ヨーロッパの印刷インキ/包装インキ市場の規模、シェア、トレンド分析レポート

Market Size in USD Billion

CAGR :

%

USD

3.11 Billion

USD

5.19 Billion

2025

2033

USD

3.11 Billion

USD

5.19 Billion

2025

2033

| 2026 –2033 | |

| USD 3.11 Billion | |

| USD 5.19 Billion | |

| % | |

|

ヨーロッパの印刷インキ/包装インキ市場の細分化、技術別(溶剤型、油性、水性、UV硬化型、LED硬化型、EB硬化型、その他)、タイプ別(フレキソインキ、オフセットインキ、グラビアインキ、ジェットインキ、金属装飾インキ、セキュリティインキ、その他)、樹脂別(ポリウレタン、アクリル、ビニル、ポリアミド、ポリケトン、ニトロセルロース、その他)、基材別(紙および板紙、ポリエチレン、アルミニウム、ポリ塩化ビニル、ポリプロピレン、ポリ酢酸ビニル、ポリオレフィン、セロハン、ポリエステル、ナイロン、その他)、用途別(食品包装、壁紙、段ボールおよび土壌ボード、パネル、ラベル、ラミネート、キャリアバッグ、アルミホイル、シュリンクラップフィルム、封筒、紙合成フィルム、包装紙、頑丈な袋、冷凍包装、衛生包装、フラワーラップ、その他)その他) - 2033年までの業界動向と予測

ヨーロッパの印刷インキ/包装インキ市場規模

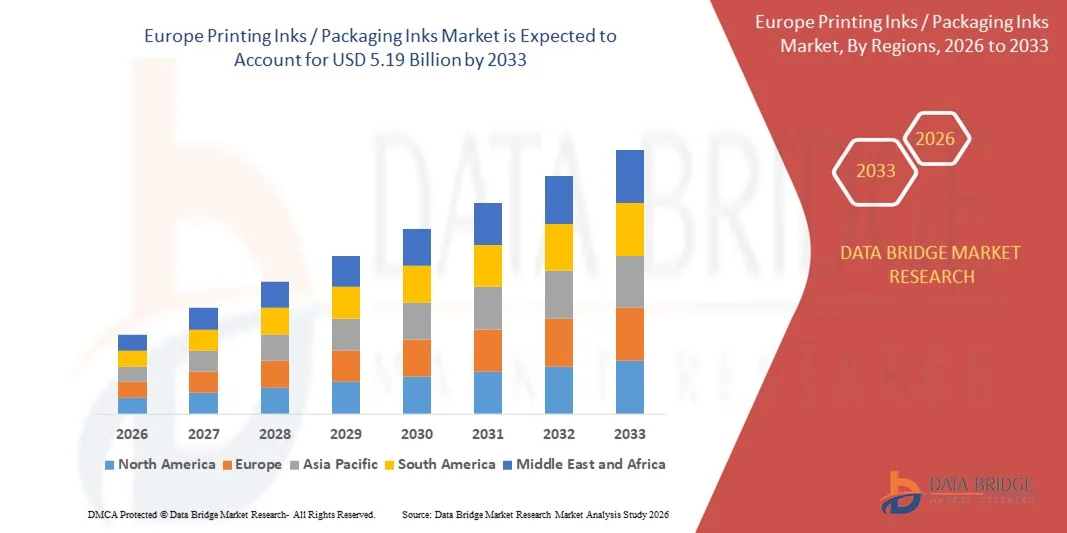

- ヨーロッパの印刷インク/包装インク市場規模は2025年に31億1000万米ドルと評価され、予測期間中に6.6%のCAGRで成長し、2033年までに51億9000万米ドルに達すると予想されています。

- 市場の成長は、包装および印刷業界における高品質で持続可能かつ環境に優しいインクの需要の増加によって主に推進されており、水性、UV硬化型、低VOCインク技術の革新を推進しています。

- さらに、見た目が魅力的で、耐久性があり、食品に安全な包装に対する消費者の嗜好が高まっているため、メーカーは規制基準を満たし、製品の美観を向上させる高度な印刷インクを採用するようになり、業界の成長が大幅に促進されています。

ヨーロッパの印刷インキ/包装インキ市場分析

- フレキソ、オフセット、グラビア、デジタルインク配合を含む印刷インクと包装インクは、商業および包装用途において、紙、板紙、プラスチック、アルミニウムなどのさまざまな基材に高品質の印刷を行うために不可欠です。

- これらのインクの需要の高まりは、主にパッケージ商品、電子商取引、ブランド差別化戦略の成長と、持続可能で移行の少ないインクソリューションの採用を促す環境規制の強化によって促進されています。

- ドイツは、強力な包装産業、高度な印刷インフラ、そして食品、飲料、医薬品の用途における持続可能で食品に安全なインクの高い需要により、2025年に印刷インク/包装インク市場を支配しました。

- 英国は、持続可能な包装の需要の高まり、食品および電子商取引の包装の成長、食品の安全性と環境コンプライアンスへの規制の強化により、予測期間中に印刷インク/包装インク市場で最も急速に成長する地域になると予想されています。

- 紙・板紙セグメントは、包装、ラベル、商業印刷における幅広い用途により、2025年には43%の市場シェアを占め、市場を席巻しました。紙ベースの素材は、印刷の容易さ、リサイクル性、そして費用対効果の高さから、メーカーとブランドオーナーの双方にとって好ましい選択肢となっています。先進国市場と新興国市場における持続可能でリサイクル可能な包装ソリューションへの需要の高まりも、この高い普及を支えています。

レポートの範囲と印刷インク/包装インク市場のセグメンテーション

|

属性 |

印刷インキ/包装インキの主要市場分析 |

|

対象セグメント |

|

|

対象国 |

ヨーロッパ

|

|

主要な市場プレーヤー |

|

|

市場機会 |

|

|

付加価値データ情報セット |

データブリッジマーケットリサーチがまとめた市場レポートには、市場価値、成長率、セグメンテーション、地理的範囲、主要プレーヤーなどの市場シナリオに関する洞察に加えて、輸出入分析、生産能力概要、生産消費分析、価格動向分析、気候変動シナリオ、サプライチェーン分析、バリューチェーン分析、原材料/消耗品概要、ベンダー選択基準、PESTLE分析、ポーター分析、規制枠組みも含まれています。 |

欧州の印刷インキ/包装インキ市場動向

持続可能で環境に優しいインクの採用増加

- 印刷インクおよび包装インク市場における重要なトレンドとして、持続可能で環境に優しいインクソリューションの採用増加が挙げられます。これは、環境への影響に対する消費者意識の高まりと、より安全な包装材へのニーズの高まりを背景にしています。この傾向により、メーカーは、印刷品質を維持しながら二酸化炭素排出量を削減できる、バイオベース、水性、低VOCインクの開発を迫られています。

- 例えば、フリントグループとサンケミカルは、フレキシブル包装および紙包装用途向けに水性および大豆ベースのインクを導入し、印刷・包装業界全体における持続可能な取り組みを支援しています。これらの取り組みは、企業が規制基準を満たし、環境意識の高い消費者のニーズに応えるのに役立ちます。

- クリーンラベルとリサイクル可能なパッケージの需要により、ブランドは色の鮮やかさを損なうことなく、完全に堆肥化またはリサイクル可能なインクを採用するよう促されています。これは、循環型経済の原則に沿った環境に優しい処方に向けた製品開発を促しています。

- 規制圧力と持続可能性認証は、印刷インキメーカーに無毒顔料と再生可能な原材料を用いた革新を促しています。EU REACH規則やFSC認証パッケージなどのイニシアチブへの準拠は、より安全で環境に優しい製品に向けた市場戦略を導きます。

- 市場では、環境に配慮した素材への高品質な印刷を実現するソリューションを共同開発するため、インクメーカーと包装メーカーの連携がますます活発化しています。こうしたパートナーシップは、機能面と美観面の両方の要件を満たしながら、持続可能な包装用インクの成長を促進しています。

- ブランド化されたプレミアムパッケージを好む消費者は、接着性、光沢性、印刷解像度の向上など、持続可能性と高性能を兼ね備えたインクを求めています。この傾向は、ブランドアイデンティティと環境への責任の両方をサポートするインクへの移行を加速させています。

ヨーロッパの印刷インキ/包装インキ市場の動向

ドライバ

高品質で食品に安全な包装の需要の高まり

- 製品の安全性を確保する高品質な包装へのニーズの高まりにより、特に食品、飲料、医薬品分野において、特殊な印刷インクや包装インクの需要が高まっています。これらのインクは、鮮明で均一な印刷品質を維持しながら、厳格な安全基準を満たす必要があります。

- 例えば、SiegwerkとHubergroupは、FDAおよびスイス条例の規制に準拠した食品安全インクを供給しており、ブランドは見た目を損なうことなく消費財を安全に包装することができます。これらのインクは、規制遵守と包装商品に対する消費者の信頼向上の両方に貢献します。

- 電子商取引と高級パッケージ製品の拡大により、輸送・保管中の印刷品質を維持する耐久性のあるインクに対する需要がさらに高まっています。ブランドは、にじみ、退色、そして包装材との化学的相互作用に耐性のあるインクを求めています。

- デジタル印刷技術とフレキソ印刷技術の進歩により、安全基準を維持しながら高速生産に対応するインクの開発が促進されています。この互換性により、運用効率が向上し、生産停止時間が削減されます。

- 持続可能性への懸念から、揮発性有機化合物(VOC)と重金属の含有量が少ないインクが好まれるようになり、環境に配慮したパッケージングの取り組みが促進されています。これらの開発により、インク配合における品質、安全性、そして環境責任の統合が強化されています。

抑制/挑戦

厳格な環境および規制遵守

- 印刷インキおよび包装インキ市場は、厳しい環境規制および規制要件により、生産に使用できる原材料や化学物質の種類が制限されるという課題に直面しています。世界および地域の規制への準拠は、製品開発とサプライチェーン管理の複雑さを増しています。

- 例えば、サンケミカルのような企業は、インクがEU REACH、FDA、その他の国際安全基準を満たすよう、研究開発に多額の投資を行っていますが、これが運用コストの増加につながっています。こうしたコンプライアンス義務は、処方の選択に影響を与え、迅速なイノベーションを阻害しています。

- 揮発性有機化合物(VOC)および有害物質の排出基準を満たすには、特殊な設備と継続的な監視が必要であり、製造工程の複雑さが増します。企業は規制遵守と生産効率およびコスト管理のバランスを取る必要があります。

- 市場は、従来のインクを使用した印刷物のリサイクルと廃棄にも課題を抱えており、バイオベースや水性インクを使用した代替品への移行を促しています。これらの要件は、製品設計と使用済み製品の処理プロセスの両方に影響を与えます。

- 厳格な規制および環境基準を遵守しながら、一貫した色彩性能を維持することは、メーカーにとって依然として大きな課題です。この制約により、市場競争力を維持するためには、より安全で規制に準拠したインク技術への継続的なイノベーションと投資が求められます。

欧州の印刷インキ/包装インキ市場の範囲

市場は、技術、タイプ、樹脂、基板、および用途に基づいて分割されています。

- テクノロジー別

印刷インク市場は、技術に基づいて、溶剤系、油性、水性、UV硬化型、LED硬化型、EB硬化型、その他に分類されます。水性インクセグメントは、環境に優しい特性、低VOC含有量、そして厳格な環境規制への適合性により、2025年には最大の市場収益シェアを獲得し、市場を席巻しました。食品・飲料包装への安全な適用と、幅広い基材との適合性から、メーカーやブランドオーナーは水性インクをますます好むようになっています。高品質の印刷を実現しながら、環境への影響と製造上の危険性を低減できるため、市場では水性インクの採用が進んでいます。

The UV curable segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by rising demand for high-speed printing, superior print durability, and enhanced resistance to chemicals and abrasion. UV curable inks are increasingly used in premium packaging applications and labels, providing vibrant colors and rapid curing times that improve production efficiency. The integration of UV curable technology with digital and flexible printing processes further accelerates its adoption across various industries.

- By Type

On the basis of type, the printing inks market is segmented into flexo inks, offset inks, gravure inks, jet inks, metal decorative inks, security inks, and others. The flexo inks segment dominated the market with the largest market revenue share in 2025, driven by its widespread use in flexible packaging, corrugated cartons, and labels. Flexo inks are preferred for their fast-drying properties, ability to print on multiple substrates, and cost-effectiveness in large-volume printing operations. Manufacturers favor flexo inks due to their compatibility with automated high-speed printing lines and consistent print quality.

The jet inks segment is expected to witness the fastest CAGR from 2026 to 2033, fueled by the growing adoption of digital printing technologies in packaging and commercial applications. Jet inks enable high-resolution prints, variable data printing, and short-run customizations, making them ideal for modern packaging demands. The increasing trend of e-commerce and personalized packaging also contributes to the accelerated adoption of jet inks across regions.

- By Resin

On the basis of resin, the printing inks market is segmented into polyurethane, acrylic, vinyl, polyamide, polyketone, nitrocellulose, and others. The acrylic segment dominated the market with the largest market revenue share in 2025, driven by its excellent adhesion, color retention, and chemical resistance across various substrates. Acrylic resins are preferred in food and beverage packaging due to their safe, non-toxic properties and ability to deliver high-quality, durable prints. The market also witnesses strong adoption of acrylic resins because of their flexibility in blending with other resins and suitability for diverse printing technologies.

The polyurethane segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by its superior mechanical strength, abrasion resistance, and versatility in specialty packaging applications. Polyurethane-based inks are increasingly used in high-end product labels, metal decorative coatings, and flexible packaging requiring enhanced durability. Rising demand for long-lasting and premium packaging solutions drives the accelerated adoption of polyurethane inks globally.

- By Substrate

On the basis of substrate, the printing inks market is segmented into paper and board, polyethylene, aluminum, polyvinyl chloride, polypropylene, polyvinyl acetate, polyolefin, cellophane, polyester, nylon, and others. The paper and board segment dominated the market with the largest market revenue share of 43% in 2025, driven by its widespread use in packaging, labeling, and commercial printing. Paper-based substrates offer ease of printing, recyclability, and cost-effectiveness, making them a preferred choice for both manufacturers and brand owners. Strong adoption is further supported by the growing demand for sustainable and recyclable packaging solutions in developed and emerging markets.

The polyethylene segment is expected to witness the fastest CAGR from 2026 to 2033, fueled by increasing applications in flexible packaging, pouches, and shrink films. Polyethylene substrates provide excellent moisture resistance, durability, and compatibility with modern ink technologies, enhancing print quality and shelf appeal. Rising consumer preference for flexible packaging and extended shelf-life products accelerates the adoption of polyethylene-based printing inks.

- By Application

On the basis of application, the printing inks market is segmented into food packaging, wall paper, corrugated and solid board, panels, labels, laminates, carrier bags, aluminum foils, shrink wrap films, envelopes, paper synthetic films, wrapping paper, heavy-duty sacks, deep freeze packaging, hygiene packaging, flower wrap, and others. The food packaging segment dominated the market with the largest market revenue share in 2025, driven by rising demand for safe, visually appealing, and functional packaging. Printing inks for food packaging are preferred for their compliance with food safety regulations, high color vibrancy, and resistance to moisture and oils. The market sees strong adoption in food packaging due to increasing consumer demand for packaged foods, convenience products, and extended shelf-life solutions.

The labels segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by expanding e-commerce, premium product branding, and regulatory labeling requirements. Label inks require high precision, durability, and compatibility with different packaging substrates, driving innovation in specialty inks. Rising demand for attractive and informative packaging labels accelerates the adoption of label-specific printing inks across multiple industries.

Europe Printing Inks / Packaging Inks Market Regional Analysis

- Germany dominated the printing inks / packaging inks market with the largest revenue share in 2025, driven by its strong packaging industry, advanced printing infrastructure, and high demand for sustainable and food-safe inks across food, beverage, and pharmaceutical applications

- Germany’s strong presence of leading ink manufacturers, robust chemical production capabilities, and strict compliance with EU environmental regulations sustain steady demand for water-based, low-VOC, and bio-based inks. Continuous investments in high-quality packaging, premium labeling, and export-oriented manufacturing further reinforce market growth

- Increasing emphasis on sustainable packaging, circular economy practices, and high-performance printing solutions, supported by companies such as Hubergroup and Siegwerk, strengthens Germany’s leading position

U.K. Printing Inks / Packaging Inks Market Insight

The U.K. is projected to register the fastest CAGR in the Europe printing inks and packaging inks market during the forecast period, supported by rising demand for sustainable packaging, growth in food and e-commerce packaging, and increasing regulatory focus on food safety and environmental compliance. For instance, companies such as Sun Chemical and Flint Group maintain a strong market presence, supporting the availability of water-based and food-safe inks across packaging applications. Expanding retail packaging, higher adoption of digital printing, and increased investment in eco-friendly packaging solutions are accelerating demand. Growing focus on recyclable packaging and premium branding positions the U.K. as the fastest-growing market in the region.

France Printing Inks / Packaging Inks Market Insight

France is expected to witness steady growth during the forecast period, driven by consistent demand from food, beverage, and cosmetic packaging, along with ongoing adoption of sustainable printing solutions. The country’s emphasis on environmentally responsible packaging and compliance with EU regulations supports continuous use of low-VOC and bio-based inks. Rising demand for visually appealing and high-quality packaging, combined with steady innovation by European ink manufacturers, contributes to stable market expansion. Sustained demand from both mass-market and premium packaging segments reinforces France’s steady growth within the Europe printing inks and packaging inks market.

Europe Printing Inks / Packaging Inks Market Share

The printing inks / packaging inks industry is primarily led by well-established companies, including:

- DIC CORPORATION (Japan)

- SAKATA INX CORPORATION (Japan)

- Siegwerk Druckfarben AG & Co. KGaA (Germany)

- TOYO INK SC HOLDINGS CO., LTD. (Japan)

- hubergroup Deutschland GmbH (Germany)

- Flint Group (Switzerland)

- Kao Collins Corporation (U.S.)

- SICPA HOLDING SA (Switzerland)

- T&K TOKA Corporation (Japan)

- TOKYO PRINTING INK MFG CO., LTD (Japan)

- Sun Chemical Corporation (U.S.)

- PPG Industries, Inc. (U.S.)

- Akzo Nobel N.V. (Netherlands)

- Zeller+Gmelin GmbH & Co. KG (Germany)

- Wikoff Color Corporation (U.S.)

Latest Developments in Europe Printing Inks / Packaging Inks Market

- 2024年5月、フリントグループは段ボール包装市場向けに、バイオベースの増量剤とコーティング剤を特徴とする環境に優しい製品ライン「TerraCode Bio」を導入し、TerraCodeシリーズを拡大しました。この発売により、フリントグループは持続可能な包装インク分野における地位を強化し、環境に配慮した素材への高まる需要に対応し、規制遵守と印刷性能の向上を兼ね備えた段ボール加工業者向けソリューションを提供します。バイオベースの成分の追加は、二酸化炭素排出量の削減に向けた市場動向を後押しし、グリーン包装への消費者の嗜好の高まりにも合致しています。

- 2024年5月、デュポンはdrupa 2024において、光学濃度の向上と食品接触適合性を重視した低粘度顔料インク「Artistri PN1000」を発表しました。この発売により、デュポンは、特に見た目の魅力と規制遵守が重要となる包装用途において、高性能で食品安全インクの拡大市場を獲得する立場を確立します。印刷品質を損なうことなく厳格な安全基準を満たすインクを提供することで、デュポンは特殊顔料および包装インク分野における競争力を強化します。

- DICインドは2024年3月、グジャラート州に年間生産能力1万トンのトルエンフリー液体インキ工場を開設しました。投資額は11億インドルピー(約13億米ドル)です。この工場は、インドおよび近隣地域における環境に配慮した低VOCインキに対する市場ニーズの高まりに対応します。この工場により、DICは持続可能なインキの生産規模を拡大し、供給の信頼性を高め、より厳しい環境・健康規制への適合を求める包装・印刷業界からの高まる需要に応えることができます。

- 2024年2月、フリントグループは、世界中の枚葉オフセット印刷機向けに設計された低臭・低移行性(LOLM)プロセスインクシリーズ「Novasens P670 PRIME」を発表しました。この開発により、印刷機の運用効率向上、廃棄物削減、そして持続可能性目標達成を支援するソリューションを提供することで、同社の市場提供が強化されます。LOLMの配合は、食品安全インクへの業界の関心の高まりと一致しており、印刷機が高品質の印刷性能を維持しながら規制基準を満たすのに役立ちます。

- 2024年1月、特殊化学品グループであるALTANAは、自動車用塗料、印刷インク、プラスチック、保護コーティング、包装消費財などの用途向けのエフェクト顔料を開発・製造する米国企業であるSilberline Groupの事業買収を完了しました。この戦略的買収により、ALTANAは高付加価値顔料用途における市場プレゼンスを拡大し、特殊インクのポートフォリオを強化し、装飾・機能性包装市場における進化する需要に応える革新的なソリューションの提供能力を強化します。

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。