Global Portable Ultrasound System Market

Market Size in USD Billion

USD

2.83 Billion

USD

4.65 Billion

2024

2032

USD

2.83 Billion

USD

4.65 Billion

2024

2032

| 2025 - 2032 | |

| USD 2.83 Billion | |

| USD 4.65 Billion | |

| % | |

|

Portable Ultrasound System Market Size

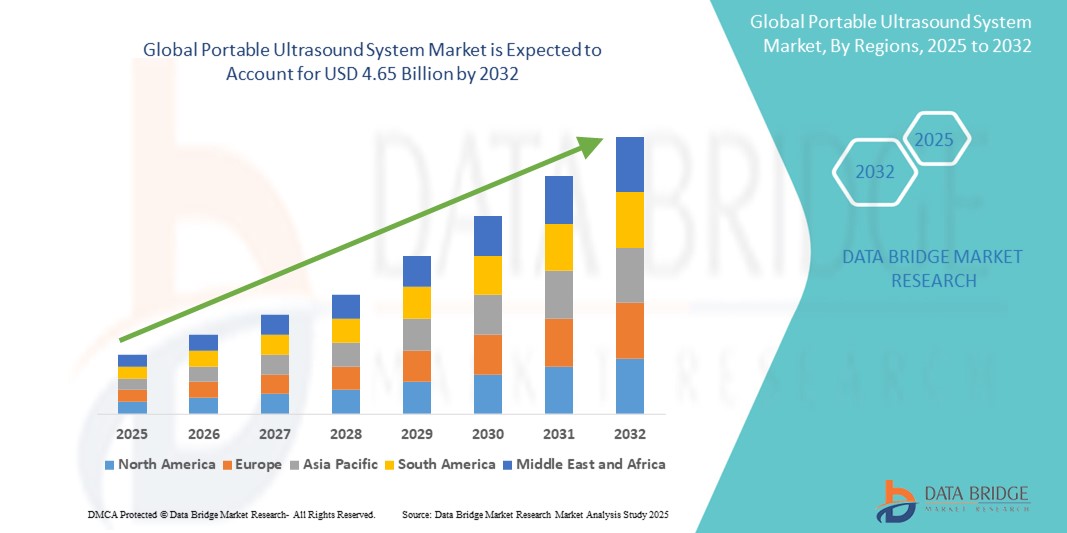

- The global portable ultrasound system market size was valued at USD 2.83 billion in 2024 and is expected to reach USD 4.65 billion by 2032, at a CAGR of 6.36% during the forecast period

- The market growth is largely fueled by the increasing prevalence of chronic diseases, growing geriatric population, and the expanding application of point-of-care diagnostics in both developed and emerging healthcare systems

- Furthermore, the demand for compact, cost-effective, and easy-to-use diagnostic imaging technologies—particularly in remote and resource-limited settings—is positioning portable ultrasound systems as a critical tool in modern healthcare delivery. These converging factors are accelerating the adoption of portable ultrasound solutions, thereby significantly boosting the industry's growth

Portable Ultrasound System Market Analysis

- Portable ultrasound systems, offering compact and mobile diagnostic imaging solutions, are becoming increasingly vital components of point-of-care diagnostics in both hospital and non-hospital settings due to their real-time imaging capability, cost-effectiveness, and ease of use across diverse medical applications such as emergency care, obstetrics, cardiology, and musculoskeletal assessments

- The escalating demand for portable ultrasound systems is primarily fueled by the growing prevalence of chronic and lifestyle-related diseases, a rising geriatric population, and increased need for rapid and accessible diagnostic tools in remote and underserved regions

- North America dominates the portable ultrasound system market with the largest revenue share of 38.2% in 2024, characterized by advanced healthcare infrastructure, high healthcare expenditure, and strong adoption of point-of-care imaging technologies, with the U.S. seeing substantial growth driven by demand in emergency departments, home care, and outpatient settings

- Asia-Pacific is expected to be the fastest growing region in the portable ultrasound system market during the forecast period due to increasing investments in healthcare infrastructure, rapid urbanization, and growing awareness of early diagnosis benefits in rural and semi-urban populations

- Trolley/ cart-based ultrasound systems segment dominates the portable ultrasound system market with a market share of 66.4% in 2024, driven by its superior imaging capabilities, larger screen size, and versatility for use in various clinical settings such as hospitals and diagnostic centers

Report Scope and Portable Ultrasound System Market Segmentation

|

Attributes |

Portable Ultrasound System Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Portable Ultrasound System Market Trends

“Advancements in AI-Enabled Imaging and Wireless Connectivity”

- A significant and accelerating trend in the global portable ultrasound system market is the integration of artificial intelligence (AI) and enhanced wireless connectivity, enabling more accurate image analysis, faster diagnostics, and improved workflow efficiency across diverse clinical settings

- For instance, Philips’ Lumify portable ultrasound system incorporates AI-driven image optimization and remote collaboration features, allowing clinicians to perform high-quality scans and consult specialists in real-time via mobile devices. Similarly, Butterfly Network’s handheld ultrasound uses AI algorithms to assist in image interpretation, improving diagnostic confidence for non-expert users

- AI integration in portable ultrasound systems supports automated measurements, anomaly detection, and adaptive imaging protocols tailored to patient-specific characteristics, thereby reducing operator dependency and enhancing diagnostic accuracy. Wireless connectivity enables seamless transfer of images and data to electronic health records (EHRs) and facilitates telemedicine applications, especially in remote and resource-limited areas.

- The convergence of AI and wireless technologies also facilitates the development of cloud-based platforms for centralized data management, remote training, and continuous software updates, promoting greater accessibility and cost-effectiveness

- This trend towards smarter, connected, and user-friendly portable ultrasound devices is reshaping clinical workflows and expanding the adoption of point-of-care ultrasound across emergency medicine, primary care, and rural healthcare. Companies such as GE Healthcare are investing in AI-enabled ultrasound solutions that provide automated organ segmentation and real-time guidance for needle placements

- The demand for portable ultrasound systems with integrated AI and wireless connectivity is growing rapidly across hospitals, outpatient clinics, and home healthcare, driven by the need for timely, accurate, and accessible diagnostic imaging

Portable Ultrasound System Market Dynamics

Driver

“Rising Demand Driven by Growing Chronic Diseases and Point-of-Care Diagnostics”

- The increasing prevalence of chronic diseases such as cardiovascular disorders, cancer, and diabetes, along with a rising geriatric population, is a significant driver fueling the demand for portable ultrasound systems globally

- For instance, in March 2024, Butterfly Network expanded its AI-powered handheld ultrasound platform to enhance point-of-care imaging capabilities in emergency and outpatient settings, highlighting how technological advancements by leading companies are expected to accelerate market growth during the forecast period

- As healthcare providers seek faster and more accessible diagnostic solutions, portable ultrasound systems offer real-time imaging, ease of use, and cost-effectiveness compared to traditional stationary ultrasound machines, making them highly desirable in both hospital and remote clinical environments

- Furthermore, the growing emphasis on early diagnosis and minimally invasive procedures is driving adoption of portable ultrasound systems, as they enable clinicians to perform bedside imaging with reduced patient movement and faster decision-making

- The convenience of portable, lightweight devices, combined with wireless connectivity and integration with mobile platforms for remote consultation and data sharing, is expanding the application of ultrasound beyond conventional radiology departments, into emergency rooms, ambulances, and rural healthcare centers. The increasing availability of user-friendly devices and telemedicine initiatives further propel market growth across diverse healthcare settings

Restraint/Challenge

“Concerns Regarding Data Security and High Initial Investment Costs”

- Concerns surrounding data security and privacy vulnerabilities associated with connected medical devices, including portable ultrasound systems, pose a significant challenge to broader market adoption. As these systems often rely on wireless connectivity and cloud-based data storage, they are susceptible to cyberattacks and unauthorized access, raising apprehensions among healthcare providers and patients about the safety of sensitive medical information

- For instance, reports of data breaches in healthcare networks have made some institutions cautious in deploying connected diagnostic devices without robust security protocols in place

- Addressing these data security concerns through stringent encryption, secure user authentication, and compliance with healthcare regulations such as HIPAA and GDPR is crucial for building trust among end-users. Companies such as GE Healthcare and Philips emphasize their commitment to cybersecurity by incorporating advanced protective measures and regular software updates in their ultrasound solutions. In addition, the relatively high initial cost of portable ultrasound systems, especially advanced models with AI capabilities and wireless connectivity, can be a barrier for smaller clinics and healthcare providers in developing regions

- While more affordable handheld and cart-based systems are becoming available, premium features such as 3D/4D imaging and integrated AI analysis often come with higher price tags, which may limit widespread adoption in cost-sensitive markets

- Overcoming these challenges through enhanced cybersecurity measures, educating healthcare providers on best practices for device security, and the development of cost-effective portable ultrasound options will be vital for sustained market growth

Portable Ultrasound System Market Scope

The market is segmented on the basis of type of device, application, technology, device display, system portability, and end user.

- By Type Of Device

On the basis of device type, the market is segmented into mobile ultrasound devices and hand-held ultrasound devices. The mobile ultrasound device segment dominates the market in 2024, due to its high versatility, wide acceptance across multiple clinical settings, and superior imaging capabilities compared to smaller devices. Mobile devices are commonly used in hospitals and diagnostic centers where portability combined with robust imaging features is required.

The hand-held ultrasound device segment is expected to witness the fastest growth during the forecast period, driven by their extremely compact design, ease of use in emergency or point-of-care scenarios, and rising demand for on-the-go diagnostics. Advances in battery technology and wireless connectivity further fuel this segment’s rapid adoption in ambulatory care, remote locations, and home healthcare services.

- By Application

On the basis of application, the market segments include radiology, cardiology, gynecology, vascular applications, urological applications, orthopedic and musculoskeletal applications, and others. The radiology segment dominates the market in 2024, as ultrasound imaging remains a primary diagnostic tool across a broad range of radiological examinations. Its widespread use in disease diagnosis, cancer detection, and organ imaging secures a substantial market share.

The cardiology segment is expected to grow at the fastest rate during forecast period, owing to the increasing incidence of cardiovascular diseases worldwide and the development of portable echocardiography systems that facilitate rapid, bedside cardiac assessments. Growing awareness of cardiac health and preventive screening also propels growth in this segment.

- By Technology

On the basis of technology, the market is divided into diagnostic ultrasound and therapeutic ultrasound. The diagnostic ultrasound segment dominates the market in 2024, supported by its critical role in non-invasive imaging, early disease detection, and wide acceptance across clinical fields. Diagnostic ultrasound benefits from continual innovations such as 3D/4D imaging and Doppler technologies that enhance clinical outcomes.

The therapeutic ultrasound segment is projected to grow the fastest during the forecast period, driven by increasing use in physiotherapy, pain management, and rehabilitation treatments. Growing interest in non-invasive therapeutic modalities and advancements in focused ultrasound technology are key factors behind this segment’s robust growth trajectory.

- By Device Display

On the basis of device display, the market is segmented into color ultrasound and black and white (B/W) ultrasound systems. The color ultrasound segment dominates the market in 2024, because color Doppler imaging offers enhanced visualization of blood flow and tissue perfusion, improving diagnostic accuracy in vascular and cardiac applications. This superior imaging quality makes color ultrasound systems the preferred choice in advanced healthcare facilities.

The black and white (B/W) ultrasound segment is expected to grow the fastest during forecast period, especially in emerging and cost-sensitive markets where affordability is critical. Despite lower imaging sophistication, B/W ultrasound devices provide essential diagnostic capabilities and serve as entry-level options in resource-limited settings.

- By Device Portability

On the basis of system portability, the market is categorized into trolley/cart-based ultrasound systems, compact/handheld ultrasound systems, and point-of-care (POC) ultrasound systems. The trolley/cart-based ultrasound systems segment dominates the market, holding a significant 66.4% share in 2024, due to its comprehensive imaging functions, multi-purpose probes, and wide hospital adoption for various diagnostic workflows. These systems balance portability with high-end features, making them staples in radiology and cardiology departments.

Conversely, the compact/handheld ultrasound systems segment is anticipated to witness the fastest growth during forecast period, propelled by increasing demand for lightweight, portable devices that facilitate bedside diagnostics, emergency response, and telemedicine applications. Technological advances, such as smartphone connectivity and AI-assisted imaging, enhance the appeal and functionality of handheld systems.

- By End User

On the basis of end user, the market is segmented into hospitals, diagnostic centers, ambulatory care centers, maternity centers, surgical centers, and others. The hospitals segment dominates the market in 2024, because hospitals have high patient volumes, varied diagnostic requirements, and the infrastructure to support multiple ultrasound systems across departments. Hospitals also invest heavily in advanced ultrasound technologies for comprehensive care.

On the other hand, the ambulatory care centers segment is expected to grow the fastest during the forecast period, driven by increasing healthcare decentralization, rising outpatient procedures, and a shift towards home-based and community care. Portable ultrasound systems in ambulatory care centers enable faster diagnosis, reduce hospital visits, and support efficient patient management, thereby fueling growth in this segment.

Portable Ultrasound System Market Regional Analysis

- North America dominates the portable ultrasound system market with the largest revenue share of 38.2% in 2024, driven by advanced healthcare infrastructure, high healthcare expenditure, and strong adoption of point-of-care imaging technologies

- Healthcare providers across the U.S. and Canada are increasingly relying on portable ultrasound systems for rapid, bedside diagnostics in emergency, critical care, and outpatient settings. The demand is further fueled by a growing geriatric population, rising incidence of chronic diseases, and the trend toward decentralized and home-based healthcare

- In addition, the presence of leading manufacturers, favorable regulatory policies, and strong investments in telehealth and diagnostic imaging are contributing to the market’s growth. The versatility and mobility of portable ultrasound systems align well with North America's focus on efficiency, precision, and accessibility in patient care, making the region a stronghold for advanced ultrasound adoption

U.S. Portable Ultrasound System Market Insight

The U.S. portable ultrasound system market captured the largest revenue share of 79.4% in 2024 within North America, driven by increasing demand for point-of-care diagnostics and rapid imaging in emergency and critical care settings. The strong presence of advanced healthcare infrastructure, rising preference for non-invasive and real-time imaging tools, and a high prevalence of chronic illnesses fuel the market’s expansion. In addition, technological innovations such as AI-enhanced imaging and wireless connectivity in handheld ultrasound devices further accelerate adoption in hospitals, outpatient facilities, and home care environments.

Europe Portable Ultrasound System Market Insight

The Europe portable ultrasound system market is projected to expand at a robust CAGR during the forecast period, spurred by rising adoption in remote care and diagnostic services across both urban and rural settings. Countries in the region are embracing portable imaging systems to enhance access to diagnostic services, especially in elderly care and general practice. Regulatory support for compact, energy-efficient devices, combined with demand for telemedicine and minimally invasive diagnostics, is driving widespread use in clinics, ambulatory surgical centers, and mobile medical units.

U.K. Portable Ultrasound System Market Insight

The U.K. portable ultrasound system market is anticipated to grow steadily, driven by healthcare reforms aimed at early diagnosis and outpatient care expansion. Demand is increasing for compact, handheld ultrasound tools that can be utilized in both general practice and emergency departments. The U.K.'s National Health Service (NHS) is actively integrating point-of-care ultrasound (POCUS) into primary care settings to reduce hospital burden, and training initiatives are equipping more clinicians with portable ultrasound proficiency to improve patient triage and monitoring.

Germany Portable Ultrasound System Market Insight

The Germany portable ultrasound system market is expected to grow at a substantial CAGR, owing to the country’s focus on digitizing healthcare and improving diagnostic efficiency. Germany's aging population and high rates of cardiovascular and musculoskeletal disorders are creating demand for fast, accurate, bedside imaging. Furthermore, the increasing shift toward outpatient and community-based diagnostic care aligns with the deployment of lightweight, advanced portable ultrasound systems in both private practices and institutional settings.

Asia-Pacific Portable Ultrasound System Market Insight

The Asia-Pacific portable ultrasound system market is poised to grow at the fastest CAGR during the forecast period of 2025 to 2032, driven by expanding healthcare infrastructure, rising demand for accessible diagnostic tools, and supportive government policies in emerging economies such as China, India, and Indonesia. Portable ultrasound systems are being widely adopted for maternal health, cardiovascular screening, and infectious disease diagnostics. In addition, growing investment in medical device manufacturing and the rising presence of local OEMs are reducing costs and enhancing product availability across diverse healthcare settings.

Japan Portable Ultrasound System Market Insight

The Japan portable ultrasound system market is gaining traction due to its rapidly aging population, high standards for medical technology, and preference for minimally invasive diagnostic methods. The country's well-developed healthcare system is increasingly leveraging portable ultrasound devices in primary care and home visit scenarios. Integration with AI, wireless transmission, and compatibility with smartphones and tablets are key features driving device preference among Japanese clinicians and healthcare providers.

India Portable Ultrasound System Market Insight

The India portable ultrasound system market accounted for the largest revenue share in Asia Pacific in 2024, supported by widespread adoption in maternal care, emergency services, and remote health outreach programs. Government-led initiatives such as Ayushman Bharat and rural telemedicine projects are encouraging the use of affordable, portable imaging devices across underserved regions. In addition, the rise of mobile diagnostic vans and point-of-care testing in India’s semi-urban and rural zones continues to accelerate market penetration.

Portable Ultrasound System Market Share

The portable ultrasound system industry is primarily led by well-established companies, including:

- GE HealthCare (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- Siemens Healthineers AG (Germany)

- CANON MEDICAL SYSTEMS CORPORATION (Japan)

- FUJIFILM Sonosite, Inc. (U.S.)

- Mindray Medical International Limited (China)

- Samsung Medison Co., Ltd. (South Korea)

- Butterfly Network, Inc. (U.S.)

- Esaote SPA (Italy)

- Konica Minolta, Inc. (Japan)

- Shenzhen Landwind Industry Co., Ltd. (China)

- Clarius (Canada)

- Terason Division, Teratech Corporation (U.S.)

- Chison Medical Technologies Co., Ltd. (China)

- Healcerion Co., Ltd. (South Korea)

- Hitachi High-Tech Corporation (Japan)

- ALPINION MEDICAL SYSTEMS Co., Ltd. (South Korea)

- Bionet Co., Ltd. (South Korea)

- KOELIS (France)

Latest Developments in Global Portable Ultrasound System Market

- In April 2024, GE HealthCare introduced the Vscan Air SL, a wireless handheld ultrasound system designed for rapid cardiac and vascular assessments. This device offers crystal-clear imaging and is well-suited for point-of-care diagnostics

- In March 2024, Philips Healthcare unveiled AI-powered enhancements for its Compact Ultrasound 5500CV, expanding advanced cardiac imaging capabilities. These enhancements aim to bring high-quality cardiac imaging to more patients through improved diagnostic precision at the bedside

- In February 2024, Fujifilm Sonosite launched the Sonosite Voice Assist, a groundbreaking voice command feature that enables proceduralists to control their ultrasound systems hands-free during sterile or clean procedures, enhancing workflow efficiency and safety

- In February 2024, Mindray Medical International introduced the TE Air Wireless Handheld Ultrasound System, a lightweight, pocket-sized device equipped with dual-head probes for versatile clinical use. The system is tailored for obstetric, emergency, and musculoskeletal applications, especially in resource-limited setting

- In January 2024, Butterfly Network, Inc. announced a strategic partnership with the Bill & Melinda Gates Foundation to deploy Butterfly iQ+ ultrasound devices in underserved regions across Africa and South Asia. This initiative aims to support maternal health, emergency medicine, and infectious disease diagnostics by providing clinicians with affordable, AI-powered imaging tools

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.