The rising adoption of precision farming technologies is being shaped by the increasing need to make agricultural production more efficient, predictable, and economically viable. As farming operations face mounting pressure from fluctuating input costs, labor constraints, and yield uncertainty, technology-enabled approaches are being embraced to gain better control over field-level variability. Tools such as GPS-guided tractors, soil and crop sensors, satellite and drone-based imaging, and automated machinery are being deployed to monitor farm conditions with greater accuracy. Through these systems, real-time data is being captured across multiple stages of the crop cycle, allowing farming decisions to be guided by measurable field insights rather than traditional trial-and-error methods.

At the operational level, precision farming technologies are enabling targeted application of critical inputs, including seeds, fertilizers, irrigation, and crop protection chemicals. Instead of uniform input distribution, variable rate technologies are being used to match application levels with specific soil conditions, crop health, and yield potential. This approach is resulting in improved input-use efficiency, reduced wastage, and lower environmental impact, while also supporting consistent yield outcomes. By minimizing overuse of resources and addressing underperforming areas within fields, farms are being managed more systematically, leading to better cost control and improved return on investment over time.

Beyond productivity gains, precision farming is also contributing to a broader transformation in how farms are planned, monitored, and optimized. Data generated from connected equipment and digital platforms is being analyzed to support yield forecasting, risk assessment, and long-term farm planning. As climate variability and weather unpredictability increase, these technologies are being relied upon to anticipate stress factors and enable timely interventions. Collectively, the adoption of precision farming technologies is positioning agriculture as a more data-driven and resilient sector, where informed decision-making is becoming central to sustainable farm growth and long-term food security.

In conclusion, the rising adoption of precision farming technologies across global agriculture supported by increasing use of connected equipment, sensors, and data-driven farm management tools is a structural and long-term driver of the agritech market. As agricultural operations become more technology-enabled, precision-oriented, and resource-efficient, precision farming solutions will remain critical to improving productivity, reducing input inefficiencies, and enabling scalable, sustainable agricultural development across regions.

Access Full Report @ https://www.databridgemarketresearch.com/reports/global-agritech-market

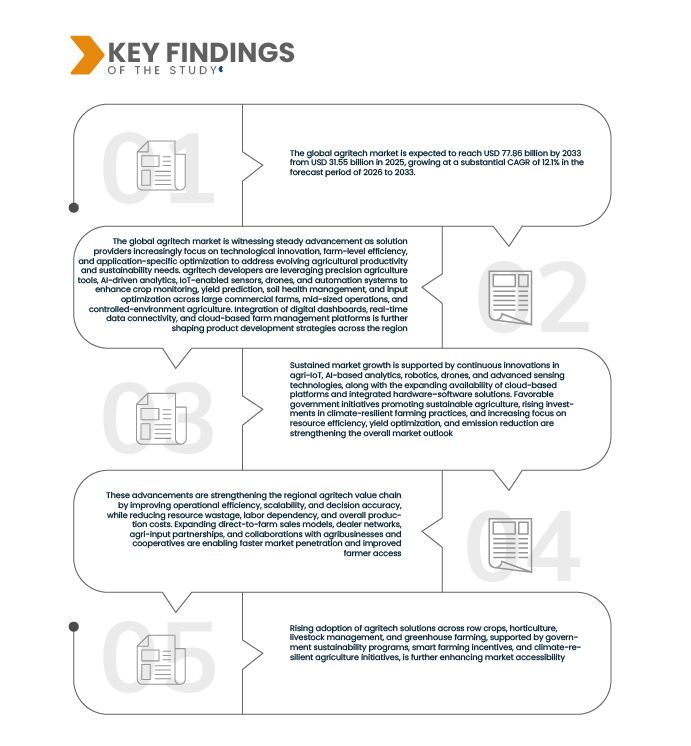

Data Bridge market research analyzes that the Global Agritech Market is expected to reach USD 77.86 billion by 2033 from USD 31.55 billion in 2025, growing at a substantial CAGR of 12.1% in the forecast period of 2026 to 2033.

Key Findings of the Study

Growing Pressure To Improve Agricultural Productivity On Limited Arable Land

Growing pressure to improve agricultural productivity on limited arable land is being driven by the combined impact of population growth, urban expansion, and the gradual degradation of cultivable soil. As agricultural land availability continues to shrink, farmers are being required to generate higher yields from existing farmland while maintaining economic viability. This challenge is intensifying the need for more efficient farming practices that maximize output per hectare without proportionally increasing input costs or environmental stress.

At the same time, competition for land from infrastructure development, industrial use, and housing is further constraining the expansion of agricultural acreage, particularly in rapidly developing regions. Traditional yield improvement methods are proving insufficient under these conditions, prompting greater reliance on advanced cultivation techniques, improved crop management practices, and technology-enabled productivity solutions. As a result, productivity enhancement is no longer viewed as optional but as a necessity for sustaining food supply chains.

In response, agritech-driven approaches are increasingly being adopted to address land constraints by improving soil health, optimizing crop planning, and enhancing yield predictability. By enabling precise resource allocation and data-informed decision-making, these solutions are supporting more intensive and efficient land use. This ongoing pressure to do more with less land is positioning productivity-focused agritech innovations as a core component of future agricultural resilience and global food security.

In conclusion, the growing pressure to improve agricultural productivity on limited arable land is emerging as a structural and long-term driver for the global agritech market, as expansion of cultivable land becomes increasingly constrained. As population growth, urbanization, and land degradation intensify competition for available farmland, productivity enhancement through technology-driven farming practices is becoming essential rather than optional. Agritech solutions that enable efficient land use, yield optimization, and sustainable resource management will remain critical to ensuring food security and long-term resilience of agricultural systems worldwide.

Report Scope and Market Segmentation

|

Report Metric

|

Details

|

|

Forecast Period

|

2025 to 2032

|

|

Base Year

|

2024

|

|

Historic Years

|

2023 (Customizable to 2018-2022)

|

|

Quantitative Units

|

Revenue in USD billion

|

|

Segments Covered

|

By Product Type (Precision Farming Equipment, Farm Management Software, Smart Irrigation Systems, Agricultural Drones and Others), By Plant Science (Genetic Engineering, Molecular Breeding, Genomic Selection And Marker-Assisted Breeding, Gene-Editing Technologies and Others), By Technology (Internet Of Things (Iot), Artificial Intelligence (AI), Big Data & Analytics, Remote Sensing, Blockchain and Others.), By Application (Crop Monitoring, Irrigation Management, Field Mapping, Soil Management, Weather Prediction, Livestock Monitoring, Supply Chain Management and Others), By Farm Size (Large Farms, Medium Farms an d Small Farms), By End User (Individual Farmers, Corporate Agribusinesses, Agricultural Cooperatives, Government & NGO Initiatives, Research Organizations and Others), By Distribution Channel (Direct and Indirect)

|

|

Countries Covered

|

U.S., Mexico, Canada, Germany, France, U.K., Hungary, Lithuania, Austria, Ireland, Norway, Poland, Italy, Spain, Russia, Turkey, Belgium, Netherlands, Switzerland, Rest of Europe, Japan, China, South Korea, India, Australia, Singapore, Thailand, Malaysia, Indonesia, Philippines, Vietnam, Rest of Asia-Pacific, Brazil, Argentina, Colombia, Peru, Chile, Ecuador, Venezuela, Bolivia, Uruguay, Paraguay, Rest of South America, Egypt, Saudi Arabia, UAE, South Africa, Israel, Rest of Middle East & Africa

|

|

Market Players Covered

|

|

|

Data Points Covered in the Report

|

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include depth expert analysis, pipeline analysis, pricing analysis, and regulatory framework.

|

Segment Analysis

The Global AgriTech Market is segmented into seven notable segments product type, plant science, technology, application, farm size, end user, and distribution channel.

- On the basis of product type, the market is segmented into Precision Farming Equipment, Farm Management Software, Smart Irrigation Systems, Agricultural Drones and Others.

In 2026, the precision farming equipment segment is expected to dominate the market

In 2026, the precision farming equipment segment is expected to dominate the market with a market share of 31.59 due to its widespread adoption of GPS-enabled machinery, variable rate application (VRA) systems, and automated guidance technologies that significantly improve input efficiency and crop yields. Rising pressure on farmers to reduce operational costs, optimize fertilizer and water usage, and enhance productivity per hectare is accelerating investments in advanced equipment. Additionally, strong government support through subsidies and smart agriculture initiatives across major agrarian economies is boosting equipment penetration. The integration of IoT sensors and AI-driven analytics into farm machinery further strengthens its value proposition. Moreover, large-scale farms in North America and Europe continue to prioritize mechanized and data-driven farming solutions, reinforcing segment dominance.

- On the basis of plant science, the market is segmented into Genetic Engineering, Molecular Breeding, Genomic Selection And Marker-Assisted Breeding, Gene-Editing Technologies and Others.

In 2026, the genetic engineering segment is expected to dominate the market

In 2026, genetic engineering segment dominates the market with a market share of 31.75% due to its critical role in enhancing crop yield, pest resistance, and climate resilience amid rising food security concerns. The segment benefits from accelerated adoption of genetically modified and gene-edited crops to address abiotic stresses such as drought and salinity. Strong R&D investments by leading agri-biotech firms and public research institutions have improved trait efficiency and commercialization timelines. Additionally, supportive regulatory reforms in major agricultural economies have enabled faster approvals of genetically engineered seeds. Growing demand for high-productivity crops from large-scale commercial farming further reinforces the segment’s market leadership.

- On the basis of technology, the market is segmented into Internet Of Things (IoT), Artificial Intelligence (AI), Big Data & Analytics, Remote Sensing, Blockchain and Others.

In 2026, the internet of things (IoT) segment is expected to dominate the market

In 2026, the internet of things (IoT) segment is expected to dominate the market with a market share of 35.36% due to its widespread adoption in precision farming, where connected sensors and smart devices enable real-time monitoring of soil moisture, crop health, weather conditions, and livestock performance. The ability of IoT platforms to deliver data-driven insights helps farmers optimize input usage such as water, fertilizers, and pesticides, directly improving yield and cost efficiency. Additionally, the rapid penetration of smart irrigation systems, connected farm machinery, and remote farm management solutions across both developed and emerging agricultural economies accelerates IoT uptake. Integration of IoT with cloud analytics and AI further enhances predictive decision-making, making it a foundational technology across the agri-value chain. Finally, strong government support for digital agriculture and increasing investments by agribusiness technology providers reinforce IoT’s dominant position within the AgriTech ecosystem.

- On the basis of application, the market is segmented into Crop Monitoring, Irrigation Management, Field Mapping, Soil Management, Weather Prediction, Livestock Monitoring, Supply Chain Management and Others.

In 2026, the Field Mapping segment is expected to dominate the market

In 2026, the Field Mapping segment is expected to dominate the market with a market share of 23.86% due to the rapid adoption of precision agriculture practices that rely on accurate geospatial data for plot-level decision-making. Field mapping enables farmers to optimize input usage such as seeds, fertilizers, and water, directly improving yield and cost efficiency. The integration of satellite imagery, GPS, drones, and AI-driven analytics has made field mapping more accurate, affordable, and scalable across farm sizes. Additionally, growing awareness around soil health monitoring, variable rate application, and regulatory reporting is driving consistent demand. Strong uptake across both developed and emerging agricultural economies further reinforces its leading market position.

- On the basis of farm size, the market is segmented into Large farms, Medium farms and Small farms.

In 2026, the large farms segment is expected to dominate the market

In 2026, the large farms segment is expected to dominate the market with a market share of 45.33% due to their higher capital availability and faster adoption of advanced AgriTech solutions such as precision farming platforms, AI-driven crop analytics, autonomous machinery, and IoT-based farm management systems. Large farms benefit from economies of scale, enabling them to justify investments in high-cost technologies that improve yield optimization and input efficiency. Additionally, they have better access to digital infrastructure, skilled labor, and data-driven decision tools, allowing seamless integration of end-to-end AgriTech solutions. Government incentives, sustainability mandates, and corporate-led smart agriculture initiatives also preferentially target large commercial farms, accelerating adoption. This combination of financial strength, operational scale, and technology readiness positions large farms as the primary revenue contributors to the global AgriTech market.

- On the basis of end user, the market is segmented into Individual farmers, Corporate agribusinesses, Agricultural cooperatives, Government & NGO initiatives, Research organizations and Others.

In 2026, the Individual farmers segment is expected to dominate the market

In 2026, the Individual farmers segment is expected to dominate the market with a market share of 36.37% due to the widespread adoption of cost-effective digital farming solutions such as precision agriculture tools, mobile-based farm management platforms, and IoT-enabled monitoring systems. Small and mid-sized farmers are increasingly leveraging government subsidies, digital advisory services, and affordable SaaS-based agri-solutions to improve crop yield and input efficiency. Rising smartphone penetration in rural areas and growing awareness of data-driven farming practices further accelerate adoption. Additionally, the availability of localized AgriTech solutions tailored to soil, weather, and crop-specific needs enhances usability at the individual farmer level. The faster decision-making cycle and direct return on investment realization also make AgriTech adoption more attractive for individual farmers compared to institutional buyers.

- On the basis of distribution channel, the market is segmented into indirect and direct.

In 2026, the indirect segment is expected to dominate the market

In 2026, the Indirect segment is expected to dominate the market with a market share of 54.95% due to its ability to leverage extensive distributor, dealer, and agribusiness networks that enable deeper penetration into fragmented rural markets. Indirect channels reduce go-to-market costs for technology providers while offering localized sales, installation, and after-sales support to farmers. These channels also benefit from strong relationships with cooperatives, input suppliers, and government-backed agricultural programs. Additionally, indirect models allow faster scaling across emerging economies where digital literacy and direct access remain limited. The availability of bundled solutions (hardware, software, financing, and advisory services) further strengthens adoption through indirect distribution.

Major Players

Deere & Company (U.S.), AGCO Corporation (U.S.), Bayer Cropscience (Germany), Syngenta AG (Switzerland), CNH Industrial N.V. (U.K.), AG Leader Technology (U.S.), Cropin Technology Solutions Private Limited (India), Corteva (U.S.), Cropx Inc (U.S.)among others.

Market Developments

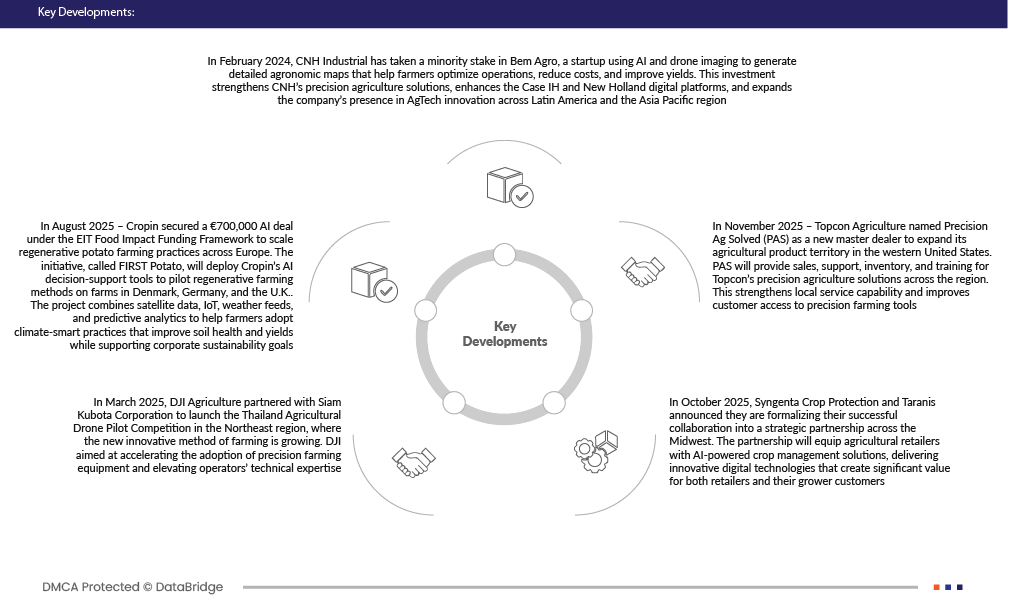

- In February 2024, CNH Industrial has taken a minority stake in Bem Agro, a startup using AI and drone imaging to generate detailed agronomic maps that help farmers optimize operations, reduce costs, and improve yields. This investment strengthens CNH’s precision agriculture solutions, enhances the Case IH and New Holland digital platforms, and expands the company’s presence in AgTech innovation across Latin America and the Asia Pacific region.

- In August 2025 – Cropin secured a €700,000 AI deal under the EIT Food Impact Funding Framework to scale regenerative potato farming practices across Europe. The initiative, called FIRST Potato, will deploy Cropin’s AI decision-support tools to pilot regenerative farming methods on farms in Denmark, Germany, and the UK. The project combines satellite data, IoT, weather feeds, and predictive analytics to help farmers adopt climate-smart practices that improve soil health and yields while supporting corporate sustainability goals.

- In 2025, August Cropin has been featured in global media for how leading agrifood companies like PepsiCo and Walmart are using AI and data intelligence from Cropin to fortify supply chains and improve yield predictions. These stories highlight Cropin’s impact in enabling real-time data tracking, predictive advisory systems, and climate-smart decision-making at scale across major agricultural value chains. Such coverage reflects broader industry recognition of Cropin’s role in digitalizing farm-to-enterprise operations.

- In November 2025 – Topcon Agriculture named Precision Ag Solved (PAS) as a new master dealer to expand its agricultural product territory in the western United States. PAS will provide sales, support, inventory, and training for Topcon’s precision agriculture solutions across the region. This strengthens local service capability and improves customer access to precision farming tools .

- In June 2025, The DJI Agriculture Smart Farm Web V5.0 introduces an all-in-one management system for efficient drone data, field planning, and device control. It features an upgraded UI for improved user experience and stability, with faster field mapping and centralized equipment management. The platform also enhances data retrieval and export processes for smarter farming.

- In October 2025, Syngenta Crop Protection and Taranis announced they are formalizing their successful collaboration into a strategic partnership across the Midwest. The partnership will equip agricultural retailers with AI-powered crop management solutions, delivering innovative digital technologies that create significant value for both retailers and their grower customers.

Regional Analysis

Geographically, the countries covered in the global agritech market report are U.S., Canada, Mexico, France, Germany, Russia, Italy, Spain, Turkey, U.K., Netherlands, Denmark, Switzerland, Belgium, Sweden, Norway, Finland, Rest Of Europe, China, India, Japan, Australia, South Korea, Indonesia, Thailand, Taiwan, Singapore, New Zealand, Malaysia, Philippines, Hong Kong, Rest of Asia-Pacific, Brazil, Argentina, Colombia, Peru, Chile, Ecuador, Venezuela, Bolivia, Uruguay, Paraguay, Rest of South America, South Africa, Egypt, Saudi Arabia, United Arab Emirates, Israel, Bahrain, Kuwait, Oman, Qatar, and Rest of Middle East & Africa.

As per Data Bridge Market Research analysis:

Asia-Pacific is the dominant region in the global agritech market during the forecast period of 2025 to 2033

Asia-Pacific is projected to dominate the global agritech market during the forecast period of 2026–2033 due to a combination of structural, economic, and policy-driven factors. The region hosts the world’s largest agricultural workforce and cultivated land base, particularly across China, India, and Southeast Asian nations, creating strong demand for productivity-enhancing technologies. Rapid population growth and rising food consumption are compelling governments to adopt smart farming, precision agriculture, and digital farm management solutions. Strong public investment and subsidy programs supporting agri-digitization, drone usage, AI-based crop monitoring, and smart irrigation systems are accelerating technology penetration.

The region is witnessing high adoption of mobile-based agri-platforms due to deep smartphone and internet penetration in rural areas. Increasing climate variability and water stress are pushing farmers toward data-driven farming and IoT-enabled solutions. Presence of a large base of small and marginal farmers encourages scalable, low-cost AgriTech innovations. Additionally, expanding agri-startup ecosystems in countries such as Japan, Australia, and South Korea are fostering rapid commercialization of advanced technologies. Collectively, these factors position Asia-Pacific as the most influential and revenue-generating region in the Global AgriTech market through 2033.

Europe is anticipated to be the witness fastest growth in the global agritech market

Europe is anticipated to witness notable growth in the global agritech market due to a convergence of regulatory, technological, and sustainability-driven factors across the region. In Europe, stringent environmental regulations and the EU’s Common Agricultural Policy (CAP) are actively encouraging farmers to adopt precision farming, smart irrigation, and digital farm management solutions to improve productivity while reducing environmental impact. The region has a high penetration of advanced farm machinery and digital infrastructure, enabling faster integration of AI, IoT, drones, and data analytics into agricultural operations. Rising labor shortages and increasing input costs are further accelerating the shift toward automation and robotics in farming. Europe also benefits from strong government funding, subsidies, and R&D programs supporting climate-resilient and sustainable agriculture technologies. Additionally, growing consumer demand for traceable, organic, and sustainably produced food is pushing farmers to invest in AgriTech solutions that enhance transparency and yield optimization.

Compared to emerging regions, Europe’s relatively mature farming ecosystem allows quicker scalability of advanced solutions after pilot adoption. While South America leads growth due to large-scale commercial farming and rapid technology uptake, Europe follows closely with steady, policy-backed adoption. The presence of several AgriTech startups and collaborations between agribusinesses, research institutions, and technology providers further strengthens the regional ecosystem. Moreover, increasing climate variability across Europe is compelling farmers to rely on predictive analytics and smart farming tools for risk mitigation. Collectively, these factors position Europe as the next major growth engine in the Global AgriTech market after South America.

For more detailed information about the Global Agritech Market report, click here – https://www.databridgemarketresearch.com/reports/global-agritech-market