Global Ai Powered Surgical Simulators Market

市场规模(十亿美元)

CAGR :

%

USD

87.23 Million

USD

332.71 Million

2024

2032

USD

87.23 Million

USD

332.71 Million

2024

2032

| 2025 –2032 | |

| USD 87.23 Million | |

| USD 332.71 Million | |

| % | |

|

全球人工智慧手術模擬器市場細分,按產品類型(基於技術的模擬器、基於模型的模擬器和基於電腦的模擬器)、應用(心臟外科、胃腸病學、神經外科、骨科手術、重建外科、腫瘤外科、移植等)、技術(虛擬患者模擬和 3D 列印)、最終用戶(學術機構、醫院、軍事組織和研究組織) - 203 年到行業預測

人工智慧手術模擬器市場規模

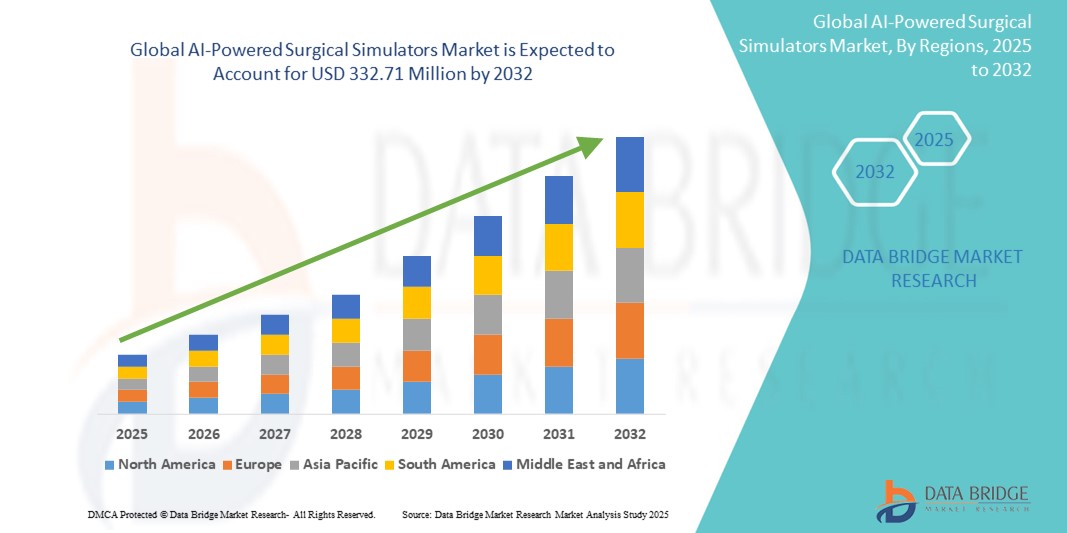

- 2024 年全球人工智慧手術模擬器市場規模為8,723 萬美元 ,預計 到 2032 年將達到 3.3271 億美元,預測期內 複合年增長率為 18.20%。

- 市場成長主要受到全球對高技能外科醫生日益增長的需求的推動,特別是隨著複雜和微創外科手術的興起,以及對病人安全和減少醫療錯誤的日益重視

- 此外,醫學課程中對基於模擬的培訓的認識和採用不斷提高,加上公共和私人實體對醫療基礎設施和研發的大量投資,正在加速採用人工智慧手術模擬器解決方案,從而顯著促進該行業的成長

人工智慧手術模擬器市場分析

- 人工智慧手術模擬器提供高度逼真和適應性的訓練環境,正在成為現代醫學教育和手術技能發展中不可或缺的工具。它們能夠提供個人化回饋、追蹤性能並複製複雜場景,從而顯著提高手術精度和患者安全性。

- 對人工智慧手術模擬器的需求激增,主要是由於對能夠執行複雜和微創手術的高技能外科醫生的需求不斷增長、對患者安全的日益重視以及虛擬現實(VR)、增強現實(AR) 和觸覺反饋系統的技術進步。需要外科手術介入的慢性病發生率不斷上升,也增加了需要高級培訓的外科醫生的數量

- 北美在人工智慧手術模擬器市場佔據主導地位,2024 年的收入份額最大,為 35.93%,其特點是其完善的醫療保健基礎設施、早期採用先進的醫療技術、領先模擬公司在研發方面的大量投資,以及對加強手術培訓的高度重視

- 由於醫療保健支出不斷增加、患者群體迅速擴大、政府推動基於模擬的培訓,預計亞太地區將成為預測期內人工智慧手術模擬器市場成長最快的地區

- 3D 列印領域在人工智慧手術模擬器市場佔據主導地位,到 2024 年市場份額將達到 50.5%,這得益於可自訂模型、增強的真實感以及對精準訓練的需求不斷增長

報告範圍和人工智慧手術模擬器市場細分

|

屬性 |

人工智慧手術模擬器關鍵市場洞察 |

|

涵蓋的領域 |

|

|

覆蓋國家 |

北美洲

歐洲

亞太

中東和非洲

南美洲

|

|

主要市場參與者 |

|

|

市場機會 |

|

|

加值資料資訊集 |

除了對市場價值、成長率、細分、地理覆蓋範圍和主要參與者等市場情景的洞察之外,Data Bridge Market Research 策劃的市場報告還包括深入的專家分析、定價分析、品牌份額分析、消費者調查、人口統計分析、供應鏈分析、價值鏈分析、原材料/消耗品概述、供應商選擇標準、PESTLE 分析、波特分析和監管框架。 |

人工智慧手術模擬器市場趨勢

“透過先進的人工智慧和觸覺技術實現超現實和自適應學習”

- A significant and accelerating trend in the global AI-powered surgical simulators market is the continuous drive towards hyper-realism through the deep integration of advanced AI algorithms and highly sophisticated haptic feedback systems. This fusion of technologies is dramatically enhancing the immersion and effectiveness of surgical training

- For instance, leading simulator manufacturers are developing platforms that utilize AI to dynamically adjust surgical scenarios based on trainee performance, providing real-time, personalized feedback on force application, tissue manipulation, and procedural steps. Haptic feedback devices are becoming increasingly precise, replicating the subtle tactile sensations of different tissues, bone drilling, and suturing with unprecedented accuracy

- AI integration in surgical simulators enables features such as intelligent performance assessment, identifying specific areas for improvement, and providing adaptive learning pathways. This goes beyond simple pass/fail metrics to offer detailed insights into a trainee's strengths and weaknesses, tailoring subsequent practice sessions to address specific skill gaps. For instance, some advanced simulators can detect inefficient movements or excessive force, offering immediate visual and haptic cues to correct technique

- The seamless integration of AI with advanced haptic feedback, combined with high-fidelity virtual reality (VR) and augmented reality (AR) environments, facilitates a truly immersive and hands-on training experience that closely mimics real-world surgical conditions. This allows trainees to develop muscle memory and refine fine motor skills in a safe, repeatable, and objective environment

- The demand for AI-powered surgical simulators that offer hyper-realistic and adaptative learning experiences is growing rapidly across medical schools, hospitals, and specialized training centers, as healthcare systems increasingly prioritize high-quality, standardized surgical education and patient safety

AI-Powered Surgical Simulators Market Dynamics

Driver

“Increasing Demand for Minimally Invasive and Complex Surgical Procedures, Coupled with an Unwavering Focus on Patient Safety”

- The escalating global demand for surgeons proficient in minimally invasive surgical (MIS) and other highly complex procedures is a primary driver for the surging adoption of AI-powered surgical simulators. MIS offers numerous patient benefits, including smaller incisions, less pain, shorter hospital stays, and quicker recovery times, making it a preferred approach. However, these procedures require exceptionally precise skills and a steeper learning curve compared to traditional open surgery

- For instance, the increasing prevalence of chronic diseases such as cancer, cardiovascular diseases, and musculoskeletal disorders necessitates a growing volume of surgical interventions, many of which are now performed using advanced MIS techniques. This creates an urgent need for effective and scalable training solutions that can rapidly equip surgeons with the necessary expertise

- Furthermore, the unwavering global focus on patient safety and the imperative to reduce medical errors are significantly propelling the market. AI-powered simulators provide a risk-free, highly realistic environment where surgeons can repeatedly practice complex procedures, make and learn from mistakes without any harm to real patients. This proactive approach enhances individual competence and team coordination, leading to better surgical outcomes and fewer complications

- The inherent ability of AI-powered simulators to provide objective, data-driven performance feedback, identify skill gaps, and offer personalized learning pathways makes them indispensable tools for continuous surgical education and competency assessment.

- Regulatory bodies and healthcare institutions are increasingly recognizing the value of simulation-based training in achieving and maintaining surgical proficiency, further contributing to market growth. The convenience of practicing anytime, anywhere (especially with cloud-based solutions) and the ability to train on a vast array of patient-specific scenarios are key factors propelling the adoption of these advanced training systems in both academic and clinical settings

Restraint/Challenge

“High Initial Costs and Complex Integration Challenges”

- A significant restraint on the widespread adoption of AI-powered surgical simulators is their high initial capital expenditure and the inherent complexity of integrating these advanced systems into existing healthcare and academic infrastructures. While the long-term benefits in terms of improved surgical outcomes and reduced errors are clear, the upfront investment can be prohibitive for many institutions, especially smaller clinics or those in developing regions

- For instance, setting up a comprehensive simulation lab with high-fidelity AI-powered simulators, haptic devices, and VR/AR equipment can range from hundreds of thousands to several million dollars. This initial cost often includes not only the hardware and software but also the necessary space development or remodeling, and ongoing expenses for maintenance, software updates, and training for instructors

- Furthermore, integrating these sophisticated AI-powered simulators with existing hospital IT systems, electronic health records (EHR), and training management platforms presents significant technical and logistical challenges. Compatibility issues can arise, requiring substantial investments in software adjustments and staff training to ensure seamless workflow and data exchange

- The intricate nature of AI algorithms, particularly those requiring vast datasets for training and real-time processing for dynamic scenarios, adds to the development and operational costs

- The need for continuous updates and upgrades to keep pace with rapid technological advancements also contributes to the total cost of ownership. This financial barrier and the technical hurdles can limit access to high-quality, AI-driven surgical training, particularly in regions with constrained healthcare budgets

AI-Powered Surgical Simulators Market Scope

The market is segmented on the basis of product type, application, technology, and end user

By Product Type (Technology-based Simulators, Model-based Simulators and Computer-based Simulators), Application (Cardiac Surgery, Gastroenterology, Neurosurgery, Orthopedic Surgery, Reconstructive Surgery, Oncology Surgery, Transplant, and Others), Technology (Virtual Patient Simulation and 3D Printing), End user (Academic Institutes, Hospitals, Military Organizations, and Research Organizations)

- By Product Type

On the basis of product type, the AI-powered surgical simulators market is segmented into Technology-based Simulators, Model-based Simulators, and Computer-based Simulators. Technology-based simulators held the largest market share in 2024. This dominance is driven by the increasing integration of AI, VR, AR, and haptic feedback to create highly immersive and realistic training environments. These simulators offer a superior level of realism and interactivity compared to traditional methods, making them highly desirable for complex surgical training. The continuous advancements in these underlying technologies, constantly pushing the boundaries of fidelity and adaptive learning, further solidify their leading position.

Technology-based simulators are also anticipated to be the fastest-growing segment from 2025 to 2032. While VR has been dominant, AR-based simulators are gaining significant traction. AR overlays digital information onto real-world environments, offering unique opportunities for training on physical models with digital guidance or for in-situ training within actual operating rooms (without patient involvement). The ability to combine physical interaction with digital augmentation provides a hybrid approach that is increasingly appealing for advanced training.

- By Application

On the basis of application, the AI-powered surgical simulators market is segmented into cardiac surgery, gastroenterology, neurosurgery, orthopedic surgery, reconstructive surgery, oncology surgery, transplant, and others. The orthopedic surgery segment held the highest market share in 2024, driven by the high volume of orthopedic procedures performed globally, coupled with the increasing complexity of these surgeries and the growing emphasis on simulation-based training for orthopedic residents. The need for precise skill development in procedures such as joint replacements and fracture repairs fuels the demand for specialized orthopedic simulators.

The reconstructive surgery segment is expected to witness a rapid growth rate during the forecast period. This growth is attributed to the rising demand for enhanced training solutions for complex reconstructive procedures, including facial, craniofacial, and breast reconstruction. The intricate nature and high stakes of these surgeries make realistic simulation crucial for surgeon proficiency and patient safety.

- By Technology

On the basis of technology, the AI-powered surgical simulators market is segmented into virtual patient simulation and 3D printing. The 3D printing segment dominated the AI-powered surgical simulators market with a market share of 50.5% in 2024, driven by customizable models, enhanced realism, and increased demand for precision training.

The 3D printing segment also holds a substantial market share from 2025 to 2032, growth is fueled by the increasing awareness regarding the benefits of creating highly realistic, patient-specific anatomical models for surgical planning and hands-on training. 3D printed models, often combined with AI for patient-specific modeling, allow surgeons to physically rehearse complex cases.

- By End User

On the basis of end user, the AI-powered surgical simulators market is segmented into academic institutes, hospitals, military organizations, and research organizations. Academic institutes held the largest market share in 2024. This is due to their critical role in surgical education and research, where simulation-based training is increasingly becoming a mandatory component of medical curricula. Universities and medical schools are primary adopters for educating future surgeons

The hospitals segment is expected to witness the fastest CAGR from 2025 to 2032, as they are key end-users for the continuous professional development and skill enhancement of their resident surgeons and practicing staff. Hospitals invest in simulators to ensure their surgical teams maintain proficiency in current techniques and adapt to new procedures, ultimately aiming to improve patient outcomes and safety.

AI-Powered Surgical Simulators Market Regional Analysis

- North America dominates the AI-powered surgical simulators market with the largest revenue share of 35.93% in 2024, driven by its well-established healthcare infrastructure, early adoption of advanced medical technologies, substantial R&D investments by leading simulation firms, and a strong focus on enhancing surgical training

- Consumers and healthcare institutions in the region highly prioritize patient safety and continuous skill development for surgeons, leading to a strong demand for sophisticated simulation tools

- This widespread adoption is further supported by the presence of key industry players, favorable government initiatives promoting simulation-based training, and the increasing volume of minimally invasive surgical procedures, establishing AI-powered surgical simulators as a critical component of surgical training in both academic and clinical settings.The U.S. leads this regional market, characterized by early adoption of advanced technologies and innovations from both established firms and startups

U.S. AI-Powered Surgical Simulators Market Insight

The U.S. AI-powered surgical simulators market largest revenue share in 2024 fueled by the rapid adoption of advanced medical technologies and the expanding emphasis on high-fidelity surgical training. Healthcare institutions and medical schools are increasingly prioritizing the enhancement of surgical skills through intelligent, immersive simulation systems. The growing preference for patient safety and the demand for highly skilled surgeons capable of performing complex procedures, combined with robust investments in R&D by leading medical technology companies, further propels the AI-powered surgical simulator industry. Moreover, the increasing integration of AI within surgical robotics and its application in personalized surgical planning are significantly contributing to the market's expansion

Europe AI-Powered Surgical Simulators Market Insight

The Europe AI-powered surgical simulators market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing investments in healthcare infrastructure, stringent regulations emphasizing patient safety, and the escalating need for enhanced surgical proficiency. The rising adoption of robotic-assisted surgeries across Europe, coupled with the demand for advanced training methodologies, is fostering the adoption of AI-powered simulators. European healthcare systems are also drawn to the efficiency and reduced complication rates these technologies offer. The region is experiencing significant growth across academic institutes and hospitals, with AI-powered simulators being incorporated into both established training programs and new surgical residency curricula

U.K. AI-Powered Surgical Simulators Market Insight

The U.K. AI-powered surgical simulators market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the escalating emphasis on medical education and a desire for heightened surgical precision and patient safety within the National Health Service (NHS). In addition, concerns regarding surgical errors and the increasing complexity of procedures are encouraging both academic institutions and hospitals to choose AI-driven simulation solutions. The UK’s embrace of technological advancements in VR/AR, alongside its robust medical research infrastructure, is expected to continue to stimulate market growth

Germany AI-Powered Surgical Simulators Market Insight

The Germany AI-powered surgical simulators market is expected to expand at a considerable CAGR during the forecast period fueled by increasing awareness of the benefits of simulation-based training and the demand for technologically advanced, high-fidelity solutions. Germany’s well-developed healthcare infrastructure, combined with its emphasis on innovation and quality in medical education, promotes the adoption of AI-powered surgical simulators, particularly in university hospitals and specialized training centers. The integration of AI-powered simulators with advancements in minimally invasive surgery is also becoming increasingly prevalent, aligning with local healthcare priorities for efficiency and patient outcomes

Asia-Pacific AI-Powered Surgical Simulators Market Insight

The Asia-Pacific AI-powered surgical simulators market is poised to grow at the fastest CAGR during the forecast period, driven by increasing healthcare investments, rising disposable incomes, and rapid technological advancements in countries such as China, Japan, and India. The region's growing inclination towards adopting advanced medical technologies, supported by government initiatives promoting digitalization and improving healthcare access, is driving the adoption of AI-powered surgical simulators. Furthermore, as APAC emerges as a hub for medical device manufacturing and technological innovation, the affordability and accessibility of advanced simulation solutions are expanding to a wider base of medical professionals

Japan AI-Powered Surgical Simulators Market Insight

The Japan AI-powered surgical simulators market is gaining momentum due to the country’s high-tech culture, rapid urbanization, and an increasing demand for highly skilled surgeons. The Japanese market places a significant emphasis on precision and patient safety, and the adoption of AI-powered simulators is driven by the growing number of complex surgical procedures and the integration of advanced technologies such as AI and VR/AR in medical training. The collaboration between academic institutions and industry players to develop innovative simulation platforms is fueling growth. Moreover, Japan's aging population is likely to spur demand for continuous training to manage age-related conditions requiring surgical intervention

India AI-Powered Surgical Simulators Market Insight

The India AI-powered surgical simulators market is experiencing significant growth, attributed to the country's expanding healthcare sector, rapid urbanization, and high rates of technological adoption. India is witnessing a surge in medical colleges and hospitals investing in simulation labs, and AI-powered simulators are becoming increasingly popular for training in various surgical specialties. The push towards enhancing medical education standards and the availability of increasingly affordable, yet advanced, simulation options, alongside strong domestic manufacturing and research efforts, are key factors propelling the market in India

AI-Powered Surgical Simulators Market Share

The AI-powered surgical simulators industry is primarily led by well-established companies, including:

- Surgical Science Sweden AB (Sweden)

- Mentice AB (Sweden)

- VirtaMed AG (Switzerland)

- Laerdal Medical (Norway)

- 3D Systems, Inc. (U.S.)

- Materialise (Belgium)

- Stratasys (Israel)

- Gaumard Scientific (U.S.)

- Simulab Corporation (U.S.)

- Fundamental Surgery (U.K.)

- Theator Inc. (U.S.)

- Alcon (U.S.)

- Intuitive Surgical, Inc. (U.S.)

- Medtronic (Ireland)

- Stryker (U.S.)

- Smith+Nephew (U.K.)

- Zimmer Biomet (U.S.)

- Activ Surgical (U.S.)

- FEops nv (Belgium)

Latest Developments in Global AI-Powered Surgical Simulators Market

- In July 2024, Materialise, a leader in medical visualization and 3D printing, acquired FEops, a company specializing in predictive simulation for structural heart interventions. This strategic move aims to combine Materialise's expertise in personalized solutions with FEops' advanced simulation capabilities, providing clinicians with more comprehensive insights into patient anatomy for improved structural heart procedures

- In June 2024, Stratasys Ltd. introduced the J5 Digital Anatomy 3D printer. This new system is designed to meet the growing need for cost-effective and highly accurate anatomical models, supporting hospitals, medical device manufacturers, and research institutions in enhancing patient outcomes, streamlining operations, and accelerating product development cycles

- In April 2022, Alcon launched the Alcon Fidelis Virtual Reality Ophthalmic Surgical Simulator. This portable VR tool is specifically designed for cataract surgery trainees, offering a realistic virtual operating room setting with haptic feedback to accurately replicate the experience of performing cataract surgery. It's integrated within the Alcon Experience Academy

- In September 2021, CAE Healthcare entered into a partnership with RCSI University of Medicine and Health Sciences to advance healthcare technology, education, and research through simulation methodologies. As part of this collaboration, the RCSI SIM Centre for Simulation Education and Research received recognition as a certified Centre of Excellence, making it the first such designation in Europe

- In March 2023, the University of Southern California (USC) Viterbi School of Engineering announced that Professor Yan Liu and Dr. Andrew Hung received a USD 3 million award from the National Institutes of Health. This funding is dedicated to advancing their research on AI tools specifically designed to measure and improve surgeons' technical skills during complex procedures such as radical prostatectomy using deep learning. This highlights a clear trend towards AI for objective and nuanced skill assessment

SKU-

研究方法

数据收集和基准年分析是使用具有大样本量的数据收集模块完成的。该阶段包括通过各种来源和策略获取市场信息或相关数据。它包括提前检查和规划从过去获得的所有数据。它同样包括检查不同信息源中出现的信息不一致。使用市场统计和连贯模型分析和估计市场数据。此外,市场份额分析和关键趋势分析是市场报告中的主要成功因素。要了解更多信息,请请求分析师致电或下拉您的询问。

DBMR 研究团队使用的关键研究方法是数据三角测量,其中包括数据挖掘、数据变量对市场影响的分析和主要(行业专家)验证。数据模型包括供应商定位网格、市场时间线分析、市场概览和指南、公司定位网格、专利分析、定价分析、公司市场份额分析、测量标准、全球与区域和供应商份额分析。要了解有关研究方法的更多信息,请向我们的行业专家咨询。

可定制

Data Bridge Market Research 是高级形成性研究领域的领导者。我们为向现有和新客户提供符合其目标的数据和分析而感到自豪。报告可定制,包括目标品牌的价格趋势分析、了解其他国家的市场(索取国家列表)、临床试验结果数据、文献综述、翻新市场和产品基础分析。目标竞争对手的市场分析可以从基于技术的分析到市场组合策略进行分析。我们可以按照您所需的格式和数据样式添加您需要的任意数量的竞争对手数据。我们的分析师团队还可以为您提供原始 Excel 文件数据透视表(事实手册)中的数据,或者可以帮助您根据报告中的数据集创建演示文稿。