Stringent regulations and globally recognized standards related to serialization and traceability are significantly reshaping industrial and logistics operations worldwide. Governments and regulatory authorities increasingly mandate standardized labeling formats, machine-readable codes, and unique product identifiers to enhance supply chain transparency, safety, and accountability across industries such as pharmaceuticals, chemicals, food, electronics, and industrial manufacturing. These regulations require the use of durable, high-accuracy labels capable of supporting barcodes, QR codes, and data matrix symbologies that remain readable throughout storage, handling, and transportation. The growing enforcement of serialization and traceability regulations across major economies highlights the critical role of standardized, high-performance labeling in modern supply chains. Regulatory mandates from the U.S., China, and India clearly demonstrate that compliance now depends on accurate, durable, and data-rich industrial and logistics labels capable of supporting global standards such as GS1. As governments continue to strengthen anti-counterfeiting measures, recall readiness, and cross-border traceability frameworks, industries are compelled to invest in advanced labeling solutions. Consequently, these stringent regulations and evolving standards consistently reinforce demand, positioning them as a decisive driver for sustained expansion of the global industrial & logistics labels market.

Access Full Report @ https://www.databridgemarketresearch.com/reports/global-industrial-and-logistics-labels-market

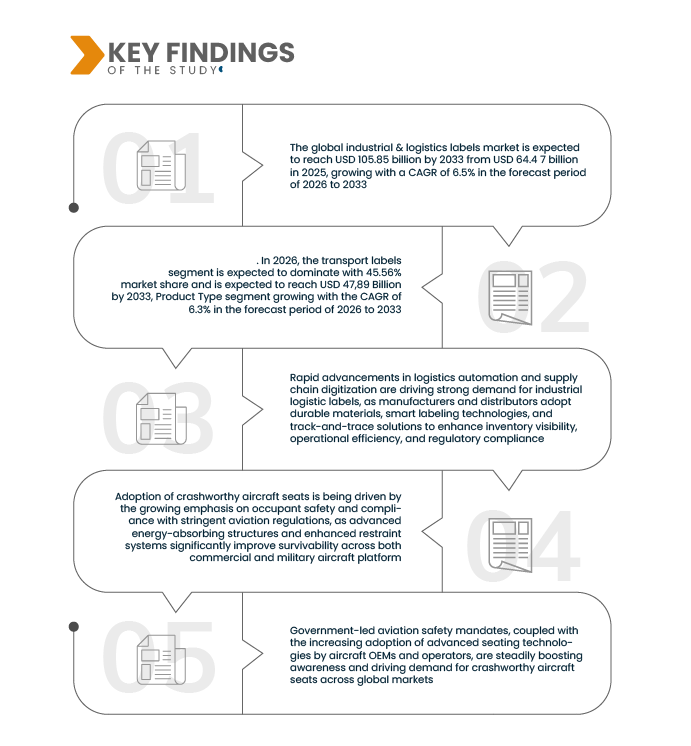

Data Bridge market research analyzes that the Global Industrial and Logistics Labels Market is expected to reach USD 105.85 billion by 2033 from USD 64.47 billion in 2025, growing with a substantial CAGR of 6.5% in the forecast period of 2026 to 2033.

Key Findings of the Study

Technological Advancements in Track and Trace Solutions

Technological advancements in track and trace solutions are significantly transforming global industrial and logistics operations, strengthening supply chain visibility, accuracy, and efficiency. The adoption of technologies such as RFID, IoT-enabled labeling, 2D Data Matrix and QR codes, cloud-based data platforms, and advanced analytics has elevated the role of industrial and logistics labels from basic identification tools to critical data carriers. Modern track and trace systems require labels that support high-speed scanning, real-time data capture, and seamless integration with warehouse management and transportation systems. Increasing automation in warehouses, smart logistics infrastructure, and digitally connected supply chains has intensified the need for durable, high-performance labels that remain readable under harsh handling, storage, and environmental conditions. These technological developments also support improved inventory control, shipment monitoring, loss prevention, and regulatory compliance across industries. As track and trace technologies continue to advance and scale globally, the demand for sophisticated, data-integrated labeling solutions increases, positioning technological advancements as a key driver for sustained growth in the global industrial & logistics labels market.

Technological advancements such as IoT, AI, blockchain, RFID, and machine-readable codes are fundamentally enhancing supply chain transparency, efficiency, and security. These innovations enable real-time tracking, predictive analytics, and fraud prevention, transforming traditional logistics into agile and intelligent systems. As industries increasingly adopt these sophisticated track and trace technologies, the demand for durable, high performance, and data-integrated industrial and logistics labels rises correspondingly. Consequently, ongoing technological progress serves as a pivotal driver fueling sustained growth in the global industrial & logistics labels market.

Report Scope and Market Segmentation

|

Report Metric

|

Details

|

|

Forecast Period

|

2026 to 2033

|

|

Base Year

|

2025

|

|

Historic Years

|

2024 (Customizable to 2018-2023)

|

|

Quantitative Units

|

Revenue in USD Billion

|

|

Segments Covered

|

By Product Type (Transport Labels, Direct Thermal Labels, Thermal Transfer Labels, RFID/Smart Labels, Linerless Labels, and Others), Printing Technology (Flexographic, Digital, and Thermal), Material (Facestock, Adhesive, and Liner), Application (Shipping & Parcel, Warehouse & Inventory, Asset Tracking & Durable ID, Cold Chain & Temp-Sensitive, HAZMAT/Regulatory, Compliance & Serialization, and Others), End User (E-commerce, 3PL & Fulfillment, Manufacturing, Food & Beverage, Healthcare & Pharmaceutical, Retail & FMCG, Postal & Courier, and Others), Distribution Channel (Indirect and Direct)

|

|

Countries Covered

|

U.S., Canada, Mexico, Germany, U.K., France, Italy, Spain, Russia, Turkey, Netherlands, Norway, Finland, Denmark, Sweden, Poland, Switzerland, Belgium, Rest of Europe, China, Japan, India, South Korea, Australia, Indonesia, Thailand, Malaysia, Singapore, Hong Kong, Philippines, Rest of Asia-Pacific, Argentina, Bolivia, Brazil, Chile, Colombia, Ecuador, Paraguay, Peru, Uruguay, Venezuela Rest of South America, U.A.E., Saudi Arabia, South Africa, Egypt, Israel, Kuwait, Oman, Qatar, Bahrain and Rest of Middle East and Africa

|

|

Market Players Covered

|

|

|

Data Points Covered in the Report

|

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework.

|

Segment Analysis

The global industrial & logistics labels market is segmented into six notable segments based on product type, printing technology, material, application, end-use industry, and distribution channel.

- On the basis of product type, the market is segmented into transport labels, direct thermal labels, thermal transfer labels, RFID/smart labels, linerless labels, and others.

In 2026, the transport labels segment is expected to dominate the market

In 2026, the transport labels segment is expected to dominate the market with a market share of 45.56% due to rapid expansion of global trade, e-commerce, and logistics networks. Transport labels are critical for shipment identification, routing, tracking, and regulatory compliance. Their high-volume usage, cost efficiency, and compatibility with automated sorting systems make them indispensable across industrial and logistics operations worldwide.

- On the basis of printing technology, the market is segmented into flexographic, digital, and thermal.

In 2026, the flexographic projects segment is expected to dominate the market

In 2026, flexographic segment dominates the market with a market share of 38.22% due to its ability to deliver high-speed, high-volume printing at low operational costs. Flexographic printing supports a wide range of substrates and inks, ensuring durability and print consistency. Its scalability, efficiency for mass production, and suitability for logistics labeling drive widespread adoption across industrial applications.

- On the basis of material, the market is segmented into facestock, adhesive, and liner.

In 2026, the facestock segment is expected to dominate the market

In 2026, the facestock segment is expected to dominate the market with a market share of 68.78% as it forms the primary printable surface of industrial and logistics labels. The growing demand for durable, tear-resistant, and weatherproof labels in transportation and warehousing boosts facestock consumption. Advancements in synthetic facestocks further enhance performance in harsh handling and environmental conditions.

- On the basis of application, the market is segmented into shipping & parcel, warehouse & inventory, asset tracking & durable ID, cold chain & temp-sensitive, HAZMAT/regulatory, compliance & serialization, and others.

In 2026, the shipping & parcel segment is expected to dominate the market

In 2026, the shipping & parcel segment is expected to dominate the market with a market share of 36.09% as they are the essential for accurate delivery, tracking, and sorting of goods. The surge in e-commerce shipments, cross-border trade, and last-mile delivery operations significantly increases label volumes, making shipping and parcel applications the largest contributor to overall market demand.

- On the basis of end use, the market is segmented into e-commerce, 3PL & fulfillment, manufacturing, food & beverage, healthcare & pharmaceutical, retail & FMCG, postal & courier, and others.

In 2026, the e-commerce segment is expected to dominate the market

In 2026, the e-commerce segment is expected to dominate the market with a market share of 38.33% due to exponential growth in online retail and direct-to-consumer shipping. High order volumes, frequent returns, and the need for real-time tracking drive continuous demand for industrial labels. Automation and fulfillment center expansion further reinforce label consumption in this sector.

- On the basis of distribution channel, the market is segmented into direct and indirect.

In 2026, the indirect segment is expected to dominate the market

In 2026, the indirect segment is expected to dominate the market with a market share of 72.05% as they are supported by extensive distributor networks, value-added resellers, and system integrators. Indirect channels offer broader market reach, technical support, and bundled solutions, making them preferred by small and mid-sized logistics and industrial customers seeking cost-effective procurement.

Major Players

Avery Dennison Corporation (U.S.), CCL Industries Inc. (Canada), UPM Corporation (Finland), Fedrigoni Self-Adhesives (Italy), Brady Corporation (U.S.), and Lintec Corporation (Japan), among others.

Market Developments

- In December 2025, 3M announced it will debut new AI powered tools and expanded digital materials capabilities at CES 2026, reinforcing its innovation pipeline that supports smarter material solutions potentially including advanced labeling and tracking applications across industries such as logistics and manufacturing.

- In August 2025, Brady Corporation completed the acquisition of Mecco, strengthening its identification and traceability solutions portfolio by integrating Mecco’s complementary technologies and market presence into Brady’s global product and service offerings.

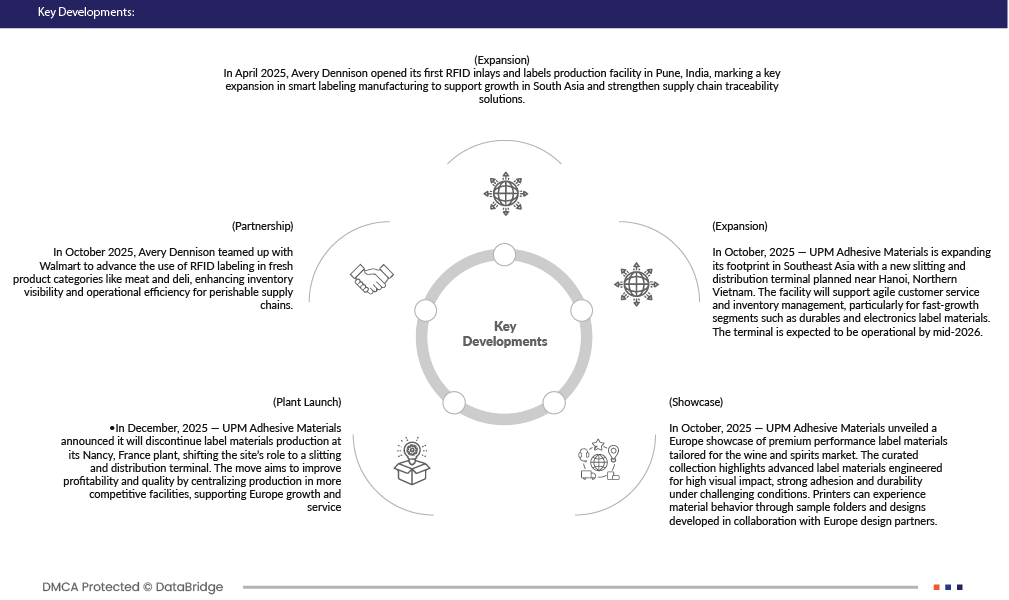

- In April 2025, Avery Dennison opened its first RFID inlays and labels production facility in Pune, India, marking a key expansion in smart labeling manufacturing to support growth in South Asia and strengthen supply chain traceability solutions.

- In March 2025, Beontag expands RFID portfolio with microwave and waterproof resistant tag. The eWave and Carrier eWave UHF RFID tag allows greater versatility and sustainability in the food and beverage sector while optimizing asset management and streamlining supply chains

- In October 2024, RAJA completed acquisition of RETIF, a European distributor of retail‑shop supplies and e‑commerce‑enabled business, adding its network of brick‑and‑mortar stores plus e‑commerce channels across 7 European countries. acquisition broadens RAJA’s distribution network and customer base boosting its ability to supply packaging and related products to a larger set of retailers, including those selling online.

- In March 2022, H.B. Fuller showcased its Swift melt pressure‑sensitive adhesives, including the Swift melt Earthic range, at PRINTPACK INDIA 2022. These adhesives are designed for labels, tapes, containers, and courier bags, sticking strongly to tough surfaces and working efficiently in production. By presenting these innovative products, H.B. Fuller strengthened its presence in the industrial and packaging markets and reinforced its role as a reliable provider of high-performance adhesive solutions.

Regional Analysis

Geographically, the countries covered in the global industrial & logistics labels market report are U.S., Canada, Mexico, Germany, France, U.K., Italy, Russia, Spain, Switzerland, Netherlands, Turkey, Belgium, Rest of Europe, China, India, Japan, South Korea, Thailand, Indonesia, Malaysia, Singapore, Philippines, Australia, Rest of Asia-Pacific, Argentina, Bolivia, Brazil, Chile, Colombia, Ecuador, Paraguay, Peru, Uruguay, Venezuela, Rest of South America, Saudi Arabia, U.A.E., South Africa, Egypt, Israel, Rest of Middle East and Africa.

As per Data Bridge Market Research analysis:

Asia-Pacific is the dominant region in the global industrial & logistics labels market during the forecast period of 2025 to 2032

Asia-Pacific is expected to dominate the market due to its cost competitive labor, large scale production capabilities, and widespread presence of label converters and raw material suppliers. Government initiatives supporting manufacturing, logistics infrastructure upgrades, and foreign direct investment further strengthen regional output. Additionally, rising domestic consumption, urbanization, and growing small and medium enterprises accelerate demand for packaging, shipping, and compliance labels across multiple end use industries throughout diverse Asia-Pacific economies regionally.

Furthermore, Asia-Pacific is expected to grow fastest during the forecast period due to accelerating e-commerce penetration, digital supply chain adoption, and increasing investments in smart logistics facilities. The shift toward sustainable packaging, smart labels, and traceability solutions is gaining momentum among manufacturers and exporters. Rapid infrastructure development, rising cross border trade, and technology adoption among logistics providers continue to enhance regional market growth prospects across emerging and developed Asia-Pacific markets globally.

North America is anticipated to be the witness growth in the global industrial & logistics labels market

North America growth in the global industrial & logistics labels market is supported by advanced logistics networks, high automation levels, and strong regulatory compliance requirements. Growth in e-commerce fulfillment, food and beverage distribution, and pharmaceutical supply chains drives consistent label demand. Additionally, technological innovation, adoption of RFID and smart labels, and investments in sustainable packaging solutions contribute to steady regional expansion across manufacturing retail and healthcare industries nationwide.

For more detailed information about the global industrial & logistics labels market report, click here – https://www.databridgemarketresearch.com/reports/global-industrial-and-logistics-labels-market