The commercial landscaping and groundskeeping sector in North America and Europe have emerged as a key demand generator for zero-turn mowers, driven by expanding urban development, commercial real estate growth, and increasing investments in public green infrastructure. In cities and suburbs across the United States, Canada, Germany, France, and the United Kingdom, professional landscapers and maintenance contractors are responsible for the upkeep of parks, golf courses, corporate campuses, municipal properties, and mixed-use developments. These large, varied grounds require efficient, high-capacity mowing solutions that can significantly reduce operational time and labor costs compared with traditional riding mowers or walk-behind units. In both regions, competitive landscaping services are increasingly focused on operational efficiency and service turnaround times to meet client expectations. Zero-turn mowers’ ability to deliver wider cutting swaths, tighter turning radii, and faster coverage directly supports the productivity needs of professional groundskeeping fleets. This commercial focus on speed, precision, and reliability paired with the strong service and maintenance infrastructure available in North America and Europe enhances the value proposition of zero-turn mowers for professional users and reinforces their adoption across large-scale landscaping applications.

In conclusion, the strong commercial landscaping and groundskeeping industry across North America and Europe serves as a critical driver for the adoption of zero-turn mowers. The presence of extensive corporate campuses, municipal parks, sports complexes, and public green spaces has created a sustained demand for professional grounds maintenance services, where efficiency, precision, and time-saving equipment are paramount.

Access Full Report @ https://www.databridgemarketresearch.com/reports/north-america-and-europe-zero-turn-mower-market

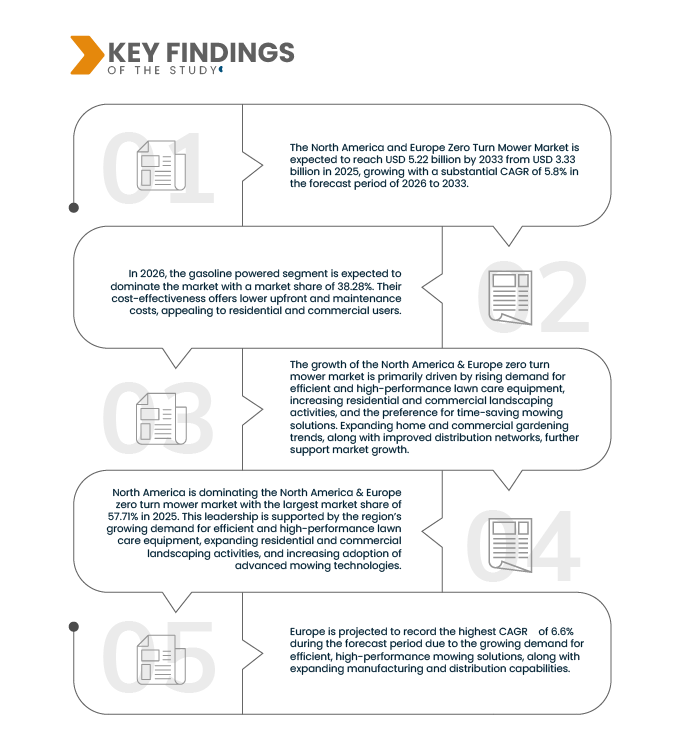

Data Bridge market research analyzes that The North America and Europe Zero Turn Mower Market is expected to reach USD 5.22 billion by 2033 from USD 3.33 billion in 2025, growing with a substantial CAGR of 5.8% in the forecast period of 2026 to 2033.

Key Findings of the Study

Labor Cost Sensitivity and Productivity Optimization

Rising labor costs and workforce shortages across North America and Europe have increasingly influenced the operational strategies of landscaping companies, municipal maintenance teams, and commercial groundskeeping services. In the United States and Canada, as well as in Germany, the U.K, and France, wage growth and limited availability of skilled groundskeeping personnel have made efficiency a central concern for both residential and commercial lawn maintenance operations. This environment has encouraged the adoption of labor-saving equipment, such as zero-turn mowers, which can significantly reduce the number of labor hours required to maintain large lawns, parks, and commercial landscapes. Zero-turn mowers allow operators to complete mowing tasks faster and with fewer passes compared to traditional riding mowers, thereby optimizing workforce utilization and reducing operational costs. The combination of high productivity, precision in maneuvering around obstacles, and lower time-per-task makes zero-turn mowers particularly attractive in regions where labor expenses are substantial and scheduling efficiency is critical. As a result, sensitivity to labor costs and the need for productivity optimization continue to drive sustained market adoption of zero-turn mowers across North America and Europe.

In conclusion, labor cost sensitivity and productivity optimization continue to play a pivotal role in driving the adoption of zero-turn mowers across North America and Europe. Rising wages, workforce shortages, and increasing non-wage employment costs in both regions have made efficiency a key operational priority for landscaping companies, municipal maintenance teams, and commercial groundskeeping service providers.

Report Scope and Market Segmentation

|

Report Metric

|

Details

|

|

Forecast Period

|

2026 to 2033

|

|

Base Year

|

2025

|

|

Historic Years

|

2024 (Customizable to 2019 - 2023)

|

|

Quantitative Units

|

Revenue in USD Thousand

|

|

Segments Covered

|

By Product Type (Gasoline-Powered, Diesel-Powered, Electric-Powered, Hybrid and Others), By Horse Power (Low (Under 20 HP), Medium (20-30 HP) and High (Over 30 HP)), By Deck Size (Under 48 Inches, 48–60 Inches and Over 60 Inches), By Application (Residential and Commercial) By End User (Individual/Domestic Users, Commercial Service Providers, Institutional Users, Hospitality & Real Estate and Municipal & Public Works), By Distribution Channel (Direct and Indirect)

|

|

Countries Covered

|

U.S., Canada, Mexico, Germany, U.K., Italy, France, Spain, Russia, Turkey, Belgium, Netherlands, Switzerland, Denmark, Poland, Sweden, and Rest of Europe

|

|

Market Players Covered

|

|

|

Data Points Covered in the Report

|

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand.

|

Segment Analysis

The North America and Europe zero turn mower market is segmented into six notable segments based on product type, horse power, deck size, application, end user, and distribution channel.

- On the basis of product type, the North America and Europe zero turn mower market is segmented into gasoline powered, diesel-powered, electric-powered, hybrid, and others.

In 2026, the gasoline powered segment is expected to dominate the market

In 2026, the gasoline powered segment is expected to dominate the market with a market share of 38.28%. Their cost-effectiveness offers lower upfront and maintenance costs, appealing to residential and commercial users. Widespread gasoline availability ensures quick refueling and minimal downtime on large properties. Superior engine performance handles thick grass and uneven terrain effectively. Extensive aftermarket support, including dealer networks and parts, boosts reliability and longevity. Despite rising electric and hybrid options due to emissions rules, gasoline's proven ecosystem maintains its lead.

- On the basis of horse power, the market is segmented into o low (under 20 HP), medium (20-30 HP), high (over 30 HP).

In 2026, the low (under 20 HP) segment is expected to dominate the market

In 2026, low (under 20 HP) segment dominates the market with a market share of 43.57%. Their suitability for smaller residential lawns makes them ideal for homeowners managing compact properties without needing excessive power. Lower operating and maintenance costs reduce long-term expenses, enhancing affordability for budget-conscious users. Ease of handling appeals to non-professionals, while growing adoption in light commercial tasks like small estates solidifies their dominance over medium and high HP segments.

- On the basis of deck size, the market is segmented into 48 inches, 48–60 inches, and over 60 inches.

In 2026, the 48 inches segment is expected to dominate the market

In 2026, the 48 inches segment is expected to dominate the market with a market share of 37.04% due to its balanced performance, ability to efficiently cover medium to large lawns, affordability, and compatibility with both residential and commercial mowing requirements.

- On the basis of application, the market is segmented into residential and commercial.

In 2026, the commercial segment is expected to dominate the market

In 2026, the commercial segment is expected to dominate the market with a market share of 65.60% due to growing demand from professional landscapers, sports and educational institutions, government grounds maintenance, and an increasing number of large-scale landscaping projects requiring efficient, high-performance mowing equipment.

- On the basis of end user, the market is segmented into individual/domestic users, commercial service providers, institutional users, hospitality & real estate, and municipal & public works.

In 2026, the commercial service providers segment is expected to dominate the market

In 2026, the commercial service providers segment is expected to dominate the market with a market share of 22.23% due to increasing outsourcing of landscaping services, higher investment in commercial grade equipment, the need for efficiency and reliability, and growing adoption across corporate, hospitality, and municipal facilities.

- On the basis of distribution channel, the market is segmented into direct and indirect.

In 2026, the commercial service providers segment is expected to dominate the market

In 2026, the direct segment is expected to dominate the market with a market share of 53.23%, due to stronger manufacturer support, better customer service, exclusive product availability, competitive pricing strategies, and the growing preference of end users to purchase directly from brands for assured quality and warranty.

Major Players

Deere & Company (U.S.), Husqvarna AB (Sweden), Stanley Black & Decker, Inc. (CUB CADET) (U.S.), Briggs & Stratton (U.S.), KUBOTA Corporation (Japan), among others.

Market Developments

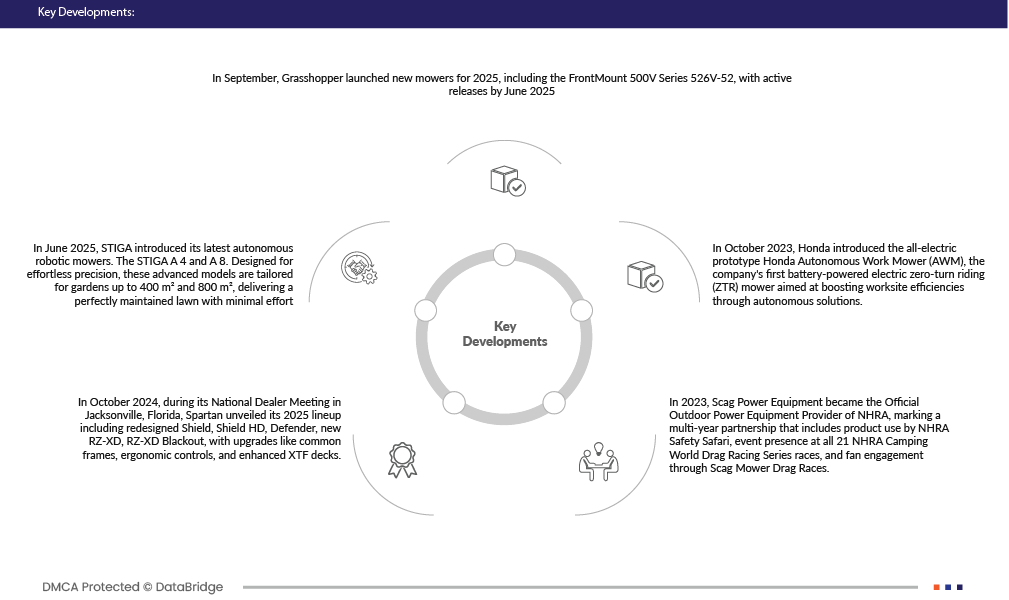

- In September, Grasshopper launched new mowers for 2025, including the FrontMount 500V Series 526V-52, with active releases by June 2025.

- In June 2025, STIGA introduced its latest autonomous robotic mowers. The STIGA A 4 and A 8. Designed for effortless precision, these advanced models are tailored for gardens up to 400 m² and 800 m², delivering a perfectly maintained lawn with minimal effort.

- In October 2024, during its National Dealer Meeting in Jacksonville, Florida, Spartan unveiled its 2025 lineup including redesigned Shield, Shield HD, Defender, new RZ-XD, RZ-XD Blackout, with upgrades like common frames, ergonomic controls, and enhanced XTF decks.

- In 2023, Scag Power Equipment became the Official Outdoor Power Equipment Provider of NHRA, marking a multi-year partnership that includes product use by NHRA Safety Safari, event presence at all 21 NHRA Camping World Drag Racing Series races, and fan engagement through Scag Mower Drag Races. The collaboration highlights Scag’s full line of commercial and residential mowers while enhancing brand visibility, customer experience, and engagement with both dealers and end users, strengthening its market presence in the motorsports and outdoor equipment communities.

- In October 2023, Honda introduced the all-electric prototype Honda Autonomous Work Mower (AWM), the company's first battery-powered electric zero-turn riding (ZTR) mower aimed at boosting worksite efficiencies through autonomous solutions.

Regional Analysis

Geographically, the countries covered in the North America and Europe Zero Turn Mower Market report are U.S., Canada, Mexico, Germany, U.K., Italy, France, Spain, Russia, Turkey, Belgium, Netherlands, Switzerland, Denmark, Poland, Sweden, and Rest of Europe.

As per Data Bridge Market Research analysis:

North America is the dominant region in the North America and Europe Zero Turn Mower Market during the forecast period of 2026 to 2033

North America is expected to dominate the market due to its mature landscaping industry, high residential homeowner demand, and extensive commercial turf management across expansive suburban and rural areas. Widespread adoption arises from favorable terrain suiting large lawns, robust dealer networks ensuring accessibility, and preferences for powerful, maneuverable mowers that excel in efficiency. These factors collectively drive its leading position through 2033.

Europe is anticipated to be the witness fastest growth in the North America and Europe Zero Turn Mower Market

Europe growth in the North America and Europe zero turn mower market is driven by rising urbanization and an increasing focus on landscaping for both commercial and residential properties. The demand for high-performance and eco-friendly mowers is boosting the market. Furthermore, the shift towards sustainable solutions, coupled with the adoption of advanced lawn care technologies, is propelling the market forward. This, along with government incentives for energy-efficient products, supports Europe’s robust growth in this segment.

For more detailed information about the North America and Europe Zero Turn Mower Market report, click here – https://www.databridgemarketresearch.com/reports/north-america-and-europe-zero-turn-mower-market