Europe Lung Cancer Surgery Market

Market Size in USD Billion

USD

1.10 Billion

USD

1.62 Billion

2025

2033

USD

1.10 Billion

USD

1.62 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.10 Billion | |

| USD 1.62 Billion | |

| % | |

|

Europe Lung Cancer Surgery Market Size

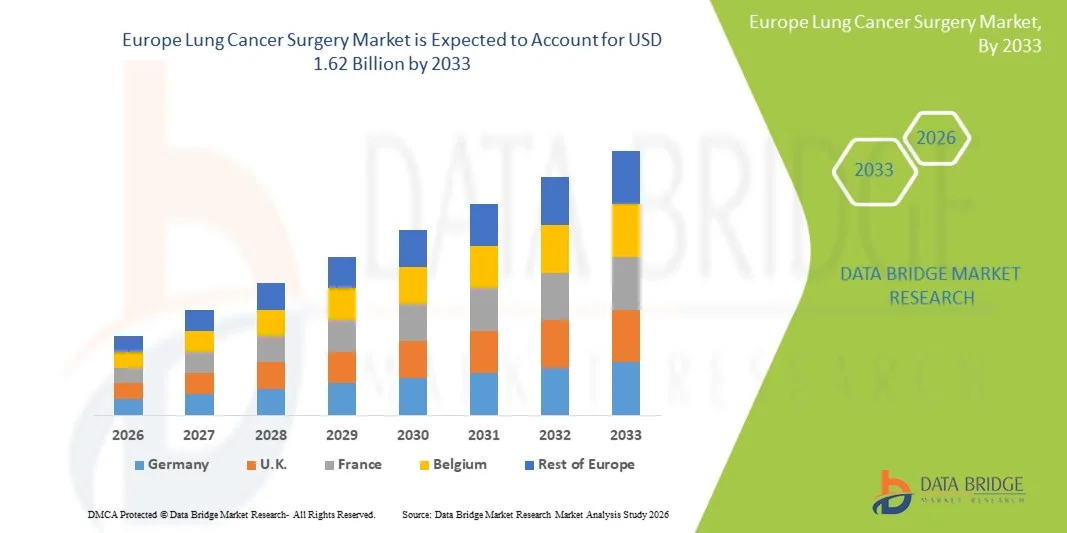

- The Europe lung cancer surgery market size was valued at USD 1.10 billion in 2025 and is expected to reach USD 1.62 billion by 2033, at a CAGR of 5.00% during the forecast period

- The market growth is primarily driven by the rising prevalence of lung cancer across Europe, increasing adoption of minimally invasive surgical procedures such as video-assisted thoracoscopic surgery (VATS) and robotic-assisted surgery, and continuous advancements in surgical technologies

- Furthermore, growing healthcare expenditure, improved access to early diagnostic screening programs, and increasing preference for precision-based surgical interventions are positioning lung cancer surgery as a critical component of cancer treatment across the region. These combined factors are accelerating the demand for advanced surgical solutions, thereby significantly boosting the market growth

Europe Lung Cancer Surgery Market Analysis

- Lung cancer surgery, encompassing a range of surgical procedures supported by advanced instruments and imaging systems, plays a vital role in the treatment of lung cancer across Europe, with increasing adoption of minimally invasive and technology-driven approaches improving surgical precision and patient recovery outcomes

- The escalating demand for lung cancer surgery is primarily driven by the rising incidence of lung cancer, growing awareness regarding early diagnosis, and the expanding utilization of advanced technologies such as robotic-assisted thoracic surgery systems and endosurgical equipment

- Germany dominated the lung cancer surgery market with the largest revenue share of 22.8% in 2025, characterized by advanced healthcare infrastructure, high healthcare spending, and a strong network of specialized thoracic surgery centers, with the country witnessing significant procedural volumes supported by favorable reimbursement policies and early screening programs

- Poland is expected to be the fastest growing country in the lung cancer surgery market during the forecast period due to improving healthcare infrastructure, increasing investments in oncology care, and rising adoption of modern surgical technologies

- Minimally invasive surgery segment dominated the lung cancer surgery market with a market share of 61.5% in 2025, driven by its benefits such as reduced hospital stay, lower post-operative complications, and faster recovery compared to traditional thoracotomy procedures

Report Scope and Europe Lung Cancer Surgery Market Segmentation

|

Attributes |

Europe Lung Cancer Surgery Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Europe Lung Cancer Surgery Market Trends

“Rising Adoption of Minimally Invasive and Robotic-Assisted Procedures”

- A significant and accelerating trend in the Europe lung cancer surgery market is the increasing adoption of minimally invasive techniques and robotic-assisted thoracic surgery systems, enhancing surgical precision and improving patient recovery outcomes across healthcare settings

- For instance, robotic-assisted platforms are being increasingly utilized in hospitals across countries such as Germany and the UK, enabling surgeons to perform complex lung resections with enhanced visualization and precision compared to conventional open surgeries

- The integration of advanced imaging and navigation technologies in lung cancer surgeries enables better tumor localization and minimally invasive intervention strategies, leading to reduced complications and shorter hospital stays for patients undergoing surgical treatment

- The growing preference for minimally invasive procedures such as video-assisted thoracoscopic surgery (VATS) is facilitating faster recovery times and improved post-operative outcomes, thereby driving widespread adoption among both patients and healthcare providers

- This trend towards technologically advanced and less invasive surgical solutions is reshaping treatment protocols and improving clinical outcomes in lung cancer care across Europe, with hospitals increasingly investing in modern surgical systems

- The demand for advanced surgical approaches that enhance precision, reduce trauma, and improve survival outcomes is growing steadily across Europe, as healthcare systems prioritize innovation and efficiency in cancer treatment

- The rising number of specialized thoracic surgery centers across Europe is further supporting the adoption of advanced surgical techniques and contributing to the overall market expansion

Europe Lung Cancer Surgery Market Dynamics

Driver

“Rising Lung Cancer Burden and Advancements in Surgical Technologies”

- The increasing prevalence of lung cancer across Europe, coupled with advancements in surgical technologies, is a significant driver for the growing demand for lung cancer surgery procedures

- For instance, in March 2025, several European healthcare institutions expanded the adoption of robotic-assisted thoracic surgery systems to enhance surgical outcomes and reduce recovery times, supporting the overall market growth

- As the burden of lung cancer continues to rise, there is a growing emphasis on early diagnosis and timely surgical intervention, which significantly improves survival rates and treatment effectiveness

- Furthermore, continuous improvements in surgical instruments, visualization systems, and endosurgical equipment are enabling more precise and less invasive procedures, thereby increasing patient acceptance and surgical success rates

- The availability of advanced healthcare infrastructure and supportive reimbursement frameworks across key European countries is further accelerating the adoption of lung cancer surgery solutions in both public and private healthcare sectors

- The increasing focus on improving patient outcomes, reducing hospital stays, and enhancing surgical efficiency is driving the integration of innovative surgical technologies across Europe

- Government initiatives and national cancer control programs aimed at early detection and treatment are further boosting the demand for surgical interventions across multiple European countries

- The growing aging population, which is more susceptible to lung cancer, is also contributing significantly to the rising demand for surgical treatment options

Restraint/Challenge

“High Cost of Advanced Surgical Systems and Limited Accessibility”

- The high cost associated with advanced surgical systems, including robotic-assisted thoracic surgery platforms and specialized instruments, poses a significant challenge to widespread adoption across all healthcare facilities

- For instance, smaller hospitals and healthcare centers in certain parts of Europe face budget constraints that limit their ability to invest in high-cost surgical technologies and infrastructure required for advanced lung cancer procedures

- In addition, disparities in healthcare access and availability of skilled thoracic surgeons across regions can hinder the uniform adoption of advanced surgical techniques, particularly in less developed healthcare systems

- The complexity of surgical procedures and the need for specialized training and expertise further create barriers for the adoption of advanced minimally invasive and robotic-assisted techniques in lung cancer treatment

- While technological advancements continue to improve surgical outcomes, the high initial investment and maintenance costs associated with these systems remain a concern for healthcare providers and policymakers

- Addressing these challenges through cost optimization, training programs, and improved healthcare accessibility will be essential for ensuring broader adoption and sustained growth of the lung cancer surgery market in Europe

- Lengthy regulatory approval processes for new surgical devices and systems can delay market entry and limit the availability of cutting-edge technologies in certain countries

- Post-operative complications and patient eligibility limitations for surgery in advanced-stage lung cancer cases can also restrict the overall volume of surgical procedures undertaken

Europe Lung Cancer Surgery Market Scope

The market is segmented on the basis of product type, surgical procedure, patient type, end user, and distribution channel.

- By Product Type

On the basis of product type, the Europe lung cancer surgery market is segmented into surgical instruments, monitoring & visualizing system, endosurgical equipment, robotic-assisted thoracic surgery systems, and others. The endosurgical equipment segment dominated the market with the largest revenue share in 2025, driven by its extensive use in minimally invasive lung cancer procedures such as video-assisted thoracoscopic surgery (VATS). These systems enable precise tumor removal with reduced incision size, leading to faster recovery and fewer complications. Hospitals across Europe increasingly rely on advanced endoscopic tools for improved visualization and surgical accuracy. The growing preference for minimally invasive techniques further strengthens the demand for these systems. In addition, continuous technological advancements and integration with imaging platforms enhance their effectiveness. The widespread availability and cost-effectiveness compared to robotic systems also contribute to their dominance.

The robotic-assisted thoracic surgery systems segment is expected to witness the fastest growth rate during the forecast period, fueled by increasing adoption of robotic platforms in complex thoracic procedures. These systems provide enhanced dexterity, 3D visualization, and improved precision, allowing surgeons to perform highly delicate operations. The rising number of robotic surgery installations in leading European hospitals is supporting this growth. Furthermore, favorable clinical outcomes and reduced post-operative complications are encouraging their adoption. Investments by healthcare providers in advanced surgical infrastructure are also accelerating uptake. The growing focus on precision medicine and technological innovation continues to drive this segment forward.

- By Surgical Procedure

On the basis of surgical procedure, the market is segmented into thoracotomy and minimally invasive surgery. The minimally invasive surgery segment dominated the market with the largest revenue share of 61.5% in 2025, driven by its advantages such as reduced hospital stay, minimal blood loss, and quicker recovery times. Procedures such as VATS are increasingly preferred by both surgeons and patients due to improved clinical outcomes. The rising adoption of advanced imaging and navigation technologies further supports the effectiveness of minimally invasive approaches. Healthcare systems in Europe are actively promoting these procedures to reduce overall treatment costs and hospital burden. In addition, patient awareness regarding less invasive treatment options is increasing. The growing availability of skilled surgeons trained in these techniques further strengthens this segment’s leadership.

The minimally invasive surgery segment is also anticipated to witness the fastest growth during the forecast period, due to continuous advancements in surgical technologies and increasing adoption of robotic-assisted techniques. The shift from traditional open surgeries to less invasive approaches is accelerating across Europe. Improved reimbursement policies and government support for advanced treatment methods are contributing to this trend. Moreover, the growing emphasis on patient-centric care is boosting demand for procedures with faster recovery and fewer complications. The expansion of specialized thoracic surgery centers is further facilitating adoption. These factors collectively drive strong growth in this segment.

- By Patient Type

On the basis of patient type, the market is segmented into male and female. The male segment dominated the market with the largest revenue share in 2025, primarily due to the higher prevalence of lung cancer among men in Europe. Historically higher smoking rates among male populations have contributed significantly to increased incidence rates. This leads to a greater volume of surgical procedures being performed on male patients. In addition, occupational exposure to carcinogens in certain industries has further elevated risk among men. Healthcare systems are witnessing a higher proportion of male patients undergoing lung cancer surgeries. Early diagnosis initiatives are also identifying more cases in this demographic. These factors collectively support the dominance of the male segment.

The female segment is expected to witness the fastest growth during the forecast period, driven by the rising incidence of lung cancer among women. Increasing smoking rates in certain regions and environmental factors are contributing to this trend. Improved awareness and screening programs are leading to earlier detection in female patients. In addition, advancements in personalized treatment approaches are encouraging surgical interventions among women. Healthcare providers are increasingly focusing on gender-specific treatment strategies. The growing emphasis on preventive healthcare and early diagnosis is further supporting growth in this segment.

- By End User

On the basis of end user, the market is segmented into hospitals, ambulatory surgical centres, academic & research laboratories, speciality cancer care centres, and others. The hospitals segment dominated the market with the largest revenue share in 2025, driven by the availability of advanced surgical infrastructure and skilled healthcare professionals. Hospitals serve as primary centers for complex lung cancer surgeries, including minimally invasive and robotic-assisted procedures. The presence of multidisciplinary teams ensures comprehensive patient care and better outcomes. In addition, higher patient inflow and established reimbursement systems contribute to their dominance. Continuous investments in modern surgical equipment further enhance hospital capabilities. The integration of advanced diagnostic and treatment technologies also supports their leading position.

The speciality cancer care centres segment is expected to witness the fastest growth during the forecast period, fueled by the increasing demand for specialized oncology services. These centers focus exclusively on cancer treatment, offering advanced surgical options and personalized care. The growing preference for specialized treatment facilities is driving patient inflow to these centers. In addition, the adoption of cutting-edge technologies and participation in clinical research enhance their capabilities. Increasing collaborations with research institutions further support innovation in treatment approaches. The emphasis on high-quality, patient-centric care is accelerating growth in this segment.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender, retail sales, online sales, and others. The direct tender segment dominated the market with the largest revenue share in 2025, driven by bulk procurement of surgical equipment and systems by hospitals and healthcare institutions. Government and private healthcare organizations often rely on direct tenders to acquire high-value surgical technologies at competitive pricing. This channel ensures reliable supply and long-term service agreements with manufacturers. In addition, large-scale procurement supports cost efficiency and standardization across healthcare facilities. The strong presence of established suppliers further strengthens this segment. The preference for direct purchasing in institutional settings continues to drive its dominance.

The online sales segment is expected to witness the fastest growth during the forecast period, driven by increasing digitalization in procurement processes. Healthcare providers are gradually adopting online platforms for purchasing surgical instruments and accessories. These platforms offer convenience, transparency, and access to a wide range of products. In addition, smaller healthcare facilities benefit from easier access to advanced equipment through online channels. The growing trend of e-commerce in the healthcare sector is supporting this shift. Improved logistics and supply chain networks further enhance the efficiency of online sales, contributing to its rapid growth.

Europe Lung Cancer Surgery Market Regional Analysis

- Germany dominated the lung cancer surgery market with the largest revenue share of 22.8% in 2025, characterized by advanced healthcare infrastructure, high healthcare spending, and a strong network of specialized thoracic surgery centers, with the country witnessing significant procedural volumes supported by favorable reimbursement policies and early screening programs

- Healthcare providers in the country strongly emphasize minimally invasive procedures, advanced imaging systems, and robotic-assisted thoracic surgeries to improve clinical outcomes and reduce recovery time for patients undergoing lung cancer treatment

- This widespread adoption is further supported by well-established healthcare infrastructure, favorable reimbursement policies, a strong presence of specialized oncology centers, and the growing focus on early diagnosis and precision-based treatment approaches, establishing lung cancer surgery as a critical component of cancer care in the country

The Germany Lung Cancer Surgery Market Insight

The Germany lung cancer surgery market is expected to expand at a considerable CAGR during the forecast period, fueled by advanced healthcare infrastructure and high adoption of innovative surgical technologies. Germany’s strong emphasis on precision medicine and early-stage cancer treatment promotes the utilization of minimally invasive and robotic-assisted procedures. The presence of specialized thoracic surgery centers and skilled professionals supports high procedural volumes across the country. In addition, favorable reimbursement policies and continuous investments in healthcare innovation are key factors driving market growth.

France Lung Cancer Surgery Market Insight

The France lung cancer surgery market is gaining momentum due to the country’s strong public healthcare system and increasing awareness regarding early cancer diagnosis. The adoption of advanced surgical techniques, including minimally invasive procedures, is contributing to improved treatment outcomes. Government initiatives aimed at cancer control and screening programs are further supporting surgical demand. Moreover, the integration of advanced imaging and surgical technologies is enhancing the efficiency and accuracy of lung cancer surgeries.

Italy Lung Cancer Surgery Market Insight

The Italy lung cancer surgery market is experiencing steady growth driven by rising lung cancer cases and improvements in healthcare infrastructure. Increasing adoption of minimally invasive surgical procedures and growing investments in modern medical equipment are supporting market expansion. The country is also witnessing a rise in specialized cancer treatment centers focusing on advanced surgical care. Furthermore, increasing awareness and early detection initiatives are contributing to higher surgical intervention rates.

Poland Lung Cancer Surgery Market Insight

The Poland lung cancer surgery market is emerging as a high-growth segment, driven by improving healthcare infrastructure and increasing investments in oncology care. The country is witnessing a gradual shift towards minimally invasive and technologically advanced surgical procedures. Government initiatives aimed at strengthening cancer treatment facilities and expanding access to early diagnosis are supporting market expansion. In addition, rising awareness and increasing patient access to specialized care are contributing to higher surgical volumes, positioning Poland as a key growth market in the region.

Europe Lung Cancer Surgery Market Share

The Europe Lung Cancer Surgery industry is primarily led by well-established companies, including:

- Medtronic (Ireland)

- Intuitive Surgical, Inc. (U.S.)

- Olympus Corporation (Japan)

- FUJIFILM Corporation (Japan)

- Ambu A/S (Denmark)

- Teleflex Incorporated (U.S.)

- Accuray Incorporated (U.S.)

- KARL STORZ SE & Co. KG (Germany)

- Richard Wolf GmbH (Germany)

- KLS Martin Group (Germany)

- Ackermann Instrumente GmbH (Germany)

- TROKAMED GmbH (Germany)

- asap endoscopic products GmbH (Germany)

- Surgical Holdings (U.K.)

- AngioDynamics, Inc. (U.S.)

- Scanlan International, Inc. (U.S.)

- Sontec Instruments, Inc. (U.S.)

- FusionKraft (Germany)

- Lepu Medical Technology (Beijing) Co., Ltd. (China)

What are the Recent Developments in Europe Lung Cancer Surgery Market?

- In January 2026, NHS England announced the launch of a major pilot program integrating artificial intelligence and robotic-assisted technologies to improve early detection and diagnosis of lung cancer. The initiative utilizes AI to analyze lung scans and robotic tools to guide precise biopsies, reducing the need for repeated procedures and enabling earlier surgical intervention

- In August 2025, Akershus University Hospital published findings from a study on 200 consecutive robotic-assisted thoracic surgery (RATS) procedures, demonstrating improved surgical efficiency and reduced complication rates over time. The study confirmed that transitioning from traditional video-assisted thoracoscopic surgery (VATS) to robotic approaches is feasible and enhances clinical outcomes

- In May 2025, European Society of Thoracic Surgeons organized its 33rd Annual Conference in Budapest, bringing together leading thoracic surgeons and oncology experts to discuss advancements in lung cancer surgery techniques. The event focused on innovations in minimally invasive and robotic-assisted thoracic procedures, along with improved perioperative care strategies

- In March 2025, Institut Curie presented significant advancements at the European Lung Cancer Congress held in Paris, showcasing progress in personalized treatment approaches and multidisciplinary strategies for lung cancer care. The institution highlighted improved outcomes through neoadjuvant therapies and real-world data validation of treatment protocols, reinforcing the growing integration of precision medicine in surgical oncology

- In May 2022, European Society of Thoracic Surgeons conducted specialized webinars focusing on robotic lung resections and advanced thoracic surgical techniques. These educational initiatives aimed to enhance surgeon expertise in minimally invasive procedures and promote the adoption of next-generation surgical technologies. The program highlights Europe’s ongoing efforts to standardize and improve surgical care quality in lung cancer treatment

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.