Global Covid 19 Infection Market

Market Size in USD Billion

USD

30.25 Billion

USD

79.28 Billion

2025

2033

USD

30.25 Billion

USD

79.28 Billion

2025

2033

| 2026 - 2033 | |

| USD 30.25 Billion | |

| USD 79.28 Billion | |

| % | |

|

COVID-19 Infection Market Size

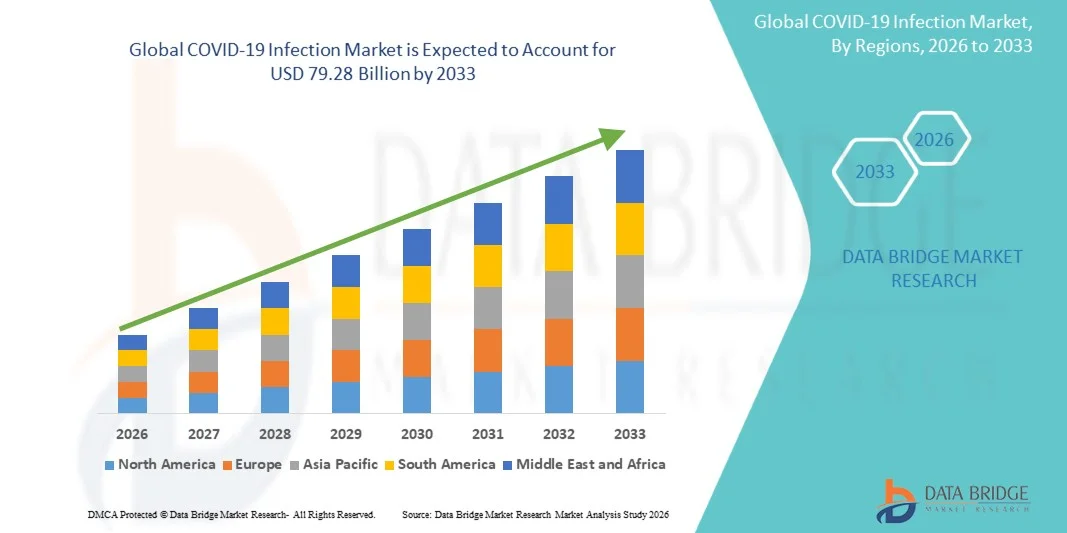

- The global COVID-19 Infection market size was valued at USD 30.25 billion in 2025 and is expected to reach USD 79.28 billion by 2033, at a CAGR of 12.80% during the forecast period

- The market growth is largely fueled by the increasing demand for effective diagnostic tools, therapeutic solutions, and preventive healthcare measures for COVID-19 infection management, leading to greater healthcare digitalization and improved disease monitoring across hospitals, laboratories, and homecare settings

- Furthermore, rising public health awareness, growing demand for rapid and accurate testing, and the continued need for vaccines, antiviral treatments, and infection control solutions are establishing COVID-19 infection management as a critical component of modern healthcare systems. These converging factors are accelerating the uptake of COVID-19 Infection solutions, thereby significantly boosting the industry's growth

COVID-19 Infection Market Analysis

- COVID-19 Infection solutions, including diagnostic tests, vaccines, antiviral therapies, monitoring tools, and infection prevention products, remain vital components of modern healthcare systems across hospitals, laboratories, clinics, and homecare settings due to their critical role in disease detection, treatment, surveillance, and outbreak preparedness

- The escalating demand for COVID-19 Infection solutions is primarily fueled by continued surveillance of emerging variants, growing emphasis on public health preparedness, increasing adoption of rapid diagnostic technologies, and rising demand for booster vaccines, antiviral drugs, and integrated infection management systems

- North America dominated the COVID-19 infection market with the largest revenue share of approximately 39.6% in 2025, characterized by advanced healthcare infrastructure, strong government healthcare spending, widespread testing capacity, and the presence of leading pharmaceutical and diagnostics companies, with the U.S. accounting for substantial demand across diagnostics, therapeutics, and vaccination programs

- Asia-Pacific is expected to be the fastest growing region in the COVID-19 Infection market during the forecast period due to expanding healthcare infrastructure, large population base, increasing government investments in disease surveillance, rising domestic vaccine manufacturing capacity, and growing demand for rapid testing solutions across China, India, Japan, and Southeast Asia

- The swab test segment accounted for the largest market revenue share of 61.2% in 2025, driven by widespread use in PCR and rapid antigen testing worldwide

Report Scope and COVID-19 Infection Market Segmentation

|

Attributes |

COVID-19 Infection Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

COVID-19 Infection Market Trends

“Enhanced Disease Surveillance Through AI Integration and Digital Health Technologies”

- A significant and accelerating trend in the global COVID-19 Infection market is the growing integration of artificial intelligence (AI), digital diagnostics, and remote healthcare technologies to improve disease surveillance, early detection, and patient management. These innovations are enhancing public health response capabilities and healthcare system efficiency

- AI-powered analytics are increasingly being used to predict outbreak patterns, identify high-risk populations, and optimize healthcare resource allocation

- For instance, organizations such as BlueDot and HealthMap utilized AI-based surveillance tools to detect unusual pneumonia clusters and track early COVID-19 spread patterns

- The adoption of rapid molecular diagnostics and at-home testing kits is also transforming infection detection by enabling faster identification of positive cases and reducing dependence on centralized laboratories

- Another major trend is the rising use of telemedicine and remote patient monitoring solutions, allowing infected individuals to receive medical consultation and symptom tracking while isolating at home. For instance, hospitals across the U.S., Europe, and Asia expanded virtual COVID-19 care platforms for monitoring oxygen levels and recovery progress remotely

- In addition, digital vaccination certificates, contact tracing systems, and integrated healthcare databases are improving pandemic management by enabling coordinated responses across governments, hospitals, and public health agencies

- This shift toward intelligent, connected, and preventive healthcare systems is fundamentally reshaping infectious disease management and strengthening preparedness for future outbreaks

COVID-19 Infection Market Dynamics

Driver

“Rising Infection Risk and Continued Demand for Diagnostics, Vaccines, and Therapeutics”

- The continued prevalence of COVID-19 variants, seasonal outbreaks, and recurring infection waves remains a major driver for the COVID-19 Infection market, sustaining demand for diagnostics, vaccines, antiviral therapies, and healthcare services

- Government immunization programs and booster dose campaigns are further supporting market demand globally

- For instance, countries such as the U.S., India, the U.K., and Japan continue targeted booster vaccination programs for elderly and immunocompromised populations

- Increased awareness regarding respiratory health, early testing, and preventive care has also encouraged greater use of home test kits, teleconsultation services, and antiviral medications

- Furthermore, the expansion of healthcare infrastructure, stockpiling of emergency medical supplies, and public-private investments in pandemic preparedness are contributing to market growth

- The growing need for rapid response systems against emerging variants and future coronavirus outbreaks is expected to maintain steady industry demand over the forecast period

Restraint/Challenge

“Declining Emergency Demand and Unequal Global Healthcare Access”

- One of the major challenges restraining the COVID-19 Infection market is the decline in emergency-level demand for testing kits, vaccines, and hospital treatments as infection severity has reduced in many regions

- Unequal healthcare access and lower vaccination coverage in low-income regions continue to limit consistent market penetration

- For instance, several countries in Sub-Saharan Africa and low-income Asian markets experienced slower booster dose uptake due to supply, funding, and logistics constraints

- Public fatigue, vaccine hesitancy, and reduced willingness to undergo routine testing have also negatively impacted recurring demand for COVID-related products and services

- In addition, pricing pressure, excess inventory, and reduced government procurement contracts have created revenue challenges for several diagnostic and vaccine manufacturers

- Overcoming these barriers through equitable healthcare access, improved awareness campaigns, variant-adapted products, and long-term infectious disease preparedness strategies will be essential for sustained market stability

COVID-19 Infection Market Scope

The market is segmented on the basis of type, treatment, diagnosis, dosage forms, route of administration, end-users, and distribution channel.

• By Type

On the basis of type, the COVID-19 Infection market is segmented into Omicron, Delta, Gamma, Beta, and Alpha. The Omicron segment dominated the largest market revenue share of 44.6% in 2025, driven by its exceptionally high transmissibility and continued presence across global regions through multiple subvariant waves. Omicron remained the most widely reported strain in several countries, resulting in sustained demand for testing kits, vaccines, antiviral medications, and healthcare services. Public health agencies continued variant surveillance programs focused heavily on Omicron due to its rapid mutation cycle. The segment also benefited from increasing booster vaccination campaigns designed to address Omicron-related immunity gaps. Hospitals and clinics continued to manage recurring seasonal spikes linked to Omicron infections. Demand for home diagnostics and telehealth consultations also increased during outbreak periods. Pharmaceutical companies invested in updated vaccines and targeted treatment solutions for Omicron-related infections. High reinfection rates further supported the commercial importance of this segment. Emerging economies also reported strong Omicron case volumes, expanding market demand. Continuous monitoring and healthcare readiness programs helped preserve segment leadership. These factors collectively sustained Omicron’s dominance in 2025.

The Delta segment is anticipated to witness the fastest growth rate of 8.7% from 2026 to 2033, fueled by increasing retrospective clinical studies and renewed preparedness planning against severe variants. Delta remains clinically significant because of its stronger association with hospitalization and respiratory complications. Governments and healthcare agencies continue monitoring Delta-like mutations through genomic surveillance networks. Growing demand for stockpiling antivirals and emergency treatment solutions supports future growth. Pharmaceutical companies are studying cross-variant therapies effective against Delta lineage strains. Researchers are also evaluating long-term immunity responses among previously infected patients. Demand for booster formulations offering broad-spectrum protection is contributing to the segment outlook. Several countries are strengthening outbreak preparedness strategies based on Delta-era healthcare learnings. Increased hospital readiness investments are indirectly supporting the segment. Academic collaborations on mutation forecasting also add momentum. Continued global surveillance programs are expected to maintain relevance. These factors position Delta as the fastest-growing type segment.

• By Treatment

On the basis of treatment, the COVID-19 Infection market is segmented into medication, vaccine, and others. The vaccine segment held the largest market revenue share of 58.3% in 2025, driven by continued immunization campaigns, booster dose programs, and strong public health procurement initiatives worldwide. Vaccines remained the most effective large-scale preventive tool for reducing severe disease, hospitalization, and mortality. Governments across developed and emerging economies continued purchasing updated vaccines for annual deployment. Technological advances in mRNA, recombinant protein, and viral vector platforms improved protection against new variants. Pediatric vaccination programs also expanded the addressable patient base. High-risk populations including elderly and immunocompromised groups contributed recurring demand for boosters. Public awareness regarding preventive healthcare further supported uptake. International partnerships helped scale manufacturing and improve vaccine availability. Institutional mandates in travel, healthcare, and workplaces added demand in select markets. Cold-chain infrastructure expansion improved accessibility in rural regions. Strong regulatory backing sustained confidence in vaccines. These factors collectively ensured segment dominance.

The medication segment is expected to witness the fastest CAGR of 9.1% from 2026 to 2033, driven by rising demand for antiviral drugs and symptom-management therapies. Oral antiviral medications are increasingly preferred due to convenience and faster early-stage treatment initiation. Growing use of combination therapies for high-risk patients is boosting prescription volumes. Hospitals are expanding inventories of emergency COVID therapeutics for contingency planning. Research into next-generation antivirals with broad variant efficacy is accelerating. Homecare treatment protocols are also increasing reliance on prescribed medications. Improved reimbursement policies in some countries support patient access. Telemedicine growth is enabling faster diagnosis-to-treatment conversion rates. Pharmaceutical companies continue launching upgraded formulations and dosage options. Long COVID symptom management is creating additional medication demand. Outpatient care expansion is another key growth factor. These drivers make medication the fastest-growing treatment segment.

• By Diagnosis

On the basis of diagnosis, the COVID-19 Infection market is segmented into swab test, antibody test, and others. The swab test segment accounted for the largest market revenue share of 61.2% in 2025, driven by widespread use in PCR and rapid antigen testing worldwide. Swab-based diagnostics remained the preferred method for detecting active infections in hospitals, clinics, airports, workplaces, and community centers. High diagnostic accuracy and broad regulatory acceptance supported continued adoption. Governments retained emergency testing infrastructure for future outbreak readiness. Rapid antigen kits using nasal swabs also saw strong consumer demand. Employers and educational institutions used swab testing for periodic screening programs. Laboratories benefited from established processing workflows and equipment compatibility. Home-use test kits further expanded segment reach. Public awareness of self-testing also supported volumes. Ongoing surveillance programs maintained demand even after pandemic peaks. Affordable rapid kits aided emerging market penetration. These factors secured segment leadership in 2025.

The antibody test segment is projected to register the fastest CAGR of 8.4% from 2026 to 2033, fueled by rising interest in immunity monitoring and serology research. Antibody tests are increasingly used to evaluate vaccine response and prior infection exposure. Governments and research bodies conduct population-level immunity surveys using serological tools. Long COVID studies are also creating demand for immune-response testing. Improved assay sensitivity and faster turnaround times are boosting adoption. Hospitals use antibody tests in selected diagnostic pathways. Academic institutions continue variant immunity comparisons using these tools. Expanding private diagnostic chains support accessibility. Awareness regarding preventive health screening is growing. Multiplex platforms are increasing clinical utility. Cost reductions are improving usage rates. These trends support strong future growth.

• By Dosage Forms

On the basis of dosage forms, the COVID-19 Infection market is segmented into capsule, tablets, injections, and others. The injections segment dominated the largest market revenue share of 47.9% in 2025, driven by massive vaccine administration and hospital-based emergency treatments. Injectable dosage forms were widely used for immunization campaigns, monoclonal antibodies, and severe patient management. They offer rapid bioavailability and reliable dosing accuracy. Hospitals preferred injections for critical respiratory cases requiring immediate intervention. Government vaccine drives significantly expanded injectable product volumes. Established cold-chain systems supported distribution efficiency. Healthcare professionals generally trust injectable formats for acute care delivery. Booster campaigns also added recurring demand. Clinical guidelines in many regions favored parenteral therapies for hospitalized patients. Innovation in prefilled syringes improved convenience. Public procurement contracts strengthened revenues. These factors sustained segment dominance.

The tablets segment is expected to witness the fastest CAGR of 9.3% from 2026 to 2033, fueled by growing demand for convenient oral antiviral treatment. Tablets are easy to store, transport, and administer in homecare settings. Patients prefer tablet-based therapies over injections for mild-to-moderate infections. Telemedicine prescriptions are accelerating tablet adoption. Pharmaceutical companies are developing improved antiviral combinations in tablet form. Lower administration costs benefit healthcare systems. Retail and online pharmacies improve access to tablet therapies. Better adherence rates support treatment outcomes. Emerging markets favor affordable oral options. Outpatient treatment pathways continue expanding. Innovation in sustained-release formulations may add growth. These factors drive the segment forward.

• By Route of Administration

On the basis of route of administration, the COVID-19 Infection market is segmented into oral, parenteral, and others. The parenteral segment held the largest market revenue share of 55.1% in 2025, driven by the extensive use of vaccines and injectable therapeutics. Parenteral administration provides rapid onset and accurate systemic delivery. Hospitals relied heavily on intravenous and intramuscular options for acute cases. Vaccination campaigns significantly elevated demand volumes. Clinical settings prefer parenteral routes for severe patients. Strong healthcare infrastructure supported mass administration programs. High trust among physicians sustained adoption. Emergency care protocols further strengthened segment share. Monoclonal antibody therapies also contributed. Public sector procurement supported revenues. Cold-chain expansion improved reach. These factors maintained leadership.

The oral segment is expected to witness the fastest CAGR of 10.2% from 2026 to 2033, driven by increasing demand for home-based treatment solutions. Oral therapies provide convenience and eliminate the need for trained administration staff. Patients prefer oral drugs during isolation and outpatient recovery. Growing telehealth consultations are increasing prescriptions. Pharmaceutical innovation in antiviral tablets supports growth. Lower treatment costs favor oral routes. Retail availability is improving across regions. Elderly patients benefit from easier dosing formats. Mild-to-moderate case management is shifting toward oral care. Government preparedness stockpiles include oral antivirals. Compliance rates are generally higher. These factors accelerate future expansion.

• By End-Users

On the basis of end-users, the COVID-19 Infection market is segmented into hospitals, specialty clinics, homecare, and others. The hospitals segment accounted for the largest market revenue share of 49.5% in 2025, driven by high patient inflow, emergency treatment, ICU admissions, and diagnostic capacity. Hospitals remained primary centers for managing moderate-to-severe COVID cases. They offered oxygen support, ventilation, and specialist care. Vaccination and testing programs also operated through hospitals in many countries. Strong procurement budgets enabled consistent product demand. Presence of multidisciplinary teams improved treatment outcomes. Public trust in hospitals supported patient preference. Government funding strengthened infrastructure expansion. Hospitals also served as surveillance and reporting hubs. Availability of advanced diagnostics increased dependence. Referral networks sustained volumes. These factors ensured segment dominance.

The homecare segment is anticipated to witness the fastest CAGR of 11.1% from 2026 to 2033, fueled by rising preference for treatment at home for mild cases. Patients increasingly use pulse oximeters, teleconsultations, and delivered medicines. Home isolation protocols normalized remote care models globally. Lower hospitalization costs attract both patients and payers. Aging populations also prefer home-based recovery. Digital monitoring apps are improving safety. Online pharmacies support medicine accessibility. Governments encourage hospital capacity optimization through homecare pathways. Family support systems aid recovery compliance. Demand for portable medical devices is rising. Telehealth platforms continue expanding rapidly. These factors support strong growth prospects.

• By Distribution Channel

On the basis of distribution channel, the COVID-19 Infection market is segmented into hospital pharmacy, retail pharmacy, online pharmacy, and others. The hospital pharmacy segment dominated the largest market revenue share of 46.2% in 2025, driven by centralized procurement of vaccines, injectables, antivirals, and emergency supplies. Hospitals required immediate medicine availability for admitted patients and emergency cases. Institutional purchasing contracts supported stable revenue generation. Controlled storage conditions favored hospital pharmacies for sensitive products. Pharmacists coordinated inpatient treatment protocols efficiently. Vaccination drives in medical centers also added demand. Integration with hospital records improved dispensing accuracy. Public hospitals represented large-volume buyers. Critical care dependency sustained medicine turnover. Trust in certified supply chains supported usage. Strong reimbursement systems aided growth. These factors maintained dominance.

The online pharmacy segment is expected to witness the fastest CAGR of 12.4% from 2026 to 2033, fueled by growing digital healthcare adoption and contactless medicine purchasing. Consumers increasingly prefer doorstep delivery for convenience and safety. Online platforms enable easy prescription uploads and refill reminders. Price comparison features attract cost-conscious buyers. Smartphone penetration is expanding customer reach globally. Telemedicine integration is accelerating order volumes. Rural patients gain improved medicine access through e-pharmacies. Promotional discounts support customer acquisition. Subscription models are increasing repeat purchases. Regulatory frameworks are gradually improving market confidence. Logistics networks continue advancing rapidly. These drivers make online pharmacy the fastest-growing channel.

COVID-19 Infection Market Regional Analysis

- North America dominated the COVID-19 infection market with the largest revenue share of approximately 39.6% in 2025, driven by advanced healthcare infrastructure, strong government healthcare spending, and widespread testing capacity across the region. The presence of leading pharmaceutical, biotechnology, and diagnostics companies has significantly supported market expansion. High demand for diagnostic kits, antiviral therapeutics, vaccines, and hospital care solutions continues to strengthen regional dominance

- Public health agencies across the region maintain robust surveillance and response systems for outbreak management. Increasing investments in next-generation vaccines and booster programs further support market growth. Strong reimbursement systems and healthcare accessibility have improved treatment uptake

- Rising awareness regarding early testing and preventive care also contributes to demand. The region benefits from continuous innovation in diagnostics and treatment technologies. Ongoing preparedness strategies for future outbreaks are expected to sustain North America’s leading market position

U.S. COVID-19 Infection Market Insight

The U.S. COVID-19 infection market captured the largest revenue share in 2025 within North America, fueled by substantial demand across diagnostics, therapeutics, and vaccination programs. The country has a highly developed healthcare system with extensive laboratory and hospital infrastructure supporting large-scale testing and treatment. Strong government funding for public health preparedness and emergency response continues to boost the market. Presence of major pharmaceutical and biotech companies supports rapid innovation in vaccines and antiviral drugs. Increasing adoption of at-home testing kits has expanded consumer access to diagnostics. High booster vaccination coverage and ongoing immunization campaigns also support demand. Rising focus on long-COVID management and post-infection care is creating new growth opportunities. Continued investments in surveillance systems and variant monitoring are strengthening market resilience. The U.S. remains the primary revenue contributor within the regional market.

Europe COVID-19 Infection Market Insight

The Europe COVID-19 infection market is projected to expand at a substantial CAGR throughout the forecast period, driven by strong public healthcare systems, widespread vaccination programs, and coordinated disease surveillance measures. Countries across the region continue to invest in pandemic preparedness and emergency stockpiles of diagnostics and therapeutics. Rising demand for rapid antigen and molecular testing solutions supports market growth. Government-backed healthcare reimbursement systems improve accessibility to treatment and preventive care. The region has strong pharmaceutical manufacturing capabilities that enhance vaccine and medicine availability. Increasing focus on managing long-term respiratory complications after infection is also driving healthcare demand. Expansion of digital health monitoring systems supports efficient patient management. Collaborative research programs across the European Union continue to accelerate innovation. Ongoing modernization of healthcare infrastructure further strengthens the regional market outlook.

U.K. COVID-19 Infection Market Insight

The U.K. COVID-19 infection market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by strong NHS-backed healthcare services and ongoing investment in disease monitoring systems. The country maintains high vaccination awareness and extensive public health outreach programs. Rising demand for home-based testing kits and digital consultation services is supporting growth. Government funding for booster doses and variant surveillance remains a key driver. Increasing focus on long-COVID treatment pathways is creating sustained healthcare demand. The presence of advanced biotech and pharmaceutical companies supports therapeutic innovation. Strong research collaborations between universities and healthcare institutions further accelerate development. Expansion of telehealth and remote care models is improving patient access. Continued preparedness measures are expected to support future market expansion.

Germany COVID-19 Infection Market Insight

The Germany COVID-19 infection market is expected to expand at a considerable CAGR during the forecast period, fueled by robust healthcare infrastructure and strong investments in diagnostics and treatment capacity. Germany has one of Europe’s most advanced hospital systems, supporting effective patient care and disease management. Rising demand for laboratory-based molecular testing and rapid diagnostics supports market growth. Strong domestic pharmaceutical manufacturing capabilities improve vaccine and medicine supply chains. Government emphasis on preventive healthcare and outbreak preparedness further boosts demand. Increasing adoption of digital health records and monitoring platforms is improving response efficiency. Growing focus on elderly and vulnerable population protection supports continued healthcare spending. Research institutions in Germany remain active in virology and vaccine innovation. These factors collectively support sustained market expansion.

Asia-Pacific COVID-19 Infection Market Insight

The Asia-Pacific COVID-19 infection market is poised to grow at the fastest CAGR of 24% during the forecast period of 2026 to 2033, driven by expanding healthcare infrastructure and a large population base. Increasing government investments in disease surveillance systems and emergency preparedness programs are accelerating regional growth. Rising domestic vaccine manufacturing capacity across China, India, Japan, and Southeast Asia is improving supply security. Growing demand for rapid testing solutions and affordable therapeutics is further boosting the market. Expanding public awareness regarding infectious disease prevention supports adoption of diagnostic services. Rapid urbanization and dense populations are increasing focus on healthcare readiness. International partnerships for vaccine research and distribution also strengthen growth prospects. Rising healthcare digitization and mobile diagnostics improve accessibility. Asia-Pacific is expected to remain the fastest-growing regional market over the forecast period.

Japan COVID-19 Infection Market Insight

The Japan COVID-19 infection market is gaining momentum due to the country’s advanced healthcare system, aging population, and strong public health preparedness measures. Japan places high emphasis on infection prevention, early diagnosis, and efficient treatment pathways. Rising demand for booster vaccinations and antiviral medications is supporting growth. Strong adoption of rapid diagnostic technologies and hospital monitoring systems improves patient outcomes. Government support for healthcare modernization continues to enhance market opportunities. Increasing focus on protecting elderly citizens and high-risk populations drives sustained demand. Domestic pharmaceutical innovation and vaccine research further strengthen the market. Growing use of telemedicine and remote monitoring platforms supports healthcare accessibility. Japan’s long-term preparedness strategies are expected to sustain growth.

China COVID-19 Infection Market Insight

The China COVID-19 infection market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country’s vast population base, expanding healthcare investments, and strong domestic vaccine manufacturing capacity. China has significantly increased disease surveillance infrastructure and laboratory testing capabilities in recent years. High production of vaccines, rapid tests, and protective healthcare products supports both domestic and export demand. Government-backed healthcare reforms and public health campaigns continue to strengthen the market. Increasing urban healthcare modernization and digital monitoring systems support disease management efficiency. Rising pharmaceutical innovation and biotech expansion are also driving growth. Strong manufacturing ecosystems improve affordability and accessibility of healthcare products. Continued focus on preparedness and infection control is expected to maintain China’s regional leadership.

COVID-19 Infection Market Share

The COVID-19 Infection industry is primarily led by well-established companies, including:

- Pfizer Inc. (U.S.)

- Moderna, Inc. (U.S.)

- Johnson & Johnson (U.S.)

- Merck & Co., Inc. (U.S.)

- Gilead Sciences, Inc. (U.S.)

- Abbott (U.S.)

- F. Hoffmann-La Roche Ltd. (Switzerland)

- Thermo Fisher Scientific Inc. (U.S.)

- Siemens Healthineers AG (Germany)

- AstraZeneca plc (U.K.)

- Novavax, Inc. (U.S.)

- Sanofi S.A. (France)

- GlaxoSmithKline plc (U.K.)

- Bharat Biotech (India)

- Serum Institute of India Pvt. Ltd. (India)

- Sinovac Biotech Ltd. (China)

- Sinopharm Group Co., Ltd. (China)

- BioNTech SE (Germany)

- Qiagen N.V. (Netherlands)

- Danaher Corporation (U.S.)

Latest Developments in Global COVID-19 Infection Market

- In November 2021, UK Medicines and Healthcare products Regulatory Agency (MHRA) granted the world’s first authorization for Molnupiravir for treatment of mild-to-moderate COVID-19 in adults with risk factors for severe illness. The approval marked a major milestone as one of the first oral antiviral therapies for COVID-19 infection

- In December 2021, U.S. Food and Drug Administration issued Emergency Use Authorization for Lagevrio (molnupiravir) for certain high-risk adults with mild-to-moderate COVID-19. The authorization expanded at-home treatment options and strengthened the commercial COVID-19 therapeutics market

- In December 2021, U.S. Food and Drug Administration also authorized Paxlovid for emergency use, providing a second major oral antiviral option for early COVID-19 infection treatment. The launch accelerated competition in the outpatient COVID therapeutics segment and significantly changed treatment protocols worldwide

- In April 2022, World Health Organization recommended broader use of oral antivirals for high-risk COVID-19 patients, including nirmatrelvir/ritonavir therapies, following evidence of reduced hospitalization risk. This recommendation boosted global adoption of antiviral therapies in both developed and emerging markets

- In May 2023, World Health Organization declared that COVID-19 no longer constituted a Public Health Emergency of International Concern. Although emergency status ended, the decision shifted the market toward long-term endemic management, seasonal vaccination programs, and continued demand for antiviral infection treatments

- In September 2023, U.S. Food and Drug Administration approved updated 2023–2024 COVID-19 vaccines from Pfizer, Moderna, and Novavax targeting newer circulating variants. The approvals reinforced the transition of the COVID-19 infection market toward annual booster commercialization

- In August 2024, U.S. Food and Drug Administration approved updated 2024–2025 COVID-19 vaccines targeting currently circulating variants, supporting seasonal immunization campaigns. This development demonstrated continued commercial demand for variant-adapted vaccines despite lower emergency-era volumes

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.