Global Portable Ultrasound System Market

市场规模(十亿美元)

CAGR :

%

USD

2.83 Billion

USD

4.65 Billion

2024

2032

USD

2.83 Billion

USD

4.65 Billion

2024

2032

| 2025 –2032 | |

| USD 2.83 Billion | |

| USD 4.65 Billion | |

| % | |

|

全球便攜式超音波系統市場細分,按設備類型(移動超音波設備和手持式超音波設備)、應用(放射科、心臟病學、婦產科、血管應用、泌尿科應用、骨科和肌肉骨骼應用及其他)、技術(診斷超音波和治療超音波)、設備顯示(彩色超音波和黑白 (B/W) 超音波)、系統便攜性(推車/緊湊型超音波)超音波系統)、最終用戶(醫院、診斷中心、門診護理中心、產科中心、外科中心及其他) - 行業趨勢和預測到 2032 年

便攜式超音波系統市場規模

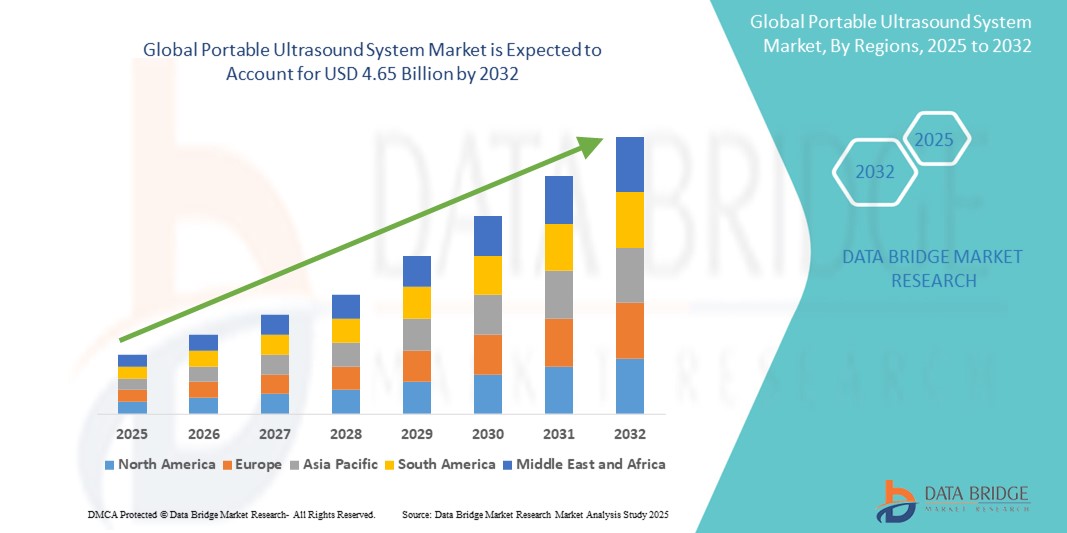

- 2024 年全球便攜式超音波系統市場規模為28.3 億美元 ,預計 到 2032 年將達到 46.5 億美元,預測期內 複合年增長率為 6.36%。

- 市場成長主要受到慢性病盛行率上升、老年人口成長以及已開發和新興醫療體系中即時診斷應用不斷擴大的推動

- 此外,對緊湊、經濟高效且易於使用的診斷成像技術的需求(尤其是在偏遠和資源有限的環境中)使得便攜式超音波系統成為現代醫療保健服務的關鍵工具。這些因素正在加速便攜式超音波解決方案的普及,從而顯著促進該行業的成長。

便攜式超音波系統市場分析

- 便攜式超音波系統提供緊湊和移動的診斷成像解決方案,由於其實時成像能力、成本效益和在急救、產科、心臟病學和肌肉骨骼評估等各種醫療應用中的易用性,正成為醫院和非醫院環境中即時診斷的重要組成部分。

- 便攜式超音波系統需求的不斷增長主要是由於慢性病和生活方式相關疾病的日益流行、老年人口的不斷增加以及偏遠和服務欠缺地區對快速、便捷診斷工具的需求不斷增加

- 北美在便攜式超音波系統市場佔據主導地位,2024 年其收入份額最大,為 38.2%,其特點是醫療基礎設施先進、醫療支出高、即時成像技術應用廣泛,而美國在急診科、家庭護理和門診環境需求的推動下,便攜式超聲系統市場將出現大幅增長

- 由於醫療基礎設施投資不斷增加、城市化進程加快以及農村和半城市人口對早期診斷益處的認識不斷提高,預計亞太地區將成為預測期內便攜式超音波系統市場增長最快的地區

- 推車式/推車式超音波系統在便攜式超音波系統市場佔據主導地位,2024 年的市場份額為 66.4%,這得益於其卓越的成像能力、更大的螢幕尺寸以及在醫院和診斷中心等各種臨床環境中使用的多功能性

報告範圍和便攜式超音波系統市場細分

|

屬性 |

便攜式超音波系統關鍵市場洞察 |

|

涵蓋的領域 |

|

|

覆蓋國家 |

北美洲

歐洲

亞太

中東和非洲

南美洲

|

|

主要市場參與者 |

|

|

市場機會 |

|

|

加值資料資訊集 |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Portable Ultrasound System Market Trends

“Advancements in AI-Enabled Imaging and Wireless Connectivity”

- A significant and accelerating trend in the global portable ultrasound system market is the integration of artificial intelligence (AI) and enhanced wireless connectivity, enabling more accurate image analysis, faster diagnostics, and improved workflow efficiency across diverse clinical settings

- For instance, Philips’ Lumify portable ultrasound system incorporates AI-driven image optimization and remote collaboration features, allowing clinicians to perform high-quality scans and consult specialists in real-time via mobile devices. Similarly, Butterfly Network’s handheld ultrasound uses AI algorithms to assist in image interpretation, improving diagnostic confidence for non-expert users

- AI integration in portable ultrasound systems supports automated measurements, anomaly detection, and adaptive imaging protocols tailored to patient-specific characteristics, thereby reducing operator dependency and enhancing diagnostic accuracy. Wireless connectivity enables seamless transfer of images and data to electronic health records (EHRs) and facilitates telemedicine applications, especially in remote and resource-limited areas.

- The convergence of AI and wireless technologies also facilitates the development of cloud-based platforms for centralized data management, remote training, and continuous software updates, promoting greater accessibility and cost-effectiveness

- This trend towards smarter, connected, and user-friendly portable ultrasound devices is reshaping clinical workflows and expanding the adoption of point-of-care ultrasound across emergency medicine, primary care, and rural healthcare. Companies such as GE Healthcare are investing in AI-enabled ultrasound solutions that provide automated organ segmentation and real-time guidance for needle placements

- The demand for portable ultrasound systems with integrated AI and wireless connectivity is growing rapidly across hospitals, outpatient clinics, and home healthcare, driven by the need for timely, accurate, and accessible diagnostic imaging

Portable Ultrasound System Market Dynamics

Driver

“Rising Demand Driven by Growing Chronic Diseases and Point-of-Care Diagnostics”

- The increasing prevalence of chronic diseases such as cardiovascular disorders, cancer, and diabetes, along with a rising geriatric population, is a significant driver fueling the demand for portable ultrasound systems globally

- For instance, in March 2024, Butterfly Network expanded its AI-powered handheld ultrasound platform to enhance point-of-care imaging capabilities in emergency and outpatient settings, highlighting how technological advancements by leading companies are expected to accelerate market growth during the forecast period

- As healthcare providers seek faster and more accessible diagnostic solutions, portable ultrasound systems offer real-time imaging, ease of use, and cost-effectiveness compared to traditional stationary ultrasound machines, making them highly desirable in both hospital and remote clinical environments

- Furthermore, the growing emphasis on early diagnosis and minimally invasive procedures is driving adoption of portable ultrasound systems, as they enable clinicians to perform bedside imaging with reduced patient movement and faster decision-making

- The convenience of portable, lightweight devices, combined with wireless connectivity and integration with mobile platforms for remote consultation and data sharing, is expanding the application of ultrasound beyond conventional radiology departments, into emergency rooms, ambulances, and rural healthcare centers. The increasing availability of user-friendly devices and telemedicine initiatives further propel market growth across diverse healthcare settings

Restraint/Challenge

“Concerns Regarding Data Security and High Initial Investment Costs”

- Concerns surrounding data security and privacy vulnerabilities associated with connected medical devices, including portable ultrasound systems, pose a significant challenge to broader market adoption. As these systems often rely on wireless connectivity and cloud-based data storage, they are susceptible to cyberattacks and unauthorized access, raising apprehensions among healthcare providers and patients about the safety of sensitive medical information

- For instance, reports of data breaches in healthcare networks have made some institutions cautious in deploying connected diagnostic devices without robust security protocols in place

- Addressing these data security concerns through stringent encryption, secure user authentication, and compliance with healthcare regulations such as HIPAA and GDPR is crucial for building trust among end-users. Companies such as GE Healthcare and Philips emphasize their commitment to cybersecurity by incorporating advanced protective measures and regular software updates in their ultrasound solutions. In addition, the relatively high initial cost of portable ultrasound systems, especially advanced models with AI capabilities and wireless connectivity, can be a barrier for smaller clinics and healthcare providers in developing regions

- While more affordable handheld and cart-based systems are becoming available, premium features such as 3D/4D imaging and integrated AI analysis often come with higher price tags, which may limit widespread adoption in cost-sensitive markets

- Overcoming these challenges through enhanced cybersecurity measures, educating healthcare providers on best practices for device security, and the development of cost-effective portable ultrasound options will be vital for sustained market growth

Portable Ultrasound System Market Scope

The market is segmented on the basis of type of device, application, technology, device display, system portability, and end user.

- By Type Of Device

On the basis of device type, the market is segmented into mobile ultrasound devices and hand-held ultrasound devices. The mobile ultrasound device segment dominates the market in 2024, due to its high versatility, wide acceptance across multiple clinical settings, and superior imaging capabilities compared to smaller devices. Mobile devices are commonly used in hospitals and diagnostic centers where portability combined with robust imaging features is required.

The hand-held ultrasound device segment is expected to witness the fastest growth during the forecast period, driven by their extremely compact design, ease of use in emergency or point-of-care scenarios, and rising demand for on-the-go diagnostics. Advances in battery technology and wireless connectivity further fuel this segment’s rapid adoption in ambulatory care, remote locations, and home healthcare services.

- By Application

On the basis of application, the market segments include radiology, cardiology, gynecology, vascular applications, urological applications, orthopedic and musculoskeletal applications, and others. The radiology segment dominates the market in 2024, as ultrasound imaging remains a primary diagnostic tool across a broad range of radiological examinations. Its widespread use in disease diagnosis, cancer detection, and organ imaging secures a substantial market share.

The cardiology segment is expected to grow at the fastest rate during forecast period, owing to the increasing incidence of cardiovascular diseases worldwide and the development of portable echocardiography systems that facilitate rapid, bedside cardiac assessments. Growing awareness of cardiac health and preventive screening also propels growth in this segment.

- By Technology

On the basis of technology, the market is divided into diagnostic ultrasound and therapeutic ultrasound. The diagnostic ultrasound segment dominates the market in 2024, supported by its critical role in non-invasive imaging, early disease detection, and wide acceptance across clinical fields. Diagnostic ultrasound benefits from continual innovations such as 3D/4D imaging and Doppler technologies that enhance clinical outcomes.

預計治療性超音波領域在預測期內將增長最快,這得益於其在物理治療、疼痛管理和復健治療中的應用日益增長。人們對非侵入性治療方式的興趣日益濃厚,以及聚焦超音波技術的進步,是該領域強勁成長軌跡的關鍵因素。

- 按設備顯示

根據設備顯示屏,市場可細分為彩色超音波和黑白 (B/W) 超音波系統。彩色超音波將在 2024 年佔據市場主導地位,因為彩色多普勒成像能夠增強血流和組織灌注的可視化,從而提高血管和心臟應用的診斷準確性。卓越的成像品質使彩色超音波系統成為先進醫療機構的首選。

黑白 (B/W) 超音波市場預計將在預測期內成長最快,尤其是在新興市場和成本敏感市場,這些市場注重價格承受能力。儘管成像精度較低,但黑白超音波設備提供了必要的診斷功能,在資源有限的地區可作為入門級選擇。

- 按設備可移植性

根據系統便攜性,市場可分為推車式/車載式超音波系統、緊湊型/手持式超音波系統和床邊 (POC) 超音波系統。推車式/車載式超音波系統佔據市場主導地位,2024 年將佔據 66.4% 的市場份額,這得益於其全面的成像功能、多用途探頭以及在醫院各種診斷工作流程中的廣泛應用。這些系統兼具便攜性和高端功能,使其成為放射科和心臟科的必備設備。

相反,緊湊型/手持式超音波系統市場預計將在預測期內實現最快成長,這得益於對輕便便攜設備日益增長的需求,這些設備可用於床邊診斷、緊急應變和遠距醫療應用。智慧型手機連接和人工智慧輔助成像等技術進步增強了手持系統的吸引力和功能。

- 按最終用戶

根據最終用戶,市場細分為醫院、診斷中心、門診護理中心、婦產中心、外科中心和其他。醫院細分市場將在2024年佔據市場主導地位,因為醫院擁有龐大的患者數量、多樣化的診斷需求以及支持跨部門多種超音波系統的基礎設施。醫院也投入巨資購置先進的超音波技術,以實現全面的照護。

另一方面,門診護理中心細分市場預計將在預測期內實現最快增長,這得益於醫療保健日益分散化、門診量不斷增加以及向居家和社區護理的轉變。門診護理中心的便攜式超音波系統能夠加快診斷速度,減少就診次數,並支持高效的患者管理,從而推動該細分市場的成長。

便攜式超音波系統市場區域分析

- 北美在便攜式超音波系統市場佔據主導地位,2024 年其收入份額最大,為 38.2%,這得益於先進的醫療基礎設施、高昂的醫療支出以及即時影像技術的廣泛採用

- 美國和加拿大的醫療保健提供者越來越依賴便攜式超音波系統,以便在急診、重症監護和門診環境中進行快速的床邊診斷。老年人口的增長、慢性病發病率的上升以及醫療保健向分散化和居家化發展的趨勢進一步推動了這一需求。

- 此外,領先製造商的存在、有利的監管政策以及對遠距醫療和診斷成像的大力投資也促進了市場的成長。便攜式超音波系統的多功能性和移動性與北美對患者護理效率、精準度和可及性的關注高度契合,使該地區成為先進超音波技術應用的重鎮。

美國便攜式超音波系統市場洞察

2024年,美國便攜式超音波系統市場佔據北美地區最大市場份額,達79.4%,這得益於急診和重症監護環境中對即時診斷和快速成像的需求不斷增長。先進的醫療基礎設施、對非侵入式即時成像工具日益增長的偏好以及慢性病的高發病率,共同推動了市場的擴張。此外,人工智慧增強影像和手持超音波設備無線連接等技術創新,進一步加速了其在醫院、門診和家庭護理環境中的普及。

歐洲便攜式超音波系統市場洞察

預計歐洲便攜式超音波系統市場在預測期內將以強勁的複合年增長率擴張,這得益於城鄉地區遠端護理和診斷服務的日益普及。該地區各國正積極採用便攜式影像系統,以增強診斷服務的可近性,尤其是在老年護理和全科醫療領域。監管部門對緊湊型節能設備的支持,加上對遠距醫療和微創診斷的需求,正在推動便攜式超音波系統在診所、門診手術中心和行動醫療單位的廣泛應用。

英國便攜式超音波系統市場洞察

The U.K. portable ultrasound system market is anticipated to grow steadily, driven by healthcare reforms aimed at early diagnosis and outpatient care expansion. Demand is increasing for compact, handheld ultrasound tools that can be utilized in both general practice and emergency departments. The U.K.'s National Health Service (NHS) is actively integrating point-of-care ultrasound (POCUS) into primary care settings to reduce hospital burden, and training initiatives are equipping more clinicians with portable ultrasound proficiency to improve patient triage and monitoring.

Germany Portable Ultrasound System Market Insight

The Germany portable ultrasound system market is expected to grow at a substantial CAGR, owing to the country’s focus on digitizing healthcare and improving diagnostic efficiency. Germany's aging population and high rates of cardiovascular and musculoskeletal disorders are creating demand for fast, accurate, bedside imaging. Furthermore, the increasing shift toward outpatient and community-based diagnostic care aligns with the deployment of lightweight, advanced portable ultrasound systems in both private practices and institutional settings.

Asia-Pacific Portable Ultrasound System Market Insight

The Asia-Pacific portable ultrasound system market is poised to grow at the fastest CAGR during the forecast period of 2025 to 2032, driven by expanding healthcare infrastructure, rising demand for accessible diagnostic tools, and supportive government policies in emerging economies such as China, India, and Indonesia. Portable ultrasound systems are being widely adopted for maternal health, cardiovascular screening, and infectious disease diagnostics. In addition, growing investment in medical device manufacturing and the rising presence of local OEMs are reducing costs and enhancing product availability across diverse healthcare settings.

Japan Portable Ultrasound System Market Insight

The Japan portable ultrasound system market is gaining traction due to its rapidly aging population, high standards for medical technology, and preference for minimally invasive diagnostic methods. The country's well-developed healthcare system is increasingly leveraging portable ultrasound devices in primary care and home visit scenarios. Integration with AI, wireless transmission, and compatibility with smartphones and tablets are key features driving device preference among Japanese clinicians and healthcare providers.

India Portable Ultrasound System Market Insight

2024年,印度便攜式超音波系統市場佔據亞太地區最大收入份額,這得益於其在孕產婦護理、急救服務和遠距醫療推廣計畫中的廣泛應用。 「印度醫療援助計畫」(Ayushman Bharat)和農村遠距醫療計畫等政府主導的舉措,正在鼓勵醫療資源匱乏的地區使用價格實惠的便攜式成像設備。此外,行動診斷車和即時偵測在印度城鄉結合部和農村地區的興起,也持續加速了市場滲透。

便攜式超音波系統市場份額

便攜式超音波系統產業主要由知名公司主導,包括:

- GE醫療(美國)

- Koninklijke Philips NV(荷蘭)

- 西門子醫療股份公司(德國)

- 佳能醫療系統株式會社(日本)

- FUJIFILM Sonosite, Inc.(美國)

- 邁瑞醫療國際有限公司 (中國)

- 三星麥迪遜有限公司(韓國)

- Butterfly Network, Inc.(美國)

- Esaote SPA(義大利)

- 柯尼卡美能達株式會社(日本)

- 深圳市藍韻實業有限公司 (中國)

- Clarius(加拿大)

- Terason 部門,Teratech 公司(美國)

- 啟生醫療科技股份有限公司 (中國)

- Healcerion有限公司(韓國)

- 日立高科技公司(日本)

- ALPINION MEDICAL SYSTEMS 有限公司(韓國)

- Bionet有限公司(韓國)

- KOELIS(法國)

全球便攜式超音波系統市場的最新發展

- 2024年4月,GE醫療推出了Vscan Air SL,這是一款無線手持式超音波系統,專為快速評估心臟和血管而設計。該設備提供清晰的圖像,非常適合即時診斷。

- 2024年3月,飛利浦醫療保健發布了其緊湊型5500CV超音波診斷儀的AI增強功能,擴展了先進的心臟影像功能。這些增強功能旨在透過提高床邊診斷的精準度,為更多患者提供高品質的心臟影像。

- 2024 年 2 月,富士索諾聲推出了 Sonosite Voice Assist,這是一項突破性的語音命令功能,使操作員能夠在無菌或清潔過程中解放雙手控制超音波系統,從而提高工作流程效率和安全性

- 2024年2月,邁瑞醫療國際推出了TE Air無線手持式超音波系統,這是一款輕巧便攜的設備,配備雙頭探頭,適用於多種臨床用途。該系統專為產科、急診和肌肉骨骼應用而設計,特別適用於資源有限的環境。

- 2024年1月,Butterfly Network, Inc. 宣布與比爾及梅琳達蓋茲基金會建立策略夥伴關係,在非洲和南亞醫療資源匱乏的地區部署 Butterfly iQ+ 超音波設備。該計劃旨在為臨床醫生提供價格實惠的 AI 影像工具,以支持孕產婦保健、急診醫學和傳染病診斷。

SKU-

研究方法

数据收集和基准年分析是使用具有大样本量的数据收集模块完成的。该阶段包括通过各种来源和策略获取市场信息或相关数据。它包括提前检查和规划从过去获得的所有数据。它同样包括检查不同信息源中出现的信息不一致。使用市场统计和连贯模型分析和估计市场数据。此外,市场份额分析和关键趋势分析是市场报告中的主要成功因素。要了解更多信息,请请求分析师致电或下拉您的询问。

DBMR 研究团队使用的关键研究方法是数据三角测量,其中包括数据挖掘、数据变量对市场影响的分析和主要(行业专家)验证。数据模型包括供应商定位网格、市场时间线分析、市场概览和指南、公司定位网格、专利分析、定价分析、公司市场份额分析、测量标准、全球与区域和供应商份额分析。要了解有关研究方法的更多信息,请向我们的行业专家咨询。

可定制

Data Bridge Market Research 是高级形成性研究领域的领导者。我们为向现有和新客户提供符合其目标的数据和分析而感到自豪。报告可定制,包括目标品牌的价格趋势分析、了解其他国家的市场(索取国家列表)、临床试验结果数据、文献综述、翻新市场和产品基础分析。目标竞争对手的市场分析可以从基于技术的分析到市场组合策略进行分析。我们可以按照您所需的格式和数据样式添加您需要的任意数量的竞争对手数据。我们的分析师团队还可以为您提供原始 Excel 文件数据透视表(事实手册)中的数据,或者可以帮助您根据报告中的数据集创建演示文稿。