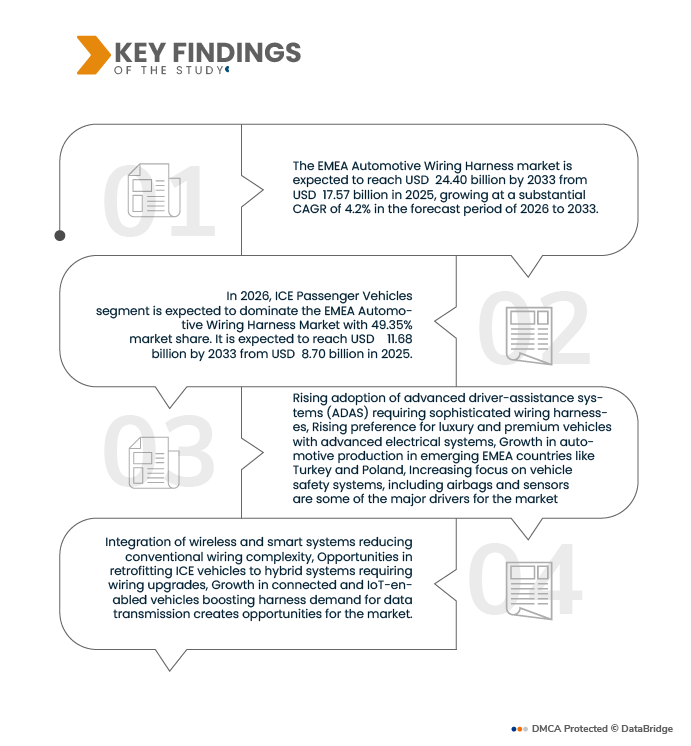

The rising adoption of advanced driver-assistance systems (ADAS) is a key driver for the EMEA automotive wiring harness market, as modern vehicles increasingly rely on electronic architectures to enhance safety, automation, and driving comfort. ADAS features such as adaptive cruise control, lane-keeping assist, automatic emergency braking, parking assistance, and driver monitoring systems require continuous communication between sensors, cameras, radar modules, control units, and actuators. Wiring harnesses serve as the critical backbone that enables high-speed data transmission and reliable power distribution among these components.

In the EMEA region, stringent vehicle safety regulations and growing consumer preference for technologically advanced vehicles are accelerating OEM integration of ADAS across both premium and mid-range vehicle segments. This shift significantly increases the complexity, density, and customization requirements of wiring harness systems, including the need for high-performance connectors, shielded cables, and lightweight designs to maintain vehicle efficiency. Additionally, the transition toward semi-autonomous driving capabilities is expanding the number of electronic control units (ECUs) within vehicles, further driving demand for advanced harness configurations. As automakers focus on improving safety ratings and meeting regulatory compliance, suppliers are witnessing increased demand for durable, high-bandwidth, and scalable wiring solutions,

reinforcing ADAS adoption as a major growth catalyst for the EMEA automotive wiring harness market.

Access Full Report @ https://www.databridgemarketresearch.com/reports/emea-automotive-wiring-harness-market

Data Bridge market research analyzes that the EMEA Automotive Wiring Harness Market is expected to reach USD 24.40 billion by 2033 from USD 17.57 billion in 2025, growing with a CAGR of 4.2% in the forecast period of 2026 to 2033.

Key Findings of the Study

Rising Preference for Luxury and Premium Vehicles with Advanced Electrical Systems

The rising preference for luxury and premium vehicles across the EMEA region is a significant driver for the automotive wiring harness market, as these vehicles incorporate a substantially higher number of electronic and

electrical components compared to conventional models. Premium vehicles are increasingly equipped with advanced features such as digital instrument clusters, multi-zone climate control systems, ambient lighting, power-adjustable seats, advanced infotainment systems, driver monitoring technologies, and enhanced safety functionalities. Each of these features requires dedicated electrical connectivity, increasing the complexity, length, and value of wiring harness systems per vehicle.

In Europe, strong consumer demand for technologically advanced and comfort-oriented vehicles, particularly in countries such as Germany, the U.K., and France, is accelerating the integration of sophisticated electronic architectures. Additionally, luxury automakers are adopting high-performance computing platforms and centralized electronic control units, which require highly reliable and high-capacity wiring solutions to ensure seamless communication between sensors, controllers, and onboard systems. The shift toward electrified luxury vehicles further intensifies this demand, as premium electric models require high-voltage harnesses for battery systems and power distribution. Consequently, the growing production and sales of premium vehicles directly increase wiring harness content per vehicle, supporting sustained market expansion across the EMEA automotive ecosystem.

Report Scope and Market Segmentation

|

Report Metric

|

Details

|

|

Forecast Period

|

2026 to 2033

|

|

Base Year

|

2025

|

|

Historic Years

|

2024 (Customizable to 2018-2023)

|

|

Quantitative Units

|

Revenue in USD billion

|

|

Segments Covered

|

By Vehicle Type (ICE Passenger Vehicles, ICE Commercial Vehicles, Electric & Hybrid Vehicles), Application (Engine, Body & Chassis, Powertrain, Infotainment & Telematics, Safety Systems, Lighting System, Battery Management System), Core Design (Low Voltage Wiring Harness, High Voltage Wiring Harness, Shielded Wiring Harness, Unshielded Wiring Harness), Material (Copper, Insulation Materials, Aluminum, Fiber Optic), Conductor Type (M Single-Core, Multi-Core), Form (Standard Wiring Harness, Modular Wiring Harness), By End Connector Type (Pin Connector, Sealed Connector, Socket Connector, Blade Connector, Non-Sealed Connector, Terminal Block, Specialty Connectors), Installation Type (OEM, Aftermarket), Vehicle Electrical Architecture (Conventional Wiring Architecture, Distributed And Smart Wiring Architecture), End Use (OEM Vehicle Manufacturers, Aftermarket Service Providers), Distribution Channel (Offline, Online)

|

|

Countries Covered

|

Europe

Middle East & Africa

|

|

Market Players Covered

|

|

|

Data Points Covered in the Report

|

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis.

|

Segment Analysis

The EMEA Automotive Wiring Harness Market is segmented into eleven notable segments based on vehicle type, application, core design, material, conductor type, form, end connector type, installation type, vehicle electrical architecture, end use, distribution channel.

- On the basis of Vehicle Type, the EMEA Automotive Wiring Harness Market is segmented into ICE Passenger Vehicles, ICE Commercial Vehicles, and Electric & Hybrid Vehicles.

In 2026, the ICE Passenger Vehicles segment is expected to dominate the market

In 2026, the ICE Passenger Vehicles segment is expected to dominate the market with share of 49.35% in 2026, due to the large installed vehicle base, stable production volumes, and continued demand for cost-optimized electrical architectures across mass-market vehicle platforms. Wiring harness demand in this segment is supported by the integration of infotainment systems, safety electronics, lighting modules, and comfort features. However, the Electric & Hybrid Vehicles segment is projected to witness the fastest growth, driven by increasing electrification trends across Europe.

- On the basis of Application, the EMEA Automotive Wiring Harness Market is segmented into Engine, Body & Chassis, Powertrain, Infotainment & Telematics, Safety Systems, Lighting System, and Battery Management System.

In 2026, the Engine segment is expected to dominate the market

In 2026, the Engine segment is expected to dominate the market with share of 19.54% in 2026, due to the extensive deployment of wiring harnesses required for engine control units (ECUs), fuel injection systems, ignition modules, emission control components, temperature and pressure sensors, and other critical powertrain electronics. These systems demand reliable electrical connectivity, thermal resistance, and vibration tolerance, which significantly contributes to higher wiring harness content per vehicle.

- On the basis of Core Design, the market is segmented into Low Voltage Wiring Harness, High Voltage Wiring Harness, Shielded Wiring Harness, and Unshielded Wiring Harness.

In 2026, the Low Voltage Wiring Harness segment is expected to dominate the market

In 2026, the Low Voltage Wiring Harness segment is anticipated to dominate the market with share of 45.29% in 2026, as conventional 12V/48V electrical systems remain widely used across ICE and hybrid vehicles. However, demand for High Voltage and Shielded Harnesses is increasing with the expansion of electric vehicle platforms and advanced electronic architectures.

- On the basis of Material, the market is segmented into Copper, Insulation Materials, Aluminum, and Fiber Optic.

In 2026, the Copper segment is expected to dominate the market

In 2026, the Copper segment is expected to dominate the market with share of 72.44% in 2026, due to its superior electrical conductivity, durability, and established supply ecosystem. Nonetheless, aluminum and fiber optic materials are gradually gaining importance as OEMs focus on vehicle lightweighting and high-speed data transmission requirements.

- On the basis of Conductor Type, the EMEA Automotive Wiring Harness Market is segmented into Single-Core and Multi-Core.

In 2026, the Single-Core segment is expected to dominate the market

In 2026, the Single-Core segment is expected to dominate the market with share of 72.96% in 2026, due to its widespread application across conventional vehicle electrical systems, including lighting circuits, basic control modules, and power distribution functions. Single-core conductors offer advantages such as lower cost, easier manufacturing, improved flexibility in routing, and simplified maintenance, making them suitable for high-volume passenger and commercial vehicle production.

- On the basis of Form, the market is segmented into Standard Wiring Harness and Modular Wiring Harness.

In 2026, the Standard Wiring Harness segment is expected to dominate the market

In 2026, the Standard Wiring Harness segment is expected to dominate the market with share in 53.63% in 2026, due to its cost efficiency and widespread adoption across high-volume vehicle production. However, modular harness systems are gaining momentum as automakers aim to simplify assembly processes, improve scalability, and enable platform sharing.

- On the basis of End Connector Type, the EMEA Automotive Wiring Harness Market is segmented into Pin Connector, Sealed Connector, Socket Connector, Blade Connector, Non-Sealed Connector, Terminal Block, and Specialty Connectors.

In 2026, the Pin Connector segment is expected to dominate the market

In 2026, the Pin Connector segment is expected to dominate the market with share 22.63% in 2026, due to its widespread usage across multiple automotive electrical applications, including body electronics, infotainment modules, lighting systems, and control units. Pin connectors offer advantages such as compact design, ease of installation, reliable electrical contact, and cost efficiency, making them highly suitable for high-volume vehicle production.

- On the basis of Installation Type, the market is segmented into OEM and Aftermarket.

In 2026, the OEM segment is expected to dominate the market

In 2026, the OEM segment is expected to dominate the market with share 86.69% in 2026, as wiring harnesses are highly vehicle-specific components that are integrated during vehicle manufacturing. Long-term supply agreements between harness suppliers and automakers further reinforce OEM channel dominance.

- On the basis of Vehicle Electrical Architecture, the market is segmented into Conventional Wiring Architecture and Distributed & Smart Wiring Architecture.

In 2026, the Conventional Wiring Architecture segment is expected to dominate the market

In 2026, the Conventional Wiring Architecture segment is expected to dominate the market with share of 61.68% in 2026, due to its continued use in entry- and mid-segment vehicles. However, distributed and smart architectures are expected to grow steadily with the adoption of zonal electrical systems and software-defined vehicle platforms.

- On the basis of End Use, the market is segmented into OEM Vehicle Manufacturers and Aftermarket Service Providers.

In 2026, the OEM Vehicle Manufacturers segment is expected to dominate the market

In 2026, the OEM Vehicle Manufacturers segment is expected to dominate the market with share of 86.69% in 2026, as most harness demand originates from new vehicle production cycles. Aftermarket demand remains comparatively limited and is largely driven by repair, replacement, and vehicle refurbishment needs.

- On the basis of Distribution Channel, the market is segmented into Offline and Online.

In 2026, the Offline segment is expected to dominate the market

In 2026, the Offline segment is expected to dominate the market with share in 91.26% in 2026, due to the technical complexity of wiring harness systems, which require direct procurement channels, engineering collaboration, and structured supplier integration processes.

Major Players

LEONI AG (Germany), DRÄXLMAIER GROUP (Germany), KROMBERG & SCHUBERT (Germany), NEXANS AUTOELECTRIC (Germany), and COROPLAST FRITZ MÜLLER (Germany)

Market Developments

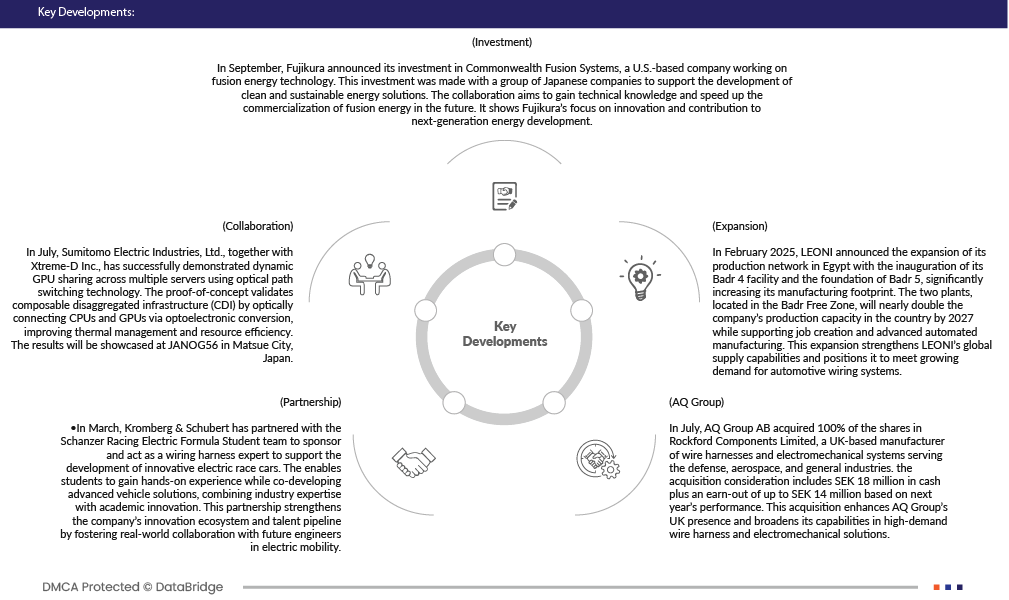

- In February 2025, LEONI announced the expansion of its production network in Egypt with the inauguration of its Badr 4 facility and the foundation of Badr 5, significantly increasing its manufacturing footprint. The two plants, located in the Badr Free Zone, will nearly double the company’s production capacity in the country by 2027 while supporting job creation and advanced automated manufacturing. This expansion strengthens LEONI’s global supply capabilities and positions it to meet growing demand for automotive wiring systems.

- In March 2025, Kromberg & Schubert has partnered with the Schanzer Racing Electric Formula Student team to sponsor and act as a wiring harness expert to support the development of innovative electric race cars. The enables students to gain hands-on experience while co-developing advanced vehicle solutions, combining industry expertise with academic innovation. This partnership strengthens the company’s innovation ecosystem and talent pipeline by fostering real-world collaboration with future engineers in electric mobility.

- In October 2024, DRÄXLMAIER Group showcased its latest innovations in low-voltage architectures, 2024 Innovation systems, high-voltage and battery technologies at the International Suppliers Fair (IZB) 2024 under the theme “Inspiring the Transformation.” The company highlighted advanced wiring harness systems for semiautonomous driving, optimized charging solutions, and integrated battery systems aimed at improving efficiency, safety, and performance in next-generation electric mobility. This showcase reinforces DRÄXLMAIER’s position as a key innovation partner for premium automakers in the transition toward electrified and connected mobility solutions.

- In January 2026, Aptiv’s new Wuhan factory main structure has been successfully topped out, marking a key construction milestone as the facility progresses toward production. The plant part of Aptiv’s global expansion in e‐mobility and advanced vehicle technologies is scheduled to begin operations in later half of 2026, where it will manufacture high‐voltage cable systems and other electrification components. This development strengthens Aptiv’s manufacturing footprint in China.

- In July 2025, Sumitomo Electric Industries, Ltd., together with Xtreme-D Inc., has successfully demonstrated dynamic GPU sharing across multiple servers using optical path technology. The proof-of-concept validates composable disaggregated infrastructure switching (CDI) by optically connecting CPUs and GPUs via optoelectronic conversion, improving thermal management and resource efficiency.

As per Data Bridge Market Research analysis:

For more detailed information about the EMEA Automotive Wiring Harness Market report, click here – https://www.databridgemarketresearch.com/reports/emea-automotive-wiring-harness-market