus sind Kniesträhnen für die postoperative Rehabilitation nach ACL und Meniskuschirurgie weit vorgeschrieben. Ihre breite Verfügbarkeit in Krankenhäusern, Apotheken und Online-Plattformen verstärkt die Marktführerschaft. Kontinuierliche Produktinnovation, einschließlich verstellbarer und leichter Designs, unterstützt nachhaltige Adoption.

Die Schulterstützen und Stützen Segment wird erwartet, dass die schnellste Wachstumsrate von 2026 bis 2033, durch steigende Sportbeteiligung, zunehmende Fälle von Rotator Manschettenverletzungen, und das Bewusstsein in Bezug auf die früheste orthopädische Intervention. Die wachsende Urbanisierung und Fitness-Kultur in Großstädten tragen zu Schulter- und Verletzungsfällen bei. Technologische Fortschritte bei druck- und haltungskorrektiven Schulterstützen erhöhen die Produktwirksamkeit. Erhöhter Zugang zu Physiotherapie-Services und Rehabilitationszentren unterstützt die Segmenterweiterung. Darüber hinaus beschleunigt die Nachfrage nach nicht-invasiven Erholungslösungen die Übernahme von Berufs- und Sportlern.

- Typ

Der Markt wird auf Basis des Typs zu weichen und elastischen Stützen und Stützen, harten und starren Stützen und Stützen sowie gelenkigen Stützen und Stützen segmentiert. Das Segment weiche und elastische Klammern und Stützen hielt den größten Marktanteil im Jahr 2025 aufgrund ihrer Erschwinglichkeit, ihres Komforts und des weit verbreiteten Einsatzes im milden Verletzungsmanagement und der vorbeugenden Pflege. Diese Klammern werden häufig für die frühesteoarthritis, Muskelgewebe und tägliche Gelenkunterstützung empfohlen. Ihre Leichtbaustruktur und atmungsaktive Materialien verbessern die Patientenkonformität für den langfristigen Gebrauch. Einfache Verfügbarkeit durch Einzelhandels-Apotheken und E-Commerce-Plattformen verstärkt ihre Marktdurchdringung. Die zunehmende Vorliebe für nicht-wulstige und flexible orthopädische Hilfsmittel treibt die Segmentherrschaft weiter voran.

Das Segment Scharnierstützen und Stützen wird von 2026 bis 2033 am schnellsten CAGR erleben, angetrieben durch die zunehmende Nachfrage nach fortschrittlichen Stabilisierungslösungen bei Bänderverletzungen und nachchirurgische Erholung. Gespannte Streben sorgen für eine kontrollierte Gelenkbewegung und verhindern eine übermäßige Belastung, wodurch sie für moderate bis schwere Verletzungen geeignet sind. Sportverletzungen und orthopädische chirurgische Verfahren in ganz Asien-Pazifik erhöhen die Nachfrage nach diesen spezialisierten Produkten. Technologische Verbesserungen in verstellbaren Scharniersystemen verbessern Anpassung und Patientenergebnisse. Das zunehmende Bewusstsein der orthopädischen Spezialisten für fortschrittliche Spannlösungen trägt weiter zum Segmentwachstum bei.

- Anwendung

Auf der Grundlage der Anwendung wird der Markt in präventive Betreuung, Ligamentverletzung, postoperative Rehabilitation, Osteoarthritis, Kompressionstherapie und andere segmentiert. Das Segment Osteoarthritis dominierte den Markt im Jahr 2025 aufgrund der schnell alternden Bevölkerung und des zunehmenden Auftretens von degenerativen Gelenkstörungen in der gesamten Region. Länder wie Japan und China berichten hohe Raten von altersbedingten Knie- und Hüftdegenerationen, was eine deutliche Auslastung der Streben bedeutet. Orthopädische Stützen sind häufig vorgeschrieben, um Schmerzen zu reduzieren, Gelenkausrichtung zu verbessern und chirurgische Eingriffe zu verzögern. Das wachsende Bewusstsein für konservative Therapieansätze beschleunigt die Nachfrage weiter. Die Ausweitung der geriatrischen Betreuungs- und Rehabilitationsinfrastruktur unterstützt auch eine nachhaltige Segmentführung.

Das postoperative Reha-Segment wird während der Prognosezeit mit dem schnellsten Tempo wachsen, unterstützt durch steigende Mengen an orthopädischen Operationen und verbesserten Gesundheitszugang. Die Erhöhung der Verfügbarkeit minimal invasiver Verfahren erhöht die regenerationsfokussierte Adoption. Strukturierte Rehabilitationsprogramme in Krankenhäusern und Kliniken fördern den konsequenten Einsatz orthopädischer Unterstützungen. Technologische Fortschritte, die eine bessere Immobilisierung und Erholungsverfolgung ermöglichen, stärken die Nachfrage weiter. Steigende Patientenpräferenz für hausbasierte Erholungslösungen Zusätzlich beschleunigt das Segmentwachstum.

- Mit dem Endbenutzer

Auf der Grundlage des Endbenutzers wird der Markt in Krankenhäuser, Kliniken, Heimgesundheit und andere segmentiert. Das Segment Krankenhäuser entfiel auf den größten Umsatzanteil im Jahr 2025 aufgrund eines hohen Patientenzuflusses für orthopädische Operationen, Traumamanagement und fortgeschrittene Bewegungsapparate. Krankenhäuser bleiben der Hauptpunkt der Verschreibung für Stützen und Stützen, insbesondere für komplexe und postchirurgische Fälle. Die Verfügbarkeit von spezialisierten orthopädischen Fachleuten und diagnostischen Einrichtungen unterstützt die Segmentherrschaft. Bulk-Beschaffungspraktiken und etablierte Lieferantenbeziehungen stärken den Vertrieb im Krankenhaus weiter. Die steigenden Investitionen in die Infrastruktur der Tertiärversorgung in ganz Asien-Pazifik bleiben weiterhin gefragt.

Das Home Healthcare-Segment wird erwartet, dass das schnellste Wachstum von 2026 bis 2033, angetrieben durch die zunehmende Präferenz für kostengünstige und komfortable Rehabilitationslösungen. Die Übernahme von Telegesundheit und die Verfügbarkeit von Fernphysiotherapie-Beratungen unterstützen den Einsatz von Zahnseen zu Hause. Ältere Patienten bevorzugen zunehmend häusliche Mobilitätsunterstützung, um häufige Krankenhausbesuche zu vermeiden. Die Erweiterung von E-Commerce-Vertriebskanälen verbessert die Produktverfügbarkeit für Heimnutzer. Darüber hinaus beschleunigt die zunehmende Sensibilisierung für präventive orthopädische Betreuung die Segmenterweiterung in Heimeinstellungen weiter.

Asien-Pazifik Orthopädische Klammern und unterstützt Markt Regionalanalyse

- China dominierte die asiatisch-pazifischen orthopädischen Klammern und unterstützt den Markt mit dem größten Umsatzanteil von 38,6% im Jahr 2025, unterstützt von seiner großen Patientenpopulation, Erweiterung der Gesundheitsinfrastruktur und steigenden Gesundheitsausgaben, mit einer starken Nachfrage in Tier-1- und Tier-2-Städten, wo der Zugang zu fortgeschrittenen orthopädischen Pflege- und Rehabilitationsdienstleistungen verbessert

- Patienten in der Region schätzen die Erschwinglichkeit, Verfügbarkeit und klinische Wirksamkeit von orthopädischen Klammern und Unterstützung für Schmerzmanagement, postoperative Erholung und Verletzungsvorbeugung sowohl in der Stadt als auch in der Halbstadt.

- Diese weit verbreitete Adoption wird durch eine schnell alternde Bevölkerung, Verbesserung der Gesundheitsinfrastruktur, Erhöhung der Gesundheitsausgaben und wachsendes Bewusstsein in Bezug auf nicht-invasive Muskel- und Skelettbehandlungsoptionen unterstützt, orthopädische Klammern zu etablieren und unterstützt als wesentliche Mobilitäts- und Rehabilitationslösungen in Krankenhäusern, Kliniken und Heimpflege-Einstellungen

Die China Orthopädische Halterungen und unterstützt Marktaufsicht

Die China orthopädischen Klammern und unterstützt den Markt gefangen genommen den größten Umsatzanteil im Jahr 2025 in Asien-Pazifik, durch die steigende Prävalenz von Osteoarthritis, zunehmende Sportverletzungen und eine rasch expandierende geriatrische Bevölkerung. Patienten priorisieren zunehmend nicht-invasive Schmerzmanagement- und Mobilitätsverbesserungslösungen durch klinisch empfohlene Streben und Unterstützungen. Die wachsende Vorliebe für die häusliche Rehabilitation, kombiniert mit der Erweiterung der Krankenhausinfrastruktur und orthopädischen Spezialzentren, fördert das Marktwachstum. Darüber hinaus tragen steigende Gesundheitsausgaben und staatliche Unterstützung bei der Inlandsproduktion von Medizinprodukten maßgeblich zur Expansion des Marktes bei.

Japan Orthopädische Halterungen und unterstützt Marktaufsicht

Die japanischen orthopädischen Streben und unterstützen den Markt wird in der gesamten Vorausschätzungsperiode mit einem beträchtlichen CAGR ausbauen, vor allem durch die alternde Bevölkerung des Landes und die hohe Häufigkeit degenerativer Gelenkerkrankungen. Das zunehmende Bewusstsein für präventive orthopädische Betreuung und strukturierte Rehabilitationsprogramme fördert die Adoption. Die japanischen Verbraucher legen großen Wert auf Qualität, Komfort und technologisch fortschrittliche Gesundheitsprodukte, die Innovation in Leichtbau- und Ergonomie-Sprechdesigns fördern. Die Integration von Rehabilitationshilfen innerhalb der hauseigenen Gesundheitsdienste unterstützt die stetige Marktentwicklung über Wohn- und klinische Einstellungen hinweg.

Indien Orthopädische Stützen und unterstützt Markt Insight

Die indischen orthopädischen Klammern und Stützen Markt wird erwartet, in einem bemerkenswerten CAGR während der Prognosezeit zu wachsen, angetrieben durch steigende Fälle von Muskel-Skelett-Verletzungen, die Ausweitung der Sportbeteiligung und die Verbesserung der gesundheitlichen Zugänglichkeit. Darüber hinaus ist die zunehmende Sensibilisierung für preisgünstige orthopädische Rehabilitationslösungen eine ermutigende Adoption unter den mittleren Einkommensgruppen. Indiens wachsendes Netzwerk von privaten Krankenhäusern, Physiotherapie-Zentren und e-Commerce medizinischen Versorgungsplattformen wird erwartet, dass das Marktwachstum weiter anregen. Regierungsinitiativen zur Stärkung der heimischen Medizinprodukteproduktion unterstützen die langfristige Expansion weiter.

Australien Orthopädische Halterungen und unterstützt Marktaufsicht

Die orthopädischen Strebe und Stützen Australiens werden voraussichtlich während des Prognosezeitraums mit einer beträchtlichen CAGR ausbauen, die durch eine starke Gesundheitsinfrastruktur und eine zunehmende Nachfrage nach Sportverletzungsmanagementlösungen bewirtschaftet wird. Australiens aktive Sportkultur und alterndes demografisches Profil fördern die stetige Adoption von Knie-, Knöchel- und Schulterstützen. Das zunehmende Bewusstsein für die vorbeugende Pflege und die postoperative Rehabilitation erhöht die Produktauslastung in Krankenhäusern und ambulanten Einstellungen. Die Vorliebe für hochwertige, klinisch zugelassene orthopädische Produkte richtet sich an die Erwartungen der Verbraucher an Sicherheit und Leistung.

Welche sind die Top-Unternehmen im asiatisch-pazifischen Orthopädischen Braces und Support-Markt

Die Asia-Pacific Orthopedic Braces and Supports Industrie wird in erster Linie von etablierten Unternehmen geleitet, darunter:

- DJO, LLC (USA)

- Össur hf. (Island)

- Smith & Nephew (USA)

- DeRoyal Industries (USA)

- Bauerfeind AG (Deutschland)

- Orthofix Medical Inc. (USA)

- Zimmer Biomet (USA)

- 3M (US)

- Trulife (Kanada)

- Thuasne Group (Frankreich)

- medi GmbH & Co. KG (Deutschland)

- Ottobock SE & Co. KGaA (Deutschland)

- CONMED Corporation (USA)

- MicroPort Orthopedics, Inc. (China)

- Aspen Medical Products (US)

- Bird & Cronin, LLC (USA)

- McDavid Inc. (USA)

- Mueller Sports Medicine, Inc. (USA)

- BORT Medical GmbH (Deutschland)

- ALCARE Co., Ltd. (Japan)

Was sind die jüngsten Entwicklungen im asiatisch-pazifischen Orthopädischen Braces and Supports Market

- Im September 2025 erweiterte G-Medics Korea seine globale Reichweite mit seinem biologisch abbaubaren Harz orthopädischen Gussprodukt BONGIPS, Vorbereitung auf den Export nach Südostasien, Europa und Nordamerika nach starker Inlandsaufnahme und klinischer Anerkennung

- Im September 2025 wurde das erste SkyWalkerTM Orthopädische Robotik-System in Südasien zur Verbesserung der Kniegelenkausrichtung und der Erholungsergebnisse mit Roboterpräzision im **Yenepoya Specialty Hospital in Mangaluru, Indien, gestartet, um die klinischen Fähigkeiten für gemeinsame Verfahren zu verbessern, die oft folgende orthopädische Unterstützung und Rehabilitationseinrichtungen erfordern

- Im September 2025 veranstalteten Apollo Hospitals das Advanced Orthopaedics Symposium 2025 in Hyderabad, das über 250 orthopädische Chirurgen versammelte, um Fortschritte in der Kniepflege, der gemeinsamen Konservierungstechnologien, der Robotik und der digitalen Diagnostik zu präsentieren, die den klinischen Innovationsschwerpunkt der Region im Bewegungsapparat hervorheben

- Im März 2025 starteten Apollo Hospitals das Apollo Joint Preservation Program in Chennai, eine Initiative zur frühzeitigen Intervention, personalisierte Behandlungspläne und Rehabilitationsleistungen für Gelenkschmerzen, Arthritis, Ligamentverletzungen und andere muskuloskeletale Bedingungen zur Erhaltung der gemeinsamen Gesundheit und zur Vermeidung oder Verzögerung der Operation

- Im März 2025 startete Apollo Hospitals bundesweit sein „Joint Preservation Programm“ in Indien, das sich auf umfassende Behandlungswege wie Rehabilitation, Physiotherapie und Lifestyle-Unterstützung für Patienten mit Gelenkschmerzen und damit verbundenen Erkrankungen konzentrierte.

SKU-

Erhalten Sie Online-Zugriff auf den Bericht zur weltweit ersten Market Intelligence Cloud

- Interaktives Datenanalyse-Dashboard

- Unternehmensanalyse-Dashboard für Chancen mit hohem Wachstumspotenzial

- Zugriff für Research-Analysten für Anpassungen und Abfragen

- Konkurrenzanalyse mit interaktivem Dashboard

- Aktuelle Nachrichten, Updates und Trendanalyse

- Nutzen Sie die Leistungsfähigkeit der Benchmark-Analyse für eine umfassende Konkurrenzverfolgung

Forschungsmethodik

Die Datenerfassung und Basisjahresanalyse werden mithilfe von Datenerfassungsmodulen mit großen Stichprobengrößen durchgeführt. Die Phase umfasst das Erhalten von Marktinformationen oder verwandten Daten aus verschiedenen Quellen und Strategien. Sie umfasst die Prüfung und Planung aller aus der Vergangenheit im Voraus erfassten Daten. Sie umfasst auch die Prüfung von Informationsinkonsistenzen, die in verschiedenen Informationsquellen auftreten. Die Marktdaten werden mithilfe von marktstatistischen und kohärenten Modellen analysiert und geschätzt. Darüber hinaus sind Marktanteilsanalyse und Schlüsseltrendanalyse die wichtigsten Erfolgsfaktoren im Marktbericht. Um mehr zu erfahren, fordern Sie bitte einen Analystenanruf an oder geben Sie Ihre Anfrage ein.

Die wichtigste Forschungsmethodik, die vom DBMR-Forschungsteam verwendet wird, ist die Datentriangulation, die Data Mining, die Analyse der Auswirkungen von Datenvariablen auf den Markt und die primäre (Branchenexperten-)Validierung umfasst. Zu den Datenmodellen gehören ein Lieferantenpositionierungsraster, eine Marktzeitlinienanalyse, ein Marktüberblick und -leitfaden, ein Firmenpositionierungsraster, eine Patentanalyse, eine Preisanalyse, eine Firmenmarktanteilsanalyse, Messstandards, eine globale versus eine regionale und Lieferantenanteilsanalyse. Um mehr über die Forschungsmethodik zu erfahren, senden Sie eine Anfrage an unsere Branchenexperten.

Anpassung möglich

Data Bridge Market Research ist ein führendes Unternehmen in der fortgeschrittenen formativen Forschung. Wir sind stolz darauf, unseren bestehenden und neuen Kunden Daten und Analysen zu bieten, die zu ihren Zielen passen. Der Bericht kann angepasst werden, um Preistrendanalysen von Zielmarken, Marktverständnis für zusätzliche Länder (fordern Sie die Länderliste an), Daten zu klinischen Studienergebnissen, Literaturübersicht, Analysen des Marktes für aufgearbeitete Produkte und Produktbasis einzuschließen. Marktanalysen von Zielkonkurrenten können von technologiebasierten Analysen bis hin zu Marktportfoliostrategien analysiert werden. Wir können so viele Wettbewerber hinzufügen, wie Sie Daten in dem von Ihnen gewünschten Format und Datenstil benötigen. Unser Analystenteam kann Ihnen auch Daten in groben Excel-Rohdateien und Pivot-Tabellen (Fact Book) bereitstellen oder Sie bei der Erstellung von Präsentationen aus den im Bericht verfügbaren Datensätzen unterstützen.