Middle East And Africa Transplant Diagnostics Market

시장 규모 (USD 10억)

연평균 성장률 :

%

USD

298.17 Million

USD

430.56 Million

2025

2033

USD

298.17 Million

USD

430.56 Million

2025

2033

| 2026 –2033 | |

| USD 298.17 Million | |

| USD 430.56 Million | |

| % | |

Middle East and Africa Transplant Diagnostics Market, By Product Type (Transplant Diagnostic Instrument, Transplant Diagnostic Software, Transplant Diagnostic Reagent), Technology (PCR-Based Molecular Assays, Sequencing-Based Molecular Assays), Transplant Type (Solid Organ Transplantation, Stem Cell Transplantation, Soft Tissue Transplantation, Bone Marrow Transplantation, Other), Application (Diagnostic Applications, Research Applications), End User (Research Laboratories and Academic Institutes, Hospital and Transplant Centers, Commercial Service Providers, Others), Distribution Channel (Direct Tender, Retail Sales and Others) - Industry Trends and Forecast to 2029.

Middle East and Africa Transplant Diagnostics Market Analysis and Insights

Transplant diagnosis is a diagnostic procedure usually divided into pre-transplant and post-transplant procedures. It helps to analyze the health status of the patient. If this is avoided, the immunocompromised person is at risk of developing HAI or worse, which can lead to death. The procedure is a harmonious collaboration between healthcare professionals and laboratory experts, ensuring better patient outcomes. In addition, close matching of donor and recipient HLA markers is important. This increases the likelihood of graft survival and minimizes serious complications of immunological transplantation. The increased prevalence of chronic illnesses among the worldwide population is likely to drive market expansion throughout the forecast years. Furthermore, the increasing use of stem cell therapy and personalized medications is gaining popularity. The use of new diagnostic techniques has improved the medical outcomes of organ transplants. The rate of organ rejection can be reduced by matching the compatibility of the donor and recipient before transplantation.

However, the high cost of procedures associated with PCR and NGS diagnostic instruments is one of the most significant. As a result, market growth may be hampered in the long run. The cost of medical equipment is one element that may challenge critical transplant diagnosis device vendors.

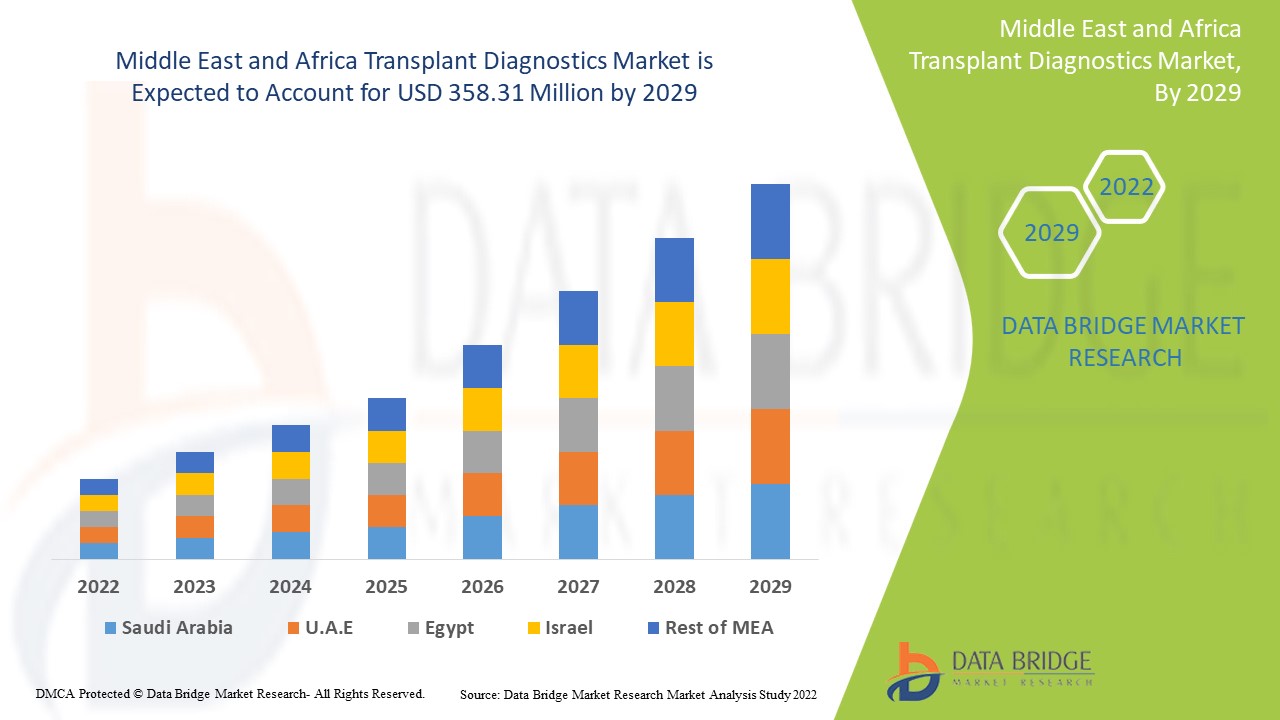

Data Bridge Market Research analyzes that the Middle East and Africa transplant diagnostics market is expected to reach a value of USD 358.31 million by 2029, at a CAGR of 4.7% during the forecast period. This market report also covers pricing analysis, patent analysis, and technological advancements in depth.

|

Report Metric |

Details |

|

Forecast Period |

2022 to 2029 |

|

Base Year |

2021 |

|

Historic Years |

2020 (Customizable to 2019-2014) |

|

Quantitative Units |

Revenue in USD Million, Pricing in USD |

|

Segments Covered |

By Product Type (Transplant Diagnostic Instrument, Transplant Diagnostic Software, Transplant Diagnostic Reagent), Technology (PCR-Based Molecular Assays, Sequencing-Based Molecular Assays), Transplant Type (Solid Organ Transplantation, Stem Cell Transplantation, Soft Tissue Transplantation, Bone Marrow Transplantation, Other), Application (Diagnostic Applications, Research Applications), End User (Research Laboratories and Academic Institutes, Hospital and Transplant Centers, Commercial Service Providers, Others), Distribution Channel (Direct Tender, Retail Sales and Others) |

|

Countries Covered |

South Africa, Saudi Arabia, U.A.E, Egypt, Israel and the rest of the Middle East and Africa |

|

Market Players Covered |

Hologic, Inc., Biofortuna Limited, Takara Bio Inc., Abbott, Thermo Fisher Scientific Inc., Luminex Corporation (A subsidiary of DiaSorin Company), DiaSorin S.p.A., Stryker, Bio-Rad Laboratories, Inc., Zimmer Biomet, QIAGEN, F. Hoffmann-La Roche Ltd, BIOMÉRIEUX, CareDx Inc., Illumina, Inc., IMMUCOR, among others |

Market Definition

Transplant diagnostics are the immunogenetics and histocompatibility of organ and hematopoietic stem cell transplantations. These diagnostics help healthcare professionals determine compatibility between potential recipients and organ donors. These are used in various disciplines, such as immunogenetics, pathology and infectious diseases, among others. Transplant diagnostics are used to determine whether the donor and the recipient of the organ are compatible before or after the transplant. With the introduction of transplant diagnostics, the prevalence of diseases that can cause organ failure, including both pre-and post-transplant screening, is expected to explode. The market has attracted the interest of healthcare professionals due to the many advantages these tests offer to verify suitability for a transplant procedure. Organ transplantation is one of the most popular treatment options for many end-stage renal disease patients on continuous dialysis.

- In addition, it is possible to investigate organ transplantation for cases involving the heart, liver, or bone marrow. Although in many cases, there is a strong association between renal failure and liver transplantation, including end-stage renal disease. New transcriptomic, proteomic and genomic indicators in molecular diagnostics can help to better tailor transplant therapy and early detection of rejection events. Also, strategic initiatives by market players, technological progressions in transplant diagnostics, high sterility assurance and increasing investment in healthcare infrastructure increase the demand for transplant diagnostics.

Middle East and Africa Transplant Diagnostics Market Dynamics

This section deals with understanding the market drivers, advantages, opportunities, restraints, and challenges. All of this is discussed in detail below:

Drivers

- Rising number of transplant procedures

The demand for organ transplantation has rapidly increased worldwide during the past decade due to the increased incidence of vital organ failure and improved post-transplant outcomes. Demand for kidney, heart, liver and lungs transplant is very high. Alcohol consumption, lack of exercise and drug abuse are leading causes of organ failure. The number of living donor transplants has been affected by the COVID-19 pandemic. But living donor transplants have increased by 14.2 percent over 2020.

- In addition, organ transplantation improves patient survival and quality of life and has a major positive impact on public health and the socioeconomic burden of organ failure. The European Union (EU) has a relatively uniform and structured approach to organ transplantation, well-developed national programs, international systems to facilitate organ sharing and well-defined exchange policies, making Europe a leader in this field.

Thus, the increasing number of transplant procedures across the globe and the increase in successful transplantations is expected to boost the Middle East and Africa transplant diagnostics market.

- Increase in the technological advancements in the field of transplants

New technologies are rapidly changing traditional approaches to organ transplantation. The main challenges in organ transplantation are how best to identify and, if possible, eliminate the need for lifelong immunosuppression and how to expand the pool of donors suitable for human transplantation. Researchers have developed an advanced system where transport time can be extended by tricking donor organs into thinking they are still inside the body. This system keeps oxygenated blood flowing through the organs to delay tissue death. A normothermic perfusion machine mimics the human body, ensuring constant blood flow to the organ. The machine can also deliver drugs or other nutrients to keep the liver in optimal condition before the transplant.

In addition, bio-artificial organ production techniques are a range of enabling techniques that can be used to produce human organs based on bionic principles. Over the past ten years, significant progress has been made in developing various organ manufacturing technologies. The past decade has seen tremendous advances in new technologies such as single-cell RNA sequencing, Nano biotechnology and CRISPR-Cas9 gene editing. However, creative applications of such new and powerful technologies to improve clinical transplantation have only begun. With such tools, there are now good opportunities to make major breakthroughs in defining and providing optimized and individualized care for all organ transplants.

Restraint

- High cost of organ transplantation

Organ transplantation therapy employs highly technologically advanced products. The development of these products involves rigorous research and development by the developing players. Thus, the procedures and product cost remains high, which proportionally increases the cost of testing. Also, organ transplants are expensive because they are incredibly resource-intensive and involve high-paid doctors, transportation and expensive medications

- In addition, desensitizing therapies have also been used to achieve transplantation from an incompatible donor. However, such procedures are very expensive and may be associated with complications and worse long-term outcomes.

Thus, the high cost of transplantation and treatment using advanced modalities and technology products will act as a major restraining factor for the growth of the Middle East and Africa transplant diagnostics market.

Opportunity

-

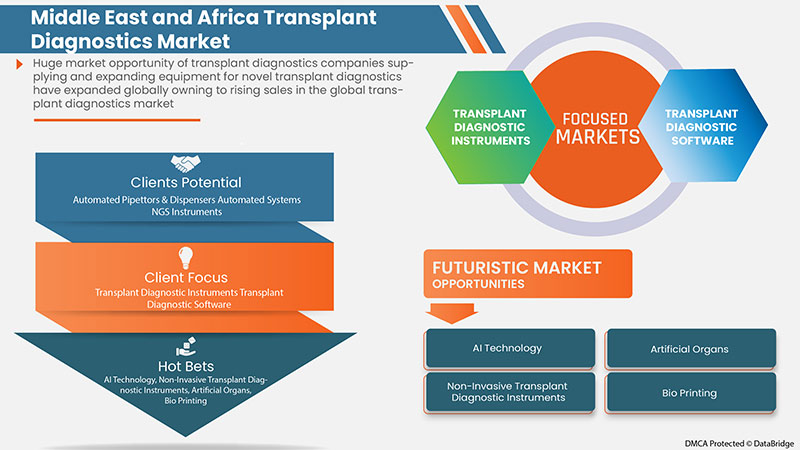

Strategic initiatives by market players

The rise in the Middle East and Africa transplant diagnostics market increases the need for strategic business ideas. It includes a partnership, business expansion and other development. The surge in demand for a donor organs is significantly increasing the demand for transplant diagnostic kits. The planned strategies allow the market players to align with the organization's functional activities to achieve set goals. It guides the company's discussions and decision-making in determining resource and budget requirements to accomplish objectives, thus increasing operational efficiency.

These strategic initiatives, such as product launches, agreements and business expansion by the major market players, will boost the market growth and are expected to act as an opportunity for the Middle East and Africa transplant diagnostics market. The strategic initiatives are expected to aid in growth and improve the company's product portfolio, ultimately leading to more revenue generation. Hence, these strategic initiatives by the market players may be expected to as an opportunity that helps them to drive the Middle East and Africa transplant diagnostics market.

Challenge

- Ethical challenges faced during organ transplantation

The surge in the incidence of failure of vital organs and inadequate supply of organs has created a wide gap between organ supply and organ demand. The issue has resulted in long approval times to receive an organ and a rise in deaths. The events, which occurred in the previous years and continue in the present, have raised many ethical, moral and societal issues regarding supply, the methods of organ allocation and the use of living donors as volunteers, including minors.

Lack of accuracy in reporting, the donated organs can't be supplied and procedures that neither relieve suffering nor prolong life are rapidly identified.

Issues such as lack of organ procurement, religious acceptance, brain death and misconceptions related to organ donation and transplantation are still present on many ethical personal and community levels, even within the medical community. The various aspects of ethical, cultural and religious nature should not be a barrier to the act of organ donation and transplantation all of these are issues to be solved. Therefore, ethical challenges faced during organ transplantation are expected to challenge market growth.

Post-COVID-19 Impact on Middle East and Africa Transplant Diagnostics Market

Middle East and Africa transplant diagnostics market has been badly affected by COVID-19. Hospital admissions were limited to non-essential treatment, and clinics were temporarily closed during the pandemic. The implementation of social distancing, blocking the population, and limited access to clinics have greatly affected the market. The slowdown in patient flows and referrals also affected the market growth. However, the market will continue to grow in the post-pandemic period due to the relaxation of previously imposed restrictions.

Manufacturers are making various strategic decisions to bounce back post-COVID-19. The players are conducting multiple R&D activities, product launches, and strategic partnerships to improve the technology and test results in the Middle East and Africa transplant diagnostics market.

Recent Developments

- In August 2022, QIAGEN announced the publication in the Journal of Molecular Pathology of an externally facilitated clinical NGS interpretation validation study, demonstrating that its clinical decision support software, QIAGEN Clinical Insight Interpret One (QCI Interpret One), achieved a higher level of concordance with a panel of experts than human reviewers achieved amongst each other. The study commissioned by QDI and carried out independently by Genomics Quality Assessment (GenQA) investigated the classification of variants reported from oncology patient samples. This has helped company to validate its research

- In January 2022, Hoffmann-La Roche Ltd introduced Cobas Infinity edge, a cloud-based point-of-care platform accessible. With its advanced technology, healthcare practitioners can handle patient data. This has helped the company to diversify their product line

Middle East and Africa Transplant Diagnostics Market Scope

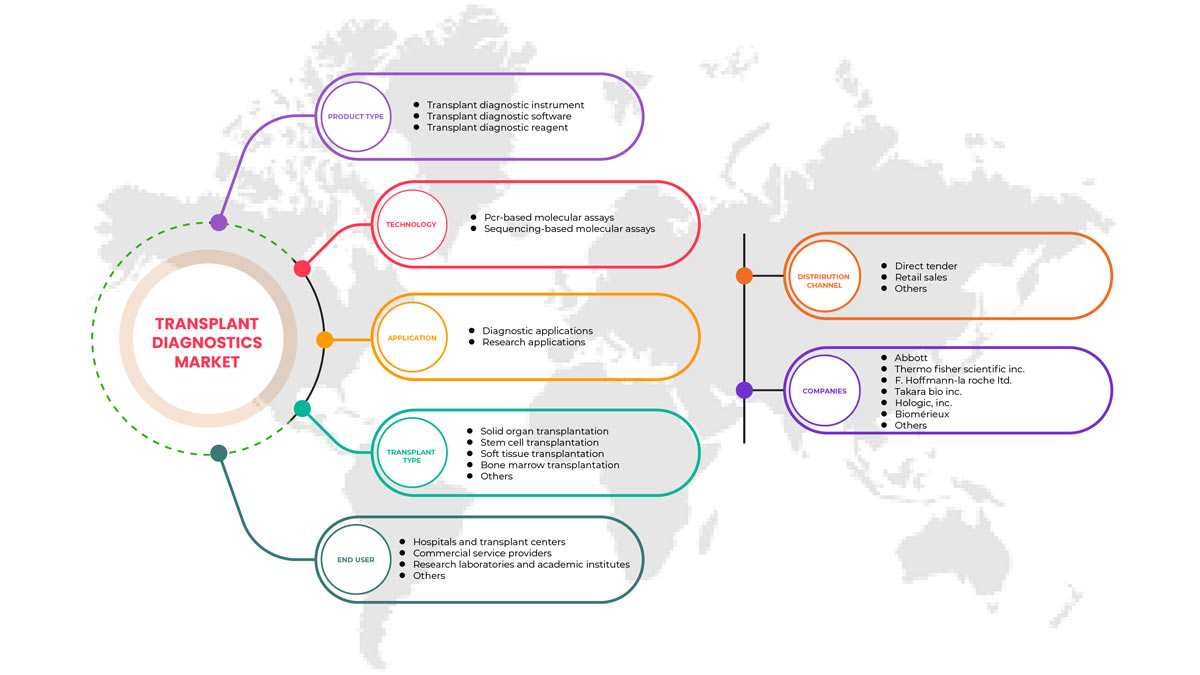

The Middle East and Africa transplant diagnostics market is segmented into product type, technology, transplant type, application, end user, and distribution channel. The growth among segments helps you analyze niche pockets of growth and strategies to approach the market and determine your core application areas and the difference in your target markets.

Product Type

- Transplant Diagnostic Instrument

- Transplant Diagnostic Software

- Transplant Diagnostic Reagent

On the basis of product type, the Middle East and Africa transplant diagnostics market is segmented into transplant diagnostic instrument, transplant diagnostic software, transplant diagnostic reagent.

Technology

- PCR-Based Molecular Assays

- Sequencing-Based Molecular Assays

On the basis of technology, the Middle East and Africa transplant diagnostics market is segmented into PCR-based molecular assays, and sequencing-based molecular assays.

Transplant Type

- Solid Organ Transplantation

- Stem Cell Transplantation

- Soft Tissue Transplantation

- Bone Marrow Transplantation

- Other Transplants

On the basis of transplant type, the Middle East and Africa transplant diagnostics market is segmented into solid organ transplantation, stem cell transplantation, soft tissue transplantation, bone marrow transplantation, and other transplants.

Application

- Diagnostic Applications

- Research Applications

On the basis of application, the Middle East and Africa transplant diagnostics market is segmented into diagnostic applications and research applications.

End User

- Research Laboratories and Academic Institutes

- Hospitals and Transplant Centers

- Commercial Service Providers

- Others

On the basis of end user, the Middle East and Africa transplant diagnostics market is segmented into research laboratories and academic institutes, hospitals and transplant centers, commercial service providers, and others.

Distribution Channel

- Direct Tender

- Retail Sales

- Others

On the basis of distribution channel, the Middle East and Africa transplant diagnostics market is segmented into direct tender, retail sales, and others.

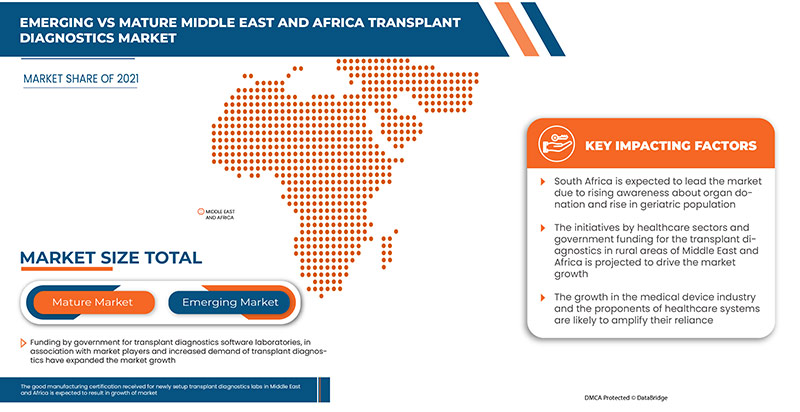

Middle East and Africa Transplant Diagnostics Market Regional Analysis/Insights

Middle East and Africa transplant diagnostics market is analyzed, and market size information is provided by country, product type, technology, transplant type, application, end user, and distribution channel.

The countries covered in the Middle East and Africa transplant diagnostics market are South Africa, Saudi Arabia, U.A.E, Egypt, Israel and the rest of the Middle East and Africa.

South Africa is expected to dominate in the Middle East and Africa transplant diagnostics market due to the rise in technological advancements.

The country section of the report also provides individual market-impacting factors and domestic regulation changes that impact the market's current and future trends. Data points such as new sales, replacement sales, country demographics, regulatory acts, and import-export tariffs are some of the major pointers used to forecast the market scenario for individual countries. Also, the presence and availability of Middle East and African brands, the challenges faced due to large or scarce competition from local and domestic brands, and the impact of sales channels are considered while providing forecast analysis of the country data.

Competitive Landscape and Middle East and Africa Transplant Diagnostics Market Share Analysis

The Middle East and Africa transplant diagnostics market competitive landscape provides details by the competitor. Details included are company overview, company financials, revenue generated, market potential, investment in R&D, new market initiatives, production sites and facilities, company strengths and weaknesses, product launch, product trials pipelines, product approvals, patents, product width and breath, application dominance, technology lifeline curve. The above data points provided are only related to the company's focus on the Middle East and Africa transplant diagnostics market.

Some of the major players operating in the Middle East and Africa transplant diagnostics market are Hologic, Inc., Biofortuna Limited, Takara Bio Inc., Abbott, Thermo Fisher Scientific Inc., Luminex Corporation (A subsidiary of DiaSorin Company), DiaSorin S.p.A., Stryker, Bio-Rad Laboratories, Inc., Zimmer Biomet, QIAGEN, F. Hoffmann-La Roche Ltd, BIOMÉRIEUX, CareDx Inc., Illumina, Inc., IMMUCOR, among others.

Research Methodology: Middle East and Africa Transplant Diagnostics Market

Data collection and base year analysis are done using data collection modules with large sample sizes. The market data is analyzed and estimated using market statistical and coherent models. In addition, market share analysis and key trend analysis are the major success factors in the market report. The key research methodology used by the DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market, and primary (industry expert) validation. Apart from this, data models include a Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Company Market Share Analysis, Standards of Measurement, Middle East and Africa vs Regional, and Vendor Share Analysis. Please request an analyst call in case of further inquiry.

SKU-

세계 최초의 시장 정보 클라우드 보고서에 온라인으로 접속하세요

- 대화형 데이터 분석 대시보드

- 높은 성장 잠재력 기회를 위한 회사 분석 대시보드

- 사용자 정의 및 질의를 위한 리서치 분석가 액세스

- 대화형 대시보드를 통한 경쟁자 분석

- 최신 뉴스, 업데이트 및 추세 분석

- 포괄적인 경쟁자 추적을 위한 벤치마크 분석의 힘 활용

목차

1 서론

1.1 연구 목적

1.2 시장 정의

1.3 중동 및 아프리카 이식 진단 시장 개요

1.4 통화 및 가격

1.5 제한 사항

1.6 대상 시장

2 시장 세분화

2.1 대상 시장

2.2 지리적 범위

연구에 2.3년이 고려됨

2.4 DBMR TRIPOD 데이터 검증 모델

2.5 주요 여론 리더와의 1차 인터뷰

2.6 다변량 모델링

2.7 시장 적용 범위 그리드

2.8 소스 라이프라인 곡선

2.9 DBMR 시장 위치 그리드

2.1 공급업체 점유율 분석

2.11 2차 소스

2.12 가정

3 요약

3.1 역학

3.2 PESTEL 분석

3.3 포터의 5가지 힘

3.4 기술 혁신

4 중동 및 아프리카 이식 진단 시장: 규정

5가지 핵심 전략적 이니셔티브

6가지 산업 통찰력:

7 시장 개요

7.1 드라이버

7.1.1 이식 수술 건수 증가

7.1.2 이식 분야의 기술적 진보 증가

7.1.3 증가하는 의료비 지출

7.1.4 이식 전 및 이식 후 교차 매칭 및 키메리즘 테스트 채택

7.2 제약

7.2.1 장기 이식의 높은 비용

7.2.2 장기 이식의 위험과 어려움

7.3 기회

7.3.1 시장 참여자의 전략적 이니셔티브

7.3.2 장기 이식을 위한 공공, 민간 및 정부 자금 지원 증가

7.3.3 장기 이식의 중요성에 대한 인식의 급증

7.4 과제

7.4.1 장기 이식 중 직면하는 윤리적 과제

7.4.2 장기 기증자 부족 또는 장기 기증자와 매년 필요한 장기 간의 격차

8 중동 및 아프리카 이식 진단 시장, 제품 유형별

8.1 개요

8.2 이식 진단 도구

8.2.1 자동 피펫 및 디스펜서

8.2.2 자동화 시스템

8.2.2.1 핵산 추출 시스템

8.2.2.2 PCR 설정

8.2.2.3 기타

8.2.3 NGS 기기

8.2.4 리더 및 분석기

8.2.5 이식 진단 키트

8.2.5.1 아스페르길루스 SPP 키트

8.2.5.2 P. JIROVECII 키트

8.2.5.3 CMV 키트

8.2.5.4 EBV 키트

8.2.5.5 BKV 키트

8.2.5.6 VZV 키트

8.2.5.7 HSV1 키트

8.2.5.8 HSV2 키트

8.2.5.9 파보바이러스 B19 키트

8.2.5.10 아데노바이러스 키트

8.2.5.11 엔테로바이러스 키트

8.2.5.12 JCV 키트

8.2.5.13 HHV6 키트

8.2.5.14 HHV7 키트

8.2.5.15 HHV8 키트

8.2.5.16 톡소플라즈마 곤디이 키트

8.2.5.17 E형 간염 키트

8.2.5.18 기타 키트

8.2.6 기타 키트

8.3 이식 진단 소프트웨어

8.3.1 DNA 소프트웨어

8.3.2 NGS 소프트웨어

8.3.3 데이터 관리 소프트웨어

8.3.4 기타 소프트웨어

8.4 이식 진단 시약

8.4.1 단일클론 항체

8.4.2 세포독성 통제

8.4.3 인간 혈청

8.4.4 기타 시약

9 중동 및 아프리카 이식 진단 시장, 기술별

9.1 개요

9.2 PCR 기반 분자 검정

9.2.1 실시간 PCR

9.2.2 서열 특정 프라이머 PCR

9.2.3 서열 특이적 올리고뉴클레오티드 PCR

9.2.4 제한 단편 길이 다형성(RFLP)

9.2.5 OTHER-PCR 기반 분자 검정

9.3 시퀀싱 기반 분자 분석

9.3.1 샌거 시퀀싱

9.3.2 차세대 시퀀싱

9.3.3 기타 시퀀싱 기반 분자 분석.

10 중동 및 아프리카 이식 진단 시장, 이식 유형별

10.1 개요

10.2 고형장기 이식

10.2.1 신장 이식

10.2.2 간 이식

10.2.3 심장 이식

10.2.4 폐 이식

10.2.5 췌장 이식

10.2.6 기타 장기 이식

10.3 줄기세포 이식

10.3.1 골수 이식(BMT)

10.3.2 말초혈액줄기세포이식

10.3.3 제대혈 이식

10.3.4 기타 줄기세포 이식

10.4 연부조직 이식

10.4.1 피부이식

10.4.2 연골 이식

10.4.3 부신 자가이식

10.4.4 기타 연부조직 이식.

10.5 골수 이식

10.5.1 자가 골수 이식

10.5.2 이종 골수 이식

10.5.3 탯줄 혈액 이식.

10.6 기타

11 중동 및 아프리카 이식 진단 시장, 응용 분야별

11.1 개요

11.2 진단 응용 프로그램

11.2.1 이식 진단 장비

11.2.1.1 자동 피펫 및 디스펜서

11.2.1.2 자동화 시스템

11.2.1.3 NGS 기기

11.2.1.4 리더 및 분석기

11.2.1.5 이식 진단 키트

11.2.1.6 기타

11.2.2 이식 진단 소프트웨어

11.2.2.1 DNA 소프트웨어

11.2.2.2 NGS 소프트웨어

11.2.2.3 데이터 관리 소프트웨어

11.2.2.4 기타 소프트웨어

11.2.3 이식 진단 시약

11.2.3.1 단일클론 항체

11.2.3.2 세포독성 통제

11.2.3.3 인간 혈청

11.2.3.4 기타 시약

11.3 연구 응용 프로그램

11.3.1 이식 진단 장비

11.3.1.1 자동 피펫 및 디스펜서

11.3.1.2 자동화 시스템

11.3.1.3 NGS 기기

11.3.1.4 리더 및 분석기

11.3.1.5 이식 진단 키트

11.3.1.6 기타

11.3.2 이식 진단 소프트웨어

11.3.2.1 DNA 소프트웨어

11.3.2.2 NGS 소프트웨어

11.3.2.3 데이터 관리 소프트웨어

11.3.2.4 기타 소프트웨어

11.3.3 이식 진단 시약

11.3.3.1 단일클론 항체

11.3.3.2 세포독성 통제

11.3.3.3 인간 혈청

11.3.3.4 기타 시약

12 중동 및 아프리카 이식 진단 시장, 최종 사용자별

12.1 개요

12.2 병원 및 이식 센터

12.3 상업 서비스 제공자

12.4 연구실 및 학술기관

12.5 기타

13 중동 및 아프리카 이식 진단 시장, 유통 채널별

13.1 개요

13.2 직접 입찰

13.3 소매 판매

13.4 기타

14 중동 및 아프리카 이식 진단 시장, 지역별

14.1 중동 및 아프리카

14.1.1 남아프리카 공화국

14.1.2 사우디 아라비아

14.1.3 아랍에미리트

14.1.4 이집트

14.1.5 이스라엘

14.1.6 중동 및 아프리카의 나머지 지역

15 중동 및 아프리카 이식 진단 시장: 회사 환경

15.1 회사 점유율 분석: 중동 및 아프리카

16 SWOT 분석

17 회사 프로필

17.1 애벗

17.1.1 회사 스냅샷

17.1.2 수익 분석

17.1.3 회사 점유율 분석

17.1.4 제품 포트폴리오

17.1.5 최근 개발 사항

17.2 써모 피셔 사이언티픽 주식회사

17.2.1 회사 스냅샷

17.2.2 수익 분석

17.2.3 회사 점유율 분석

17.2.4 제품 포트폴리오

17.2.5 최근 개발 사항

17.3 F. 호프만 라 로슈 유한회사

17.3.1 회사 스냅샷

17.3.2 수익 분석

17.3.3 회사 점유율 분석

17.3.4 제품 포트폴리오

17.3.5 최근 개발

17.4 다카라바이오 주식회사

17.4.1 회사 스냅샷

17.4.2 수익 분석

17.4.3 회사 점유율 분석

17.4.4 제품 포트폴리오

17.4.5 최근 개발 사항

17.5 홀로직 주식회사

17.5.1 회사 스냅샷

17.5.2 수익 분석

17.5.3 회사 점유율 분석

17.5.4 제품 포트폴리오

17.5.5 최근 개발 사항

17.6 적응형 생명공학

17.6.1 회사 스냅샷

17.6.2 수익 분석

17.6.3 제품 포트폴리오

17.6.4 최근 개발

17.7 알토나 진단

17.7.1 회사 스냅샷

17.7.2 제품 포트폴리오

17.7.3 최근 개발 사항

17.8 아커 진단 유한회사

17.8.1 회사 스냅샷

17.8.2 제품 포트폴리오

17.8.3 최근 개발 사항

17.9 백 다이어그노스틱스 GMBH

17.9.1 회사 스냅샷

17.9.2 제품 포트폴리오

17.9.3 최근 개발 사항

17.1 바이오포르투나 리미티드

17.10.1 회사 스냅샷

17.10.2 제품 포트폴리오

17.10.3 최근 개발

17.11 비오메리유

17.11.1 회사 스냅샷

17.11.2 수익 분석

17.11.3 제품 포트폴리오

17.11.4 최근 개발 사항

17.12 바이오라드 연구소 주식회사

17.12.1 회사 스냅샷

17.12.2 수익 분석

17.12.3 제품 포트폴리오

17.12.4 최근 개발

17.13 바이오타입 GMBH

17.13.1 회사 스냅샷

17.13.2 제품 포트폴리오

17.13.3 최근 개발 사항

17.14 카레드엑스 주식회사

17.14.1 회사 스냅샷

17.14.2 수익 분석

17.14.3 제품 포트폴리오

17.14.4 최근 개발 사항

17.15 클로닛 SRL

17.15.1 회사 스냅샷

17.15.2 제품 포트폴리오

17.15.3 최근 개발

17.16 롱우드 진단 SL

17.16.1 회사 스냅샷

17.16.2 제품 포트폴리오

17.16.3 최근 개발 사항

17.17 디아소린 스파

17.17.1 회사 스냅샷

17.17.2 수익 분석

17.17.3 제품 포트폴리오

17.17.4 최근 개발

17.18 엘리트그룹

17.18.1 회사 스냅샷

17.18.2 제품 포트폴리오

17.18.3 최근 개발 사항

17.19 유로핀스 비라코르

17.19.1 회사 스냅샷

17.19.2 제품 포트폴리오

17.19.3 최근 개발 사항

17.2 호리바 주식회사

17.20.1 회사 스냅샷

17.20.2 수익 분석

17.20.3 제품 포트폴리오

17.20.4 최근 개발

17.21 일루미나 주식회사

17.21.1 회사 스냅샷

17.21.2 수익 분석

17.21.3 제품 포트폴리오

17.21.4 최근 개발 사항

17.22 면역학

17.22.1 회사 스냅샷

17.22.2 제품 포트폴리오

17.22.3 최근 개발 사항

17.23 LABORATORY CORPORATION OF AMERICA HOLDINGS.

17.23.1 회사 스냅샷

17.23.2 수익 분석

17.23.3 제품 포트폴리오

17.23.4 최근 개발 사항

17.24 LUMINEX CORPORATION. (DIASORIN의 자회사)

17.24.1 회사 스냅샷

17.24.2 수익 분석

17.24.3 제품 포트폴리오

17.24.4 최근 개발

17.25 나노스트링

17.25.1 회사 스냅샷

17.25.2 수익 분석

17.25.3 제품 포트폴리오

17.25.4 최근 개발

17.26 병리학

17.26.1 회사 스냅샷

17.26.2 제품 포트폴리오

17.26.3 최근 개발 사항

17.27 보존 솔루션 주식회사

17.27.1 회사 스냅샷

17.27.2 제품 포트폴리오

17.27.3 최근 개발 사항

17.28 퀴아젠

17.28.1 회사 스냅샷

17.28.2 수익 분석

17.28.3 제품 포트폴리오

17.28.4 최근 개발 사항

17.29 RANDOX 연구소 LTD.

17.29.1 회사 스냅샷

17.29.2 제품 포트폴리오

17.29.3 최근 개발 사항

17.3 스트라이커

17.30.1 회사 스냅샷

17.30.2 수익 분석

17.30.3 제품 포트폴리오

17.30.4 최근 개발

17.31 트랜스메딕스

17.31.1 회사 스냅샷

17.31.2 수익 분석

17.31.3 제품 포트폴리오

17.31.4 최근 개발 사항

17.32 초음속.

17.32.1 회사 스냅샷

17.32.2 제품 포트폴리오

17.32.3 최근 개발

17.33 짐머 바이오멧

17.33.1 회사 스냅샷

17.33.2 수익 분석

17.33.3 제품 포트폴리오

17.33.4 최근 개발 사항

18 설문지

19 관련 보고서

표 목록

표 1 중동 및 아프리카 이식 진단 시장, 제품 유형별, 2020-2029년(백만 달러)

표 2 중동 및 아프리카 이식 진단 시장에서의 이식 진단 도구, 지역별, 2020-2029년(백만 달러)

표 3 중동 및 아프리카 이식 진단 시장에서의 이식 진단 기기, 제품 유형별, 2020-2029년(백만 달러)

표 4 중동 및 아프리카 자동화 시스템 이식 진단 시장, 제품 유형별, 2020-2029년(백만 달러)

표 5 중동 및 아프리카 이식 진단 시장에서의 이식 진단 키트, 제품 유형별, 2020-2029년(백만 달러)

표 6 중동 및 아프리카 이식 진단 소프트웨어, 지역별 이식 진단 시장, 2020-2029 (백만 달러)

표 7 중동 및 아프리카 이식 진단 소프트웨어 시장, 제품 유형별, 2020-2029년(백만 달러)

표 8 중동 및 아프리카 이식 진단 시약 시장, 지역별, 2020-2029년(백만 달러)

표 9 중동 및 아프리카 이식 진단 시약 시장, 제품 유형별, 2020-2029년(백만 달러)

표 10 중동 및 아프리카 이식 진단 시장, 기술별, 2020-2029년(백만 달러)

표 11 중동 및 아프리카 지역별 이식 진단 시장에서의 PCR 기반 분자 검사, 2020-2029년(백만 달러)

표 12 중동 및 아프리카 이식 진단 시장에서의 PCR 기반 분자 검사, 기술별, 2020-2029년(백만 달러)

표 13 중동 및 아프리카 이식 진단 시장에서의 시퀀싱 기반 분자 검사, 지역별, 2020-2029년(백만 달러)

표 14 중동 및 아프리카 이식 진단 시장에서의 시퀀싱 기반 분자 검사, 기술별, 2020-2029년(백만 달러)

표 15 중동 및 아프리카 이식 진단 시장, 이식 유형별, 2020-2029년(백만 달러)

표 16 중동 및 아프리카 지역별 이식 진단 시장에서의 고형 장기 이식, 2020-2029년(백만 달러)

표 17 중동 및 아프리카 이식 진단 시장에서의 고형 장기 이식, 이식 유형별, 2020-2029년(백만 달러)

표 18 중동 및 아프리카 지역별 이식 진단 시장에서의 줄기세포 이식, 2020-2029년(백만 달러)

표 19 중동 및 아프리카 이식 진단 시장에서의 줄기세포 이식, 이식 유형별, 2020-2029년(백만 달러)

표 20 중동 및 아프리카 연조직 이식의 지역별 이식 진단 시장, 2020-2029년(백만 달러)

표 21 중동 및 아프리카 연조직 이식의 이식 진단 시장, 이식 유형별, 2020-2029년(백만 달러)

표 22 중동 및 아프리카 골수 이식의 이식 진단 시장, 지역별, 2020-2029 (백만 달러)

표 23 중동 및 아프리카 골수 이식의 이식 진단 시장, 이식 유형별, 2020-2029년(백만 달러)

표 24 중동 및 아프리카 기타 지역별 이식 진단 시장, 2020-2029년(백만 달러)

표 25 중동 및 아프리카 이식 진단 시장, 응용 분야별, 2020-2029년(백만 달러)

표 26 중동 및 아프리카 지역별 이식 진단 시장에서의 진단 응용 프로그램, 2020-2029년(백만 달러)

표 27 중동 및 아프리카 이식 진단 시장의 진단 응용 프로그램, 제품 유형별, 2020-2029년(백만 달러)

표 28 중동 및 아프리카 이식 진단 기기 시장(제품 유형별), 2020-2029년(백만 달러)

표 29 중동 및 아프리카 이식 진단 소프트웨어, 제품 유형별 중동 및 아프리카 이식 진단 시장, 2020-2029(백만 달러)

표 30 중동 및 아프리카 이식 진단 시약 중동 및 아프리카 이식 진단 시장, 제품 유형별, 2020-2029년(백만 달러)

표 31 중동 및 아프리카 이식 진단 시장에서의 연구 응용 프로그램, 지역별, 2020-2029년(백만 달러)

표 32 중동 및 아프리카 이식 진단 시장의 연구 응용 프로그램, 제품 유형별, 2020-2029년(백만 달러)

표 33 중동 및 아프리카 이식 진단 기기 시장, 제품 유형별 중동 및 아프리카 이식 진단 기기, 2020-2029년(백만 달러)

표 34 중동 및 아프리카 이식 진단 소프트웨어, 제품 유형별 중동 및 아프리카 이식 진단 시장, 2020-2029년(백만 달러)

표 35 중동 및 아프리카 이식 진단 시약, 제품 유형별 중동 및 아프리카 이식 진단 시장, 2020-2029년(백만 달러)

표 36 중동 및 아프리카 이식 진단 시장, 최종 사용자별, 2020-2029년(백만 달러)

표 37 중동 및 아프리카 지역별 이식 진단 시장의 병원 및 이식 센터, 2020-2029년 지역별 (백만 달러)

표 38 중동 및 아프리카 지역별 이식 진단 시장의 상업 서비스 제공자, 2020-2029년(백만 달러)

표 39 중동 및 아프리카 지역별 이식 진단 시장 연구소 및 학술 기관, 2020-2029년(백만 달러)

표 40 중동 및 아프리카 기타 지역별 이식 진단 시장, 2020-2029년(백만 달러)

표 41 중동 및 아프리카 이식 진단 시장, 유통 채널별, 2020-2029년(백만 달러)

표 42 중동 및 아프리카 지역별 이식 진단 시장 직접 입찰, 2020-2029년(백만 달러)

표 43 중동 및 아프리카 이식 진단 시장의 소매 판매, 지역별, 2020-2029년(백만 달러)

표 44 중동 및 아프리카 기타 지역별 이식 진단 시장, 2020-2029년(백만 달러)

표 45 중동 및 아프리카 이식 진단 시장, 국가별, 2020-2029년(백만 달러)

표 46 중동 및 아프리카 이식 진단 시장, 제품 유형별, 2020-2029년(백만 달러)

표 47 중동 및 아프리카 이식 진단 장비 시장, 제품 유형별, 2020-2029년(백만 달러)

표 48 중동 및 아프리카 자동화 시스템 이식 진단 시장, 제품 유형별, 2020-2029년(백만 달러)

표 49 중동 및 아프리카 이식 진단 시장에서의 이식 진단 키트, 제품 유형별, 2020-2029년(백만 달러)

표 50 중동 및 아프리카 이식 진단 소프트웨어 시장, 제품 유형별, 2020-2029년(백만 달러)

표 51 중동 및 아프리카 이식 진단 시약 시장, 제품 유형별, 2020-2029년(백만 달러)

표 52 중동 및 아프리카 이식 진단 시장, 기술별, 2020-2029년(백만 달러)

표 53 중동 및 아프리카 이식 진단 시장에서의 PCR 기반 분자 검사, 기술별, 2020-2029년(백만 달러)

표 54 중동 및 아프리카 이식 진단 시장에서의 시퀀스 기반 분자 분석, 제품 유형별, 2020-2029년(백만 달러)

표 55 중동 및 아프리카 이식 진단 시장, 이식 유형별, 2020-2029년(백만 달러)

표 56 중동 및 아프리카 이식 진단 시장에서의 고형 장기 이식, 이식 유형별, 2020-2029년(백만 달러)

표 57 중동 및 아프리카 이식 진단 시장에서의 줄기세포 이식, 이식 유형별, 2020-2029년(백만 달러)

표 58 중동 및 아프리카 연조직 이식의 이식 진단 시장, 이식 유형별, 2020-2029년(백만 달러)

표 59 중동 및 아프리카 골수 이식 이식 진단 시장, 이식 유형별, 2020-2029(백만 달러)

표 60 중동 및 아프리카 이식 진단 시장, 응용 분야별, 2020-2029년(백만 달러)

표 61 중동 및 아프리카 진단 응용 프로그램 이식 진단 시장, 제품 유형별, 2020-2029년(백만 달러)

표 62 중동 및 아프리카 이식 진단 장비 시장, 제품 유형별, 2020-2029년(백만 달러)

표 63 중동 및 아프리카 이식 진단 소프트웨어 시장, 제품 유형별, 2020-2029년(백만 달러)

표 64 중동 및 아프리카 이식 진단 시약 시장, 제품 유형별, 2020-2029년(백만 달러)

표 65 중동 및 아프리카 연구 응용 프로그램 이식 진단 시장, 제품 유형별, 2020-2029년(백만 달러)

표 66 중동 및 아프리카 이식 진단 장비 시장, 제품 유형별, 2020-2029년(백만 달러)

표 67 중동 및 아프리카 이식 진단 소프트웨어 시장, 제품 유형별, 2020-2029년(백만 달러)

표 68 중동 및 아프리카 이식 진단 시약 시장, 제품 유형별, 2020-2029년(백만 달러)

표 69 중동 및 아프리카 이식 진단 시장, 최종 사용자별, 2020-2029년(백만 달러)

표 70 중동 및 아프리카 이식 진단 시장, 유통 채널별, 2020-2029년(백만 달러)

표 71 남아프리카 이식 진단 시장, 제품 유형별, 2020-2029년(백만 달러)

표 72 남아프리카 이식 진단 장비 시장 내 제품 유형별 이식 진단 장비, 2020-2029년(백만 달러)

표 73 남아프리카 공화국 자동 피펫 및 디스펜서, 제품 유형별, 2020-2029 볼륨(단위)

표 74 남아프리카 공화국 자동 피펫 및 디스펜서, 제품 유형별, 2020-2029 ASP(USD)

표 75 남아프리카 자동화 시스템 이식 진단 시장, 제품 유형별, 2020-2029년(백만 달러)

표 76 남아프리카 이식 진단 시장에서의 제품 유형별 이식 진단 장비, 2020-2029년 수량(대)

표 77 남아프리카 이식 진단 키트, 제품 유형별 이식 진단 시장, 2020-2029 ASP(USD)

표 78 남아프리카 이식 진단 시장에서의 제품 유형별 이식 진단 장비, 2020-2029년 수량(대)

표 79 남아프리카 이식 진단 키트, 제품 유형별 이식 진단 시장, 2020-2029 ASP(USD)

표 80 남아프리카 이식 진단 키트, 제품 유형별 이식 진단 시장, 2020-2029년(백만 달러)

표 81 남아프리카 이식 진단 키트, 제품 유형별 이식 진단 시장, 2020-2029 수량(단위)

표 82 남아프리카 이식 진단 키트, 제품 유형별 이식 진단 시장, 2020-2029 ASP(USD)

표 83 남아프리카 이식 진단 소프트웨어 시장, 제품 유형별, 2020-2029년(백만 달러)

표 84 남아프리카 이식 진단 시약 시장, 제품 유형별, 2020-2029년(백만 달러)

표 85 남아프리카 이식 진단 시약 시장 내 제품 유형별, 2020-2029년 수량(단위)

표 86 남아프리카 이식 진단 시약 시장, 제품 유형별, 2020-2029 ASP(USD)

표 87 기술별 남아프리카 이식 진단 시장, 2020-2029년(백만 달러)

표 88 남아프리카 공화국 이식 진단 시장에서의 PCR 기반 분자 검사, 기술별, 2020-2029년(백만 달러)

표 89 남아프리카 공화국 이식 진단 시장에서의 시퀀스 기반 분자 분석, 제품 유형별, 2020-2029년(백만 달러)

표 90 남아프리카 이식 진단 시장, 이식 유형별, 2020-2029년(백만 달러)

표 91 2020-2029년 이식 유형별 남아프리카 공화국 고형 장기 이식 이식 진단 시장(백만 달러)

표 92 이식 진단 시장에서의 남아프리카 줄기세포 이식, 이식 유형별, 2020-2029년(백만 달러)

표 93 이식 진단 시장에서의 남아프리카 연조직 이식, 이식 유형별, 2020-2029년(백만 달러)

표 94 이식 진단 시장에서의 남아프리카 골수 이식, 이식 유형별, 2020-2029년(백만 달러)

표 95 남아프리카 이식 진단 시장, 응용 분야별, 2020-2029년(백만 달러)

표 96 남아프리카 진단 응용 프로그램 이식 진단 시장, 제품 유형별, 2020-2029년(백만 달러)

표 97 남아프리카 이식 진단 장비 시장 내 제품 유형별 이식 진단 장비, 2020-2029년(백만 달러)

표 98 남아프리카 이식 진단 소프트웨어 시장, 제품 유형별, 2020-2029년(백만 달러)

표 99 남아프리카 이식 진단 시약 시장, 제품 유형별, 2020-2029년(백만 달러)

표 100 남아프리카 공화국 연구 응용 프로그램 이식 진단 시장, 제품 유형별, 2020-2029년(백만 달러)

표 101 남아프리카 이식 진단 장비 시장 내 제품 유형별, 2020-2029년(백만 달러)

표 102 남아프리카 이식 진단 소프트웨어, 제품 유형별 이식 진단 시장, 2020-2029년(백만 달러)

표 103 남아프리카 이식 진단 시약 시장, 제품 유형별, 2020-2029년(백만 달러)

표 104 최종 사용자별 남아프리카 이식 진단 시장, 2020-2029년(백만 달러)

표 105 유통 채널별 남아프리카 이식 진단 시장, 2020-2029년(백만 달러)

표 106 사우디 아라비아 이식 진단 시장, 제품 유형별, 2020-2029년(백만 달러)

표 107 사우디 아라비아 이식 진단 장비 시장, 제품 유형별, 2020-2029년(백만 달러)

표 108 사우디 아라비아 자동 피펫 및 디스펜서, 제품 유형별, 2020-2029 용량(단위)

표 109 사우디 아라비아 자동 피펫 및 디스펜서, 제품 유형별, 2020-2029 ASP(USD)

표 110 사우디 아라비아 자동화 시스템 이식 진단 시장, 제품 유형별, 2020-2029년(백만 달러)

표 111 사우디 아라비아 이식 진단 시장에서의 이식 진단 기기, 제품 유형별, 2020-2029년 수량(대)

표 112 사우디 아라비아 이식 진단 키트, 제품 유형별 이식 진단 시장, 2020-2029 ASP(USD)

표 113 사우디 아라비아 이식 진단 시장에서의 이식 진단 기기, 제품 유형별, 2020-2029년 수량(대)

표 114 사우디 아라비아 이식 진단 키트, 제품 유형별 이식 진단 시장, 2020-2029 ASP(USD)

표 115 사우디 아라비아 이식 진단 키트, 제품 유형별 이식 진단 시장, 2020-2029년(백만 달러)

표 116 사우디 아라비아 이식 진단 키트, 제품 유형별 이식 진단 시장, 2020-2029 수량(단위)

표 117 사우디 아라비아 이식 진단 키트, 제품 유형별 이식 진단 시장, 2020-2029 ASP(USD)

표 118 사우디 아라비아 이식 진단 소프트웨어 시장, 제품 유형별, 2020-2029년(백만 달러)

표 119 사우디 아라비아 이식 진단 시약 시장, 제품 유형별, 2020-2029년(백만 달러)

표 120 사우디 아라비아 이식 진단 시약 시장 내 제품 유형별, 2020-2029년 수량(단위)

표 121 사우디 아라비아 이식 진단 시약 시장, 제품 유형별, 2020-2029 ASP(USD)

표 122 사우디 아라비아 이식 진단 시장, 기술별, 2020-2029 (백만 달러)

표 123 사우디 아라비아 이식 진단 시장에서의 PCR 기반 분자 검사, 기술별, 2020-2029년(백만 달러)

표 124 사우디 아라비아 이식 진단 시장에서의 시퀀스 기반 분자 분석, 제품 유형별, 2020-2029년(백만 달러)

표 125 사우디 아라비아 이식 진단 시장, 이식 유형별, 2020-2029 (백만 달러)

표 126 사우디 아라비아 이식 진단 시장에서의 고형 장기 이식, 이식 유형별, 2020-2029년(백만 달러)

표 127 이식 진단 시장에서의 사우디 아라비아 줄기세포 이식, 이식 유형별, 2020-2029년(백만 달러)

표 128 사우디 아라비아 연부조직 이식, 이식 유형별 이식 진단 시장, 2020-2029(백만 달러)

표 129 사우디 아라비아 골수 이식 이식 진단 시장, 이식 유형별, 2020-2029 (백만 달러)

표 130 사우디 아라비아 이식 진단 시장, 응용 분야별, 2020-2029년(백만 달러)

표 131 사우디 아라비아 진단 응용 프로그램 이식 진단 시장, 제품 유형별, 2020-2029년(백만 달러)

표 132 사우디 아라비아 이식 진단 장비 시장 내 제품 유형별, 2020-2029년(백만 달러)

표 133 사우디 아라비아 이식 진단 소프트웨어 시장, 제품 유형별, 2020-2029년(백만 달러)

표 134 사우디 아라비아 이식 진단 시약 시장, 제품 유형별, 2020-2029년(백만 달러)

표 135 사우디 아라비아 연구 응용 프로그램 이식 진단 시장, 제품 유형별, 2020-2029년(백만 달러)

표 136 사우디 아라비아 이식 진단 장비 시장, 제품 유형별, 2020-2029년(백만 달러)

표 137 사우디 아라비아 이식 진단 소프트웨어 시장, 제품 유형별, 2020-2029년(백만 달러)

표 138 사우디 아라비아 이식 진단 시약 시장, 제품 유형별, 2020-2029년(백만 달러)

표 139 사우디 아라비아 이식 진단 시장, 최종 사용자별, 2020-2029(백만 달러)

표 140 사우디 아라비아 이식 진단 시장, 유통 채널별, 2020-2029년(백만 달러)

표 141 UAE 이식 진단 시장, 제품 유형별, 2020-2029년(백만 달러)

표 142 UAE 이식 진단 장비 시장, 제품 유형별, 2020-2029(백만 달러)

표 143 UAE 자동 피펫 및 디스펜서, 제품 유형별, 2020-2029 용량(단위)

표 144 UAE 자동 피펫 및 디스펜서, 제품 유형별, 2020-2029 ASP(USD)

표 145 UAE 자동화 시스템 이식 진단 시장, 제품 유형별, 2020-2029(백만 달러)

표 146 UAE 이식 진단 장비 시장, 제품 유형별, 2020-2029 수량(대)

표 147 UAE 이식 진단 키트, 제품 유형별 이식 진단 시장, 2020-2029 ASP(USD)

표 148 UAE 이식 진단 장비 시장, 제품 유형별, 2020-2029 수량(대)

표 149 UAE 이식 진단 키트, 제품 유형별 이식 진단 시장, 2020-2029 ASP(USD)

표 150 UAE 이식 진단 키트, 제품 유형별 이식 진단 시장, 2020-2029(백만 달러)

표 151 UAE 이식 진단 키트, 제품 유형별 이식 진단 시장, 2020-2029 수량(단위)

표 152 이식 진단 시장에서의 UAE 이식 진단 키트, 제품 유형별, 2020-2029 ASP(USD)

표 153 UAE 이식 진단 소프트웨어, 제품 유형별 이식 진단 시장, 2020-2029(백만 달러)

표 154 UAE 이식 진단 시약, 제품 유형별 이식 진단 시장, 2020-2029(백만 달러)

표 155 이식 진단 시장에서의 UAE 이식 진단 시약, 제품 유형별, 2020-2029 수량(단위)

표 156 UAE 이식 진단 시약 시장, 제품 유형별, 2020-2029 ASP(USD)

표 157 기술별 UAE 이식 진단 시장, 2020-2029년(백만 달러)

표 158 UAE PCR 기반 분자 검사 시장, 기술별, 2020-2029(백만 달러)

표 159 UAE SEQUENCE 기반 분자 검사 시장, 제품 유형별, 2020-2029(백만 달러)

표 160 이식 유형별 UAE 이식 진단 시장, 2020-2029년(백만 달러)

표 161 이식 진단 시장에서의 UAE 고형 장기 이식, 이식 유형별, 2020-2029년(백만 달러)

표 162 이식 진단 시장에서의 UAE 줄기세포 이식, 이식 유형별, 2020-2029년(백만 달러)

표 163 이식 진단 시장에서의 UAE 연조직 이식, 이식 유형별, 2020-2029년(백만 달러)

표 164 이식 진단 시장에서의 UAE 골수 이식, 이식 유형별, 2020-2029년(백만 달러)

표 165 UAE 이식 진단 시장, 응용 분야별, 2020-2029(백만 달러)

표 166 UAE 진단 응용 프로그램 이식 진단 시장, 제품 유형별, 2020-2029년(백만 달러)

표 167 UAE 이식 진단 장비 시장, 제품 유형별, 2020-2029(백만 달러)

표 168 UAE 이식 진단 소프트웨어, 제품 유형별 이식 진단 시장, 2020-2029(백만 달러)

표 169 UAE 이식 진단 시약, 제품 유형별 이식 진단 시장, 2020-2029(백만 달러)

표 170 UAE 연구 응용 프로그램 이식 진단 시장, 제품 유형별, 2020-2029년(백만 달러)

표 171 UAE 이식 진단 장비 시장, 제품 유형별, 2020-2029년(백만 달러)

표 172 UAE 이식 진단 소프트웨어, 제품 유형별 이식 진단 시장, 2020-2029(백만 달러)

표 173 UAE 이식 진단 시약 시장, 제품 유형별, 2020-2029(백만 달러)

표 174 최종 사용자별 UAE 이식 진단 시장, 2020-2029년(백만 달러)

표 175 유통 채널별 UAE 이식 진단 시장, 2020-2029년(백만 달러)

표 176 이집트 이식 진단 시장, 제품 유형별, 2020-2029년(백만 달러)

표 177 이집트 이식 진단 장비 시장, 제품 유형별, 2020-2029년(백만 달러)

표 178 이집트 자동 피펫 및 디스펜서, 제품 유형별, 2020-2029 용량(단위)

표 179 이집트 자동 피펫 및 디스펜서, 제품 유형별, 2020-2029 ASP(USD)

표 180 이집트 자동화 시스템 이식 진단 시장, 제품 유형별, 2020-2029년(백만 달러)

표 181 이집트 이식 진단 장비 시장, 제품 유형별, 2020-2029 수량(단위)

표 182 이식 진단 시장에서의 이집트 이식 진단 키트, 제품 유형별, 2020-2029 ASP(USD)

표 183 이집트 이식 진단 장비 시장, 제품 유형별, 2020-2029년 볼륨(단위)

표 184 이집트 이식 진단 키트, 제품 유형별 이식 진단 시장, 2020-2029 ASP(USD)

표 185 이식 진단 시장에서의 이집트 이식 진단 키트, 제품 유형별, 2020-2029년(백만 달러)

표 186 이식 진단 시장에서의 이집트 이식 진단 키트, 제품 유형별, 2020-2029년 수량(단위)

표 187 이식 진단 시장에서의 이집트 이식 진단 키트, 제품 유형별, 2020-2029 ASP(USD)

표 188 이집트 이식 진단 소프트웨어, 제품 유형별 이식 진단 시장, 2020-2029년(백만 달러)

표 189 이집트 이식 진단 시약, 제품 유형별 이식 진단 시장, 2020-2029 (백만 달러)

표 190 이집트 이식 진단 시약, 제품 유형별 이식 진단 시장, 2020-2029 수량(단위)

표 191 이집트 이식 진단 시약, 제품 유형별 이식 진단 시장, 2020-2029 ASP(USD)

표 192 이집트 이식 진단 시장, 기술별, 2020-2029 (백만 달러)

표 193 이집트 이식 진단 시장에서의 PCR 기반 분자 검사, 기술별, 2020-2029년(백만 달러)

표 194 이집트 이식 진단 시장에서의 서열 기반 분자 분석, 제품 유형별, 2020-2029년(백만 달러)

표 195 이식 유형별 이집트 이식 진단 시장, 2020-2029년(백만 달러)

표 196 이집트 이식 진단 시장에서의 고형 장기 이식, 이식 유형별, 2020-2029년(백만 달러)

표 197 이식 진단 시장에서의 이집트 줄기세포 이식, 이식 유형별, 2020-2029년(백만 달러)

표 198 이식 진단 시장에서의 이집트 연부조직 이식, 이식 유형별, 2020-2029년(백만 달러)

표 199 이식 진단 시장에서의 이집트 골수 이식, 이식 유형별, 2020-2029년(백만 달러)

표 200 이집트 이식 진단 시장, 응용 분야별, 2020-2029(백만 달러)

표 201 이집트 진단 응용 프로그램 이식 진단 시장, 제품 유형별, 2020-2029년(백만 달러)

표 202 이집트 이식 진단 장비 시장, 제품 유형별, 2020-2029년(백만 달러)

표 203 이집트 이식 진단 소프트웨어, 제품 유형별 이식 진단 시장, 2020-2029(백만 달러)

표 204 이집트 이식 진단 시약, 제품 유형별 이식 진단 시장, 2020-2029 (백만 달러)

표 205 이집트 연구 응용 프로그램 이식 진단 시장, 제품 유형별, 2020-2029년(백만 달러)

표 206 이집트 이식 진단 장비 시장, 제품 유형별, 2020-2029년(백만 달러)

표 207 이집트 이식 진단 소프트웨어, 제품 유형별 이식 진단 시장, 2020-2029 (백만 달러)

표 208 이집트 이식 진단 시약, 제품 유형별 이식 진단 시장, 2020-2029 (백만 달러)

표 209 이집트 이식 진단 시장, 최종 사용자별, 2020-2029(백만 달러)

표 210 이집트 이식 진단 시장, 유통 채널별, 2020-2029년(백만 달러)

표 211 이스라엘 이식 진단 시장, 제품 유형별, 2020-2029년(백만 달러)

표 212 이스라엘 이식 진단 장비 시장, 제품 유형별, 2020-2029년(백만 달러)

표 213 이스라엘 자동 피펫 및 디스펜서, 제품 유형별, 2020-2029 용량(단위)

표 214 이스라엘 자동 피펫 및 디스펜서, 제품 유형별, 2020-2029 ASP(USD)

표 215 이스라엘 자동화 시스템 이식 진단 시장, 제품 유형별, 2020-2029년(백만 달러)

표 216 이스라엘 이식 진단 기기 시장 내 제품 유형별, 2020-2029년 수량(대)

표 217 이스라엘 이식 진단 키트, 제품 유형별 이식 진단 시장, 2020-2029 ASP(USD)

표 218 이스라엘 이식 진단 기기 시장 내 제품 유형별, 2020-2029년 수량(대)

표 219 이스라엘 이식 진단 키트, 제품 유형별 이식 진단 시장, 2020-2029 ASP(USD)

표 220 이스라엘 이식 진단 키트, 제품 유형별 이식 진단 시장, 2020-2029년(백만 달러)

표 221 이스라엘 이식 진단 키트, 제품 유형별 이식 진단 시장, 2020-2029 수량(단위)

표 222 이스라엘 이식 진단 키트, 제품 유형별 이식 진단 시장, 2020-2029 ASP(USD)

표 223 이스라엘 이식 진단 소프트웨어, 제품 유형별 이식 진단 시장, 2020-2029(백만 달러)

표 224 이스라엘 이식 진단 시약 시장, 제품 유형별, 2020-2029년(백만 달러)

표 225 이스라엘 이식 진단 시약 시장 내 제품 유형별, 2020-2029년 수량(단위)

표 226 이스라엘 이식 진단 시약, 제품 유형별 이식 진단 시장, 2020-2029 ASP(USD)

표 227 이스라엘 이식 진단 시장, 기술별, 2020-2029 (백만 달러)

표 228 이스라엘 이식 진단 시장에서의 PCR 기반 분자 검사, 기술별, 2020-2029년(백만 달러)

표 229 이스라엘의 이식 진단 시장에서의 시퀀스 기반 분자 분석, 제품 유형별, 2020-2029년(백만 달러)

표 230 이스라엘 이식 진단 시장, 이식 유형별, 2020-2029 (백만 달러)

표 231 이스라엘 이식 진단 시장에서의 고형 장기 이식, 이식 유형별, 2020-2029년(백만 달러)

표 232 이스라엘 줄기세포 이식, 이식 유형별 이식 진단 시장, 2020-2029(백만 달러)

표 233 이스라엘 연부조직 이식, 이식 유형별 이식 진단 시장, 2020-2029(백만 달러)

표 234 이스라엘 골수 이식 이식 진단 시장, 이식 유형별, 2020-2029 (백만 달러)

표 235 이스라엘 이식 진단 시장, 응용 분야별, 2020-2029년(백만 달러)

표 236 이스라엘 진단 응용 프로그램 이식 진단 시장, 제품 유형별, 2020-2029년(백만 달러)

표 237 이스라엘 이식 진단 장비 시장 내 제품 유형별 이식 진단 장비, 2020-2029년(백만 달러)

표 238 이스라엘 이식 진단 소프트웨어, 제품 유형별 이식 진단 시장, 2020-2029(백만 달러)

표 239 이스라엘 이식 진단 시약 시장, 제품 유형별, 2020-2029년(백만 달러)

표 240 이스라엘 연구 응용 프로그램 이식 진단 시장, 제품 유형별, 2020-2029년(백만 달러)

표 241 이스라엘 이식 진단 장비 시장, 제품 유형별, 2020-2029년(백만 달러)

표 242 이스라엘 이식 진단 소프트웨어, 제품 유형별 이식 진단 시장, 2020-2029(백만 달러)

표 243 이스라엘 이식 진단 시약 시장, 제품 유형별, 2020-2029년(백만 달러)

표 244 이스라엘 이식 진단 시장, 최종 사용자별, 2020-2029(백만 달러)

표 245 이스라엘 이식 진단 시장, 유통 채널별, 2020-2029년(백만 달러)

표 246 중동 및 아프리카의 나머지 지역 이식 진단 시장, 제품 유형별, 2020-2029년(백만 달러)

그림 목록

그림 1 중동 및 아프리카 이식 진단 시장: 세분화

그림 2 중동 및 아프리카 이식 진단 시장: 데이터 삼각 측량

그림 3 중동 및 아프리카 이식 진단 시장: DROC 분석

그림 4 중동 및 아프리카 이식 진단 시장: 중동 및 아프리카 대 지역 시장 분석

그림 5 중동 및 아프리카 이식 진단 시장: 회사 연구 분석

그림 6 중동 및 아프리카 이식 진단 시장: 인터뷰 인구 통계

그림 7 중동 및 아프리카 이식 진단 시장: 시장 응용 범위 그리드

그림 8 중동 및 아프리카 이식 진단 시장: DBMR 시장 위치 그리드

그림 9 중동 및 아프리카 이식 진단 시장: 공급업체 점유율 분석

그림 10 중동 및 아프리카 이식 진단 시장: 세분화

그림 11 이식 진단 사용 증가는 예측 기간 동안 중동 및 아프리카 이식 진단 시장을 주도할 것으로 예상됩니다.

그림 12 이식 진단 장비 부문은 2022년 및 2029년 중동 및 아프리카 이식 진단 시장에서 가장 큰 점유율을 차지할 것으로 예상됩니다.

그림 13 중동 및 아프리카 이식 진단 시장의 동인, 제약, 기회 및 과제

그림 14 중동 및 아프리카 이식 진단 시장: 제품 유형별, 2021년

그림 15 중동 및 아프리카 이식 진단 시장: 제품 유형별, 2022-2029년(백만 달러)

그림 16 중동 및 아프리카 이식 진단 시장: 제품 유형별, CAGR(2022-2029)

그림 17 중동 및 아프리카 이식 진단 시장: 제품 유형별, 수명선 곡선

그림 18 중동 및 아프리카 이식 진단 시장: 기술별, 2021

그림 19 중동 및 아프리카 이식 진단 시장: 기술별, 2022-2029년(백만 달러)

그림 20 중동 및 아프리카 이식 진단 시장: 기술별, CAGR(2022-2029)

그림 21 중동 및 아프리카 이식 진단 시장: 기술별, 수명선 곡선

그림 22 중동 및 아프리카 이식 진단 시장: 이식 유형별, 2021

그림 23 중동 및 아프리카 이식 진단 시장: 이식 유형별, 2022-2029년(백만 달러)

그림 24 중동 및 아프리카 이식 진단 시장: 이식 유형별, CAGR(2022-2029)

그림 25 중동 및 아프리카 이식 진단 시장: 이식 유형별, 수명선 곡선

그림 26 중동 및 아프리카 이식 진단 시장: 응용 분야별, 2021

그림 27 중동 및 아프리카 이식 진단 시장: 응용 분야별, 2022-2029년(백만 달러)

그림 28 중동 및 아프리카 이식 진단 시장: 응용 분야별, CAGR(2022-2029)

그림 29 중동 및 아프리카 이식 진단 시장: 응용 분야별, 수명선 곡선

그림 30 중동 및 아프리카 이식 진단 시장: 최종 사용자별, 2021년

그림 31 중동 및 아프리카 이식 진단 시장: 최종 사용자별, 2022-2029년(백만 달러)

그림 32 중동 및 아프리카 이식 진단 시장: 최종 사용자별, CAGR(2022-2029)

그림 33 중동 및 아프리카 이식 진단 시장: 최종 사용자별, 수명선 곡선

그림 34 중동 및 아프리카 이식 진단 시장: 유통 채널별, 2021년

그림 35 중동 및 아프리카 이식 진단 시장: 유통 채널별, 2022-2029년(백만 달러)

그림 36 중동 및 아프리카 이식 진단 시장: 유통 채널별, CAGR(2022-2029)

그림 37 중동 및 아프리카 이식 진단 시장: 유통 채널별, 수명선 곡선

그림 38 중동 및 아프리카 이식 진단 시장: 스냅샷(2021)

그림 39 중동 및 아프리카 이식 진단 시장: 국가별(2021년)

그림 40 중동 및 아프리카 이식 진단 시장: 국가별(2022년 및 2029년)

그림 41 중동 및 아프리카 이식 진단 시장: 국가별(2021년 및 2029년)

그림 42 중동 및 아프리카 이식 진단 시장: 제품 유형별(2022-2029)

그림 43 중동 및 아프리카 이식 진단 시장: 회사 점유율 2021(%)

연구 방법론

데이터 수집 및 기준 연도 분석은 대규모 샘플 크기의 데이터 수집 모듈을 사용하여 수행됩니다. 이 단계에는 다양한 소스와 전략을 통해 시장 정보 또는 관련 데이터를 얻는 것이 포함됩니다. 여기에는 과거에 수집한 모든 데이터를 미리 검토하고 계획하는 것이 포함됩니다. 또한 다양한 정보 소스에서 발견되는 정보 불일치를 검토하는 것도 포함됩니다. 시장 데이터는 시장 통계 및 일관된 모델을 사용하여 분석하고 추정합니다. 또한 시장 점유율 분석 및 주요 추세 분석은 시장 보고서의 주요 성공 요인입니다. 자세한 내용은 분석가에게 전화를 요청하거나 문의 사항을 드롭하세요.

DBMR 연구팀에서 사용하는 주요 연구 방법론은 데이터 마이닝, 시장에 대한 데이터 변수의 영향 분석 및 주요(산업 전문가) 검증을 포함하는 데이터 삼각 측량입니다. 데이터 모델에는 공급업체 포지셔닝 그리드, 시장 타임라인 분석, 시장 개요 및 가이드, 회사 포지셔닝 그리드, 특허 분석, 가격 분석, 회사 시장 점유율 분석, 측정 기준, 글로벌 대 지역 및 공급업체 점유율 분석이 포함됩니다. 연구 방법론에 대해 자세히 알아보려면 문의를 통해 업계 전문가에게 문의하세요.

사용자 정의 가능

Data Bridge Market Research는 고급 형성 연구 분야의 선두 주자입니다. 저희는 기존 및 신규 고객에게 목표에 맞는 데이터와 분석을 제공하는 데 자부심을 느낍니다. 보고서는 추가 국가에 대한 시장 이해(국가 목록 요청), 임상 시험 결과 데이터, 문헌 검토, 재생 시장 및 제품 기반 분석을 포함하도록 사용자 정의할 수 있습니다. 기술 기반 분석에서 시장 포트폴리오 전략에 이르기까지 타겟 경쟁업체의 시장 분석을 분석할 수 있습니다. 귀하가 원하는 형식과 데이터 스타일로 필요한 만큼 많은 경쟁자를 추가할 수 있습니다. 저희 분석가 팀은 또한 원시 엑셀 파일 피벗 테이블(팩트북)로 데이터를 제공하거나 보고서에서 사용 가능한 데이터 세트에서 프레젠테이션을 만드는 데 도움을 줄 수 있습니다.