Global Speciality Silicas Market

Market Size in USD Billion

CAGR :

%

USD

8.93 Billion

USD

15.92 Billion

2025

2033

USD

8.93 Billion

USD

15.92 Billion

2025

2033

| 2026 –2033 | |

| USD 8.93 Billion | |

| USD 15.92 Billion | |

| % | |

|

Speciality Silicas Market Size

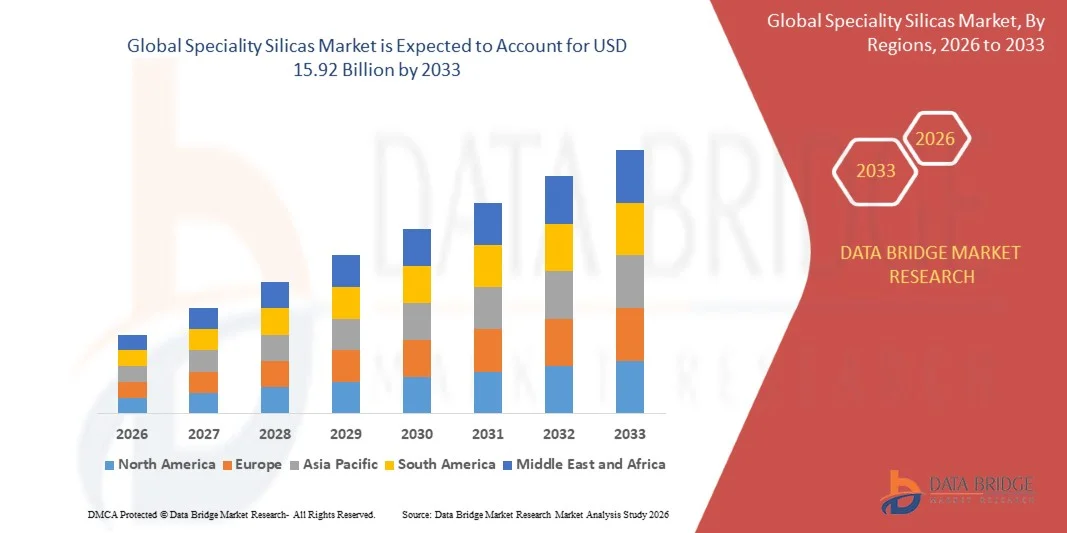

- The global speciality silicas market size was valued at USD 8.93 billion in 2025 and is expected to reach USD 15.92 billion by 2033, at a CAGR of 7.5% during the forecast period

- The market growth is largely fueled by the increasing demand for high-performance materials in the automotive and tire industry, where speciality silicas are widely used to improve fuel efficiency, durability, and wet grip performance of tires

- Furthermore, rising adoption of sustainable and energy-efficient solutions across rubber, coatings, and industrial applications is accelerating the shift toward advanced silica materials that enhance product performance while reducing environmental impact

Speciality Silicas Market Analysis

- Speciality silicas are high-purity silica-based materials used as reinforcing agents, thickeners, anti-caking agents, and performance enhancers across multiple industries such as rubber, food and healthcare, coatings, and plastics

- The escalating demand for speciality silicas is primarily driven by expanding automotive production, growing usage in high-performance rubber products, and increasing adoption in sustainable industrial and consumer applications

- Asia-Pacific dominated the speciality silicas market with a share of 42.5% in 2025, due to strong demand from rubber, automotive, and construction industries, along with rapid industrial expansion across emerging economies

- North America is expected to be the fastest growing region in the speciality silicas market during the forecast period due to increasing demand from tire manufacturing, coatings, and industrial rubber applications

- Precipitated silica segment dominated the market with a market share of 43.5% in 2025, due to its extensive use as a reinforcing agent in tire and rubber manufacturing. Its strong performance in improving tensile strength, abrasion resistance, and fuel efficiency has made it a preferred material across automotive applications

Report Scope and Speciality Silicas Market Segmentation

|

Attributes |

Speciality Silicas Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Speciality Silicas Market Trends

“Rising Adoption of Sustainable and Bio-Based Silica Production Technologies”

- A significant trend in the speciality silicas market is the increasing shift toward sustainable and bio-based production technologies driven by rising environmental regulations and demand for low-carbon industrial materials across end-use industries such as automotive, construction, and personal care. Manufacturers are focusing on reducing energy intensity and carbon emissions during silica synthesis while maintaining high performance standards for advanced applications such as tire reinforcement and coatings

- For instance, Evonik Industries and Solvay have developed silica production processes incorporating improved energy efficiency and reduced environmental footprint, supporting sustainable tire manufacturing and industrial applications. These advancements are strengthening adoption across global supply chains where sustainability compliance is becoming a key procurement requirement

- The integration of rice husk ash and other agricultural waste-based silica sources is gaining traction as industries aim to reduce dependence on conventional quartz-based raw materials. This shift is improving circular economy practices and enabling cost-efficient raw material utilization in silica manufacturing

- Automotive tire manufacturers are increasingly collaborating with silica producers to develop low rolling resistance tires that enhance fuel efficiency and reduce emissions. Companies such as Michelin and Bridgestone are actively incorporating advanced silica formulations into tire tread compounds to improve performance and sustainability outcomes

- The coatings and adhesives industry is also adopting eco-friendly silica variants to enhance product performance while aligning with regulatory standards on volatile emissions. This is supporting broader industrial transition toward green material inputs in high-performance formulations

- The market is witnessing continuous innovation in production technologies focused on reducing waste generation and optimizing process efficiency. This sustained transition toward sustainable silica manufacturing is reshaping competitive positioning across global speciality silica producers

Speciality Silicas Market Dynamics

Driver

“Growing Demand from Tire and Automotive Performance Enhancement Applications”

- The growing demand from tire and automotive industries is a key driver for the speciality silicas market as manufacturers increasingly use high-performance silica to improve fuel efficiency, wet traction, and durability of tires. The shift toward electric vehicles and stringent emission regulations is further accelerating the use of silica-based compounds in tire formulations

- For instance, Cabot Corporation supplies specialty silica grades used in energy-efficient tires developed by major tire manufacturers such as Goodyear. These materials help reduce rolling resistance while improving grip performance under diverse driving conditions

- The rising focus on vehicle lightweighting and fuel economy is encouraging the use of silica as a reinforcing filler in rubber and polymer applications. This enhances mechanical strength while supporting regulatory compliance for lower emissions in automotive manufacturing

- Automotive OEMs are collaborating with material suppliers to develop advanced tire technologies that enhance safety and performance efficiency. This is increasing the adoption of high-dispersion silica solutions in premium and high-performance tire segments

- The continued growth in global automotive production and replacement tire demand is sustaining long-term consumption of speciality silicas. This is positioning the automotive sector as a dominant end-user driving steady market expansion

Restraint/Challenge

“Volatile Raw Material Prices Impacting Production Costs”

- The speciality silicas market faces significant challenges due to fluctuations in raw material prices, particularly silica precursors such as sodium silicate and quartz-based feedstocks, which directly affect production costs and profit margins. Supply chain disruptions and energy price volatility further intensify cost pressures across manufacturing operations

- For instance, PQ Corporation and Cabot Corporation have experienced cost fluctuations in silica production linked to variations in energy and raw material supply conditions across global markets. These cost instabilities influence pricing strategies and long-term contract negotiations with end users

- The dependency on energy-intensive processes for silica extraction and refinement increases vulnerability to electricity and fuel price fluctuations. This results in inconsistent production economics and challenges in maintaining stable pricing structures

- Global supply chain uncertainties and transportation cost variations further contribute to cost unpredictability in raw material procurement. Manufacturers are often required to adjust sourcing strategies to manage input cost volatility

- The inability to fully offset rising raw material costs through pricing adjustments places pressure on profitability across the speciality silicas value chain. This continues to challenge manufacturers in achieving cost-efficient and stable production outcomess

Speciality Silicas Market Scope

The market is segmented on the basis of product type and application.

• By Product Type

On the basis of product type, the speciality silicas market is segmented into precipitated silica, silica gel, fused silica, colloidal silica, and fumed silica. The precipitated silica segment dominated the largest market revenue share of 43.5% in 2025, driven by its extensive use as a reinforcing agent in tire and rubber manufacturing. Its strong performance in improving tensile strength, abrasion resistance, and fuel efficiency has made it a preferred material across automotive applications. The segment also benefits from cost-effectiveness and large-scale industrial production, supporting consistent demand from tire manufacturers globally. Increasing focus on sustainable mobility and low rolling resistance tires further strengthens its adoption.

The fumed silica segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by rising demand in high-performance coatings, adhesives, and electronics applications. Its superior thickening, anti-caking, and rheology control properties make it highly suitable for advanced industrial formulations. The segment is gaining traction due to expanding use in lithium-ion batteries, pharmaceuticals, and precision chemicals. Continuous innovation in nanostructured materials and growing demand for lightweight, high-strength composites further accelerate its growth trajectory.

• By Application

On the basis of application, the speciality silicas market is segmented into rubber, food and healthcare, coatings, plastics, abrasives and refractories, and others. The rubber segment dominated the largest market revenue share in 2025, driven by strong demand from the automotive tire industry and industrial rubber goods manufacturing. Speciality silicas enhance rolling resistance, grip, and durability, making them essential in high-performance tire formulations. The segment also benefits from increasing vehicle production and replacement tire demand across emerging economies. Strong regulatory emphasis on fuel efficiency and emission reduction further supports adoption in rubber applications.

The food and healthcare segment is anticipated to witness the fastest growth rate from 2026 to 2033, driven by rising demand for silica as an anti-caking agent, stabilizer, and carrier in food additives and pharmaceuticals. Its increasing use in drug formulation and dietary supplements supports improved product stability and bioavailability. The segment is further supported by expanding health-conscious consumer trends and stricter food safety regulations. Growth in nutraceuticals and pharmaceutical manufacturing continues to accelerate adoption across global markets.

Speciality Silicas Market Regional Analysis

- Asia-Pacific dominated the speciality silicas market with the largest revenue share of 42.5% in 2025, driven by strong demand from rubber, automotive, and construction industries, along with rapid industrial expansion across emerging economies

- The region benefits from large-scale manufacturing capacity, rising investments in tire production, and increasing consumption of high-performance materials in coatings and plastics applications

- Expanding chemical production hubs, cost-efficient raw material availability, and supportive industrial policies are further strengthening speciality silica consumption across multiple end-use industries

China Speciality Silicas Market Insight

China held the largest share in the Asia-Pacific speciality silicas market in 2025, owing to its dominant position in rubber manufacturing, tire production, and large-scale chemical processing industries. Strong domestic demand from automotive and industrial sectors, along with extensive export-oriented manufacturing, supports market growth. Continuous investments in high-performance materials and specialty chemicals further reinforce China’s leading position in the regional market.

India Speciality Silicas Market Insight

India is witnessing the fastest growth in the Asia-Pacific region, driven by expanding automotive production, rising tire demand, and growing investments in construction and industrial manufacturing. Government initiatives supporting domestic manufacturing and infrastructure development are accelerating silica consumption across multiple applications. Increasing participation in global supply chains for rubber and chemical products is further boosting market expansion.

Europe Speciality Silicas Market Insight

The Europe speciality silicas market is expanding steadily, supported by strong demand for high-performance tires, advanced coatings, and sustainable material solutions. The region’s strict environmental regulations are encouraging the adoption of fuel-efficient and low-emission rubber products. Growing focus on innovation and specialty chemical development is further strengthening market penetration across industrial applications.

Germany Speciality Silicas Market Insight

Germany’s speciality silicas market is driven by its strong automotive industry, advanced chemical manufacturing base, and leadership in engineering and material innovation. High demand for premium tire solutions and industrial rubber products supports consistent silica consumption. Strong R&D infrastructure and focus on sustainable mobility solutions continue to enhance market development in the country.

U.K. Speciality Silicas Market Insight

The U.K. market is supported by growing demand from automotive, construction, and coatings industries, along with increasing adoption of advanced materials in industrial applications. Rising focus on sustainability and energy-efficient products is encouraging the use of speciality silicas in high-performance formulations. Ongoing investments in chemical innovation and manufacturing capabilities are further contributing to market growth.

North America Speciality Silicas Market Insight

North America is projected to grow at the fastest CAGR from 2026 to 2033, driven by increasing demand from tire manufacturing, coatings, and industrial rubber applications. Rapid advancements in automotive technologies and strong emphasis on fuel efficiency are boosting adoption of speciality silicas. In addition, rising investments in high-performance materials and sustainable product development are supporting regional market expansion.

U.S. Speciality Silicas Market Insight

The U.S. accounted for the largest share in the North America market in 2025, supported by a strong automotive sector, advanced chemical manufacturing base, and high demand for specialty rubber and coating materials. The country’s focus on innovation, sustainability, and performance-driven materials is driving silica adoption across multiple industries. Presence of key manufacturers and well-established supply chains further strengthens its leading position in the region.

Speciality Silicas Market Share

The speciality silicas industry is primarily led by well-established companies, including:

- Solvay (Belgium)

- Nissan Chemical Corporation (Japan)

- W. R. Grace & Co. (U.S.)

- Dalian Fuchang Chemical Co., Ltd. (China)

- Qingdao Makall Group Inc. (China)

- Anten Chemical Co., Ltd. (China)

- 3M (U.S.)

- Nalco Holding Company (U.S.)

- Oriental Silicas Corporation (Taiwan)

- Glassven C.A. (Venezuela)

- Madhu Silica Pvt. Ltd. (India)

- PQ Corporation (U.S.)

- Tosoh Corporation (Japan)

- Ecolab (U.S.)

- Tokuyama Corporation (Japan)

- Cabot Corporation (U.S.)

- Evonik Industries AG (Germany)

- Wacker Chemie AG (Germany)

- Kemira Oyj (Finland)

Latest Developments in Global Speciality Silicas Market

- In January 2026, Solvay launched Europe’s first bio-circular silica production facility at its Livorno site in Italy, utilizing bio-based sodium silicate derived from rice husk ash to manufacture highly dispersible silica (HDS) for sustainable tire applications. This development significantly strengthens the market’s shift toward low-carbon and circular economy solutions by reducing CO2 emissions by 35% per metric ton compared to conventional production methods. It also enhances regional supply chain sustainability by integrating agricultural waste streams into industrial silica manufacturing, supporting regulatory frameworks such as the European Green Deal

- In November 2025, Tata Chemicals sanctioned a USD 110 million expansion plan to increase soda ash and precipitated silica capacities across its Mithapur and Cuddalore facilities in India. The expansion, adding 50 ktpa of precipitated silica capacity, is aimed at meeting growing demand from automotive tires, glass, detergents, and clean energy applications including solar panels and EV batteries. This investment strengthens India’s domestic specialty silica production base while improving supply reliability for rapidly expanding end-use industries

- In November 2024, PQ Corporation completed a major specialty silica capacity expansion at its Pasuruan facility in Indonesia, introducing advanced micronizer technology to enhance production efficiency and product performance. This upgrade increases output of high-quality silica grades used in coatings, personal care, and pharmaceutical applications, helping the company address rising demand across Asia-Pacific markets. The expansion also improves product consistency and supports innovation in high-performance silica formulations

- In June 2024, Evonik Industries expanded its global silica production capabilities by optimizing its fumed and precipitated silica facilities in Europe and North America to support growing demand from tire, adhesives, and battery separator applications. This development enhances supply chain resilience and strengthens Evonik’s position in high-performance silica solutions, particularly for energy-efficient tire manufacturing and advanced industrial applications. The expansion also supports growing sustainability requirements through improved production efficiency and reduced environmental footprint

- In March 2024, W. R. Grace & Co. enhanced its precipitated silica manufacturing operations in North America through process optimization and capacity debottlenecking initiatives aimed at improving output for rubber and industrial applications. This development enables the company to better serve increasing demand from tire manufacturers focused on fuel efficiency and performance enhancement. It also strengthens regional supply capabilities and supports innovation in next-generation silica-based reinforcing materials

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Speciality Silicas Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Speciality Silicas Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Speciality Silicas Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.