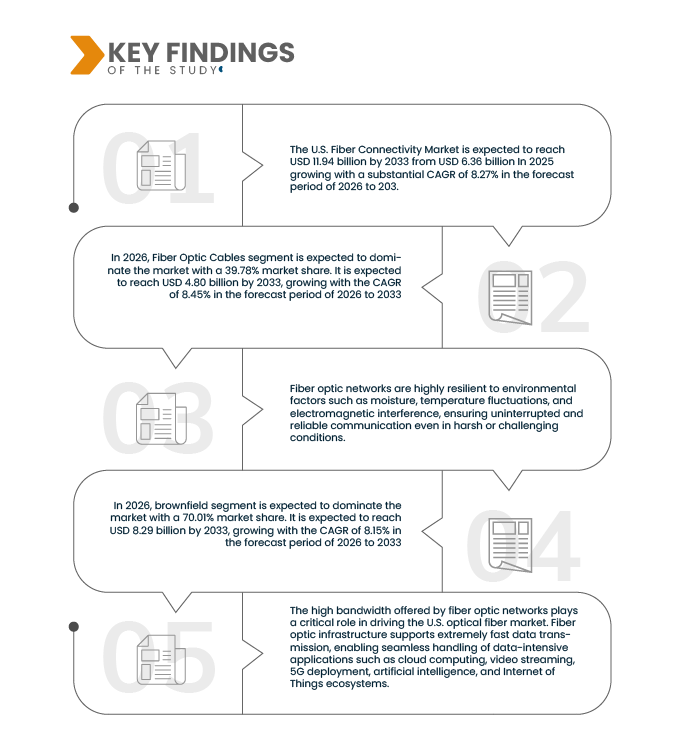

Fiber optic networks are highly resilient to environmental factors such as moisture, temperature fluctuations, and electromagnetic interference, ensuring uninterrupted and reliable communication even in harsh or challenging conditions. This robustness makes fiber optics particularly suitable for critical infrastructure, including energy grids, transportation systems, industrial facilities, and emergency response networks, where consistent connectivity is essential for operational efficiency. Unlike traditional copper cables, which are prone to signal degradation and outages under adverse conditions, fiber maintains stable performance and high-speed data transmission, supporting real-time monitoring, remote operations, and large-scale data transfers. The inherent durability and reliability of fiber networks also reduce maintenance costs and minimize downtime, enhancing overall network resilience. This ability to deliver consistent, interference-free connectivity under all conditions acts as a strong driver for the growth of the market.

Access Full Report @ https://www.databridgemarketresearch.com/reports/us-fiber-connectivity-market

The U.S. Fiber Connectivity Market is expected to reach USD 11.94 billion by 2033 from USD 6.36 billion In 2025 growing with a substantial CAGR of 8.27% in the forecast period of 2026 to 2033.

Key Findings of the Study

High Bandwidth Offered By Fiber Optic Networks

The high bandwidth offered by fiber optic networks plays a critical role in driving the U.S. optical fiber market. Fiber optic infrastructure supports extremely fast data transmission, enabling seamless handling of data-intensive applications such as cloud computing, video streaming, 5G deployment, artificial intelligence, and Internet of Things ecosystems. Compared to traditional copper networks, fiber delivers greater capacity, lower latency, and higher reliability, which aligns with rising consumer and enterprise demand for uninterrupted high-speed connectivity. Telecommunications operators and enterprises increasingly prioritize fiber deployment to support expanding digital traffic and future-ready communication systems. As digital transformation accelerates across industries, the demand for high-bandwidth infrastructure continues to rise. This superior bandwidth capability directly acts as a major driver for the growth of the market.

Report Scope and Market Segmentation

|

Report Metric

|

Details

|

|

Forecast Period

|

2026 to 2033

|

|

Base Year

|

2025

|

|

Historic Years

|

2018-2024 (Customizable to 2013-2017)

|

|

Quantitative Units

|

Revenue in USD Million

|

|

Segments Covered

|

By Component (Fiber Optic Cables, Transceivers, Connectors, Splitters, Enclosures & Panels, and Others), Network Type (FTTx (FTTH, FTTB, FTTC), Metro Networks, 5G Backhaul, Data Center Interconnect (DCI), Long-Haul Networks, Access Networks (Non-FTTx enterprise/local access), Enterprise / LAN Fiber, Others), Deployment Mode (Brownfield, and Greenfield), Application (Telecommunication, Data Centers, Enterprise & Institutional, Industrial, and Others) End User (Telecom Operators (AT&T, Verizon, Lumen, Frontier, Windstream), Internet Service Providers (ISPs), Cable Multisystem Operators (Comcast, Charter, Cox), Hyperscale Data Center Providers (AWS, Azure, Google, Meta), Enterprises, Government & Municipal Entities, Utilities, and Others) Distribution Channel (Direct, Indirect)

|

|

Countries Covered

|

California, Texas, Florida, New York, Pennsylvania, Illinois, Ohio, Georgia, North Carolina, Michigan, New Jersey, Virginia, Washington, Arizona, Tennessee, Massachusetts, Indiana, Maryland, Missouri, Colorado, Wisconsin, Minnesota, South Carolina, Alabama, Kentucky, Louisiana, Oregon, Oklahoma, Connecticut, Utah, Nevada, Iowa, Arkansas, Kansas, Mississippi, New Mexico, Idaho, Nebraska, West Virginia, Hawaii, New Hampshire, Maine, Montana, Rhode Island, Delaware, South Dakota, North Dakota, Alaska, Vermont, Wyoming, District of Columbia

|

|

Market Players Covered

|

|

|

Data Points Covered in the Report

|

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand.

|

Segment Analysis

U.S. Fiber Connectivity market is categorized into six notable segments which are based on component, network type, deployment mode, application, end user, and distribution channel.

- On the basis of component, the market is segmented into fiber optic cables, transceivers, connectors, splitters, enclosures & panels, and others.

In 2026, Fiber Optic Cables segment is expected to dominate the market

In 2026, Fiber Optic Cables segment is expected to dominate due to sustained broadband expansion, large-scale fiber-to-the-home (FTTH) deployments, and rapid data center interconnection growth. Increasing 5G backhaul requirements and government-supported rural infrastructure projects are accelerating underground, aerial, and submarine cable installations. Single-mode fiber continues to lead demand for long-distance and high-bandwidth applications, while multimode supports enterprise and campus networks. Additionally, rising investments in hyperscale facilities and metro network upgrades are driving large-volume cable procurement, positioning fiber optic cables as the foundational and highest-value component across connectivity infrastructure projects.

- On the basis of network type, the market is segmented into FTTx (FTTH, FTTB, FTTC), metro networks, 5G backhaul, data center interconnect (DCI), long-haul networks, access networks (non-FTTx enterprise/local access), enterprise / LAN fiber, and others.

In 2026, FTTx (FTTH, FTTB, FTTC) segment is expected to dominate the market

In 2026, FTTx (FTTH, FTTB, FTTC), segment is expected to dominate the market due to accelerated broadband expansion initiatives and increasing demand for high-speed residential and business internet services. Federal and state funding programs aimed at closing the digital divide are driving large-scale fiber-to-the-home deployments, particularly in underserved and rural regions. Growing bandwidth consumption from streaming, remote work, cloud applications, and smart home technologies further strengthens demand. Additionally, telecom operators are prioritizing fiber access networks to replace legacy copper infrastructure, ensuring long-term scalability, higher reliability, and improved network performance nationwide.

- On the basis of deployment mode, the market is segmented into brownfield, and greenfield.

In 2026, brownfield segment is expected to dominate the market

In 2026, brownfield segment is expected to dominate the market due to the ongoing upgrade and modernization of existing network infrastructure. Telecom operators and enterprises are increasingly replacing legacy copper systems with fiber to enhance bandwidth, reliability, and scalability without building entirely new networks. Brownfield deployments are often more cost-effective and faster to implement, as they leverage existing ducts, conduits, and rights-of-way. Additionally, urban densification, 5G small-cell integration, and enterprise campus upgrades are driving significant retrofit activity, positioning brownfield projects as the primary focus of near-term fiber investment strategies.

- On the basis of application, the market is segmented into telecommunication, data centers, enterprise & institutional, industrial, and others.

In 2026, telecommunication segment is expected to dominate the market

In 2026, telecommunication segment is expected to dominate the market due to continuous network expansion, 5G deployment, and nationwide broadband initiatives. Telecom operators are heavily investing in fiber infrastructure to support rising data consumption, cloud services, streaming, and mobile traffic growth. Government-led digital infrastructure programs, including smart city projects and public broadband expansion, further strengthen demand. Additionally, sectors such as healthcare, education, broadcast, and retail increasingly rely on high-speed, low-latency connectivity for mission-critical operations. The ongoing replacement of legacy copper networks with scalable fiber solutions positions telecommunications as the primary driver of overall market growth.

- On the basis of end user, the market is segmented into telecom operators (AT&T, verizon, lumen, frontier, windstream), internet service providers (ISPs), cable multisystem operators (comcast, charter, Cox), hyperscale data center providers (AWS, Azure, Google, Meta), enterprises, government & municipal entities, utilities, and others.

In 2026, telecom operators (AT&T, verizon, lumen, frontier, windstream) segment is expected to dominate the market

In 2026, telecom operators (AT&T, verizon, lumen, frontier, windstream) segment is expected to dominate the market due to aggressive fiber network expansion and long-term infrastructure modernization strategies. These operators are investing heavily in fiber-to-the-home (FTTH), metro network upgrades, and 5G backhaul to enhance service coverage, improve bandwidth capacity, and replace legacy copper infrastructure. Large-scale capital expenditure programs, supported in part by federal broadband funding, are accelerating deployment across urban and rural markets. Their extensive subscriber base and nationwide footprint position telecom operators as the primary drivers of fiber procurement and infrastructure development.

- On the basis of distribution channel, the market is segmented into direct, and indirect.

In 2026, direct segment is expected to dominate the market

In 2026, direct segment is expected to dominate the market due to increasing preference for direct procurement from manufacturers through company websites and dedicated e-commerce platforms. Large telecom operators, hyperscale data centers, and enterprise buyers prefer direct channels to secure customized solutions, bulk pricing advantages, faster lead times, and stronger technical support. Direct engagement also enables manufacturers to build long-term contracts, improve margin control, and offer value-added services such as design assistance and warranty programs. Growing digital procurement systems and streamlined online ordering platforms further strengthen the dominance of direct sales channels

Major Players

Corning Incorporated (U.S.), CommScope Holding Company, Inc. (U.S.), Prysmian Group (Italy), OFS (Furukawa Electric Co., Ltd.) (U.S.), Sumitomo Electric Lightwave (U.S.), AFL (Fujikura Ltd.) (U.S.), Dell Inc. (U.S.), Cisco Systems, Inc. (U.S.), Coherent Corp. (U.S.), Ciena Corporation (U.S.), Amphenol Corporation (U.S.), TE Connectivity (Switzerland), Legrand (France), Nokia Corporation (Finland), Belden Inc. (U.S.), Leviton Manufacturing Co., Inc. (U.S.), HUBER+SUHNER (Switzerland), Ribbon Communications (U.S.), ADTRAN, Inc. (U.S.), Panduit Corp. (U.S.), Clearfield, Inc. (U.S.), Superior Essex Inc. (U.S.), The Siemon Company (U.S.), Hexatronic Group AB (Sweden), Windy City Wire (U.S.), Dongguan Finecables Co., Ltd. (China), Remee Products Corporation (U.S.), Vertical Cable (U.S.), Proterial Cable America, Inc. (U.S.), and American Cable Assemblies (U.S.)

Market Developments

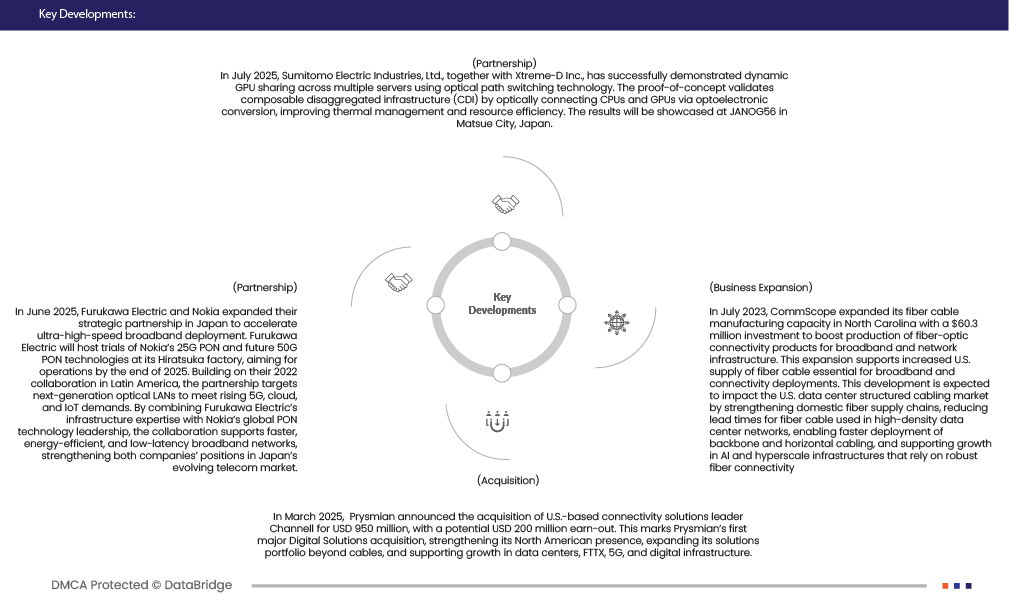

- In July 2025, Sumitomo Electric Industries, Ltd., together with Xtreme-D Inc., has successfully demonstrated dynamic GPU sharing across multiple servers using optical path switching technology. The proof-of-concept validates composable disaggregated infrastructure (CDI) by optically connecting CPUs and GPUs via optoelectronic conversion, improving thermal management and resource efficiency. The results will be showcased at JANOG56 in Matsue City, Japan.

- In June 2025, Furukawa Electric and Nokia expanded their strategic partnership in Japan to accelerate ultra-high-speed broadband deployment. Furukawa Electric will host trials of Nokia’s 25G PON and future 50G PON technologies at its Hiratsuka factory, aiming for operations by the end of 2025. Building on their 2022 collaboration in Latin America, the partnership targets next-generation optical LANs to meet rising 5G, cloud, and IoT demands. By combining Furukawa Electric’s infrastructure expertise with Nokia’s global PON technology leadership, the collaboration supports faster, energy-efficient, and low-latency broadband networks, strengthening both companies’ positions in Japan’s evolving telecom market.

- In March 2025, Prysmian announced the acquisition of U.S.-based connectivity solutions leader Channell for USD 950 million, with a potential USD 200 million earn-out. This marks Prysmian’s first major Digital Solutions acquisition, strengthening its North American presence, expanding its solutions portfolio beyond cables, and supporting growth in data centers, FTTX, 5G, and digital infrastructure.

- In July 2023, CommScope expanded its fiber cable manufacturing capacity in North Carolina with a $60.3 million investment to boost production of fiber-optic connectivity products for broadband and network infrastructure. This expansion supports increased U.S. supply of fiber cable essential for broadband and connectivity deployments. This development is expected to impact the U.S. data center structured cabling market by strengthening domestic fiber supply chains, reducing lead times for fiber cable used in high-density data center networks, enabling faster deployment of backbone and horizontal cabling, and supporting growth in AI and hyperscale infrastructures that rely on robust fiber connectivity

As per Data Bridge Market Research analysis:

For more detailed information about the U.S. fiber connectivity market report, click here – https://www.databridgemarketresearch.com/reports/us-fiber-connectivity-market