The growing adoption of liquid-cooling-compatible rack systems is being driven by the rapid expansion of high-density computing environments, particularly those supporting AI, machine learning, and hyperscale cloud workloads. Traditional air-cooling methods are increasingly insufficient for managing the heat generated by advanced processors and GPUs operating at higher power densities. As a result, data center operators are shifting toward liquid cooling technologies such as direct-to-chip and immersion cooling, which offer superior thermal efficiency, reduced energy consumption, and improved performance stability. To support these technologies, rack systems are being redesigned with enhanced structural strength, leak detection systems, integrated coolant distribution units (CDUs), and optimized cable and airflow management.

Liquid-cooling-compatible racks also enable higher rack power densities, often exceeding 30–50 kW per rack, which is critical for next-generation AI servers. This transition not only improves energy efficiency and sustainability but also reduces the overall data center footprint, making liquid-ready rack systems a key trend shaping modern data center infrastructure development.

Access Full Report @ https://www.databridgemarketresearch.com/reports/us-data-center-rack-market

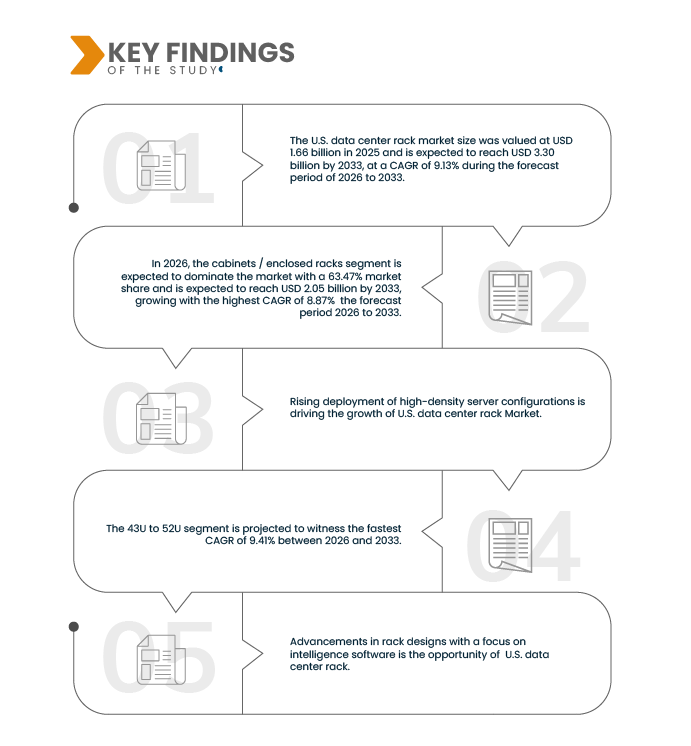

Data Bridge market research analyzes that the U.S. Data Center Rack Market size was valued at USD 1.66 billion in 2025 and is expected to reach USD 3.30 billion by 2033, at a CAGR of 9.13% during the forecast period of 2026 to 2033.

Key Findings of the Study

Rising deployment of high-density server configurations

The rising deployment of high-density server configurations is primarily driven by the rapid growth of data-intensive technologies such as artificial intelligence (AI), machine learning, cloud computing, big data analytics, and edge computing. Modern processors and GPUs deliver significantly higher performance but also consume more power, leading to increased rack power densities that often exceed 20–50 kW per rack. Enterprises and hyperscale data center operators are consolidating workloads into fewer, more powerful servers to maximize computational output within limited physical space. This shift enables improved space utilization, lower latency, and better scalability to handle growing digital demands. However, high-density configurations also generate substantial heat, creating challenges related to thermal management, power distribution, and infrastructure reliability. As a result, operators are upgrading power systems, advanced cooling solutions, and intelligent monitoring technologies to ensure operational efficiency and minimize downtime. The trend toward high-density server deployments reflects the broader transformation of data centers into highly efficient, performance-optimized facilities capable of supporting next-generation digital ecosystems.

Report Scope and Market Segmentation

|

Report Metric

|

Details

|

|

Forecast Period

|

2026 to 2033

|

|

Base Year

|

2025

|

|

Historic Years

|

2018-2024 (Customizable to 2013-2017)

|

|

Quantitative Units

|

Revenue in USD billion

|

|

Segments Covered

|

By Rack Type (Cabinets / Enclosed Racks, Open Frame Racks), Rack Height (43U to 52U, 42U Below, Above 52U), Rack Width (19 Inch, 23 Inch, Others), Data Center Size (Large Data Centers, Small and Mid-Sized Data Centers), Form Factor (Floor-Standing, Wall-Mounted), Cooling Options (Passive Ventilation, Active Cooling), Material (Steel, Aluminum, Composite), End User (IT and Telecom, Banking, Financial Services, And Insurance (BFSI), Government and Defense, Retail, Manufacturing, Healthcare, Energy and Utilities, Others), Sales Channel (Indirect, Direct)

|

|

Countries Covered

|

U.S.

|

|

Market Players Covered

|

|

|

Data Points Covered in the Report

|

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand.

|

Segment Analysis

The U.S. data center rack market is segmented into nine notable segments based on the rack type, rack height, rack width, data center size, form factor, cooling options, material, end user, sales channel.

- On the basis of rack type is segmented into cabinets / enclosed racks and open frame racks.

In 2026 cabinets / enclosed racks segment is expected to dominate the market

In 2026 cabinets / enclosed racks segment is expected to dominate the U.S. data center rack market with 63.47% share due to its superior security, structured cable management, enhanced airflow control, and compatibility with high-density server environments. Enclosed cabinets provide better protection for critical IT equipment, improved thermal efficiency, and noise reduction compared to open frame racks. With increasing deployment of hyperscale and colocation facilities across the U.S., demand for scalable, secure, and high-load supporting rack infrastructure is rising, strengthening the dominance of cabinets and enclosed rack systems nationwide.

- On the basis of rack height, market is segmented into 43U to 52U, 42U and below, and above 52U.

In 2026, the 43U to 52U segment is expected to dominate the market

In 2026, the 43U to 52U segment is expected to dominate the U.S. data center rack market with 58.44% share due to its optimal balance between space efficiency and equipment density. This height range supports higher server consolidation without exceeding structural or cooling limitations. It is widely preferred in hyperscale and enterprise data centers where maximizing floor space and improving rack-level power distribution are critical. Additionally, it accommodates modern high-density servers and networking equipment, making it a practical and cost-effective choice for expanding and upgrading facilities.

- On the basis of rack width, the market is segmented into 19-inch, 23 inches, others.

In 2026, the 19-inch segment is anticipated to dominate the market

In 2026, the 19-inch segment is anticipated to dominate the U.S. data center rack market with 83.32% share due to the universal industry acceptance and compatibility with most IT and networking equipment. The 19-inch standard has become the benchmark configuration for servers, switches, and storage devices, ensuring interoperability and simplified procurement. Its widespread adoption reduces customization costs and enhances scalability across facilities. Additionally, standardized dimensions support efficient cable management and airflow design, making 19-inch racks the preferred choice for hyperscale, colocation, and enterprise data centers nationwide.

- On the basis of data center size, the market is segmented into large data centers, small and mid-sized data centers.

In 2026, the large data centers segment is anticipated to dominate the market

In 2026, the large data centers segment is anticipated to dominate the U.S. data center rack market with 60.00% share due to substantial investments in hyperscale and colocation facilities. Growing cloud computing, artificial intelligence workloads, and digital transformation initiatives are driving large-scale infrastructure expansion. These facilities require significant volumes of racks to support high server density and scalable architecture. Major technology firms and cloud service providers continue to expand capacity across key states, increasing demand for standardized, high-performance rack solutions in large data center environments nationwide.

- On the basis of form factor, the market is segmented into floor-standing, wall-mounted.

In 2026, the floor-standing segment is anticipated to dominate the market

In 2026, the floor-standing segment is anticipated to dominate the U.S. data center rack market with 77.89% share due to its suitability for large-scale deployments and high load-bearing capacity. Floor-standing racks support heavier equipment, higher rack heights, and improved structural stability compared to wall-mounted options. They are widely used in hyperscale, enterprise, and colocation facilities where scalability and durability are critical. Additionally, floor-standing designs allow better cable routing and airflow management, making them the preferred configuration for modern high-density data center environments.

- On the basis of cooling options, the market is segmented into passive ventilation, active cooling.

In 2026, the passive ventilation segment is anticipated to dominate the market

In 2026, the passive ventilation segment is anticipated to dominate the U.S. data center rack market with 65.99% share due its cost-effectiveness and energy efficiency. Passive cooling designs rely on optimized airflow patterns and perforated doors to manage heat dissipation without additional power consumption. Many modern data centers integrate advanced facility-level cooling systems, reducing the need for rack-level active cooling components. This approach lowers operational costs, simplifies maintenance, and supports sustainability initiatives, making passive ventilation a preferred option for large-scale deployments nationwide.

- On the basis of material, the market is segmented into steel, aluminum, and composite.

In 2026, the steel segment is anticipated to dominate the market

In 2026, the steel segment is anticipated to dominate the U.S. data center rack market with 71.58% share due its superior strength, durability, and load-bearing capacity. Steel racks provide enhanced structural integrity for supporting high-density servers and heavy networking equipment. They also offer improved resistance to wear, vibration, and long-term operational stress. Compared to aluminum and composite materials, steel is more cost-effective and widely available, making it the preferred material for hyperscale, enterprise, and colocation data centers requiring reliable and robust infrastructure solutions

- On the basis of end user, the market is segmented into IT and telecom, banking, financial services, and insurance (BFSI), government and defense, retail, manufacturing, healthcare, energy and utilities, and others.

In 2026, the IT and telecom segment is anticipated to dominate the market

In 2026, the IT and telecom segment is anticipated to dominate the U.S. data center rack market with 36.30% share due continuous expansion of cloud services, 5G networks, edge computing, and data traffic growth. Telecommunications providers and technology companies are investing heavily in new data center facilities and infrastructure upgrades to support digital services and connectivity demands. These developments require large volumes of standardized, high-capacity racks. The rapid evolution of digital platforms and communication networks further strengthens demand from the IT and telecom sector nationwide

- On the basis of sales channel, the market is segmented into indirect, and direct.

In 2026, the indirect segment is anticipated to dominate the market

In 2026, the indirect segment is anticipated to dominate the U.S. data center rack market with 68.24% share due the extensive reach of company websites and e-commerce platforms. Indirect channels enable manufacturers to access a broader customer base, including small and mid-sized enterprises, through streamlined procurement processes. Online platforms offer product comparisons, customization options, and faster delivery timelines. Additionally, digital sales channels reduce overhead costs and improve supply chain efficiency, making indirect distribution an increasingly preferred route for rack procurement across the country

Major Players

Schneider Electric (France), Vertiv Group Corp. (U.S.), Eaton Corporation (Ireland), Rittal Pvt. Ltd. (Germany), Hewlett Packard Enterprise Development LP (U.S.)

Market Developments

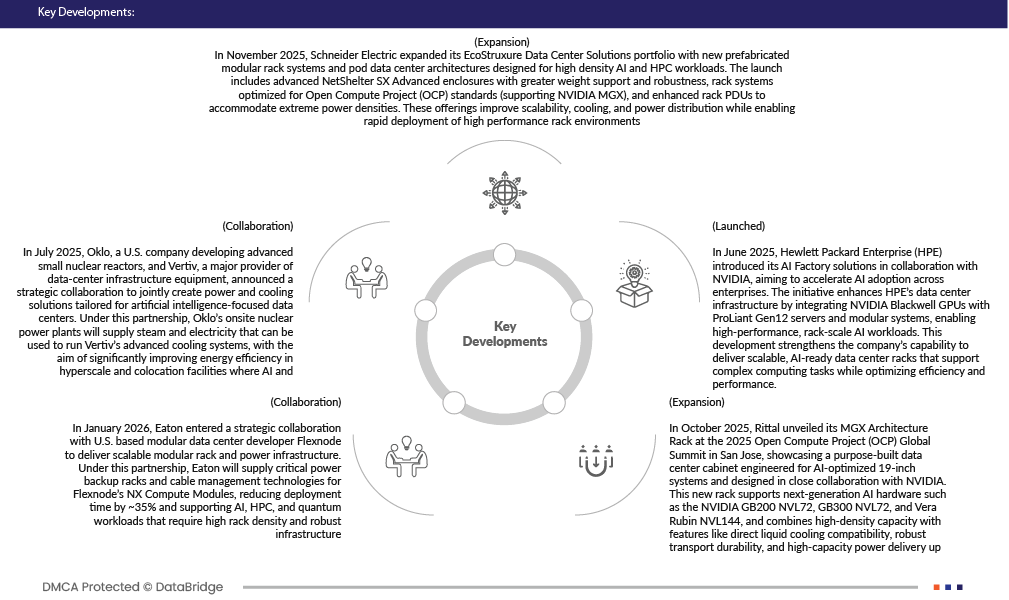

- In November 2025, Schneider Electric expanded its EcoStruxure Data Center Solutions portfolio with new prefabricated modular rack systems and pod data center architectures designed for high density AI and HPC workloads. The launch includes advanced NetShelter SX Advanced enclosures with greater weight support and robustness, rack systems optimized for Open Compute Project (OCP) standards (supporting NVIDIA MGX), and enhanced rack PDUs to accommodate extreme power densities. These offerings improve scalability, cooling, and power distribution while enabling rapid deployment of high-performance rack environments.

- In July 2025, Oklo, a U.S. company developing advanced small nuclear reactors, and Vertiv, a major provider of data-center infrastructure equipment, announced a strategic collaboration to jointly create power and cooling solutions tailored for artificial intelligence-focused data centers. Under this partnership, Oklo’s onsite nuclear power plants will supply steam and electricity that can be used to run Vertiv’s advanced cooling systems, with the aim of significantly improving energy efficiency in hyperscale and colocation facilities where AI and high-performance computing workloads are growing rapidly.

- In January 2026, Eaton entered a strategic collaboration with U.S. based modular data center developer Flexnode to deliver scalable modular rack and power infrastructure. Under this partnership, Eaton will supply critical power backup racks and cable management technologies for Flexnode’s NX Compute Modules, reducing deployment time by ~35% and supporting AI, HPC, and quantum workloads that require high rack density and robust infrastructure.

- In October 2025, Rittal unveiled its MGX Architecture Rack at the 2025 Open Compute Project (OCP) Global Summit in San Jose, showcasing a purpose‑built data center cabinet engineered for AI‑optimized 19‑inch systems and designed in close collaboration with NVIDIA. This new rack supports next‑generation AI hardware such as the NVIDIA GB200 NVL72, GB300 NVL72, and Vera Rubin NVL144, and combines high‑density capacity with features like direct liquid cooling compatibility, robust transport durability, and high‑capacity power delivery up to 1,400 A to meet the demanding thermal and electrical requirements of modern AI workloads.

- In June 2025, Hewlett Packard Enterprise (HPE) introduced its AI Factory solutions in collaboration with NVIDIA, aiming to accelerate AI adoption across enterprises. The initiative enhances HPE’s data center infrastructure by integrating NVIDIA Blackwell GPUs with ProLiant Gen12 servers and modular systems, enabling high-performance, rack-scale AI workloads. This development strengthens the company’s capability to deliver scalable, AI-ready data center racks that support complex computing tasks while optimizing efficiency and performance.

As per Data Bridge Market Research analysis:

For more detailed information about the U.S. data center rack market report, click here – https://www.databridgemarketresearch.com/reports/us-data-center-rack-market