Asia Pacific Dental 3d Printing Market

Market Size in USD Billion

USD

3.55 Billion

USD

9.98 Billion

2024

2032

USD

3.55 Billion

USD

9.98 Billion

2024

2032

| 2025 - 2032 | |

| USD 3.55 Billion | |

| USD 9.98 Billion | |

| % | |

|

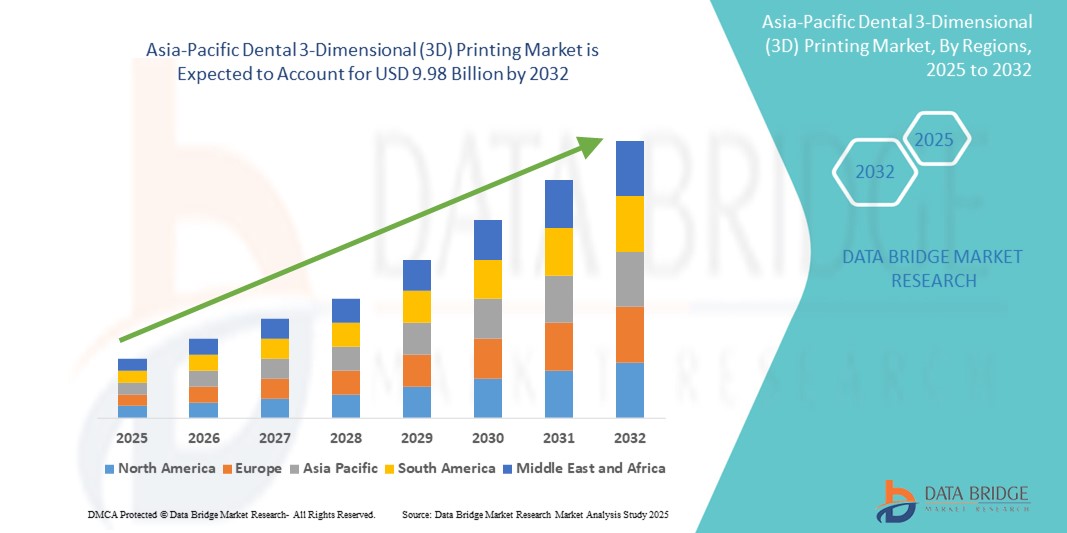

Asia-Pacific Dental 3-Dimensional (3D) Printing Market Size

- The Asia-Pacific Dental 3-Dimensional (3D) printing market size was valued at USD 3.55 billion in 2024 and is expected to reach USD 9.98 billion by 2032, at a CAGR of 13.80% during the forecast period

- The market expansion is primarily driven by the rising adoption of digital dentistry and increasing demand for customized dental prosthetics and implants across the region, supported by a growing geriatric population and rising dental tourism

- Moreover, advancements in 3D printing materials and technologies, along with supportive government initiatives and investments in healthcare infrastructure, are further accelerating the adoption of dental 3D printing solutions positioning the technology as a core enabler of next-generation dental care

Asia-Pacific Dental 3-Dimensional (3D) Printing Market Analysis

- Dental 3D printing, enabling the precise fabrication of dental restorations, prosthetics, and orthodontic devices, is becoming a transformative element of digital dentistry in the Asia-Pacific region due to its ability to deliver customized, high-quality solutions with faster turnaround times and reduced material wastage

- The surging demand for dental 3D printing is primarily driven by increasing awareness of oral health, growing prevalence of dental disorders, and rising acceptance of advanced dental procedures among the aging population

- China dominated the Asia-Pacific Dental 3-Dimensional (3D) printing market with the largest revenue share of 37.3% in 2024, attributed to its expanding dental clinics network, strong manufacturing capabilities, and government support for innovation in healthcare, while Japan and South Korea are also emerging as key contributors due to their tech-forward healthcare ecosystems

- India is expected to witness the fastest growth during the forecast period owing to improving healthcare infrastructure, growing dental tourism, and increasing investments by global dental technology companies

- System segment dominated the Asia-Pacific Dental 3-Dimensional (3D) printing market with a market share of 64.7% in 2024, driven by its ability to offer complete, high-precision in-house dental fabrication solutions and streamline clinical workflows

Report Scope and Asia-Pacific Dental 3-Dimensional (3D) Printing Market Segmentation

|

Attributes |

Asia-Pacific Dental 3-Dimensional (3D) Printing Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Asia-Pacific Dental 3-Dimensional (3D) Printing Market Trends

“Digitalization of Dentistry with AI and Customized Solutions”

- A prominent and accelerating trend in the Asia-Pacific dental 3D printing market is the convergence of digital dentistry with AI and CAD/CAM technologies, enabling the production of highly customized dental prosthetics, implants, and orthodontic devices with improved precision and speed

- For instance, companies such as DIO Corporation and Shenzhen Speed Dental Technology Co., Ltd. are offering AI-integrated 3D dental solutions that optimize scanning, modeling, and fabrication, streamlining the dental workflow from diagnosis to delivery

- AI-driven dental 3D printing systems can auto-correct errors in digital impressions, predict patient-specific prosthetic requirements, and enhance material utilization, resulting in reduced turnaround times and fewer remakes. Customized treatment plans can now be generated quickly and aligned with each patient’s unique anatomy

- Integration with intraoral scanners and cloud-based platforms further allows seamless communication between dental clinics and labs. Dentists can remotely approve models, send files, or even print devices chairside, contributing to a more efficient and patient-centric care model

- This trend is reshaping clinical practices by enabling more accurate, faster, and minimally invasive treatments, which is particularly important in high-volume markets such as China and India where demand for affordable, high-quality dental care is rising rapidly

- The growing need for personalized dental solutions, especially in prosthodontics and orthodontics, is accelerating investment in AI-powered 3D printing technologies across hospitals, clinics, and laboratories, setting the foundation for the next evolution in digital oral healthcare

Asia-Pacific Dental 3-Dimensional (3D) Printing Market Dynamics

Driver

“Rising Dental Disorders and Shift Toward Digital Dentistry”

- The growing prevalence of dental disorders, increasing demand for cosmetic and restorative procedures, and a shift toward digital workflows are key drivers accelerating the adoption of 3D printing in dentistry across Asia-Pacific

- For instance, in June 2024, 3D Systems collaborated with Nissin Dental Products to launch an integrated 3D printing platform in Japan, designed specifically for dental education and prosthetics, highlighting the regional push toward digitized oral healthcare

- With increasing awareness of oral health and rising disposable incomes, especially in emerging economies such as India, Vietnam, and the Philippines, patients are seeking faster, aesthetic, and less invasive solutions benefits that 3D printing readily delivers

- The ability to create accurate, patient-specific restorations and surgical guides using digital impressions and 3D printing allows for better patient outcomes and greater clinical efficiency, fueling widespread adoption in both private clinics and institutional settings

- In addition, expanding dental tourism in Southeast Asia and favorable government initiatives to enhance healthcare infrastructure are contributing to greater penetration of advanced dental technologies in the region

Restraint/Challenge

“High Equipment Costs and Limited Training Among Practitioners”

- The high initial cost of 3D printing equipment and materials remains a significant barrier to adoption, particularly among small to mid-sized dental clinics and labs in cost-sensitive markets within Asia-Pacific

- For instance, entry-level dental 3D printers with sufficient precision and regulatory approval can still cost several thousand dollars, excluding the software, post-processing tools, and maintenance required for long-term operation

- Furthermore, the lack of technical expertise and limited access to structured training programs for dental professionals are hindering widespread implementation of 3D printing technologies in some parts of the region

- While leading dental schools and training centers in countries such as South Korea and Singapore are incorporating digital dentistry into their curricula, many practitioners across rural or underserved areas still rely on conventional methods due to knowledge gaps or lack of exposure

- Overcoming these challenges through cost-effective printer options, broader access to training, and industry partnerships aimed at improving practitioner education will be crucial to ensure inclusive and sustained market growth across the diverse Asia-Pacific region

Asia-Pacific Dental 3-Dimensional (3D) Printing Market Scope

The market is segmented on the basis of product, material, technology, application, end user, and distribution channel.

- By Product

On the basis of product, the Asia-Pacific dental 3D printing market is segmented into system and accessories. The system segment dominated the market with the largest market revenue share of 64.7% in 2024, driven by its ability to offer high-precision, in-house manufacturing capabilities and streamline digital workflows in dental labs and clinics. These systems allow for faster, more accurate production of restorations and appliances, leading to improved patient satisfaction and operational efficiency.

The accessories segment is anticipated to witness steady growth during the forecast period, fueled by the recurring need for materials, nozzles, and maintenance components required to support system functionality and ensure consistent print quality.

- By Material

On the basis of material, the Asia-Pacific dental 3D printing market is segmented into polymer, metal, ceramics, plastic, and others. The polymer segment held the largest market revenue share of 48.5% in 2024, driven by its widespread use in dental models, surgical guides, and temporary restorations. Polymers offer cost efficiency, ease of handling, and compatibility with multiple printing technologies such as SLA and DLP, making them the material of choice for many dental applications.

The ceramics segment is projected to witness the fastest growth rate from 2025 to 2032, owing to its superior biocompatibility, durability, and aesthetic properties making it ideal for permanent restorations such as crowns and bridges.

- By Technology

On the basis of technology, the Asia-Pacific dental 3D printing market is segmented into light curing, powder bed fusion (PBF), and fused deposition modelling (FDM). The light curing segment dominated the market with the largest market revenue share of 46.7% in 2024, driven by its ability to produce high-resolution dental components with smooth surface finishes and precise detail, which are essential in clinical applications. This technology is highly favored for creating crowns, bridges, and orthodontic aligners.

The powder bed fusion (PBF) segment is projected to witness the fastest growth rate from 2025 to 2032, due to its ability to fabricate durable metal dental implants and frameworks, while FDM is gaining traction in academic and research settings for prototyping and educational models due to its affordability and ease of use.

- By Application

On the basis of application, the Asia-Pacific dental 3D printing market is segmented into prosthodontics, implantology, orthodontics, oral and maxillofacial surgery, and others. The prosthodontics segment dominated the market with the largest market revenue share of 38.6% in 2024, driven by rising demand for customized dental prosthetics including dentures, crowns, and bridges. The precision and speed offered by 3D printing are transforming prosthetic workflows across dental practices and labs.

The orthodontics segment is is projected to witness the fastest growth rate from 2025 to 2032, fueled by the growing popularity of clear aligners and the ability to efficiently produce custom-fit devices for patients across varied age groups.

- By End User

On the basis of end user, the Asia-Pacific dental 3D printing market is segmented into dental laboratories, dental hospitals and clinics, and academic & research institutes. The dental laboratories segment held the largest market revenue share of 52.1% in 2024, driven by their central role in producing large volumes of custom dental appliances using high-end 3D printing systems. The demand for rapid and cost-effective prosthetic fabrication further supports high adoption in labs.

The dental hospitals and clinics segment is projected to exhibit strong growth during forecast period, due to increasing adoption of chairside 3D printers and digital workflows that enable same-day procedures and improved patient turnaround times.

- By Distribution Channel

On the basis of distribution channel, the Asia-Pacific dental 3D printing market is segmented into third party distributors and direct tenders. The third party distributors segment dominated the market with the largest revenue share of 58.4% in 2024, driven by the preference of clinics and laboratories to rely on established distributors for the procurement, training, and servicing of dental 3D printing systems and materials.

The direct tenders segment is is projected to witness the fastest growth rate from 2025 to 2032, especially within large hospitals, group dental practices, and academic institutions, which often procure equipment in bulk through centralized or government procurement channels.

Asia-Pacific Dental 3-Dimensional (3D) Printing Market Regional Analysis

- China dominated the largest revenue share of the Asia-Pacific dental 3D printing market with 37.3% in 2024, attributed to its expanding dental clinics network, strong manufacturing capabilities, and government support for innovation in healthcare

- The country’s large patient pool, growing middle-class population, and expanding network of dental clinics are fueling demand for customized, efficient, and cost-effective dental solutions enabled by 3D printing technologies

- Furthermore, government support for innovation, integration of AI and CAD/CAM systems, and the presence of leading local manufacturers are accelerating technology adoption, firmly establishing China as the regional leader in dental 3D printing across both clinical and commercial segment

China Dental 3D Printing Market Insight

The China dental 3D printing market dominated the Asia-Pacific market with the largest revenue share of 36.8% in 2024, attributed to its vast patient population, expanding dental care sector, and strong local production of 3D printing systems. Government initiatives to modernize healthcare, increasing adoption of CAD/CAM technologies, and integration of AI in digital workflows are driving market expansion. China's focus on innovation and its role as a manufacturing hub make it a key player in both domestic demand and global supply of dental 3D printing solutions.

Japan Dental 3D Printing Market Insight

The Japan dental 3D printing market is experiencing steady growth, supported by the country’s advanced healthcare infrastructure, aging population, and high demand for precision dental care. The use of dental 3D printing is increasing in prosthodontics and implantology, as practitioners seek faster, patient-specific treatment solutions. Integration with intraoral scanners and chairside systems is expanding as clinics move toward same-day restorations. Japan’s focus on technology and efficiency continues to drive adoption in both private practices and academic settings.

India Dental 3D Printing Market Insight

The India dental 3D printing market is emerging as one of the fastest-growing markets for dental 3D printing in Asia-Pacific, driven by rising dental awareness, a growing middle class, and expanding dental tourism. The availability of cost-effective 3D printing solutions and the push for digitalization in healthcare are propelling adoption among dental clinics and laboratories. Government-backed healthcare reforms, along with increased training and education in digital dentistry, are further enhancing market potential across metro and tier-2 cities.

South Korea Dental 3D Printing Market Insight

The South Korea dental 3D printing market is gaining momentum due to the country's strong dental export industry, high level of technological adoption, and growing demand for cosmetic dentistry. Clinics are increasingly adopting 3D printing to deliver faster, more precise dental solutions such as aligners, surgical guides, and crowns. Integration of AI and digital scanning tools is common, and the nation’s robust R&D landscape ensures continuous innovation in materials and systems used in dental applications.

Asia-Pacific Dental 3-Dimensional (3D) Printing Market Share

The Asia-Pacific Dental 3-Dimensional (3D) Printing industry is primarily led by well-established companies, including:

- 3D Systems, Inc. (U.S.)

- Stratasys Ltd. (Israel)

- Dentsply Sirona Inc. (U.S.)

- EnvisionTEC, Inc. (Germany)

- Formlabs, Inc. (U.S.)

- DIO Corporation (South Korea)

- Roland DG Corporation (Japan)

- Shenzhen Speed Dental Technology Co., Ltd. (China)

- Straumann Group (Switzerland)

- Prodways Group (France)

- Asiga (Australia)

- NextDent B.V. (Netherlands)

- SHINING 3D Tech Co., Ltd. (China)

- Dentis Co., Ltd. (South Korea)

- VOCO GmbH (Germany)

- DeltaMed GmbH (Germany)

- SprintRay Inc. (U.S.)

- Zortrax S.A. (Poland)

- Planmeca Group (Finland)

- GE Additive (Germany)

What are the Recent Developments in Asia-Pacific Dental 3-Dimensional (3D) Printing Market?

- In June 2024, 3D Systems Corporation partnered with Nissin Dental Products Inc. in Japan to launch a comprehensive 3D printing platform aimed at dental education and prosthetic production. This collaboration combines 3D Systems’ high-precision printing technology with Nissin’s educational expertise to streamline training and accelerate adoption of digital workflows in dental institutions, enhancing the region's digital dentistry capabilities

- In May 2024, Shenzhen Speed Dental Technology Co., Ltd., a China-based digital dental solution provider, introduced a next-generation resin-based 3D printer specifically designed for chairside applications. The compact system enables same-day production of crowns and surgical guides, marking a shift toward faster, patient-centric dental care in clinics across urban China and Southeast Asia

- In April 2024, Straumann Group expanded its footprint in India by launching a new dental 3D printing lab facility in Bengaluru, aiming to provide localized access to high-quality, customized prosthetics. This strategic move enhances Straumann’s service delivery and reduces turnaround times for dental professionals, reinforcing its position as a leader in digital dental solutions in the Asia-Pacific region

- In February 2024, Roland DG Corporation announced the launch of its new DGSHAPE 3D printer series for dental labs in South Korea and Australia. These printers offer enhanced material compatibility and automation features, addressing the growing demand for efficiency and precision in dental prosthetic manufacturing. The initiative supports the ongoing digital transformation across dental laboratories in the region

- In January 2024, DIO Corporation, a major dental implant and 3D printing company based in South Korea, unveiled its upgraded DIOnavi Full Arch solution at the International Dental Show Asia. This AI-integrated system enables full-arch restorations with minimal chair time, supporting the demand for faster, accurate implant procedures. The launch reflects DIO’s commitment to innovation in personalized, technology-driven dental care

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.