Global Satellite Antenna Market

Market Size in USD Billion

USD

7.03 Billion

USD

13.25 Billion

2025

2033

USD

7.03 Billion

USD

13.25 Billion

2025

2033

| 2026 - 2033 | |

| USD 7.03 Billion | |

| USD 13.25 Billion | |

| % | |

|

Satellite Antenna Market Overview

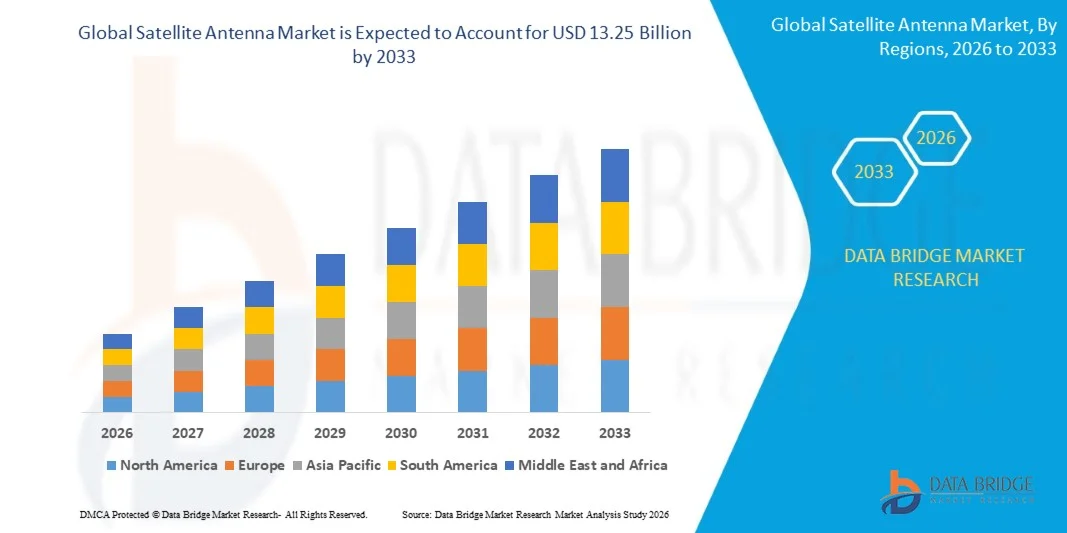

The Satellite Antenna Market was valued at USD 7.03 billion in 2025 and is projected to reach USD 13.25 billion by 2033, growing at a CAGR of 8.25% from 2026 to 2033. The market is experiencing strong growth driven by rising deployment of satellite communication infrastructure, increasing demand for high-speed broadband connectivity, and expanding applications across defense, maritime, aviation, broadcasting, and remote communication sectors. Rapid advancements in low Earth orbit (LEO) satellite constellations, phased-array antenna technologies, and high-throughput satellite systems are further accelerating adoption of advanced satellite antenna solutions globally.

The growing need for reliable communication networks in remote and underserved regions, combined with rising investments in space exploration, military surveillance, and connected mobility solutions, is compelling governments, telecom operators, and aerospace companies to adopt next-generation satellite antenna systems. Electronically steerable antennas, flat-panel antennas, and high-frequency satellite communication terminals are increasingly replacing conventional parabolic systems in many applications, offering improved mobility, faster signal acquisition, lower latency, and enhanced operational flexibility for broadband communication, in-flight connectivity, maritime communication, and defense intelligence operations.

Key Market Trends & Insights

- North America dominated the satellite antenna market with the largest revenue share of approximately 36.4% in 2025, supported by strong presence of major satellite communication providers, increasing military and aerospace investments, and rapid adoption of advanced phased-array and electronically steered antenna technologies across commercial and defense sectors.

- Asia-Pacific is expected to be the fastest-growing region, recording a CAGR of 9.8% from 2026 to 2033. Growth is driven by expanding satellite broadband initiatives, rising space research activities in China, India, Japan, and South Korea, and increasing demand for maritime, aviation, and rural connectivity solutions across emerging economies.

- The Parabolic Reflector Antenna segment held the largest market revenue share of approximately 41.7% in 2025 driven by its widespread deployment across satellite broadcasting, defense communication, maritime connectivity, and teleport infrastructure applications. These antennas are preferred due to their high signal gain, long-distance transmission capability, and strong reliability across high-frequency communication environments.

- The Flat Panel Antenna segment is projected to register the fastest growth at a CAGR of 11.6% from 2026 to 2033, driven by increasing deployment across low Earth orbit satellite communication systems, connected mobility platforms, and in-flight broadband services. Rising adoption of electronically steerable antennas in commercial aviation, autonomous vehicles, and maritime broadband connectivity is accelerating segment growth globally.

- The Reflectors segment accounted for the largest market revenue share of nearly 34.8% in 2025 supported by increasing demand for high-performance satellite signal reception and transmission systems across broadcasting, military, and enterprise communication infrastructure. Reflector systems remain critical for maintaining signal precision, transmission strength, and operational efficiency in high-frequency satellite communication applications.

- The Low Noise Block (LNB) Converters segment is expected to witness strong growth during the forecast period due to rising adoption of high-frequency satellite broadband systems and direct-to-home television services. Increasing demand for low-noise signal amplification and enhanced reception quality in residential and commercial communication systems is contributing to rising segment expansion.

- The SOTM segment accounted for the largest market revenue share of approximately 58.9% in 2025 driven by increasing deployment of satellite communication systems on moving platforms such as naval vessels, military vehicles, trains, and aircraft. These technologies support uninterrupted communication, real-time navigation, and secure broadband connectivity during high-mobility operations.

- The SOTP segment is projected to register notable growth from 2026 to 2033 due to increasing investments in fixed satellite communication infrastructure for enterprise networking, disaster recovery communication, and remote industrial monitoring operations. Rising deployment of ground stations and fixed communication terminals across emerging economies is further supporting market expansion.

- The Land segment held the largest market revenue share of approximately 39.6% in 2025 supported by expanding deployment of satellite communication infrastructure across military bases, telecom networks, enterprise communication systems, and remote industrial operations. Governments and telecom providers are increasingly investing in land-based satellite terminals to improve broadband access and emergency communication capabilities.

- The Airborne segment is anticipated to witness the fastest growth at a CAGR of 10.9% from 2026 to 2033 driven by rising demand for in-flight connectivity, defense surveillance systems, and satellite-enabled aviation communication technologies. Increasing commercial airline investments in passenger broadband services and real-time aircraft communication systems are accelerating segment growth.

- The K/Ku/Ka Band segment dominated the market with the largest revenue share of approximately 44.2% in 2025 due to increasing utilization in high-speed broadband communication, direct broadcast services, and advanced military communication systems. These bands support high-capacity data transmission and low-latency communication required for next-generation satellite broadband networks.

- The X Band segment is expected to witness significant growth during the forecast period driven by increasing deployment across military radar, defense intelligence, and secure government communication applications. Rising geopolitical tensions and increasing investments in secure satellite communication infrastructure are contributing to higher adoption of X Band communication systems globally.

- The Land segment accounted for the largest market revenue share of approximately 37.4% in 2025 driven by increasing use of satellite antennas across enterprise broadband services, rural connectivity infrastructure, military communication networks, and disaster recovery systems. Expanding deployment of satellite-enabled communication services in remote and underserved areas continues to support segment dominance.

- The Maritime segment is projected to witness strong growth from 2026 to 2033 due to increasing demand for uninterrupted ship-to-shore communication, vessel monitoring systems, and onboard broadband connectivity solutions. Commercial shipping operators and naval defense organizations are increasingly integrating satellite antenna systems to improve navigation safety, fleet management, and operational communication efficiency across global maritime routes.

Market Size & Forecast

- Global Market Value (2025): USD 7.03 Billion

- Expected Market Value (2033): USD 13.25 Billion

- Forecast CAGR (2026–2033): 8.25%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Satellite Antenna Market Segmentation

|

Attributes |

Satellite Antenna Key Market Insights |

|

Segments Covered |

· By Antenna Type: Parabolic Reflector Antenna, Flat Panel Antenna, Fiberglass Reinforced Plastic Antenna, Horn Antenna, Iron Antenna with Mold Stamping, and Others · By Component: Reflectors, Feed Horns, Feed Networks, Low Noise Block (LNB) Converters, and Others · By Technology: SOTM and SOTP · By Platform: Land, Space, Maritime, and Airborne · By Frequency Band: K/Ku/Ka Band, L & S Band, C Band, X Band, VHF & UHF Band, and Others · By Application: Space, Land, Maritime, and Airborne |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Airbus S.A.S. (France) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Satellite Antenna Market Trends

Trend: Increasing Deployment Of Low Earth Orbit Satellite Constellations And Flat-Panel Antenna Technologies

Rapid expansion of satellite broadband services, connected mobility applications, and global communication infrastructure is increasing demand for advanced satellite antenna systems across telecommunications, aviation, maritime, and defense sectors. Conventional satellite communication systems often face limitations related to signal latency, mechanical steering complexity, and restricted mobility, encouraging operators to adopt electronically steerable and flat-panel antenna technologies capable of supporting high-speed, low-latency communication networks.

In modern aviation and maritime operations, companies are increasingly integrating flat-panel satellite antennas, For instance for in-flight connectivity and vessel communication systems, to improve broadband reliability, coverage, and operational efficiency while reducing maintenance complexity. In defense and emergency communication systems, advanced phased-array antennas are being deployed to support secure, real-time communication and surveillance operations in remote and high-risk environments.

The rapid deployment of low Earth orbit (LEO) satellite constellations by companies such as SpaceX Starlink, OneWeb, and Amazon Kuiper is also accelerating demand for compact, electronically steerable antennas capable of maintaining continuous satellite connectivity. In addition, satellite antenna technologies continue to gain importance in autonomous transportation, remote industrial monitoring, and disaster management systems because of their ability to provide uninterrupted connectivity in infrastructure-limited regions. Growing industry validation through commercial aviation trials conducted during 2025 integrating next-generation flat-panel antennas demonstrated broadband speed improvements of nearly 20–30% with reduced signal interruption during high-mobility operations

Satellite Antenna Market Dynamics

Key Market Driver: Rising Demand For High-Speed Global Connectivity And Satellite Broadband Services

Governments, telecom operators, and enterprises worldwide are increasingly investing in satellite communication infrastructure to address rising demand for high-speed internet connectivity, remote communication services, and resilient communication networks. Expanding digital transformation initiatives, combined with growing internet penetration in rural and underserved regions, are creating strong demand for advanced satellite antenna systems capable of supporting broadband communication across geographically challenging environments.

Industries such as aviation, maritime, defense, and telecommunications are increasingly deploying satellite antennas to enable continuous communication, real-time navigation, and secure data transmission across mobile and remote operations. Telecom providers are actively expanding satellite broadband services, For instance through LEO and medium Earth orbit satellite deployments, to support increasing demand for low-latency communication and enterprise connectivity solutions.

Similarly, government agencies and military organizations are investing heavily in satellite communication systems to strengthen disaster recovery capabilities, border surveillance, and secure defense communication networks. Real-world satellite broadband deployments across North America and Europe during 2024 integrating phased-array satellite antennas demonstrated network latency reductions of approximately 35–40% compared to conventional geostationary satellite communication systems

Key Restraint/Challenge: High Deployment Costs And Signal Interference Limitations

Advanced satellite antenna systems require significant investment in hardware, installation infrastructure, and network integration technologies, creating affordability challenges for small enterprises and developing regions. Complex manufacturing requirements associated with phased-array antennas, electronically steerable systems, and high-frequency communication modules further increase production costs and limit large-scale deployment across cost-sensitive markets.

In addition, signal attenuation caused by extreme weather conditions, physical obstructions, and electromagnetic interference continues to affect communication reliability in certain operational environments. Regulatory restrictions related to frequency spectrum allocation and satellite communication licensing also create deployment challenges for international satellite operators and communication providers.

Commercial performance benchmarking studies indicate that electronically steerable flat-panel satellite antennas, For instance advanced phased-array systems used in mobility applications, can increase deployment costs by nearly 25–40% compared to conventional mechanically steered antenna systems, limiting adoption in price-sensitive commercial sectors

Key Market Opportunity: Expansion Of Connected Mobility And Defense Communication Infrastructure

Modern aircraft, connected vehicles, naval fleets, and autonomous industrial systems increasingly require uninterrupted, high-speed communication capabilities capable of supporting real-time navigation, monitoring, and data-intensive applications. Conventional terrestrial communication infrastructure often lacks coverage in remote environments, creating strong demand for advanced satellite antenna systems capable of delivering reliable connectivity across land, air, and sea operations.

Aerospace and mobility companies are increasingly integrating satellite antennas, For instance for in-flight entertainment, autonomous navigation, and connected logistics operations, to improve operational efficiency, passenger connectivity, and communication reliability across transportation networks. In defense applications, rising investments in secure battlefield communication, surveillance drones, and satellite-enabled intelligence systems are accelerating adoption of advanced phased-array and electronically steerable antenna technologies.

In addition, advancements in miniaturized antenna architectures, multi-orbit compatibility, and software-defined communication systems are improving antenna performance and deployment flexibility, creating opportunities across smart transportation, remote healthcare, and industrial IoT infrastructure markets in Asia-Pacific and North America. Satellite communication trials conducted during 2025 across commercial aviation networks in the U.S. and Europe reported connectivity stability improvements of around 15–22% after integrating next-generation electronically steerable flat-panel antenna systems into aircraft communication platforms.

Satellite Antenna Market Scope

The market is segmented on the basis of antenna type, component, technology, platform, frequency band, and application.

- By Antenna Type

On the basis of antenna type, the satellite antenna market is segmented into Parabolic Reflector Antenna, Flat Panel Antenna, Fiberglass Reinforced Plastic Antenna, Horn Antenna, Iron Antenna with Mold Stamping, and Others. The Parabolic Reflector Antenna segment held the largest market revenue share of approximately 41.7% in 2025 driven by its widespread deployment across satellite broadcasting, defense communication, maritime connectivity, and teleport infrastructure applications. These antennas are preferred due to their high signal gain, long-distance transmission capability, and strong reliability across high-frequency communication environments.

The Flat Panel Antenna segment is projected to register the fastest growth at a CAGR of 11.6% from 2026 to 2033, driven by increasing deployment across low Earth orbit satellite communication systems, connected mobility platforms, and in-flight broadband services. Rising adoption of electronically steerable antennas in commercial aviation, autonomous vehicles, and maritime broadband connectivity is accelerating segment growth globally.

- By Component

On the basis of component, the satellite antenna market is segmented into Reflectors, Feed Horns, Feed Networks, Low Noise Block (LNB) Converters, and Others. The Reflectors segment accounted for the largest market revenue share of nearly 34.8% in 2025 supported by increasing demand for high-performance satellite signal reception and transmission systems across broadcasting, military, and enterprise communication infrastructure. Reflector systems remain critical for maintaining signal precision, transmission strength, and operational efficiency in high-frequency satellite communication applications.

The Low Noise Block (LNB) Converters segment is expected to witness strong growth during the forecast period due to rising adoption of high-frequency satellite broadband systems and direct-to-home television services. Increasing demand for low-noise signal amplification and enhanced reception quality in residential and commercial communication systems is contributing to rising segment expansion.

- By Technology

On the basis of technology, the satellite antenna market is segmented into SOTM and SOTP. The SOTM segment accounted for the largest market revenue share of approximately 58.9% in 2025 driven by increasing deployment of satellite communication systems on moving platforms such as naval vessels, military vehicles, trains, and aircraft. These technologies support uninterrupted communication, real-time navigation, and secure broadband connectivity during high-mobility operations.

The SOTP segment is projected to register notable growth from 2026 to 2033 due to increasing investments in fixed satellite communication infrastructure for enterprise networking, disaster recovery communication, and remote industrial monitoring operations. Rising deployment of ground stations and fixed communication terminals across emerging economies is further supporting market expansion.

- By Platform

On the basis of platform, the satellite antenna market is segmented into Land, Space, Maritime, and Airborne. The Land segment held the largest market revenue share of approximately 39.6% in 2025 supported by expanding deployment of satellite communication infrastructure across military bases, telecom networks, enterprise communication systems, and remote industrial operations. Governments and telecom providers are increasingly investing in land-based satellite terminals to improve broadband access and emergency communication capabilities.

The Airborne segment is anticipated to witness the fastest growth at a CAGR of 10.9% from 2026 to 2033 driven by rising demand for in-flight connectivity, defense surveillance systems, and satellite-enabled aviation communication technologies. Increasing commercial airline investments in passenger broadband services and real-time aircraft communication systems are accelerating segment growth.

- By Frequency Band

On the basis of frequency band, the satellite antenna market is segmented into K/Ku/Ka Band, L & S Band, C Band, X Band, VHF & UHF Band, and Others. The K/Ku/Ka Band segment dominated the market with the largest revenue share of approximately 44.2% in 2025 due to increasing utilization in high-speed broadband communication, direct broadcast services, and advanced military communication systems. These bands support high-capacity data transmission and low-latency communication required for next-generation satellite broadband networks.

The X Band segment is expected to witness significant growth during the forecast period driven by increasing deployment across military radar, defense intelligence, and secure government communication applications. Rising geopolitical tensions and increasing investments in secure satellite communication infrastructure are contributing to higher adoption of X Band communication systems globally.

- By Application

On the basis of application, the satellite antenna market is segmented into Space, Land, Maritime, and Airborne. The Land segment accounted for the largest market revenue share of approximately 37.4% in 2025 driven by increasing use of satellite antennas across enterprise broadband services, rural connectivity infrastructure, military communication networks, and disaster recovery systems. Expanding deployment of satellite-enabled communication services in remote and underserved areas continues to support segment dominance.

The Maritime segment is projected to witness strong growth from 2026 to 2033 due to increasing demand for uninterrupted ship-to-shore communication, vessel monitoring systems, and onboard broadband connectivity solutions. Commercial shipping operators and naval defense organizations are increasingly integrating satellite antenna systems to improve navigation safety, fleet management, and operational communication efficiency across global maritime routes.

Satellite Antenna Market Regional Analysis

North America Satellite Antenna Market Insight

North America dominated the satellite antenna market with the largest revenue share of 38.6% in 2025, supported by rising investments in satellite communication infrastructure, strong defense modernization programs, and increasing deployment of broadband connectivity services across remote and rural regions. The region benefits from the presence of major aerospace and satellite communication companies, along with growing adoption of low Earth orbit satellite networks for commercial and government applications. Increasing demand for in-flight connectivity, maritime communication, and secure military communication systems is further strengthening market growth across North America.

U.S. Satellite Antenna Market Insight

The U.S. satellite antenna market captured the largest revenue share in 2025 within North America, fueled by rapid expansion of satellite broadband services, increasing defense communication investments, and strong deployment of advanced space technologies. Government agencies and private satellite operators are increasingly investing in phased-array antennas and electronically steerable communication systems to improve connectivity reliability and support next-generation communication infrastructure. Moreover, the growing adoption of satellite-enabled aviation communication systems, autonomous defense technologies, and connected mobility solutions is significantly contributing to market expansion.

Europe Satellite Antenna Market Insight

The Europe satellite antenna market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by increasing investments in space communication programs, rising defense modernization initiatives, and expanding demand for secure broadband connectivity across commercial and government sectors. The region is witnessing growing deployment of satellite communication systems across aviation, maritime, and industrial operations. European countries are also emphasizing technological innovation and cross-border satellite communication infrastructure development, supporting strong demand for advanced antenna systems across multiple industries.

U.K. Satellite Antenna Market Insight

The U.K. satellite antenna market is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing investments in satellite communication infrastructure, rising defense surveillance activities, and growing adoption of connected aviation and maritime technologies. The country’s strong aerospace ecosystem, combined with expanding satellite broadband deployment and increasing demand for secure communication systems, is accelerating adoption of advanced satellite antenna technologies. Furthermore, the growing integration of low Earth orbit satellite services into commercial communication networks is expected to further support market expansion.

Germany Satellite Antenna Market Insight

The Germany satellite antenna market is expected to witness the fastest growth rate from 2026 to 2033, fueled by increasing adoption of advanced industrial communication technologies, strong investments in aerospace innovation, and rising deployment of satellite-enabled connectivity systems across transportation and defense sectors. Germany’s emphasis on technological advancement, manufacturing efficiency, and smart infrastructure development is promoting the integration of satellite communication systems across commercial and industrial operations. The increasing use of phased-array antennas and satellite broadband systems in automotive testing and industrial IoT infrastructure is further contributing to market growth.

Asia-Pacific Satellite Antenna Market Insight

The Asia-Pacific satellite antenna market is expected to witness the fastest growth rate from 2026 to 2033, supported by rapid urbanization, expanding digital connectivity initiatives, and increasing investments in satellite communication infrastructure across China, India, Japan, and South Korea. Governments across the region are actively investing in space programs, rural broadband expansion, and defense communication modernization to improve connectivity and national communication capabilities. Furthermore, the growing presence of regional satellite manufacturers and increasing deployment of connected transportation infrastructure are supporting strong market expansion across Asia-Pacific.

Japan Satellite Antenna Market Insight

The Japan satellite antenna market is expected to witness the fastest growth rate from 2026 to 2033 due to the country’s advanced aerospace sector, strong focus on disaster communication preparedness, and increasing investments in satellite-enabled transportation systems. Japan is actively deploying advanced satellite communication technologies across aviation, maritime, and emergency response infrastructure to improve operational efficiency and communication reliability. In addition, rising demand for connected mobility solutions, smart city infrastructure, and secure communication technologies is accelerating the adoption of advanced satellite antenna systems throughout the country.

China Satellite Antenna Market Insight

The China satellite antenna market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to rapid expansion of satellite broadband infrastructure, strong government investments in national space programs, and increasing deployment of connected communication systems across commercial and defense sectors. China continues to strengthen its satellite manufacturing capabilities and low Earth orbit satellite deployment activities to improve broadband coverage and technological independence. The growing adoption of satellite communication systems across smart transportation, industrial automation, and rural connectivity initiatives is significantly contributing to market growth in China.

Satellite Antenna Market Share

The Satellite Antenna industry is primarily led by well-established companies, including:

• Airbus S.A.S. (Netherlands)

• Honeywell International Inc. (U.S.)

• General Dynamics Mission Systems, Inc. (U.S.)

• Cobham Limited (U.K.)

• Harris Corporation (U.S.)

• Mitsubishi Electric Corporation (Japan)

• Maxar Technologies Ltd. (U.S.)

• GILAT SATELLITE NETWORKS. (Israel)

• Elite Antennas Ltd. (U.K.)

• Xi'an Space Star Technology (Group) Co., Ltd (China)

• Viasat, Inc. (U.S.)

• Norsat International Inc. (Canada)

• Kymeta Corporation (U.S.)

• Digisat International Inc. (U.S.)

• SVH Tech Pvt. Ltd. (India)

• TICRA (Denmark)

Latest Developments in Satellite Antenna Market

- In July 2024, Cobham SATCOM, product launch, unveiled its next-generation Sea Tel TVRO antenna system for maritime applications to improve onboard satellite connectivity and communication reliability for commercial and defense vessels. The advanced antenna integrates enhanced tracking and signal optimization technologies to ensure uninterrupted connectivity in challenging marine environments. This launch is expected to strengthen maritime communication infrastructure and support growing demand for high-bandwidth satellite services across global shipping and naval operations.

- In May 2024, Airbus, product development, delivered the first active antenna for the SpainSat NG I satellite program aimed at enhancing secure communication capabilities for Spanish defense and security agencies. The active antenna system is designed to support advanced military-grade connectivity with improved transmission efficiency and secure communication performance. This development reinforces Airbus’s position in the defense satellite communication sector while accelerating modernization of secure satellite infrastructure across Europe.

- In March 2024, Hanwha Phasor, product launch, announced the release of its Phasor L3300B Active Electronically Steered Antenna (AESA) developed for commercial and military land-based communication applications. The antenna enables uninterrupted satellite connectivity with dual simultaneous receive channels, supporting seamless satellite handovers without signal loss. This innovation is expected to increase adoption of electronically steered antennas across defense, mobility, and next-generation communication markets.

- In February 2024, L3Harris Technologies, Inc., technology demonstration, showcased its digital phased array antenna system designed to improve high-speed satellite communication efficiency and network flexibility. The system demonstrated advanced beamforming and high-capacity data transmission capabilities during live testing at the company’s Florida facility. This advancement is expected to accelerate deployment of next-generation satellite communication systems for defense, aerospace, and commercial broadband applications.

- In October 2023, Kymeta, product launch, introduced the Osprey u8 HGL hybrid GEO/LEO terminal for military mobility applications to provide secure and uninterrupted connectivity across land and maritime defense platforms. The terminal utilizes multi-orbit satellite integration to enhance communication resilience and operational flexibility for military missions. This launch strengthens hybrid satellite communication adoption and supports increasing demand for advanced mobile defense connectivity solutions.

- In June 2023, Kymeta and OneWeb, commercial launch partnership, introduced the Peregrine u8 LEO terminal featuring electronically steered flat-panel antenna technology for maritime satellite communication services. The solution enables high-speed low-earth-orbit connectivity for vessels operating across global maritime routes while reducing latency and improving communication efficiency. This partnership is expected to accelerate commercialization of flat-panel satellite antennas and expand adoption of LEO-based maritime connectivity solutions.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Satellite Antenna Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Satellite Antenna Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Satellite Antenna Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.