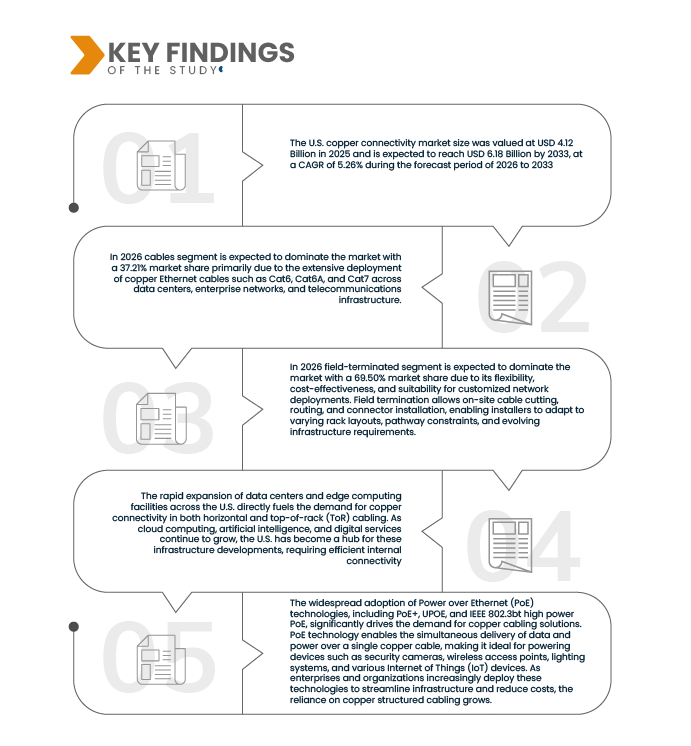

The rapid expansion of data centers and edge computing facilities across the U.S. directly fuels the demand for copper connectivity in both horizontal and top-of-rack (ToR) cabling. As cloud computing, artificial intelligence, and digital services continue to grow, the U.S. has become a hub for these infrastructure developments, requiring efficient internal connectivity. While fiber optics are predominantly used for long-distance backbone connections, copper remains the preferred solution for short-range, cost-effective interconnects within the data center. Copper’s reliability, ease of installation, and cost-efficiency make it ideal for patch cords, trunk assemblies, and internal cabling, where high-speed, low-latency connectivity is needed between servers and network equipment. With a substantial increase in data center transactions and expansions, as reported in industry publications, the demand for structured cabling solutions, including copper-based products, has surged.

Access Full Report @ https://www.databridgemarketresearch.com/reports/us-copper-connectivity-market

Data Bridge market research analyzes that the U.S. Copper Connectivity Market size was valued at USD 4.12 Billion in 2025 and is expected to reach USD 6.18 Billion by 2033, at a CAGR of 5.26% during the forecast period of 2026 to 2033.

Key Findings of the Study

POWER OVER ETHERNET (POE) ADOPTION

The widespread adoption of Power over Ethernet (PoE) technologies, including PoE+, UPOE, and IEEE 802.3bt high power PoE, significantly drives the demand for copper cabling solutions. PoE technology enables the simultaneous delivery of data and power over a single copper cable, making it ideal for powering devices such as security cameras, wireless access points, lighting systems, and various Internet of Things (IoT) devices. As enterprises and organizations increasingly deploy these technologies to streamline infrastructure and reduce costs, the reliance on copper structured cabling grows.

Report Scope and Market Segmentation

|

Report Metric

|

Details

|

|

Forecast Period

|

2026 to 2033

|

|

Base Year

|

2025

|

|

Historic Years

|

2024 (Customizable to 2019-2023)

|

|

Quantitative Units

|

Revenue in USD Billion

|

|

Segments Covered

|

By Product Type (Cables, Connectors & Jacks, Patch Cords, Patch Panels, Cable Management & Pathways, Cross-Connect & Termination Hardware, Faceplates, Boxes & Outlets), Installation Type (Field-Terminated, Pre-Terminated Assemblies), Function (Data Transmission, Power Over Ethernet (PoE/PoE+/UPOE/802.3bt), Cross-Connect And Distribution, Cable Management And Organization, Shielding And EMI/RFI Mitigation, Grounding And Bonding), Application (Data Centers, Enterprise Lan, Commercial & Smart Buildings (BAS, PoE Lighting, Security), Telecom Access & Outside Plant (Copper Last-Mile), Industrial Ethernet & Automation, Residential & SOHO) End User (IT & Telecom, BFSI, Manufacturing, Government & Public Sector, Healthcare, Retail & Hospitality, Education, Energy & Utilities, Transportation & Logistics) Distribution Channel (Direct, Indirect)

|

|

Countries Covered

|

California, Texas, Florida, New York, Pennsylvania, Illinois, Ohio, Georgia, North Carolina, Michigan, New Jersey, Virginia, Washington, Arizona, Tennessee, Massachusetts, Indiana, Maryland, Missouri, Colorado, Wisconsin, Minnesota, South Carolina, Alabama, Kentucky, Louisiana, Oregon, Oklahoma, Connecticut, Utah, Nevada, Iowa, Arkansas, Kansas, Mississippi, New Mexico, Idaho, Nebraska, West Virginia, Hawaii, New Hampshire, Maine, Montana, Rhode Island, Delaware, South Dakota, North Dakota, Alaska, Vermont, Wyoming, District of Columbia

|

|

Market Players Covered

|

|

|

Data Points Covered in the Report

|

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand.

|

Segment Analysis

The U.S. copper connectivity market is segmented into six notable segments which are based on product type, installation type, function, application, end user and distribution channel.

- On the basis of product type, the market is segmented into cables, connectors & jacks, patch cords, patch panels, cable management & pathways, cross-connect & termination hardware, faceplates, boxes & outlets, and others.

In 2026, the cables segment is expected to dominate the market

In 2026 cables segment is expected to dominate the market with a 37.21% market share primarily due to the extensive deployment of copper Ethernet cables such as Cat6, Cat6A, and Cat7 across data centers, enterprise networks, and telecommunications infrastructure.

The patch cords segment is anticipated to witness the fastest CAGR of 5.72% from 2026 to 2033, fueled by increasing network upgrades, rising demand for flexible and modular connectivity solutions, and expansion of edge computing, telecom facilities, and enterprise IT environments.

- On the basis of installation type, the market is segmented into field-terminated, and pre-terminated assemblies.

In 2026, the In field-terminated segment is expected to dominate the market

In 2026 field-terminated segment is expected to dominate the market with a 69.50% market share due to its flexibility, cost-effectiveness, and suitability for customized network deployments. Field termination allows on-site cable cutting, routing, and connector installation, enabling installers to adapt to varying rack layouts, pathway constraints, and evolving infrastructure requirements.

The pre-terminated assemblies segment is projected to witness the highest CAGR of 5.49% during the forecast period of 2026 to 2033. The high growth is mainly driven by increasing AI and GPU-intensive workloads, rising demand for high-density data center deployments, and the need for faster, scalable, and standardized connectivity solutions across multiple facilities.

- On the basis of function, the market is segmented into data transmission, power over ethernet (PoE/PoE+/UPOE/802.3bt), cross-connect and distribution, cable management and organization, shielding and EMI/RFI mitigation, grounding and bonding, and others.

In 2026, the data transmission segment is expected to dominate the market

In 2026 the data transmission segment is expected to dominate the market with a 35.33% market share owing to the widespread use of copper Ethernet cabling for reliable short-to-medium distance data communication across enterprise networks, data centers, and telecom facilities.

The power over ethernet (PoE/PoE+/UPOE/802.3bt) segment is anticipated to witness the fastest CAGR of 5.69% from 2026 to 2033, driven by increasing deployment of IP cameras, wireless access points, VoIP phones, IoT devices, and smart building systems that require both power and data through a single cable.

- On the basis of application, the market is segmented into data centers, enterprise LAN, commercial & smart buildings (BAS, PoE lighting, security), telecom access & outside plant (copper last-mile), industrial ethernet & automation, residential & SOHO, and others.

In 2026, the data centers segment is expected to dominate the market

In 2026 the data centers segment is expected to dominate the market with a 33.49% market share due to the expansion of hyperscale cloud facilities, AI infrastructure deployments, and high-density rack interconnect requirements to support compute-intensive workloads. However, this segment is also projected to witness the highest CAGR of 5.49% during the forecast period of 2026 to 2033. The high growth is mainly driven by rising edge computing deployments, enterprise digital transformation initiatives, and increasing demand for localized data processing.

- On the basis of end user, the market is segmented into IT & Telecom, BFSI, manufacturing, government & public sector, healthcare, retail & hospitality, education, energy & utilities, transportation & logistics, and others.

In 2026, the IT & Telecom segment is expected to dominate the market

In 2026 theIT & Telecom segment is expected to dominate the market with a 34.39% market share due to their high bandwidth requirements, scalability, and compatibility with dense networking and server deployments. Copper cabling solutions remain crucial for short-reach connectivity within hyperscale and colocation facilities, supporting structured cabling standards, PoE applications, and reliable network access.

This segment is also anticipated to witness the fastest CAGR of 6.08% from 2026 to 2033, fueled by edge computing deployments, remote offices, telecom hubs, and distributed retail or industrial sites where fiber may not be cost-effective or practical for short-range connectivity.

- On the basis of distribution channel, the market is segmented into direct and indirect.

In 2026, the indirect segment is expected to dominate the market

In 2026 the indirect segment is expected to dominate the market with a 58.68% market share due to its ease of procurement, lower upfront costs, and suitability for moderate-density network deployments. Copper cabling and connectivity solutions offered through distributors, resellers, and system integrators are widely adopted by enterprises, SMBs, and legacy data centers.

Major Players

CommScope (U.S.), Corning Incorporated (U.S.), TE Connectivity (Switzerland), Amphenol Corporation (U.S.), Schneider Electric (France), Southwire Company, LLC (U.S.), Belden Inc. (U.S.), AFL (U.S.), Hubbell Incorporated (U.S.), Black Box (U.S.), Panduit Corp. (U.S.), Legrand (France), Eaton (Ireland), Prysmian (Italy), Nexans (France), Superior Essex International Inc. (U.S.), Leviton Manufacturing Co., Inc. (U.S.), Molex (U.S.), HARTING Technology Group (Germany), Windy City Wire (U.S.), The Siemon Company (U.S.), R&M (REICHLE & DE-MASSARI) (Switzerland), Platinum Tools (U.S.), American Cable Assemblies, Inc. (U.S.), Proterial Cable America, Inc. (U.S.), General Wires Inc. (U.S.) among others.

Market Developments

- In March 2023, Corning Inc. has been awarded formal certification to the ISO 45001:2018 standard for its occupational health and safety management system, as documented in the recently issued certificate signed by the certification body Bureau Veritas. This internationally recognized standard sets out requirements for managing workplace health and safety risks and improving the protection of employees and others involved in the company’s operations. Achieving ISO 45001 certification shows that Corning has implemented a structured and systematic approach to identifying and controlling hazards, complying with relevant regulations, and continually enhancing safety performance across multiple sites involved in the design, manufacture, sales, and support of optical communications products and accessories.

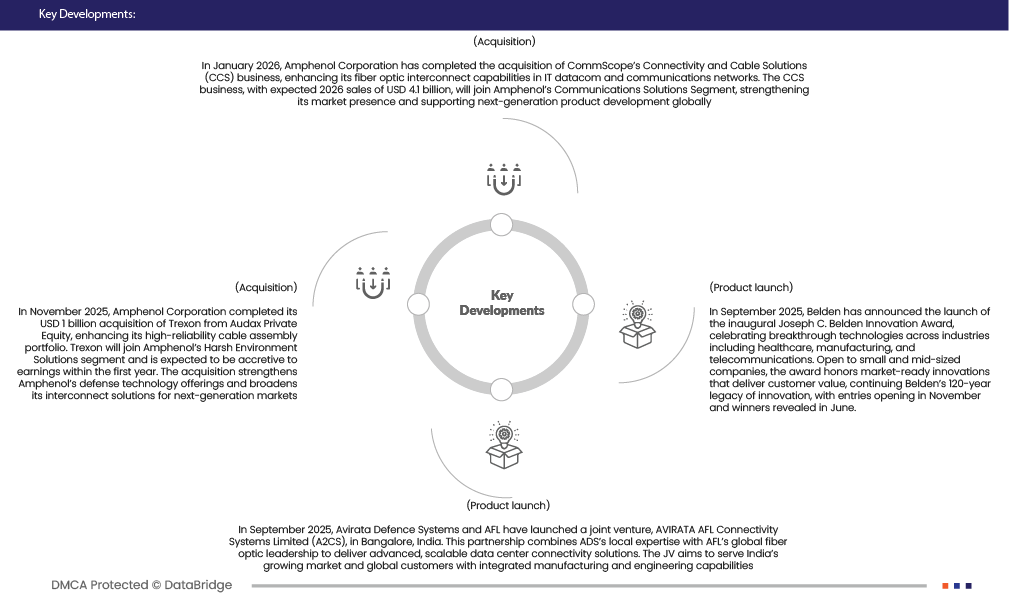

- In January 2026, Amphenol Corporation has completed the acquisition of CommScope’s Connectivity and Cable Solutions (CCS) business, enhancing its fiber optic interconnect capabilities in IT datacom and communications networks. The CCS business, with expected 2026 sales of USD 4.1 billion, will join Amphenol’s Communications Solutions Segment, strengthening its market presence and supporting next-generation product development globally.

- In November 2025, Amphenol Corporation completed its USD 1 billion acquisition of Trexon from Audax Private Equity, enhancing its high-reliability cable assembly portfolio. Trexon will join Amphenol’s Harsh Environment Solutions segment and is expected to be accretive to earnings within the first year. The acquisition strengthens Amphenol’s defense technology offerings and broadens its interconnect solutions for next-generation markets.

- In September 2025, Avirata Defence Systems and AFL have launched a joint venture, AVIRATA AFL Connectivity Systems Limited (A2CS), in Bangalore, India. This partnership combines ADS’s local expertise with AFL’s global fiber optic leadership to deliver advanced, scalable data center connectivity solutions. The JV aims to serve India’s growing market and global customers with integrated manufacturing and engineering capabilities.

- In September 2025, Belden has announced the launch of the inaugural Joseph C. Belden Innovation Award, celebrating breakthrough technologies across industries including healthcare, manufacturing, and telecommunications. Open to small and mid-sized companies, the award honors market-ready innovations that deliver customer value, continuing Belden’s 120-year legacy of innovation, with entries opening in November and winners revealed in June.

As per Data Bridge Market Research analysis:

California holds a strong dominant position in the U.S. copper connectivity market, accounting for the highest market share of 10.76% and is projected to grow at a robust CAGR of 6.17% during the forecast period. The state’s high concentration of cloud data centers, enterprise campuses, and colocation facilities drives strong demand for copper cabling and structured connectivity solutions. California’s well-established IT infrastructure, low-latency network access, and dense enterprise networks make it a preferred location for short-reach copper deployments, PoE-enabled networks, and modular structured cabling, supporting continued market leadership in both hyperscale and enterprise segments.

Texas is anticipated to show the fastest growth during the forecast period. Is driven by strong demand from expanding data centers, telecom infrastructure, and energy projects across the state. Growth in 5G deployment, industrial automation, and power grid upgrades increases the need for reliable copper cabling and connectors. Additionally, Texas’ rapidly growing construction and manufacturing sectors further support market expansion.

For more detailed information about the U.S. copper connectivity market report, click here – https://www.databridgemarketresearch.com/reports/us-copper-connectivity-market