Asia Pacific Lithium Ion Battery Recycling Market

Market Size in USD Billion

CAGR :

%

USD

2.25 Billion

USD

11.27 Billion

2025

2033

USD

2.25 Billion

USD

11.27 Billion

2025

2033

| 2026 –2033 | |

| USD 2.25 Billion | |

| USD 11.27 Billion | |

| % | |

|

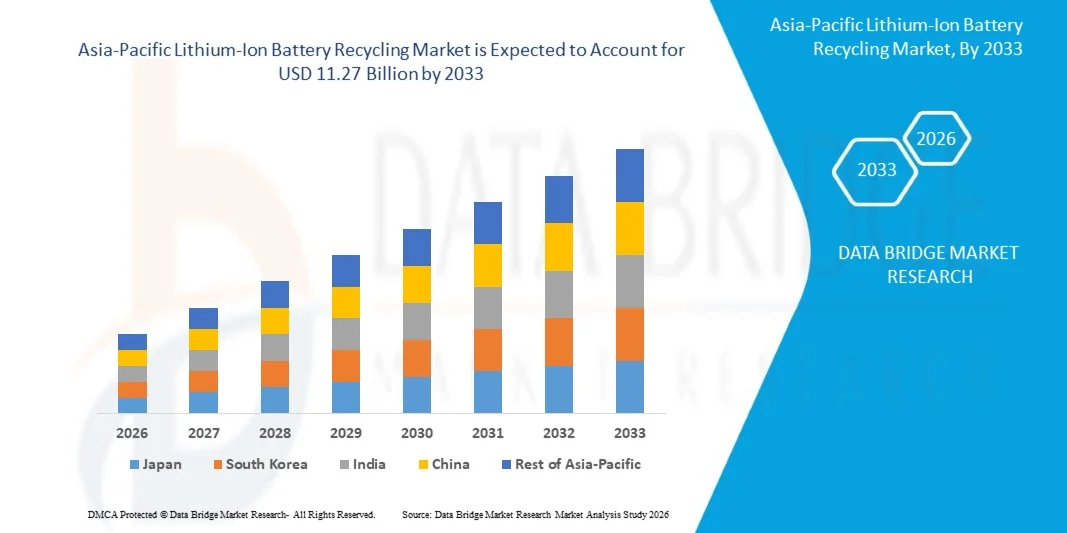

Asia-Pacific Lithium-Ion Battery Recycling Market Size

- The Asia-Pacific lithium-ion battery recycling market size was valued at USD 2.25 billion in 2025and is expected to reach USD 11.27 billion by 2033, at a CAGR of 22.30% during the forecast period

- The market growth is largely fuelled by the rapid increase in electric vehicle adoption, rising battery waste generation, and growing demand for sustainable raw material recovery such as lithium, cobalt, and nickel

- Government regulations promoting circular economy practices, battery disposal mandates, and incentives for recycling infrastructure are accelerating market expansion globally

Asia-Pacific Lithium-Ion Battery Recycling Market Analysis

- The market is witnessing strong momentum due to increasing concerns over critical mineral shortages and the strategic importance of securing secondary battery material supply chains for energy storage and automotive industries

- Rising investments from battery manufacturers, automakers, and recycling firms in closed-loop recycling systems are strengthening industry scalability and long-term profitability

- China dominated the lithium-ion battery recycling market with the largest revenue share in 2025, driven by massive electric vehicle production volumes, extensive battery manufacturing capacity, and growing end-of-life battery generation

- Japan is expected to witness the highest compound annual growth rate (CAGR) in the Asia-Pacific lithium-ion battery recycling market due to advanced recycling technology development, increasing renewable energy storage adoption, strong sustainability commitments, and expanding investments in critical material recovery systems

- The Active Material segment held the largest market revenue share in 2025 driven by the high economic value of recoverable metals such as lithium, cobalt, nickel, and manganese, which are essential for battery remanufacturing and secondary raw material supply chains. Active material recycling is prioritized due to its strategic importance in reducing dependence on virgin mining and supporting circular economy initiatives across electric vehicle and energy storage industries

Report Scope and Asia-Pacific Lithium-Ion Battery Recycling Market Segmentation

|

Attributes |

Asia-Pacific Lithium-Ion Battery Recycling Key Market Insights |

|

Segments Covered |

· By Component: Active Material and Non-Active Material · By Chemistry: Lithium-Nickel Manganese Cobalt (Li-NMC), Lithium Cobalt Oxide (LCO), Lithium-Manganese Oxide (LMO), Lithium-Iron Phosphate (LFP), Lithium-Nickel Cobalt Aluminium Oxide (NCA), and Lithium-Titanate Oxide (LTO) · By Recycling Process: Hydrometallurgical Process, Pyrometallurgy Process, and Physical/ Mechanical Process |

|

Countries Covered |

Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific |

|

Key Market Players |

• GEM Co., Ltd. (China) |

|

Market Opportunities |

• Expansion Of Electric Vehicle Battery Recycling Networks |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Asia-Pacific Lithium-Ion Battery Recycling Market Trends

“Surging Expansion of Electric Vehicle Battery Waste and Circular Economy Initiatives”

- The rapid growth of electric vehicle adoption and large-scale battery deployment is significantly transforming the lithium-ion battery recycling market, as increasing volumes of end-of-life batteries create substantial demand for sustainable recycling solutions. Recycling processes are becoming essential for recovering valuable metals such as lithium, cobalt, nickel, and manganese, which are critical for battery manufacturing. This trend is strengthening the role of recycling in reducing dependence on virgin raw materials while supporting circular economy objectives across automotive, consumer electronics, and energy storage industries

- Growing concerns regarding resource scarcity, battery waste management, and environmental sustainability are accelerating the implementation of advanced lithium-ion battery recycling systems. Governments, automakers, and battery manufacturers are prioritizing closed-loop supply chains to secure strategic mineral supplies and reduce landfill waste. This has encouraged significant investments in recycling facilities, collection networks, and strategic partnerships to improve recycling efficiency and supply security

- Sustainability regulations, battery disposal mandates, and corporate ESG commitments are influencing purchasing and operational strategies, with organizations increasingly emphasizing responsible battery lifecycle management. Manufacturers are investing in environmentally friendly recycling technologies such as hydrometallurgical and direct recycling methods to improve material recovery rates and minimize carbon emissions. These factors are helping companies strengthen brand positioning while meeting evolving regulatory compliance requirements

- For instance, in 2024, Tesla and Redwood Materials expanded battery recycling collaborations to recover critical battery materials from electric vehicles and manufacturing scrap for reuse in new battery production. These initiatives were introduced to improve supply chain resilience, reduce raw material dependency, and enhance sustainability goals. The partnerships also supported broader commercialization of closed-loop battery ecosystems, reinforcing long-term industry competitiveness

- While lithium-ion battery recycling demand is rapidly expanding, long-term market growth depends on technological advancements, cost-effective recovery methods, and efficient battery collection infrastructure. Companies are focusing on improving process scalability, recovery efficiency, and supply chain coordination to ensure sustainable profitability and broader adoption

Asia-Pacific Lithium-Ion Battery Recycling Market Dynamics

Driver

“Increasing Demand for Critical Mineral Recovery and Sustainable Battery Supply Chains”

- Rising global demand for critical minerals used in electric vehicle batteries and energy storage systems is a major driver for the lithium-ion battery recycling market. Recycling provides a strategic secondary source of essential materials such as lithium, cobalt, and nickel, reducing supply chain vulnerabilities and geopolitical risks associated with mining. This trend is encouraging manufacturers to incorporate recycled materials into battery production to support sustainability and cost optimization

- Expanding battery applications in electric vehicles, consumer electronics, industrial equipment, and renewable energy storage are significantly increasing battery waste volumes, which directly supports market growth. Lithium-ion battery recycling enables manufacturers to recover high-value materials while addressing environmental concerns related to hazardous battery disposal. The increasing adoption of electrification technologies globally further reinforces this growth trajectory

- Automotive OEMs, battery producers, and recycling companies are actively expanding recycling capabilities through investments, partnerships, and technological innovation. These initiatives are supported by stronger environmental regulations and corporate sustainability commitments, while also fostering improvements in recovery efficiency, logistics, and battery disassembly systems

- For instance, in 2023, CATL and Li-Cycle increased investments in battery recycling infrastructure to recover battery-grade materials from electric vehicle batteries and production waste. These expansions followed rising battery demand and growing concerns over material shortages, supporting large-scale commercialization of recycled battery materials. Both companies also emphasized sustainable sourcing and carbon footprint reduction to strengthen long-term market positioning

- Although strong mineral demand and sustainability goals support growth, broader adoption depends on reducing recycling costs, enhancing processing efficiency, and establishing reliable global battery collection systems. Continued innovation in recycling technologies and strategic collaboration across the battery value chain will be essential for long-term competitiveness

Restraint/Challenge

“High Processing Costs and Complex Battery Collection Infrastructure”

- The high cost associated with lithium-ion battery recycling remains a major challenge, particularly due to expensive collection, transportation, dismantling, and material recovery processes. Advanced recycling technologies require substantial capital investment, specialized equipment, and regulatory compliance, which can limit participation among smaller market players. In addition, fluctuating battery chemistries create complexity in standardized recycling operations

- Collection and logistics infrastructure for end-of-life batteries remains underdeveloped in many markets, creating barriers to efficient recycling. Safe transportation and storage requirements for hazardous lithium-ion batteries further increase operational complexity and cost burdens. Limited consumer awareness and inconsistent collection programs also reduce battery recovery rates, slowing supply chain development

- Regulatory inconsistencies, technological limitations, and volatile commodity prices further impact market stability. Recycling firms must navigate changing compliance standards, environmental requirements, and market fluctuations that affect profitability. Companies also face challenges in maintaining high recovery yields while minimizing environmental impact and operational costs

- For instance, in 2024, several battery recyclers supplying major automotive and electronics manufacturers reported profitability pressures due to high logistics costs, complex battery sorting requirements, and fluctuating cobalt and lithium prices. These challenges affected operational margins and slowed capacity expansion plans, despite increasing demand for battery recycling services

- Addressing these challenges will require cost-efficient recycling technologies, expanded collection infrastructure, and stronger regulatory alignment. Strategic investments in automation, battery design standardization, and consumer awareness initiatives will be critical for unlocking the full long-term potential of the global lithium-ion battery recycling market

Asia-Pacific Lithium-Ion Battery Recycling Market Scope

The market is segmented on the basis of component, chemistry, and recycling process.

- By Component

On the basis of component, the Asia-Pacific lithium-ion battery recycling market is segmented into Active Material and Non-Active Material. The Active Material segment held the largest market revenue share in 2025 driven by the high economic value of recoverable metals such as lithium, cobalt, nickel, and manganese, which are essential for battery remanufacturing and secondary raw material supply chains. Active material recycling is prioritized due to its strategic importance in reducing dependence on virgin mining and supporting circular economy initiatives across electric vehicle and energy storage industries.

The Non-Active Material segment is expected to witness steady growth from 2026 to 2033, supported by increasing recovery of aluminum, copper, plastics, and electrolytes from spent batteries. Growing emphasis on comprehensive material utilization and stricter environmental regulations are encouraging recyclers to improve processing capabilities for non-active components, enhancing total recycling efficiency and profitability.

- By Chemistry

On the basis of chemistry, the Asia-Pacific lithium-ion battery recycling market is segmented into Lithium-Nickel Manganese Cobalt (Li-NMC), Lithium Cobalt Oxide (LCO), Lithium-Manganese Oxide (LMO), Lithium-Iron Phosphate (LFP), Lithium-Nickel Cobalt Aluminium Oxide (NCA), and Lithium-Titanate Oxide (LTO). The Li-NMC segment accounted for the largest market revenue share in 2025 owing to its widespread use in electric vehicles and large-format energy storage systems. The high concentration of valuable metals such as nickel and cobalt in Li-NMC batteries significantly improves recycling profitability, making this chemistry a primary focus for Asia-Pacifican recyclers.

The LFP segment is expected to witness steady growth from 2026 to 2033 due to its increasing adoption in electric vehicles, grid storage, and commercial energy systems. Although LFP batteries contain lower-value metals, their rising deployment volumes and expanding end-of-life battery generation are creating substantial recycling opportunities, encouraging innovation in cost-efficient recovery technologies.

- By Recycling Process

On the basis of recycling process, the Asia-Pacific lithium-ion battery recycling market is segmented into Hydrometallurgical Process, Pyrometallurgy Process, and Physical/Mechanical Process. The Hydrometallurgical Process segment held the dominant market share in 2025 due to its higher recovery efficiency for critical battery metals, lower greenhouse gas emissions, and greater environmental sustainability compared to conventional alternatives. This process is widely preferred for its ability to recover high-purity lithium, cobalt, and nickel suitable for direct reintegration into battery production.

The Physical/Mechanical Process segment is anticipated to witness significant growth from 2026 to 2033 driven by advancements in battery dismantling, sorting, and pre-treatment technologies. Mechanical recycling offers cost advantages and improved material separation efficiency, particularly when integrated with secondary hydrometallurgical systems, supporting broader commercialization of sustainable recycling infrastructure across Asia-Pacific.

Asia-Pacific Lithium-Ion Battery Recycling Market Regional Analysis

- China dominated the lithium-ion battery recycling market with the largest revenue share in 2025, driven by massive electric vehicle production volumes, extensive battery manufacturing capacity, and growing end-of-life battery generation

- Industries and governments across the region place strong emphasis on securing critical battery materials, reducing environmental pollution, and supporting domestic circular economy frameworks, significantly boosting recycling market penetration

- This dominant regional presence is reinforced by large-scale industrial infrastructure, favorable policy support, and the rapid commercialization of battery recycling technologies, positioning Asia-Pacific as the global leader in lithium-ion battery recycling capacity

Japan Lithium-Ion Battery Recycling Market Insight

The Japan lithium-ion battery recycling market is anticipated to witness significant growth from 2026 to 2033, fueled by advanced technological innovation, increasing energy storage adoption, and strong sustainability commitments from automotive and electronics industries. Japan is focusing heavily on efficient battery resource utilization, rare metal recovery, and minimizing battery waste through advanced recycling systems. Growing research into next-generation recycling technologies and strong collaboration between manufacturers and recyclers are driving market competitiveness. Furthermore, supportive national policies promoting resource efficiency and carbon neutrality are significantly enhancing Japan’s lithium-ion battery recycling market growth.

Asia-Pacific Lithium-Ion Battery Recycling Market Share

The Asia-Pacific lithium-ion battery recycling industry is primarily led by well-established companies, including:

- GEM Co., Ltd. (China)

- Brunp Recycling Technology Co., Ltd. (China)

- Ganfeng Lithium Group Co., Ltd. (China)

- CATL Brunp Recycling (China)

- SungEel HiTech Co., Ltd. (South Korea)

- SK ecoplant Co., Ltd. (South Korea)

- Taisen Recycling Co., Ltd. (Japan)

- Sumitomo Metal Mining Co., Ltd. (Japan)

- Mitsubishi Materials Corporation (Japan)

- Contemporary Amperex Technology Recycling (China)

- Ecopro Co., Ltd. (South Korea)

- TES-AMM Pte Ltd. (Singapore)

- Livium Ltd. (Australia)

- Envirostream Australia Pty Ltd. (Australia)

- Hitachi Zosen Corporation (Japan)

Latest Developments in Asia-Pacific Lithium-Ion Battery Recycling Market

- In March 2024, Mitsui & Co., Joint Venture Development, partnered with major lithium-ion battery manufacturers to optimize battery recycling processes and improve critical material recovery efficiency across Asia-Pacific. This initiative is designed to strengthen sustainable raw material supply chains, enhance recycling scalability, and support the rapidly growing electric vehicle and battery manufacturing sectors

- In 2024, leading Asia-Pacific battery recyclers and manufacturers, Industry Expansion, increased investments in advanced hydrometallurgical and direct recycling technologies to improve processing efficiency, material recovery rates, and environmental sustainability. These developments are accelerating commercialization, improving regional resource security, and strengthening competitive positioning in the global battery recycling market

- In June 2023, India’s Ministry of Electronics and Information Technology (MeitY), Technology Transfer Development, provided advanced lithium-ion battery recycling technology to multiple domestic startups and firms to strengthen India’s recycling capabilities. This initiative supports domestic innovation, reduces dependence on imported critical materials, and accelerates the growth of India’s circular battery economy

- In 2023, CATL Brunp Recycling, Capacity Expansion, expanded lithium-ion battery recycling operations to enhance battery-grade material recovery and support China’s rapidly growing electric vehicle supply chain. This expansion increased large-scale recycling capacity, strengthened domestic critical mineral security, and reinforced China’s market leadership in battery recycling

- In 2022, SungEel HiTech, Strategic Expansion, strengthened its battery recycling processing infrastructure across Asia-Pacific to meet increasing volumes of end-of-life batteries from consumer electronics and electric vehicles. This development improved regional recycling capabilities, supported sustainable battery disposal, and enhanced access to secondary raw materials

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Asia Pacific Lithium Ion Battery Recycling Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Asia Pacific Lithium Ion Battery Recycling Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Asia Pacific Lithium Ion Battery Recycling Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.