The rapid expansion of cloud computing and hyperscale data centers is a major driver of the U.S. data center structured cabling market. As businesses increasingly depend on cloud services for storage, computing power, AI workloads, and application delivery, demand for large-scale, high-performance data centers continues to rise. Hyperscale facilities designed to support robust, scalable cloud environments—require highly efficient and reliable cabling systems to ensure high-speed data transmission, ultra-low latency, and minimal downtime.

Structured cabling plays a critical role in these environments by organizing and standardizing network infrastructure to support scalability, flexibility, and future upgrades. Traditional point-to-point cabling is inefficient and difficult to manage in hyperscale settings due to extreme density and performance requirements. Instead, advanced structured cabling solutions enable fiber-dense architectures, spine-and-leaf network designs, and support for 400G and 800G Ethernet deployments.

The shift toward cloud-based infrastructure is accelerating investments in high-performance fiber optic and enhanced copper cabling systems, along with intelligent cable management solutions. Structured cabling also improves airflow management, simplifies maintenance, and allows rapid reconfiguration to accommodate fluctuating cloud demand.

Public cloud and hyperscale expansion is projected to contribute approximately 7%–10% CAGR growth to the U.S. structured cabling market, driven by continuous data center capacity additions. As digital transformation advances across AI, IoT, fintech, and streaming industries, hyperscale development will remain strong, fueling sustained capital expenditure in structured cabling. Overall, cloud and hyperscale growth represents a long-term, compounding demand driver for the U.S. structured cabling market.

Access Full Report @ https://www.databridgemarketresearch.com/reports/us-data-centre-structured-cabling-market

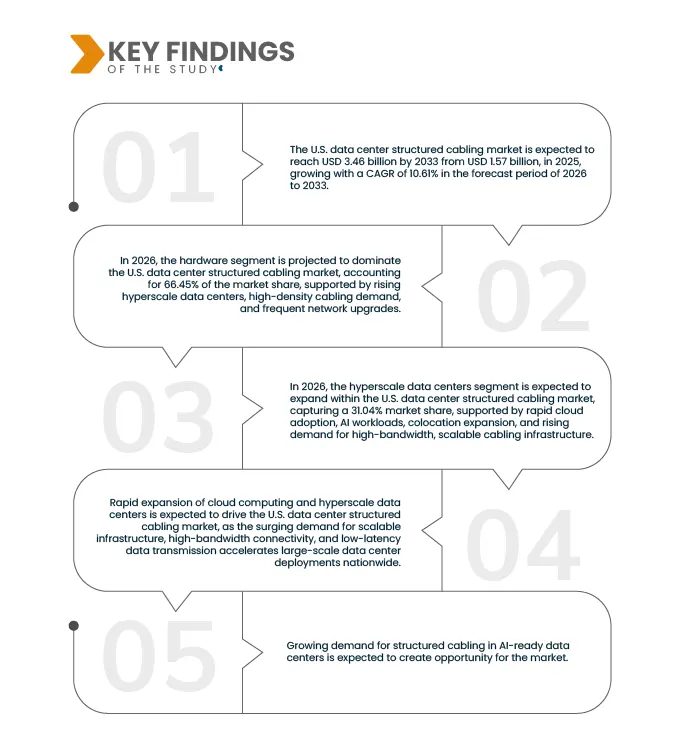

Data Bridge market research analyzes that the U.S. Data Center Structure Cabling Market is expected to reach USD 3.45 billion by 2033 from USD 1.57 billion in 2025, growing with a substantial CAGR of 10.61% in the forecast period of 2026 to 2033.

Key Findings of the Study

Rising Demand for Low-Latency and High-Bandwidth Networks

Rising demand for low-latency, high-bandwidth networks is a major driver of the U.S. data center structured cabling market. As data-intensive applications such as cloud computing, artificial intelligence (AI), real-time analytics, video streaming, high-performance computing (HPC), and edge computing expand, data centers must handle massive volumes of east-west traffic with minimal delay. Performance expectations now require ultra-fast data transmission, near-zero latency, and uninterrupted connectivity.

Structured cabling systems—particularly high-capacity fiber-optic solutions are essential to meeting these requirements. Advanced fiber infrastructures, including singlemode and multimode fiber, support 100G, 400G, and emerging 800G speeds, enabling AI workloads, hyperscale cloud environments, and latency-sensitive applications. Compared to traditional copper-based systems, fiber-optic cabling offers higher bandwidth capacity, reduced signal degradation, lower electromagnetic interference, and improved reliability in always-on digital environments.

Standardized structured cabling also enhances scalability and flexibility. It allows operators to increase fiber density per rack, optimize airflow, reduce congestion, and simplify maintenance and upgrades. Modular and intelligent cable management solutions further support rapid scale-out capabilities, helping data centers adapt quickly to fluctuating workload demands.

Overall, the need for low-latency and high-bandwidth connectivity is not only expanding market size but also transforming technology standards and value propositions. Structured cabling has evolved from a passive infrastructure component into a strategic enabler of next-generation digital ecosystems, strengthening its role as a critical pillar of the U.S. data economy.

Report Scope and Market Segmentation

|

Report Metric

|

Details

|

|

Forecast Period

|

2026 to 2033

|

|

Base Year

|

2025

|

|

Historic Years

|

2018-2024 (Customizable)

|

|

Quantitative Units

|

Revenue in USD Billion

|

|

Segments Covered

|

By Offering (Hardware, Services, and Software), Data Center Type (Enterprise Data Centers, Colocation Data Centers, Hyperscale Data Centers, and Edge Data Centers), Color Coding (Aqua, Yellow, Blue, Red, Black, and Others), Architecture (Top‑of‑Rack (T0R), Middle‑of‑Row (MOR), End‑of‑Row (EOR), and Centralized Cabling), Application (Networking, Power Distribution, Security System, Cooling System Support, and Others), Type (Horizontal Cabling and Backbone Cabling), Infrastructure Support (Racks & Pathways and Labeling & Documentation), Distribution Areas (Equipment Distribution Area (EDA), Horizontal Distribution Area (HDA), Main Distribution Area (MDA), and Entrance Room), Installation Type (New Installation and Retrofit), End User (IT & Telecommunication, BFSI, Government & Education, Healthcare, Retail & E‑commerce, Energy & Power, Media & Entertainment, Oil & Gas, Residential, and Others)

|

|

Countries Covered

|

U.S.

|

|

Market Players Covered

|

|

|

Data Points Covered in the Report

|

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand.

|

Segment Analysis

The U.S. data center structured cabling market is segmented into ten notable segments based on the offering, data centre type, color coding, architecture, application, type, infrastructure support, distribution areas, installation type, end user.

- On the basis of offering, the market is segmented into hardware, software, and services.

In 2026, the Hardware segment is expected to dominate the market

In 2026, the hardware segment is projected to dominate the U.S. data center structured cabling market with the largest market share of 66.45%, due to strong demand for cables, connectors, patch panels, and racks driven by data center expansion, network upgrades, higher bandwidth requirements, and increased deployment of high-density infrastructure.

- On the basis of data center type, the market is segmented into enterprise data centers, colocation data centers, hyperscale data centers, and edge data centers.

In 2026, the hyperscale data centers segment is expected to dominate the market

In 2026, the hyperscale data centers segment is projected to dominate the market with a market share of 31.04%, due to rapid cloud adoption, growing AI and big data workloads, large-scale infrastructure investments by hyperscale operators, and increasing need for scalable, high-performance, and cost-efficient structured cabling systems.

- On the basis of color coding, the market is segmented into aqua, yellow, blue, red, black, and others.

In 2026, the aqua segment is expected to dominate the market

In 2026, the aqua segment is projected to dominate the market with a share of 37.88%, driven by its widespread adoption for multimode fiber applications, improved visual identification, compliance with industry standards, enhanced network management efficiency, and increasing deployment of high-speed optical fiber cabling in modern data centers.

- On the basis of architecture, the market is segmented into top‑of‑rack (ToR), middle‑of‑row (MoR), end‑of‑row (EoR), and centralized cabling.

In 2026, the top‑of‑rack (ToR) segment is expected to dominate the market

In 2026, the top‑of‑rack (ToR) segment is projected to dominate the market with the largest market share of 41.90%, owing to the reduced cable lengths, lower latency, improved airflow management, simplified scalability, enhanced energy efficiency, and its suitability for high-density server environments in hyperscale and colocation data centers.

- On the basis of application, the market is segmented into networking, power distribution, security system, cooling system support, and others.

In 2026, the networking segment is expected to dominate the market

In 2026, the networking segment is projected to dominate the market with the largest market share of 53.75%, owing to the increasing data traffic, rising demand for high-speed connectivity, expansion of cloud services, deployment of advanced Ethernet technologies, and continuous upgrades to support low-latency and high-bandwidth network infrastructure.

- On the basis of type, the market is segmented into horizontal cabling and backbone cabling.

In 2026, the horizontal cabling segment is expected to dominate the market

In 2026, the horizontal cabling segment is projected to dominate the market with the largest market share of 62.54%, owing to its extensive use in connecting equipment to distribution areas, ease of installation, flexibility, cost-effectiveness, and growing deployment across enterprise, colocation, and hyperscale data center facilities.

- On the basis of infrastructure support, the market is segmented into racks & pathways and labeling & documentation.

In 2026, the racks & pathways segment is expected to dominate the market

In 2026, the acks & pathways segment is projected to dominate the market with a market share of 72.96%, due to increasing need for organized cable management, support for high-density installations, improved airflow and cooling efficiency, scalability, and rising investments in modern data center infrastructure design and optimization.

- On the basis of distribution areas, the market is segmented into equipment distribution area (EDA), horizontal distribution area (HDA), main distribution area (MDA), and entrance room.

In 2026, the equipment distribution area (EDA) segment is expected to dominate the market

In 2026, the equipment distribution area (EDA) segment is projected to dominate the market with a share of 41.36%, driven by its critical role in connecting servers and network equipment, rising server density, growing deployment of ToR architectures, and increased demand for efficient, high-performance cabling at the rack level.

- On the basis of installation type, the market is segmented into new installation and retrofit.

In 2026, the new installation segment is expected to dominate the market

In 2026, the new installation segment is projected to dominate the market with a market share of 60.73%, due to increasing construction of hyperscale and colocation data centers, rising cloud investments, expansion of digital infrastructure, and growing demand for advanced structured cabling solutions in newly built facilities.

- On the basis of end user, the market is segmented into IT & telecommunication, BFSI, government & education, healthcare, retail & e‑commerce, energy & power, media & entertainment, oil & gas, residential, and others.

In 2026, the IT & telecommunication segment is expected to dominate the market

In 2026, the IT & telecommunication segment is projected to dominate the market with a market share of 40.11%, due to rapid growth in data traffic, expanding cloud computing adoption, nationwide 5G network rollouts, rising demand for low-latency and high-bandwidth connectivity, increasing digitalization across industries, and continuous investments in upgrading, expanding, and modernizing data center infrastructure throughout the U.S.

Major Players

Belden, Inc. (U.S.), CommScope (U.S.), Corning Incorporated (U.S.), Nexans (France), Panduit (U.S.), Legrand (France), and among others.

Latest Developments in U.S. Data Center Structured Cabling Market

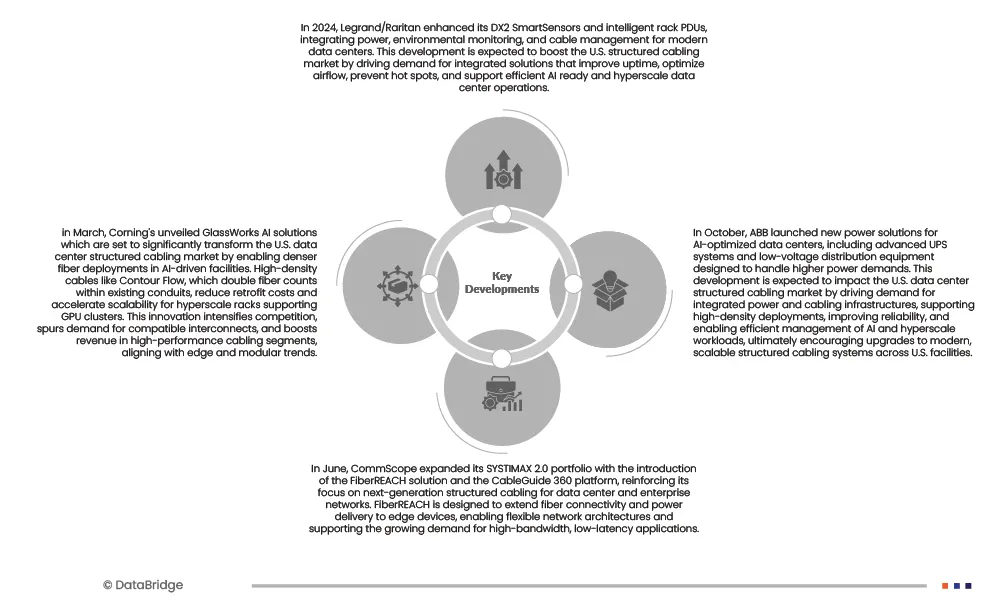

- In October 2025, ABB announced a collaboration with NVIDIA to develop next generation AI data centers featuring 800 VDC power architectures, enabling high-efficiency, scalable power delivery for megawatt-scale racks. This initiative is expected to influence the U.S. data center structured cabling market by driving demand for cabling solutions that integrate with high-voltage DC systems, supporting denser rack deployments, improving energy efficiency, and facilitating the design of future-proof infrastructures for AI and hyperscale workloads.

- In June, CommScope expanded its SYSTIMAX 2.0 portfolio with the introduction of the FiberREACH solution and the CableGuide 360 platform, reinforcing its focus on next-generation structured cabling for data center and enterprise networks. FiberREACH is designed to extend fiber connectivity and power delivery to edge devices, enabling flexible network architectures and supporting the growing demand for high-bandwidth, low-latency applications.

- In April 2025, TERACAI, part of the CXtec ecosystem, formalized an authorized partnership with Juniper Networks, strengthening its ability to integrate Juniper’s networking platforms into enterprise environments—many of which rely on robust structured cabling infrastructure. This partnership is expected to impact the U.S. data center structured cabling market by increasing demand for coordinated cabling and networking rollouts, improving interoperability between physical connectivity and networking systems, and accelerating deployments that support high-performance, scalable data center and campus networks.

- In March 2024, FS has announced an expanded collaboration with US Conec to deliver advanced high-density interconnect solutions for data centers and enterprise networks. The partnership introduces the MMC connector, combining a reduced-size MT-style ferrule (TMT) with a very small form factor (VSFF) connector, offering low insertion loss and ultra-high-density performance. As high-performance computing (HPC) and machine learning (ML) drive exponential data growth, this collaboration enables clients to deploy efficient 400G/800G optical link architectures and scalable fiber networks. By leveraging US Conec’s expertise and FS’ global reach, customers benefit from cutting-edge connectivity, improved network efficiency, and future-ready high-performance fiber infrastructure.

Regional Analysis:

Geographically, the states covered in the U.S. data center structured cabling market report are Virginia, Texas, California, Arizona, Georgia, Illinois, Ohio, Oregon, Washington, Iowa, Nevada, New York, Florida, North Carolina, Nebraska, Utah, New Jersey, Pennsylvania, Minnesota, Tennessee, Indiana, Colorado, Massachusetts, Missouri, Maryland, Wisconsin, Michigan, Wyoming, New Mexico, Oklahoma, Alabama, Kentucky, South Carolina, Kansas, Connecticut, Louisiana, Idaho, Montana, Arkansas, Delaware, New Hampshire, South Dakota, Mississippi, Rhode Island, West Virginia, Maine, Hawaii, District Of Columbia, Alaska, North Dakota, and Vermont.

As per Data Bridge Market Research analysis:

Virginia is the dominant and fastest growing state in the U.S. data center structured cabling market during the forecast period of 2026 to 2033

Virginia is expected to dominate the market due to concentration of hyperscale data centers, particularly in Northern Virginia, the world’s largest data center hub. Strong cloud provider presence, robust fiber connectivity, favorable tax incentives, reliable power infrastructure, and continuous capacity expansion drive sustained investments in advanced structured cabling solutions across the state.

Moreover, Virginia is projected to register the highest CAGR during the forecast period of 2026 to 2033 owing to continued hyperscale expansions, rising AI and cloud investments, strong colocation demand, expanding fiber networks, and supportive state policies. Ongoing large-scale capacity additions and power infrastructure development further accelerate structured cabling deployments across new and existing data center facilities.

For more detailed information about the U.S. data center structured cabling market report, click here – https://www.databridgemarketresearch.com/reports/us-data-centre-structured-cabling-market