Global Influenza Drug Market

حجم السوق بالمليار دولار أمريكي

CAGR :

%

USD

981.68 Billion

USD

1,168.36 Billion

2024

2032

USD

981.68 Billion

USD

1,168.36 Billion

2024

2032

| 2025 –2032 | |

| USD 981.68 Billion | |

| USD 1,168.36 Billion | |

| % | |

|

Global Influenza Drug Market Segmentation, By Type (Influenza A, Influenza B, and Influenza C), Treatment (Vaccines and Drugs), Route of Administration (Oral, Intramuscular, Intradermal, Intranasal, and Intravenous), Age (Pediatrics and Adults), End User (Hospitals, and Home Care), Distribution Channel (Direct Tenders and Retail Sales) - Industry Trends and Forecast to 2032

Influenza Drug Market Size

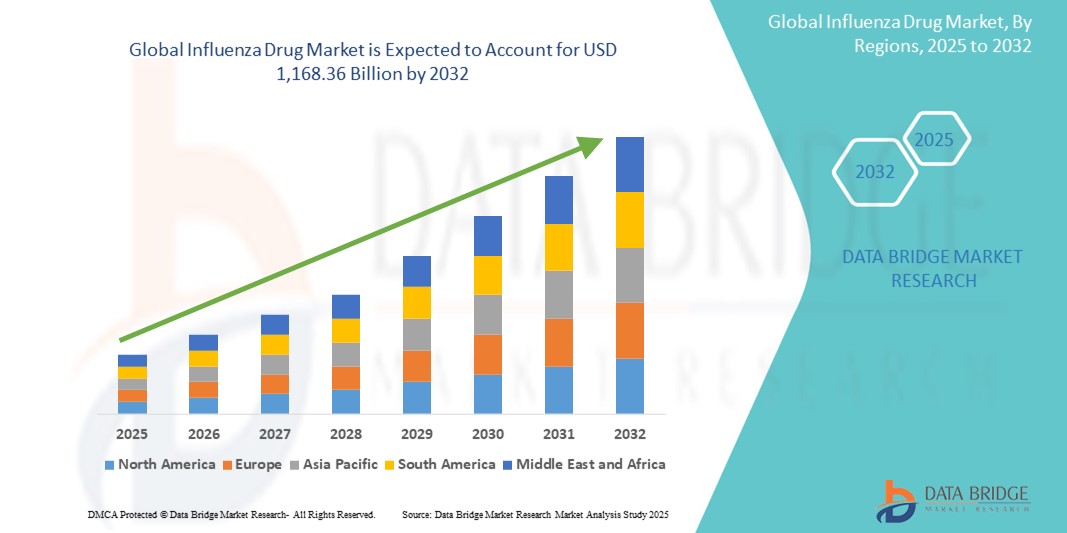

- The global influenza drug market size was valued at USD 981.68 billion in 2024 and is expected to reach USD 1,168.36 billion by 2032, at a CAGR of 2.20% during the forecast period

- The market growth is largely fueled by the growing incidence of seasonal flu and other contagious respiratory illnesses, along with an increasing patient population at risk of developing flu-related complications

- Furthermore, rising investments in research and development activities by pharmaceutical companies and research institutions to develop advanced and improved medications, including novel antiviral drugs and recombinant vaccines, are accelerating the uptake of influenza drug solutions, thereby significantly boosting the industry's growth

Influenza Drug Market Analysis

- The global influenza drug market encompasses a range of antiviral medications and vaccines designed to prevent, treat, and alleviate the symptoms of influenza infections, which pose a significant public health challenge due to their recurrent and seasonal nature, constant viral mutations, and potential for pandemics

- The escalating demand for influenza drugs is primarily fueled by the consistent global prevalence of influenza infections, increasing awareness about the benefits of vaccination, and continuous advancements in pharmaceutical research leading to more effective antiviral therapies and next-generation vaccines

- North America dominates the influenza drug market with the largest revenue share of 60.5% in 2024, characterized by robust healthcare infrastructure, high vaccination coverage rates, and the presence of major pharmaceutical companies. The U.S. experiences strong market growth driven by extensive public health campaigns, government initiatives for pandemic preparedness, and ongoing R&D in novel influenza treatments and vaccines

- Asia-Pacific is expected to be the fastest growing region in the influenza drug market during the forecast period due to increasing awareness about influenza, rising healthcare expenditure, growing urbanization, and a large patient pool susceptible to infections in densely populated countries

- Influenza A segment dominates the influenza drug market with a market share of 47.78% in 2024, driven by its higher mutation rate, wider host range, significant pandemic potential, and increased severity of illness, necessitating more complex vaccination strategies and frequent updates to treatments

Report Scope and Influenza Drug Market Segmentation

|

Attributes |

Influenza Drug Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Influenza Drug Market Trends

“Rising Adoption of Telemedicine and Digital Health Tools”

- A significant and accelerating trend in the global influenza drug market is the increasing integration of telemedicine and digital health tools for influenza management, diagnosis, and prescription. This fusion of technologies is significantly enhancing accessibility to healthcare services, especially for flu patients

- For instance, virtual consultations allow individuals with flu-like symptoms to connect with healthcare professionals from the comfort of their homes, reducing the risk of viral transmission in clinics and hospitals. Telemedicine platforms can facilitate rapid diagnosis based on symptom assessment and guide patients on appropriate self-care or prescription of antiviral medications such as oseltamivir or baloxavir. Approximately 33% of health systems integrate influenza treatment into telemedicine services, enhancing accessibility in rural regions

- Digital health tools, including mobile apps and wearable devices, enable continuous monitoring of physiological parameters that can indicate the onset or progression of influenza. Some smart thermometers, such as those from KINSA, can track aggregate temperature data to identify potential flu hotspots. These technologies can provide early alerts, prompting individuals to seek medical advice sooner, which is crucial for the efficacy of antiviral treatments

- The seamless integration of digital health tools with healthcare systems also supports broader public health surveillance efforts. Data from wearable devices can contribute to real-time influenza surveillance, helping health authorities track outbreaks and allocate resources more effectively. This enhanced surveillance can inform targeted vaccination campaigns and timely distribution of antiviral drugs

- This trend towards more accessible, proactive, and data-driven influenza management is fundamentally reshaping patient engagement and healthcare delivery. Consequently, pharmaceutical companies and healthcare providers are exploring partnerships and developing platforms that leverage these digital capabilities to improve patient outcomes and medication adherence

- The demand for influenza drugs is indirectly boosted by these trends, as telemedicine makes it easier for patients to receive timely prescriptions, and digital monitoring can lead to earlier diagnosis and intervention, maximizing the effectiveness of available treatments

Influenza Drug Market Dynamics

Driver

“Growing Need Due to Consistent Global Prevalence of Influenza and Public Health Initiatives”

- The increasing and consistent global prevalence of seasonal influenza epidemics, coupled with the ongoing threat of pandemic strains and robust public health initiatives, is a significant driver for the heightened demand for influenza drugs and vaccines

- For instance, governments worldwide, including the U.S. and those in Europe and Asia, continually launch extensive vaccination campaigns and invest in national immunization programs to mitigate the impact of annual flu seasons and prepare for potential pandemics. These initiatives, along with increased surveillance and rapid diagnostic advancements, lead to a greater push for vaccination and early treatment with antiviral drugs

- As awareness among the general population and healthcare providers grows regarding the severity of influenza and its potential complications, there's a heightened demand for both preventive and therapeutic solutions. This is particularly true for high-risk populations such as the elderly, young children, and individuals with underlying health conditions

- Furthermore, continuous research and development efforts by pharmaceutical companies to create more effective and broader-spectrum antiviral drugs, as well as next-generation vaccines, are expanding the available treatment landscape and improving the efficacy of existing interventions, thereby propelling market growth

- The necessity for updated vaccine formulations each year due to the constantly evolving nature of influenza viruses ensures a sustained and recurring demand for novel products. This continuous cycle of development, production, and distribution is a key factor propelling the influenza drug market in both developed and emerging economies

Restraint/Challenge

“Challenges of Viral Mutability and Drug Resistance, and High Development Costs”

- A significant challenge to the global influenza drug market is the inherent mutability of influenza viruses, which constantly undergo antigenic drift and shift. This rapid evolution can render existing vaccines less effective and lead to the emergence of antiviral drug resistance, posing a continuous threat to public health

- For instance, the frequent need to update vaccine strains annually necessitates a continuous cycle of research, development, and production, which is both time-consuming and costly. Furthermore, the emergence of drug-resistant strains, such as those resistant to older antivirals such as amantadine or, more recently, some H1N1 viruses showing resistance to oseltamivir (Tamiflu), limits treatment options and complicates clinical management

- Addressing these biological challenges requires significant and sustained investment in R&D for novel antiviral agents with new mechanisms of action and broader-spectrum activity, as well as universal influenza vaccines that can offer long-lasting protection against multiple strains. However, vaccine and drug development is an exceptionally lengthy and expensive process, often taking 10-15 years and costing hundreds of millions to over a billion USD, with a high failure rate

- In addition, logistical challenges, particularly maintaining the "cold chain" for vaccine distribution from manufacturing sites to remote areas, can lead to wastage and reduced efficacy. Factors such as inadequate infrastructure, human error, and power outages in lower-income countries pose significant barriers

- The high initial cost of developing and bringing new influenza drugs and vaccines to market, combined with stringent regulatory approval processes, creates significant hurdles for manufacturers. This often translates to higher prices for advanced treatments, potentially limiting access in price-sensitive markets or for underinsured populations

- Overcoming these challenges through international collaborations, increased public and private funding for R&D, streamlined regulatory pathways, and investment in robust global distribution infrastructures will be vital for sustained market growth and effective pandemic preparedness

Influenza Drug Market Scope

The market is segmented on the basis of type, treatment, route of administration, age, end user, and distribution channel.

- By Type

On the basis of type, the influenza drug market is segmented into influenza A, influenza B, and influenza C. The influenza A segment dominates the market with a market share of 47.78% in 2024, driven by its higher mutation rate, wider host range, significant pandemic potential, and increased severity of illness, necessitating more complex vaccination strategies to control outbreaks. The consistent threat of Influenza A strains such as H1N1 and H3N2 ensures a sustained demand for related drugs and vaccines

Influenza B is expected to witness highest CAGR in market due to its inclusion in quadrivalent vaccines, which offer broader protection against both A and B strains. The increasing awareness of Influenza B's role in seasonal epidemics and the growing emphasis on comprehensive flu prevention strategies are driving demand for more effective vaccines that cover these strains, particularly in vulnerable populations

- By Treatment

On the basis of treatment, the influenza drug market is segmented into vaccines and drugs. The vaccines segment dominates the market with a market share of 87.23% in 2024, due to its pivotal role in preventing illness, reducing transmission, and addressing public health concerns associated with seasonal outbreaks and potential pandemics. Continuous advancements in vaccine technology, including the development of quadrivalent vaccines offering broader protection, further solidify their market leadership

The drugs segment, including antivirals such as oseltamivir and baloxavir, plays a crucial role in treating established infections, with baloxavir marboxil (Xofluza) noted as the fastest-growing drug type due to its single-dose administration and efficacy

- By Route of Administration

On the basis of route of administration, the influenza drug market is segmented into oral, intramuscular, intradermal, intranasal, and intravenous. The oral segment is expected to dominate the market with a market share of 45.04% in 2024, primarily driven by its convenience, ease of self-administration, and widespread accessibility for patients in both outpatient and home care settings. Oral antiviral medications are often the first line of treatment for influenza

The intranasal segment is expected to be the fastest-growing route of administration during the forecast period. This is attributed to its non-invasive, needle-free administration, which improves patient compliance, especially in pediatric populations, and its ability to induce both systemic and mucosal immunity

- By Age

On the basis of age, the influenza drug market is segmented into pediatrics and adults. The adult segment is the largest in the influenza market, with a 66.7% share in 2024, propelled by elevated vaccination rates among seniors and individuals with chronic illnesses, who are at higher risk of severe flu complications

The pediatrics segment is poised to grow at a notable CAGR, as young children, particularly those under 5 years, are at higher risk of severe influenza complications, accelerating the market scope for child-friendly formulations and vaccination efforts.

- By End Use

On the basis of end user, the influenza drug market is segmented into hospitals, and home care. The hospitals segment dominates the global influenza drug market with a market share of 72.62% in 2024, largely due to their role in managing severe influenza cases requiring intensive monitoring, intravenous antivirals, and critical care for high-risk patients. Hospitals also serve as key points for vaccination drives

The home care segment is expected to witness the fastest compound annual growth rate (CAGR) from 2025 to 2032 in the global influenza drug market, driven by the increasing preference for at-home treatment options, advancements in telemedicine, and the growing adoption of home healthcare services. These factors enable patients to manage influenza symptoms effectively within the comfort of their homes, reducing the need for hospitalization and minimizing exposure to healthcare facilities.

- By Distribution Channel

On the basis of distribution channel, the global influenza drug market is segmented into direct tenders and retail sales. The direct tenders segment is projected to dominate the global influenza drug market with the largest market share of 56.34% in 2024, primarily driven by large-scale procurement of vaccines and antiviral drugs by governments and public health organizations for national immunization programs and strategic stockpiling. This channel ensures bulk purchasing and efficient distribution for mass vaccination campaigns.

The retail sales segment is also a dominant channel, acting as key access points for both vaccines and over-the-counter and prescription treatments for the general public, and is expected to see significant growth, particularly through online pharmacies due to convenience and accessibility.

Influenza Drug Market Regional Analysis

- North America dominates the influenza drug market with the largest revenue share of 60.5% in 2024, driven by robust healthcare infrastructure, high vaccination coverage rates, and the presence of major pharmaceutical companies

- يولي المستهلكون في المنطقة أهمية كبيرة للرعاية الصحية الوقائية ويسهل الوصول إلى اللقاحات والعلاجات المضادة للفيروسات

- ويتم دعم هذا التبني الواسع النطاق من خلال سياسات السداد المواتية، والسكان المتقدمين من الناحية التكنولوجية، والتركيز المتزايد على مبادرات الصحة العامة، مما يجعل أدوية الإنفلونزا عنصراً أساسياً في إدارة الأمراض الموسمية.

نظرة على سوق أدوية الإنفلونزا في الولايات المتحدة

استحوذ سوق أدوية الإنفلونزا في الولايات المتحدة على أكبر حصة من الإيرادات في أمريكا الشمالية، بنسبة 56.2% في عام 2024، مما يعكس تطور نظام الرعاية الصحية في البلاد واستراتيجيات الصحة العامة الاستباقية. تُعدّ الولايات المتحدة محركًا رئيسيًا لسوق الإنفلونزا نظرًا لارتفاع معدلات الإصابة بالإنفلونزا الموسمية، وبرامج التطعيم القوية، والاستثمار المستمر في البحث والتطوير لعلاجات ولقاحات جديدة. يُولي المستهلكون أولوية متزايدة للتدابير الوقائية، ويسهل الحصول على أدوية الإنفلونزا. ويساهم التكامل القوي لتوصيات الصحة العامة، والتوافر الواسع للقاحات والأدوية المضادة للفيروسات، والعدد الكبير من المرضى، في استدامة الطلب.

نظرة على سوق أدوية الإنفلونزا في أوروبا

من المتوقع أن يشهد سوق أدوية الإنفلونزا في أوروبا نموًا بمعدل نمو سنوي مركب قدره 2.5% خلال الفترة المتوقعة، مدفوعًا بشكل رئيسي بالمبادرات الحكومية الراسخة للتطعيم ضد الإنفلونزا وعلاجه، وإرشادات الصحة العامة الصارمة، وارتفاع معدل الإصابة بالإنفلونزا الموسمية. ويساهم تركيز المنطقة على الرعاية الصحية الوقائية، إلى جانب البنية التحتية المتطورة للرعاية الصحية وزيادة الوعي بمضاعفات الإنفلونزا، في تعزيز اعتماد أدوية الإنفلونزا. وتشهد الدول الأوروبية طلبًا مستمرًا على كل من اللقاحات والعلاجات المضادة للفيروسات استجابةً لتفشي الأمراض سنويًا.

نظرة على سوق أدوية الإنفلونزا في المملكة المتحدة

من المتوقع أن ينمو سوق أدوية الإنفلونزا في المملكة المتحدة بمعدل نمو سنوي مركب ملحوظ خلال فترة التوقعات، مدفوعًا ببرامج التطعيم الحكومية القوية، والتركيز المتزايد على الصحة العامة، والرغبة في تعزيز الحماية من الإنفلونزا الموسمية. ويشجع نظام الرعاية الصحية الراسخ في المملكة المتحدة، والتوصيات القوية بتطعيم الإنفلونزا سنويًا، على الإقبال الكبير على اللقاحات والعلاجات المضادة للفيروسات بين السكان. كما أن التزام المملكة المتحدة بمبادرات الصحة العامة يُحفز نمو السوق بشكل أكبر.

نظرة على سوق أدوية الإنفلونزا في ألمانيا

من المتوقع أن يشهد سوق أدوية الإنفلونزا في ألمانيا نموًا بمعدل نمو سنوي مركب كبير خلال فترة التوقعات، مدفوعًا بتزايد الوعي بأمن الصحة العامة، والتركيز القوي على الطب الوقائي، والطلب على الحلول التكنولوجية المتقدمة. تُعزز البنية التحتية المتطورة للرعاية الصحية في ألمانيا، إلى جانب تركيزها على معدلات التطعيم العالية والإدارة الفعالة للأمراض، اعتماد أدوية الإنفلونزا، لا سيما في كل من الطب العام والمستشفيات. ويتماشى دمج التشخيصات المتقدمة وتفضيل العلاجات القائمة على الأدلة مع توقعات المستهلكين المحليين والقطاع الطبي.

نظرة عامة على سوق أدوية الإنفلونزا في منطقة آسيا والمحيط الهادئ

من المتوقع أن يشهد سوق أدوية الإنفلونزا في منطقة آسيا والمحيط الهادئ نموًا بأسرع معدل نمو سنوي مركب خلال الفترة المتوقعة، مدفوعًا بالتوسع الحضري المتزايد، وارتفاع الدخل المتاح، والتقدم التكنولوجي في مجال الرعاية الصحية في دول مثل الصين واليابان والهند. يُعدّ التعداد السكاني الكبير والمتزايد في المنطقة عرضة بشكل كبير لتفشي الإنفلونزا، مما يؤدي إلى زيادة الوعي والطلب على العلاجات واللقاحات الفعالة. علاوة على ذلك، ومع توسع منطقة آسيا والمحيط الهادئ في بنيتها التحتية للرعاية الصحية، وتعزيز المبادرات الحكومية لتوفير الأدوية الأساسية على نطاق أوسع، فإن أسعار أدوية الإنفلونزا وسهولة الحصول عليها تتسع لتشمل قاعدة مستهلكين أوسع.

نظرة على سوق أدوية الإنفلونزا في اليابان

يشهد سوق أدوية الإنفلونزا في اليابان زخمًا متزايدًا في مجال الأدوية المضادة للفيروسات، نظرًا لارتفاع معدل الإصابة بالإنفلونزا الموسمية في البلاد، والتوسع العمراني السريع، والطلب القوي على خيارات العلاج الفعالة. ويولي السوق الياباني اهتمامًا بالغًا بالصحة العامة وتغطية اللقاحات، ويعود اعتماد أدوية الإنفلونزا إلى تزايد الوعي بالمضاعفات، لا سيما بين كبار السن. ويساهم دمج الأدوية المضادة للفيروسات المتقدمة وجهود البحث والتطوير المستمرة في تعزيز النمو، حيث تولي اليابان الأولوية للحد من عبء الإنفلونزا.

نظرة على سوق أدوية الإنفلونزا في الهند

استحوذ سوق أدوية الإنفلونزا في الهند على حصة سوقية كبيرة في منطقة آسيا والمحيط الهادئ عام 2024، ويعزى ذلك إلى توسع الطبقة المتوسطة في البلاد، والتوسع الحضري السريع، وتزايد فرص الحصول على الرعاية الصحية. تُعدّ الهند سوقًا كبيرةً تعاني من عبءٍ كبيرٍ من الأمراض المعدية، وتزداد أهمية أدوية الإنفلونزا في كلٍّ من برامج الصحة العامة والرعاية الصحية الخاصة. ويُعدّ السعي نحو تحسين البنية التحتية للرعاية الصحية، وتوافر أدوية الإنفلونزا المصنعة محليًا والمستوردة، من العوامل الرئيسية التي تدفع السوق في الهند، بمعدل نمو سنوي مركب متوقع يبلغ 2.6%.

حصة سوق أدوية الإنفلونزا

وتدار صناعة أدوية الإنفلونزا بشكل أساسي من قبل شركات راسخة، بما في ذلك:

- شركة AbbVie Inc. (الولايات المتحدة)

- أسترازينيكا (المملكة المتحدة)

- بيونتيك إس إي (ألمانيا)

- شركة بريستول مايرز سكويب (الولايات المتحدة)

- سيبلا (الهند)

- شركة كوكريستال فارما (الولايات المتحدة)

- CSL (المملكة المتحدة)

- شركة داييتشي سانكيو المحدودة (اليابان)

- مختبرات الدكتور ريدي المحدودة (الهند)

- F. هوفمان-لاروش (سويسرا)

- شركة جيلياد للعلوم (الولايات المتحدة)

- شركة جلاكسو سميث كلاين (المملكة المتحدة)

- شركة جونسون آند جونسون للخدمات، المحدودة (الولايات المتحدة)

- شركة ميرك وشركاه المحدودة (الولايات المتحدة)

- شركة موديرنا (الولايات المتحدة)

- شركة نوفارتيس إيه جي (سويسرا)

- نوفافاكس (الولايات المتحدة)

- أوسيفاكس (فرنسا)

- سانوفي إس إيه (فرنسا)

أحدث التطورات في سوق أدوية الإنفلونزا العالمية

- في سبتمبر 2024، تمت الموافقة على لقاح فلوميست من أسترازينيكا للاستخدام الذاتي في الولايات المتحدة. ويمثل هذا تقدمًا كبيرًا، إذ يُعد أول لقاح إنفلونزا لا يتطلب إعطاءه من قِبل مقدم رعاية صحية، مما يُعزز سهولة الوصول إليه وراحته للأفراد الذين يسعون للوقاية من الإنفلونزا. وقد وافقت إدارة الغذاء والدواء الأمريكية على لقاح فلوميست للاستخدام الذاتي للبالغين حتى سن 49 عامًا، أو من قِبل أحد الوالدين/مقدمي الرعاية للأفراد الذين تتراوح أعمارهم بين 2 و17 عامًا.

- في أغسطس 2024، طوّر علماء من كلية الطب بجامعة هارفارد بخاخًا أنفيًا يُسمى بخاخ التقاط وتحييد مسببات الأمراض (PCANS)، أو Profi. يُزعم أن هذا البخاخ يحمي من الإنفلونزا ونزلات البرد وكوفيد-19 بفعالية تزيد عن 99.99%، وذلك من خلال تكوين حاجز في تجويف الأنف يلتقط الفيروسات والبكتيريا ويُحيّدها.

- في مايو 2024، أعلنت سانوفي ونوفافاكس عن اتفاقية ترخيص حصرية مشتركة للتسويق المشترك للقاح كوفيد-19 المُضاف إليه مواد مساعدة من نوفافاكس حاليًا في جميع أنحاء العالم، وتطوير لقاح مُركّب جديد للإنفلونزا وكوفيد-19. تهدف هذه الشراكة إلى تسريع تطوير اللقاحات المُركّبة، مما يوفر راحةً وحمايةً مُحسّنتين للمرضى.

- في أبريل 2023، أعلنت شركة سينوفاك بيوتيك المحدودة عن بدء تشغيل مصنعها الجديد لتصنيع لقاحات الإنفلونزا في بكين. يُعزز هذا التوسع الطاقة الإنتاجية العالمية للقاحات الإنفلونزا، مما يُسهم في زيادة توافرها وتوريدها.

- في مارس 2023، انعقدت اللجنة الاستشارية للقاحات والمنتجات البيولوجية ذات الصلة التابعة لإدارة الغذاء والدواء الأمريكية (VRBPAC) لتحديد تركيبة اللقاح لموسم الإنفلونزا الأمريكي 2023-2024. تُعد هذه العملية السنوية بالغة الأهمية لضمان فعالية اللقاحات ضد سلالات فيروسات الإنفلونزا المنتشرة.

SKU-

احصل على إمكانية الوصول عبر الإنترنت إلى التقرير الخاص بأول سحابة استخبارات سوقية في العالم

- لوحة معلومات تحليل البيانات التفاعلية

- لوحة معلومات تحليل الشركة للفرص ذات إمكانات النمو العالية

- إمكانية وصول محلل الأبحاث للتخصيص والاستعلامات

- تحليل المنافسين باستخدام لوحة معلومات تفاعلية

- آخر الأخبار والتحديثات وتحليل الاتجاهات

- استغل قوة تحليل المعايير لتتبع المنافسين بشكل شامل

منهجية البحث

يتم جمع البيانات وتحليل سنة الأساس باستخدام وحدات جمع البيانات ذات أحجام العينات الكبيرة. تتضمن المرحلة الحصول على معلومات السوق أو البيانات ذات الصلة من خلال مصادر واستراتيجيات مختلفة. تتضمن فحص وتخطيط جميع البيانات المكتسبة من الماضي مسبقًا. كما تتضمن فحص التناقضات في المعلومات التي شوهدت عبر مصادر المعلومات المختلفة. يتم تحليل بيانات السوق وتقديرها باستخدام نماذج إحصائية ومتماسكة للسوق. كما أن تحليل حصة السوق وتحليل الاتجاهات الرئيسية هي عوامل النجاح الرئيسية في تقرير السوق. لمعرفة المزيد، يرجى طلب مكالمة محلل أو إرسال استفسارك.

منهجية البحث الرئيسية التي يستخدمها فريق بحث DBMR هي التثليث البيانات والتي تتضمن استخراج البيانات وتحليل تأثير متغيرات البيانات على السوق والتحقق الأولي (من قبل خبراء الصناعة). تتضمن نماذج البيانات شبكة تحديد موقف البائعين، وتحليل خط زمني للسوق، ونظرة عامة على السوق ودليل، وشبكة تحديد موقف الشركة، وتحليل براءات الاختراع، وتحليل التسعير، وتحليل حصة الشركة في السوق، ومعايير القياس، وتحليل حصة البائعين على المستوى العالمي مقابل الإقليمي. لمعرفة المزيد عن منهجية البحث، أرسل استفسارًا للتحدث إلى خبراء الصناعة لدينا.

التخصيص متاح

تعد Data Bridge Market Research رائدة في مجال البحوث التكوينية المتقدمة. ونحن نفخر بخدمة عملائنا الحاليين والجدد بالبيانات والتحليلات التي تتطابق مع هدفهم. ويمكن تخصيص التقرير ليشمل تحليل اتجاه الأسعار للعلامات التجارية المستهدفة وفهم السوق في بلدان إضافية (اطلب قائمة البلدان)، وبيانات نتائج التجارب السريرية، ومراجعة الأدبيات، وتحليل السوق المجدد وقاعدة المنتج. ويمكن تحليل تحليل السوق للمنافسين المستهدفين من التحليل القائم على التكنولوجيا إلى استراتيجيات محفظة السوق. ويمكننا إضافة عدد كبير من المنافسين الذين تحتاج إلى بيانات عنهم بالتنسيق وأسلوب البيانات الذي تبحث عنه. ويمكن لفريق المحللين لدينا أيضًا تزويدك بالبيانات في ملفات Excel الخام أو جداول البيانات المحورية (كتاب الحقائق) أو مساعدتك في إنشاء عروض تقديمية من مجموعات البيانات المتوفرة في التقرير.