Asia Pacific Automotive Level Sensor Market

Market Size in USD Million

USD

431.14 Million

USD

560.75 Million

2024

2032

USD

431.14 Million

USD

560.75 Million

2024

2032

| 2025 - 2032 | |

| USD 431.14 Million | |

| USD 560.75 Million | |

| % | |

|

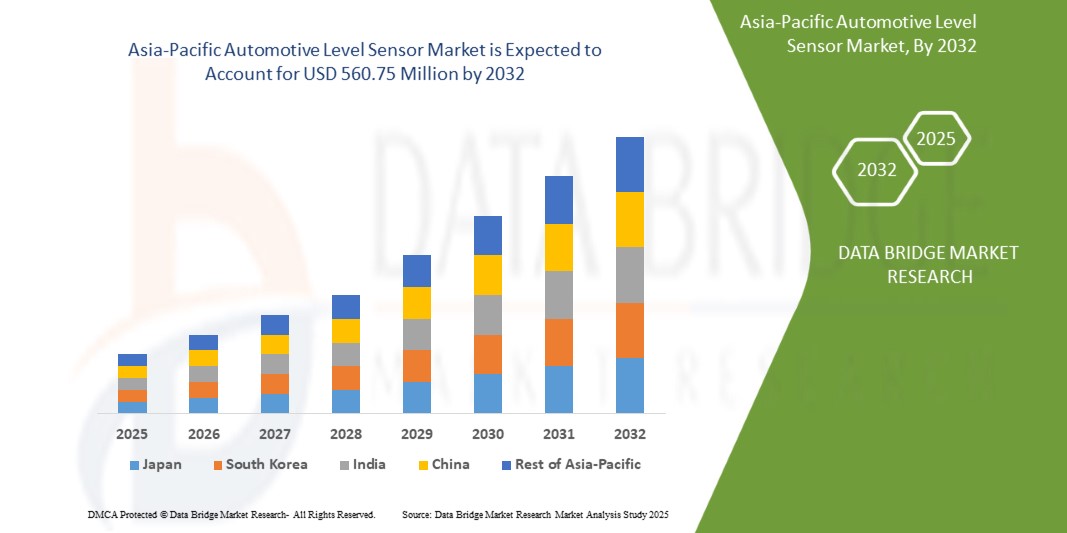

Asia-Pacific Automotive Level Sensor Market Size

- The Asia-Pacific automotive level sensor market size was valued at USD 431.14 million in 2024 and is expected to reach USD 560.75 million by 2032, at a CAGR of 3.34% during the forecast period

- The market growth is largely fueled by the increasing adoption of advanced vehicle technologies, rising emphasis on fuel efficiency, and stringent government regulations on emission control. Automotive level sensors play a vital role in monitoring critical fluids such as fuel, engine oil, and coolant, ensuring vehicle performance, safety, and compliance with evolving environmental standards

- Furthermore, growing demand for connected and electric vehicles, coupled with the integration of smart diagnostic systems, is accelerating the adoption of innovative level sensing solutions. These converging factors are driving rapid uptake across both passenger and commercial vehicles, thereby significantly boosting the industry’s growth

Asia-Pacific Automotive Level Sensor Market Analysis

- Automotive level sensors are precision devices designed to detect and monitor liquid levels in vehicles, including fuel, engine oil, brake fluid, coolant, and power steering fluid. These sensors are critical for maintaining engine efficiency, preventing mechanical failures, and ensuring safe vehicle operation across diverse driving conditions

- The growing demand for automotive level sensors is primarily driven by rising vehicle production, stricter safety and emission norms, and increasing consumer preference for technologically advanced and fuel-efficient vehicles. The expanding role of sensors in hybrid and electric vehicles further underscores their importance, making them a key enabler in the automotive industry transformation

- China dominated the automotive level sensor market in 2024, due to its strong automotive manufacturing base, high vehicle production volumes, and rapid adoption of advanced sensor technologies

- India is expected to be the fastest growing country in the automotive level sensor market during the forecast period due to rising vehicle production, rapid urbanization, and increasing demand for fuel-efficient and safer vehicles

- Continuous level monitoring segment dominated the market with a market share of 62% in 2024, due to its ability to provide real-time and accurate measurement of critical automotive fluids such as fuel, engine oil, and coolant. Automakers increasingly prefer continuous monitoring systems to enhance vehicle efficiency, prevent breakdowns, and ensure regulatory compliance. The integration of advanced sensors with onboard diagnostic systems further strengthens its adoption, making it a preferred choice for both passenger and commercial vehicles

Report Scope and Asia-Pacific Automotive Level Sensor Market Segmentation

|

Attributes |

Asia-Pacific Automotive Level Sensor Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Asia-Pacific Automotive Level Sensor Market Trends

Rising Consumer Demand for Safety and Comfort

- The increasing emphasis on vehicle safety and superior driving comfort is fueling the demand for advanced automotive level sensors across global markets. These sensors are becoming critical components in vehicles, ensuring accurate monitoring of fluid levels and enabling systems that improve driver experience, vehicle efficiency, and passenger protection

- For instance, Bosch has developed a range of advanced fuel and engine oil level sensors integrated with warning systems, enabling car manufacturers to enhance safety standards and offer improved user convenience. Similarly, HELLA GmbH provides washer fluid and brake fluid sensors designed to alert drivers in time, preventing breakdowns and maintaining driving comfort

- Automotive level sensors contribute directly to safety by enabling accurate detection of low oil, brake fluid, or coolant levels, thereby preventing engine damage, brake failure, and overheating. Their role in ensuring timely alerts reduces risks during driving and extends the operational lifespan of vehicle components, strengthening their value in modern automotive systems

- The rising consumer demand for premium experiences is also encouraging adoption of level sensors in luxury and mid-range cars. Applications such as advanced fuel monitoring systems integrated with digital dashboards increase driving comfort by providing precise real-time insights, aligning with the expectations of tech-savvy consumers

- In addition, electrification trends in the automotive sector are pushing manufacturers to adopt sophisticated battery coolant and electrolyte level sensors to ensure optimal performance and safety of electric vehicles. This signifies how consumer expectations for both comfort and safety are directly shaping the evolution of level sensor technologies

- Overall, the rising consumer preference for vehicles that combine performance, comfort, and safety ensures that automotive level sensors will remain indispensable. This trend is driving manufacturers to prioritize sensor innovation and integration, thereby reshaping the broader automotive design and customer experience landscape

Asia-Pacific Automotive Level Sensor Market Dynamics

Driver

Rapidly Expanding Automotive Industry

- The rapid growth of the global automotive industry, particularly in emerging economies, is driving substantial demand for automotive level sensors. With increasing vehicle production and rising adoption of passenger and commercial vehicles, manufacturers are integrating advanced sensors to meet both regulatory standards and consumer expectations

- For instance, DENSO Corporation supplies a wide variety of liquid level sensors to global automotive OEMs, supporting the expansion of both internal combustion engine vehicles and hybrid models. The company’s growing partnerships with automakers highlight the increasing role of level sensors in facilitating industry growth

- The automotive boom in markets such as India, China, and Southeast Asia is boosting the requirement for fuel, coolant, and brake fluid monitoring to maintain vehicle performance under diverse driving conditions. These rapidly developing markets are becoming strong growth centers for the adoption of cost-effective yet reliable level sensor solutions

- In addition, the shift towards electric and hybrid vehicles has added fresh momentum to level sensor adoption. Battery management, thermal control systems, and energy optimization in EVs depend on highly accurate level sensing technologies, making sensors crucial to the transition towards sustainable mobility

- In conclusion, the expansion of the automotive industry, with its growing complexity and reliance on sensor-driven performance, is fueling consistent growth in the level sensor market. The alignment of consumer demand, technological innovation, and automotive production ensures that this driver will sustain long-term industry development

Restraint/Challenge

High Cost of Advanced Sensors

- The high costs associated with advanced automotive level sensors present a key restraint to market growth, particularly in cost-sensitive segments and developing regions. Sophisticated sensors, such as those equipped with ultrasonic and capacitive technologies, involve higher production expenses due to the use of precision components and advanced electronics

- For instance, Continental AG provides advanced multi-fluid level sensing solutions that deliver highly accurate monitoring for modern vehicles, but at a cost higher than traditional float-based sensors. This price differential makes manufacturers wary of integrating advanced sensors into lower-priced vehicle categories where margins are tight

- The challenge is further exacerbated by the need for regular calibration, maintenance, and potential replacements, adding to long-term expenses for manufacturers and consumers. These ongoing costs limit adoption in regions where affordability is a primary purchasing factor for customers

- In addition, the increasing complexity of vehicles, particularly EVs and hybrids, requires integration of multiple specialized sensors, significantly elevating the overall electronic content and cost of the vehicle. Automakers often face trade-offs between keeping vehicles affordable and incorporating advanced sensor technologies across all models

- As a result, high costs remain a barrier to widespread penetration of advanced level sensors in all vehicle segments. Bridging this gap will require manufacturers to focus on cost-optimized designs, economies of scale, and innovation in sensor manufacturing processes to ensure affordability and widespread adoption in the coming years

Asia-Pacific Automotive Level Sensor Market Scope

The market is segmented on the basis of product type, type, monitoring type, application, vehicle type, sales channel, and distribution channel.

- By Product Type

On the basis of product type, the automotive level sensor market is segmented into fuel level sensor, engine oil level sensor, coolant level sensor, brake fluid level sensor, power steering fluid level sensor, magnetic sensor, and others. The fuel level sensor segment dominated the largest market revenue share in 2024, owing to its critical role in real-time fuel monitoring, improved driving efficiency, and preventing engine stalling. Automakers increasingly prioritize advanced fuel level sensors to optimize fuel economy, comply with stringent emission norms, and enhance driving experience, making them indispensable in both passenger and commercial vehicles.

The engine oil level sensor segment is anticipated to witness the fastest growth rate from 2025 to 2032, driven by rising awareness regarding engine health and the need to prevent damage from oil starvation. Modern vehicles integrate engine oil level sensors with onboard diagnostic systems, providing real-time alerts to drivers and reducing maintenance costs. Growing adoption in premium and mid-range vehicles, coupled with consumer preference for advanced vehicle safety and efficiency features, accelerates demand in this segment.

- By Type

On the basis of type, the automotive level sensor market is segmented into capacitive, resistive film, ultrasonic, discrete resistors, optical, and others. The capacitive sensor segment accounted for the largest market revenue share in 2024, supported by its high accuracy, reliability, and versatility in detecting liquid levels across automotive fluids. Capacitive sensors are widely preferred due to their durability, low maintenance, and ability to function effectively in harsh operating environments, making them a standard choice for OEMs.

The ultrasonic sensor segment is expected to record the fastest growth rate during 2025–2032, as automakers increasingly adopt non-contact sensing technologies. Ultrasonic sensors provide precise level detection without being affected by temperature variations or fluid contamination, offering superior accuracy in critical applications. Their integration with advanced driver assistance systems (ADAS) and IoT-based monitoring platforms further enhances their adoption in next-generation vehicles.

- By Monitoring Type

On the basis of monitoring type, the automotive level sensor market is categorized into continuous level monitoring and point level monitoring. The continuous level monitoring segment dominated the market with a share of 62% in 2024, driven by its ability to provide real-time and accurate measurement of critical automotive fluids such as fuel, engine oil, and coolant. Automakers increasingly prefer continuous monitoring systems to enhance vehicle efficiency, prevent breakdowns, and ensure regulatory compliance. The integration of advanced sensors with onboard diagnostic systems further strengthens its adoption, making it a preferred choice for both passenger and commercial vehicles.

The point level monitoring segment is projected to witness the fastest CAGR from 2025 to 2032, supported by its cost-effectiveness and wide use in detecting minimum and maximum fluid thresholds. Increasing demand in entry-level vehicles and aftermarket installations for reliable threshold detection strengthens its growth. This segment is especially gaining traction in regions with high adoption of budget-friendly vehicles where affordability remains a key factor.

- By Application

On the basis of application, the market is segmented into tank refueling and fuel draining monitoring, fuel theft prevention, and fuel consumption monitoring. The fuel consumption monitoring segment held the largest market share in 2024, as rising fuel prices and stricter emission regulations push consumers and fleet operators to optimize fuel usage. OEMs are integrating advanced fuel consumption monitoring sensors to improve efficiency, lower carbon footprint, and meet environmental mandates.

The fuel theft prevention segment is expected to expand at the fastest pace from 2025 to 2032, driven by growing concerns in commercial fleets and logistics operations. Increasing cases of fuel pilferage in emerging markets encourage adoption of advanced anti-theft level sensors with GPS integration. The combination of real-time monitoring and security features ensures better fleet management and cost savings, accelerating demand in this segment.

- By Vehicle Type

On the basis of vehicle type, the market is divided into passenger vehicles and commercial vehicles. The passenger vehicle segment dominated the market revenue share in 2024, driven by high vehicle production volumes and the increasing incorporation of advanced sensor systems in mid-range and premium models. Consumer preference for safety, performance, and efficiency upgrades continues to push demand in this category.

The commercial vehicle segment is anticipated to record the fastest growth during 2025–2032, fueled by the rising adoption of level sensors for fleet management, fuel theft detection, and maintenance optimization. Regulatory pressures on fuel efficiency and emissions, coupled with the growing logistics and transportation sector, further increase the integration of advanced level monitoring solutions in commercial fleets.

- By Sales Channel

On the basis of sales channel, the market is segmented into original equipment manufacturer (OEM) and aftermarket. The OEM segment captured the largest revenue share in 2024, owing to the rising trend of integrating advanced sensors directly into vehicles during production. Automakers prefer factory-installed level sensors to enhance brand reliability and meet stringent government mandates on emissions and safety.

The aftermarket segment is projected to grow at the fastest rate from 2025 to 2032, driven by increasing replacement demand and the adoption of upgraded sensors in aging vehicle fleets. Cost-conscious consumers in developing regions are investing in aftermarket installations to extend vehicle life and improve efficiency, making this a lucrative growth avenue.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into online and offline. The offline segment dominated the market in 2024, as automotive components are largely distributed through established dealership networks, repair shops, and auto service centers. Offline distribution offers reliability, physical inspection, and professional installation services, making it the preferred choice among consumers.

The online segment is expected to expand at the fastest CAGR during 2025–2032, supported by the rapid growth of e-commerce platforms and digital marketplaces for automotive components. Consumers increasingly prefer online purchases for cost advantages, product variety, and doorstep delivery. The availability of sensor integration guides and easy return policies further encourage this shift toward online channels.

Asia-Pacific Automotive Level Sensor Market Regional Analysis

- China dominated the automotive level sensor market with the largest revenue share in 2024, driven by its strong automotive manufacturing base, high vehicle production volumes, and rapid adoption of advanced sensor technologies

- Increasing government regulations on fuel efficiency and emission control, coupled with the demand for safety and performance upgrades, have accelerated sensor integration. The presence of leading domestic and international sensor manufacturers, along with robust supply chains, further strengthens China’s dominance in the regional market.

- Rising demand for connected and smart vehicles, expanding electric vehicle (EV) production, and advancements in sensor miniaturization have further enhanced market adoption. Ongoing investments in R&D, partnerships with global automotive OEMs, and large-scale manufacturing capabilities ensure China maintains its leadership in the Asia-Pacific market

Japan Automotive Level Sensor Market Insight

The Japan market is anticipated to grow steadily from 2025 to 2032, supported by strong consumer preference for technologically advanced vehicles and stringent automotive safety regulations. Japanese automakers emphasize innovation, reliability, and efficiency, driving higher adoption of capacitive and ultrasonic level sensors. Growth is further supported by the country’s leadership in hybrid and electric vehicle production, where accurate fluid monitoring systems are essential. A mature automotive ecosystem, focus on quality, and continuous R&D investments position Japan as a stable and innovation-driven market for automotive level sensors.

India Automotive Level Sensor Market Insight

India is projected to register the fastest CAGR in the Asia-Pacific automotive level sensor market during 2025–2032. Growth is fueled by rising vehicle production, rapid urbanization, and increasing demand for fuel-efficient and safer vehicles. Expanding adoption of level sensors in commercial fleets for fuel theft prevention and consumption monitoring further supports market penetration. Government initiatives promoting emission control and vehicle safety standards are pushing automakers to integrate advanced sensors. Domestic manufacturing expansion, coupled with the growing aftermarket and rising consumer preference for affordable yet advanced technologies, positions India as the fastest-growing market in the region.

Asia-Pacific Automotive Level Sensor Market Share

The automotive level sensor industry is primarily led by well-established companies, including:

- Continental AG (Germany)

- Littelfuse, Inc. (U.S.)

- Bosch Rexroth Sp. Z O.O. (Poland)

- Elobau Gmbh & Co. KG.C (Germany),

- Pricol Limited (India)

- Bourns Inc (U.S.)

- Guangdong Zhengyang Sensing Technology Co., Ltd. (China)

- Misensor Tech Co., Ltd. (China)

- Omnicomm (Estonia)

- Soway Tech Limited (China)

- Spark Minda (India)

- Standex Electronics, Inc (U.S.)

- Technoton (Czech Republic)

- Wema UK (U.K.)

Latest Developments in Asia-Pacific Automotive Level Sensor Market

- In August 2024, Littelfuse, Inc. unveiled its advanced SMBLCEHR HRA, SMCLCE-HR/HRA, and SMDLCE-HR/HRA High-Reliability Low Capacitance TVS Diode Series, specifically engineered to protect avionics systems from lightning strikes and severe overvoltage events. This development establishes a new industry benchmark in high-reliability protection, reinforcing Littelfuse’s leadership in aerospace electronics. By setting higher safety and durability standards, the company strengthens its competitive edge and expands its adoption in the aviation sector, where resilience and reliability are critical

- In August 2024, Continental AG’s Executive Board announced the evaluation of a potential spin-off of its Automotive Group sector into an independent company. This strategic review aims to unlock greater value creation, enhance operational agility, and maximize growth opportunities amid rapidly evolving automotive market conditions. If approved by the Executive and Supervisory Boards and later by shareholders in April 2025, the spin-off could be completed by the end of 2025. Such a move is expected to reshape Continental’s business structure, enabling sharper focus on its Tires and ContiTech sectors while allowing the new entity to pursue accelerated innovation and partnerships in the automotive space

- In July 2024, Continental AG showcased its expanded product portfolio at the Automechanika trade fair in Frankfurt, featuring innovations such as advanced ADAS sensors, sustainable multi V-belts, and the UltracContact NXT tire containing up to 65% sustainable materials. This demonstration reinforced Continental’s technological leadership and also highlighted its strong commitment to sustainability. By aligning with industry trends in green mobility and advanced safety, the company enhanced its global brand positioning, attracted potential customers, and strengthened partnerships with OEMs focused on eco-friendly and high-performance automotive solutions

- In April 2024, Littelfuse, Inc. launched the LS0502SCD33S Single Cell Super Capacitor Protection IC, an advanced addition to its eFuse Protection IC portfolio. This innovation improves the safety and reliability of backup power sources operating under extreme conditions, a critical requirement in automotive, industrial, and energy applications. By setting a new standard for performance and protection, Littelfuse has expanded its footprint in the protection IC market, addressing the rising demand for robust electronic safeguards across critical infrastructure sectors

- In March 2024, Continental AG announced a strategic collaboration with Ambarella, Inc., a leader in AI vision silicon, to co-develop next-generation ADAS and automated driving solutions. This partnership combines Ambarella’s high-performance AI processing with Continental’s extensive sensor and system integration expertise. The collaboration is expected to accelerate the deployment of intelligent, safe, and scalable automated driving technologies, strengthening Continental’s role in shaping the future of mobility while addressing the growing demand for advanced driver assistance systems

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.