世界の鼻ポリープ治療薬市場の規模、シェア、トレンド分析レポート

Market Size in USD Billion

CAGR :

%

USD

3.28 Billion

USD

5.07 Billion

2025

2033

USD

3.28 Billion

USD

5.07 Billion

2025

2033

| 2026 –2033 | |

| USD 3.28 Billion | |

| USD 5.07 Billion | |

| % | |

|

世界の鼻ポリープ治療薬市場のセグメンテーション:薬剤別(鼻腔内コルチコステロイド、経口および注射用コルチコステロイド、デュピクセント、その他)、投与経路別(経口、非経口、鼻腔内、その他)、エンドユーザー別(病院、在宅医療、専門クリニック、その他)、流通チャネル別(病院薬局、オンライン薬局、小売薬局)- 業界動向と2033年までの予測

鼻ポリープ治療薬市場規模

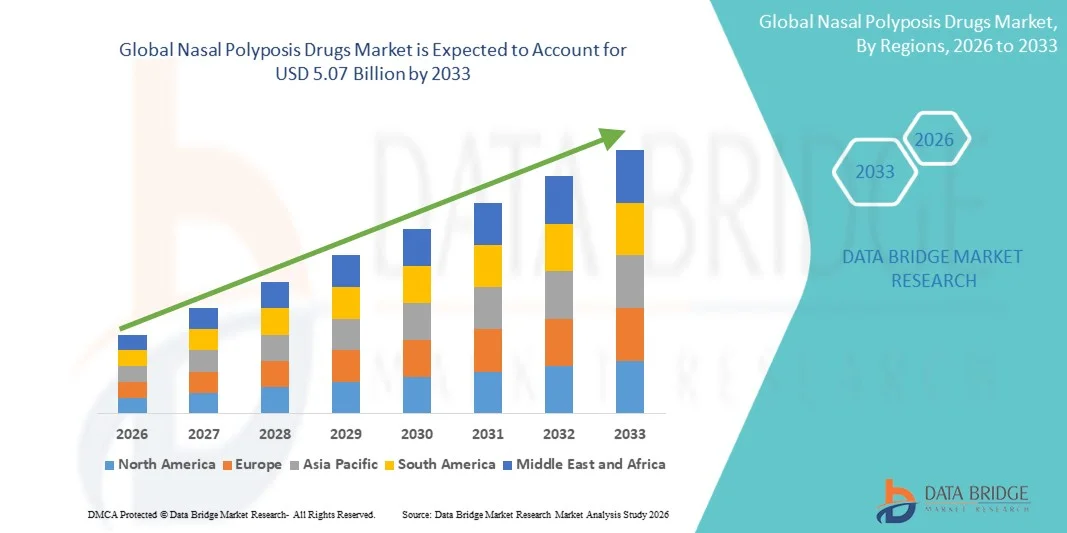

- 世界の鼻ポリープ治療薬市場規模は、2025年には32億8,000万米ドルと評価され、予測期間中の年平均成長率(CAGR)5.60%で、2033年には50億7,000万米ドル に達すると予測されている。

- 市場の成長は主に、鼻ポリープを伴う慢性副鼻腔炎(CRSwNP)の罹患率の上昇、効果的な治療選択肢に関する認識の高まり、および生物学的製剤やコルチコステロイド療法の拡大によって牽引されている。

- さらに、非外科的・低侵襲治療に対する患者の嗜好の高まりと、世界的な医療アクセスの向上により、鼻ポリープ治療薬は慢性副鼻腔疾患の管理に不可欠なものとして位置づけられています。これらの要因が相まって、市場拡大を加速させ、この分野の持続的な成長を牽引しています。

鼻ポリープ治療薬市場分析

- 鼻ポリープ症治療薬(鼻腔内ステロイド、経口および注射用ステロイド、デュピクセント、その他の新規治療法など)は、炎症を軽減し、鼻腔気流を改善し、外科的介入の必要性を最小限に抑える効果があるため、鼻ポリープを伴う慢性副鼻腔炎(CRSwNP)の管理においてますます重要になっている。

- 鼻ポリープ治療薬の需要増加は、主に慢性副鼻腔炎(CRSwNP)の罹患率の上昇、非外科的治療選択肢への認識の高まり、そして生物学的製剤やコルチコステロイドなどの標的療法の普及拡大によって促進されており、これらの治療法はより優れた疾患コントロールを提供する。

- 北米は、高い患者意識、高度な医療インフラ、デュピクセントなどの治療法の早期導入に支えられ、2025年には38.7%という最大の収益シェアで鼻ポリープ治療薬市場を席巻した。米国市場では、早期介入を重視する臨床ガイドラインに牽引され、新規コルチコステロイドおよび生物製剤の処方量が著しく増加した。

- アジア太平洋地域は、医療へのアクセス向上、慢性副鼻腔炎(CRSwNP)の罹患率上昇、都市部の医療施設における先進治療法の普及拡大により、予測期間中に鼻ポリープ治療薬市場で最も急速に成長する地域になると予想されています。

- 鼻腔内コルチコステロイド分野は、その有効性、投与の容易さ、軽度から中等度の慢性副鼻腔炎(CRSwNP)患者に対する第一選択療法としての広範な推奨により、2025年には市場シェア41.3%で鼻ポリープ治療薬市場を牽引しました。

レポートの範囲と鼻ポリープ治療薬市場のセグメンテーション

|

属性 |

鼻ポリープ治療薬の主要市場動向 |

|

対象分野 |

|

|

対象国 |

北米

ヨーロッパ

アジア太平洋

中東およびアフリカ

南アメリカ

|

|

主要市場プレーヤー |

|

|

市場機会 |

|

|

付加価値データ情報セット |

Data Bridge Market Researchが作成した市場レポートには、市場価値、成長率、セグメンテーション、地理的範囲、主要企業などの市場シナリオに関する洞察に加え、専門家による詳細な分析、患者疫学、パイプライン分析、価格分析、規制枠組みも含まれています。 |

鼻ポリープ治療薬市場の動向

「生物製剤と標的療法の出現」

- 世界の鼻ポリープ治療薬市場における重要かつ加速的な傾向の一つは、デュピクセントなどの生物学的製剤の採用拡大である。これらの製剤は、重度の慢性副鼻腔炎(CRSwNP)症例に対する標的治療を提供し、繰り返しの外科的介入の必要性を軽減する。

- 例えば、デュピクセントは、標準的なコルチコステロイド療法に反応しない患者において、ポリープのサイズを縮小し、鼻腔気流を改善する効果を示しており、重症例に対する生物学的製剤の優先的な選択肢としての地位を確立している。

- 鼻腔内コルチコステロイドの先進的な製剤も開発されており、投与効率と患者の服薬遵守率を高め、全身曝露を最小限に抑えつつ局所的な有効性を最大限に高めることを目指している。

- 生物学的製剤と最適化されたコルチコステロイド療法は、従来の治療法と並んで治療プロトコルにますます組み込まれており、医師は疾患の重症度と患者の反応に基づいて介入を調整することができる。

- 精密医療と標的型薬物送達へのこうした傾向は、患者の期待と治療パラダイムを再構築し、製薬会社に製剤、投与量、併用療法における革新を促している。

- 先進国市場と新興国市場の両方で、効果的で低侵襲かつ個別化された鼻ポリープ治療への需要が急速に高まっている。患者は副作用の少ない長期的な疾患コントロールを求めている。

- 低分子化合物や次世代バイオ医薬品を含む新規治療法の研究開発への投資増加は、さらなるイノベーションを促進し、慢性副鼻腔炎(CRSwNP)患者の治療選択肢を拡大することが期待される。

鼻ポリープ治療薬市場の動向

ドライバ

「慢性副鼻腔炎(鼻ポリープ合併)の罹患率増加と患者の意識向上」

- 慢性副鼻腔炎(鼻ポリープを伴う)(CRSwNP)の罹患率の上昇と、利用可能な治療選択肢に対する認識の高まりが、鼻ポリープ治療薬の需要増加の大きな要因となっている。

- 例えば、米国で行われた研究では、成人人口の4%が慢性副鼻腔炎(CRSwNP)に罹患しており、第一選択薬および進行期治療薬としてコルチコステロイドや生物学的製剤の処方が増加していることが明らかになった。

- 患者教育イニシアチブや擁護プログラムの拡大により、非外科的治療の選択肢についての認識が高まり、早期介入や処方された治療法の遵守が促進されている。

- 医療従事者は、患者の治療成績を向上させ、再発率を低下させるために、生物学的製剤と鼻腔内ステロイド剤などの併用療法を推奨するケースが増えている。

- 先進国市場における先進治療薬の保険適用範囲と償還額の増加は、患者がこれらの薬剤にアクセスしやすくし、普及を促進している。

- 疾病管理、生活の質の向上、外科的介入の予防への注目の高まりが、世界的な市場の持続的な成長を牽引している。

- 例えば、製薬会社と病院の提携関係の拡大は、患者アクセスプログラムを拡大し、医療サービスが行き届いていない地域での先進的な治療法の普及を促進している。

- Advancements in telemedicine and digital health platforms are enabling remote diagnosis, monitoring, and prescription of nasal polyposis drugs, increasing patient convenience and treatment adherence

Restraint/Challenge

“High Cost of Biologics and Limited Access in Emerging Markets”

- The high cost of biologic therapies and certain advanced corticosteroid formulations poses a significant challenge to wider adoption of nasal polyposis drugs, particularly in price-sensitive regions

- For instance, Dupixent therapy can cost several thousand dollars annually, limiting accessibility for patients without comprehensive insurance coverage

- Regulatory hurdles and complex approval processes for novel biologics can delay market entry in some countries, constraining growth opportunities

- In emerging markets, limited healthcare infrastructure and inadequate distribution networks restrict patient access to advanced therapies, even where demand is rising

- Additionally, the need for regular monitoring, follow-up visits, and physician-administered injections for certain therapies can be a barrier for patient adherence and convenience

- Overcoming these challenges through cost-reduction strategies, expanded reimbursement, and localized distribution programs will be critical for expanding the market in underserved regions

- For instance, patient assistance programs and subsidy schemes introduced by pharmaceutical companies can help reduce the financial burden and improve therapy adoption in low-income areas

- Limited awareness among general practitioners about the latest biologic therapies can delay referrals to specialists, impacting timely treatment initiation and overall market growth

Nasal Polyposis Drugs Market Scope

The market is segmented on the basis of drugs, route of administration, end-users, and distribution channel.

- By Drugs

On the basis of drugs, the nasal polyposis drugs market is segmented into nasal corticosteroids, oral and injectable corticosteroids, Dupixent, and others. The nasal corticosteroids segment dominated the market with the largest revenue share of 41.3% in 2025, driven by their first-line recommendation for CRSwNP management, ease of self-administration, and strong efficacy in reducing inflammation and polyp size. Physicians often prefer nasal corticosteroids for mild to moderate cases due to their safety profile and minimal systemic side effects. The segment also benefits from patient familiarity and the availability of multiple brands and formulations across key markets. Their integration into standard treatment guidelines further reinforces their market dominance. Strong consumer awareness and accessibility through various pharmacies contribute to consistent adoption and revenue generation.

The Dupixent segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing prescriptions for severe CRSwNP cases unresponsive to corticosteroids. Dupixent, a targeted biologic therapy, offers improved patient outcomes and reduced recurrence rates, making it highly attractive for specialists. Growing clinical evidence, patient support programs, and expanding insurance coverage are accelerating adoption. Physicians increasingly recommend Dupixent as a preferred advanced therapy, while awareness campaigns highlight its benefits for long-term disease control. Biologics such as Dupixent are also driving innovation in personalized treatment approaches, contributing to rapid market expansion.

- By Route of Administration

On the basis of route of administration, the market is segmented into oral, parenteral, nasal, and others. The nasal route dominated the market with the largest revenue share in 2025 due to its direct delivery to the target site, high efficacy in controlling polyp growth, and convenience for patients in self-administering therapy at home. Nasal sprays are widely prescribed and form a cornerstone of CRSwNP management, offering rapid relief and minimal systemic exposure. Their dominance is supported by guideline recommendations and strong physician familiarity. Patients also prefer nasal administration for comfort and ease of use over oral or injectable options. The availability of combination sprays with optimized dosing further reinforces their market leadership.

The parenteral route is expected to witness the fastest growth from 2026 to 2033, driven by the expanding use of biologics and injectable corticosteroids for severe or refractory cases. Parenteral administration allows precise dosing, improved systemic bioavailability, and longer-lasting effects, making it ideal for advanced therapies. Increasing adoption in hospitals and specialty clinics, along with patient education on injection techniques, is boosting uptake. This segment benefits from rising physician confidence in biologic therapies and improved access programs for patients in need of advanced treatment.

- By End-Users

On the basis of end-users, the market is segmented into hospitals, homecare, specialty clinics, and others. The hospital segment dominated the market with the largest revenue share of 39.5% in 2025, driven by inpatient treatment for severe CRSwNP cases, administration of advanced biologics, and management of comorbid conditions. Hospitals provide access to specialist care, diagnostic testing, and monitoring that ensure effective treatment outcomes. The concentration of ENT specialists and access to advanced therapies in hospital settings reinforces this dominance. Institutional treatment protocols and insurance coverage also favor hospital-based prescriptions. The segment remains strong due to ongoing investments in hospital infrastructure and patient education programs.

The homecare segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by rising patient preference for self-administered therapies such as nasal corticosteroids and home-use biologic injections. Convenience, reduced hospital visits, and increased awareness about at-home care solutions are driving adoption. Remote patient monitoring and telehealth guidance further support homecare growth. The segment is also expanding due to improved distribution of nasal sprays and support services for at-home biologic administration.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, online pharmacy, and retail pharmacy. The retail pharmacy segment dominated the market with the largest revenue share of 45.2% in 2025, driven by widespread accessibility, convenience, and immediate availability of nasal corticosteroids and oral medications. Patients commonly rely on retail pharmacies for OTC and prescription therapies, supported by pharmacist guidance and brand recognition. Strong distribution networks, promotional campaigns, and loyalty programs contribute to high retail adoption. The presence of multiple branded formulations and generic alternatives further strengthens this segment.

The online pharmacy segment is expected to witness the fastest growth from 2026 to 2033, fueled by increasing e-commerce adoption, patient preference for home delivery, and the convenience of subscription-based refills. Online pharmacies provide access to both prescription and advanced therapies, including biologics, expanding reach to remote areas. Growing digital health literacy, telemedicine integration, and secure online payment platforms are accelerating this trend. Online channels also facilitate discreet purchase and timely medication adherence, boosting market growth.

Nasal Polyposis Drugs Market Regional Analysis

- North America dominated the nasal polyposis drugs market with the largest revenue share of 38.7% in 2025, supported by high patient awareness, advanced healthcare infrastructure, and early adoption of therapies such as Dupixent

- Patients and healthcare providers in the region highly value the effectiveness, targeted treatment options, and improved quality of life offered by advanced therapies such as Dupixent and optimized nasal corticosteroids

- This widespread adoption is further supported by strong insurance coverage, high patient awareness, early adoption of innovative therapies, and easy access to hospitals and specialty clinics, establishing nasal polyposis drugs as a key solution for managing chronic sinus conditions in both mild and severe cases

U.S. Nasal Polyposis Drugs Market Insight

The U.S. nasal polyposis drugs market captured the largest revenue share of 82% in 2025 within North America, fueled by the high prevalence of chronic rhinosinusitis with nasal polyps (CRSwNP) and widespread adoption of advanced therapies such as nasal corticosteroids and Dupixent. Patients increasingly prioritize effective, non-surgical treatment options to manage inflammation, improve nasal airflow, and reduce polyp recurrence. The growing awareness of targeted biologic therapies, combined with robust insurance coverage and strong healthcare infrastructure, further propels market growth. Moreover, the integration of specialty care programs and patient support services is significantly enhancing access and adherence to prescribed therapies.

Europe Nasal Polyposis Drugs Market Insight

The Europe nasal polyposis drugs market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing prevalence of CRSwNP and rising demand for effective, guideline-recommended therapies. Growing urbanization, increasing healthcare expenditure, and awareness campaigns are fostering the adoption of corticosteroids and biologics. European patients are also drawn to treatments that improve quality of life and reduce surgical interventions. The region is experiencing significant growth across hospitals, specialty clinics, and homecare settings, with therapies being integrated into both new treatment protocols and updated clinical guidelines.

U.K. Nasal Polyposis Drugs Market Insight

The U.K. nasal polyposis drugs market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising patient awareness and preference for minimally invasive, effective treatment options. Additionally, increasing prevalence of CRSwNP and concerns regarding disease progression are encouraging both patients and healthcare providers to adopt advanced therapies, including biologics. The U.K.’s well-established healthcare infrastructure and strong insurance coverage, alongside growing digital health adoption and online pharmacy channels, are expected to continue stimulating market growth.

Germany Nasal Polyposis Drugs Market Insight

ドイツの鼻ポリープ治療薬市場は、慢性副鼻腔疾患に対する認識の高まりと、高度で標的を絞った治療法への需要の高まりを背景に、予測期間中に著しい年平均成長率(CAGR)で拡大すると予想されています。ドイツの強固な医療インフラ、イノベーションへの注力、そして高い患者コンプライアンスは、特に病院や専門クリニックにおいて、生物学的製剤や最適化されたコルチコステロイド治療の普及を促進しています。また、再発を減らし、長期的な予後を改善する治療法への強い嗜好から、患者支援プログラムや遠隔医療サービスの統合もますます普及しています。

アジア太平洋地域における鼻ポリープ治療薬市場のインサイト

アジア太平洋地域の鼻ポリープ治療薬市場は、中国、日本、インドなどの国々における都市化の進展、可処分所得の増加、技術革新を背景に、2026年から2033年の予測期間中に年平均成長率(CAGR)23%という最速の成長率で拡大すると見込まれています。政府の医療イニシアチブや生物製剤へのアクセス拡大に支えられた、慢性副鼻腔炎(CRSwNP)治療選択肢に対する地域住民の意識の高まりが、これらの薬剤の普及を促進しています。さらに、現地の医薬品製造・流通ネットワークの発展により、鼻ポリープ治療薬の価格と入手しやすさが向上し、より多くの患者に薬剤を届けられるようになっています。

日本の鼻ポリープ治療薬市場に関する洞察

日本の鼻ポリープ治療薬市場は、慢性副鼻腔炎(CRSwNP)の高い罹患率、充実した医療インフラ、そして早期介入への重視といった要因により、勢いを増している。日本の患者は、専門医によるケアプログラムに支えられた、鼻腔内ステロイド剤や生物学的製剤といった効果的な非外科的治療法をますます好むようになっている。鼻ポリープ治療薬のデジタルヘルスプラットフォームや在宅ケアへの統合も、市場の成長を後押ししている。さらに、日本の高齢化は、在宅医療と臨床現場の両方において、使いやすく安全で効果的な治療法への需要を高める可能性が高い。

インドの鼻ポリープ治療薬市場に関する洞察

2025年には、インドの鼻ポリープ治療薬市場はアジア太平洋地域で最大の市場収益シェアを占める見込みであり、これは慢性副鼻腔炎(CRSwNP)の罹患率の上昇、医療意識の高まり、中間層人口の拡大によるものです。インドは、手頃な価格、アクセスのしやすさ、病院、専門クリニック、在宅医療における普及の拡大を背景に、コルチコステロイド療法と生物製剤の両方にとって重要な市場として台頭しています。医療インフラと遠隔医療を促進する政府の取り組みと、強力な国内製薬産業が、インドにおける市場成長の主要因となっています。

鼻ポリープ治療薬の市場シェア

鼻ポリープ治療薬業界は、主に以下のような実績のある企業によって牽引されています。

- サノフィ(フランス)

- GSK plc(英国)

- イーライリリー・アンド・カンパニー(米国)

- ノバルティスAG(スイス)

- ファイザー社(米国)

- リジェネロン・ファーマシューティカルズ社(米国)

- アムジェン社(米国)

- アストラゼネカ(英国)

- オプティノーズUS社(米国)

- Intersect ENT, Inc. (米国)

- テバ・ファーマシューティカルズ(イスラエル)

- F. ホフマン・ラ・ロシュ社(スイス)

- メルク・アンド・カンパニー(米国)

- Keymed Biosciences, Inc. (米国)

- バイオヘイブン・ファーマシューティカルズ社(米国)

- 広東恒瑞製薬有限公司(中国)

- アップストリーム・バイオ社(米国)

- サンシャイン国健製薬有限公司(中国)

- Genrix Biotherapeutics(中国)

- 嘉泰天青製薬集団有限公司(中国)

世界の鼻ポリープ治療薬市場における最近の動向とは?

- 2025年10月、米国FDAは、胸腺間質リンパ球増殖因子(TSLP)を標的とする新規作用機序により、ポリープの重症度を大幅に軽減し、手術やステロイドの必要量を減らすという、既存の治療法をはるかに超える大きな進歩を示す、慢性副鼻腔炎(鼻ポリープを伴う)(CRSwNP)に対する新しい生物学的製剤TEZSPIRE®(テゼペルマブ-エッコ)を承認しました。

- 2025年6月、デュピクセント®(デュピルマブ)は、慢性副鼻腔炎(CRSwNP)と喘息を併発している患者を対象とした初の直接比較第4相臨床試験において、ゾレア®(オマリズマブ)に対する優位性を示し、鼻ポリープの大きさ、嗅覚、喘息コントロールにおいてより良好な結果を示しました。これは、複雑な症例における生物学的製剤の処方選択に影響を与える可能性があります。

- 2025年1月、GSKのヌカラ®(メポリズマブ)は、慢性副鼻腔炎(CRSwNP)の成人患者の治療薬として中国で承認され、世界最大級の市場の一つである中国で新たな生物学的製剤の選択肢を提供し、欧米地域以外への治療アクセスを拡大した。

- 2024年9月、米国FDAはデュピクセント®の承認範囲を拡大し、鼻ポリープを伴う慢性副鼻腔炎のコントロール不良の青年(12~17歳)の治療にも適用しました。これにより、主要な生物学的製剤がより若い患者にも利用可能となり、対象となる患者層が拡大しました。

- 2021年7月(市場動向の重要な基準点)、FDAは成人における鼻ポリープを伴う慢性副鼻腔炎の治療薬としてヌカラ(メポリズマブ)を初めて承認し、鼻ポリープに対する初のIL-5標的生物学的製剤を確立するとともに、その後の生物学的製剤の競争と治療の多様化の基盤を築いた。

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。