Asia Pacific Micro Invasive Glaucoma Surgery Migs Devices Market

Market Size in USD Billion

USD

116.90 Billion

USD

193.46 Billion

2025

2033

USD

116.90 Billion

USD

193.46 Billion

2025

2033

| 2026 - 2033 | |

| USD 116.90 Billion | |

| USD 193.46 Billion | |

| % | |

|

Asia-Pacific Micro Invasive Glaucoma Surgery (MIGS) Devices Market Overview

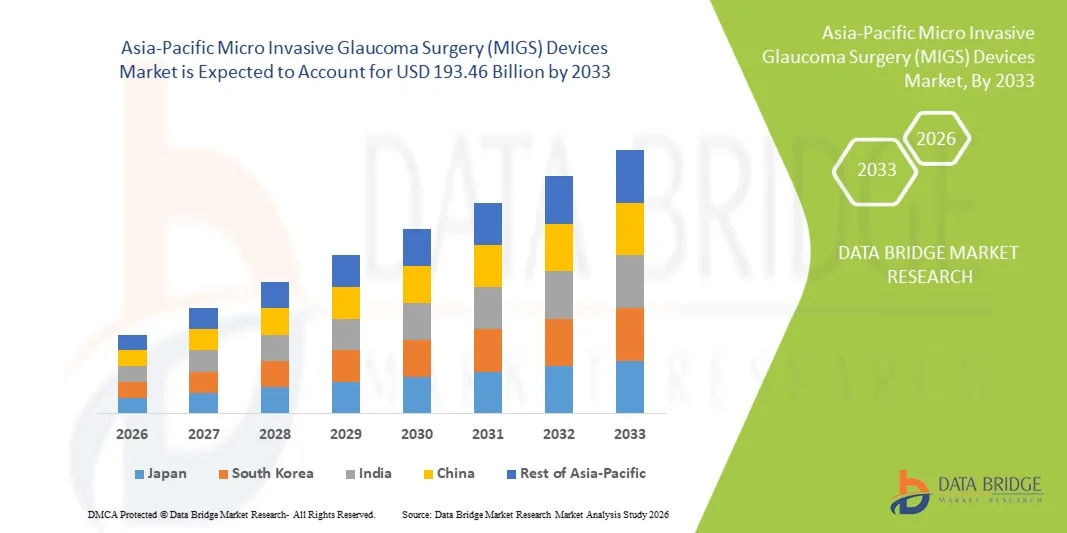

The Asia-Pacific Micro Invasive Glaucoma Surgery (MIGS) Device’s market was valued at USD 116.9 billion in 2025 and is projected to reach USD 193.46 billion by 2033, growing at a CAGR of 6.50% from 2026 to 2033. The Micro Invasive Glaucoma Surgery (MIGS) Devices Market is experiencing consistent growth driven by the rising prevalence of glaucoma, increasing adoption of minimally invasive surgical procedures, growing geriatric population, and continuous advancements in ophthalmic surgical technologies. The demand for MIGS devices is expanding as ophthalmologists increasingly prefer safer, faster, and less invasive alternatives to traditional glaucoma surgeries, offering reduced recovery time, improved patient outcomes, and lower surgical complications.

The increasing global burden of glaucoma-related vision impairment, combined with growing awareness of early diagnosis and advanced treatment options, is encouraging healthcare providers to adopt innovative MIGS technologies. Devices such as glaucoma stents, drainage implants, and canal-based surgical systems are gaining traction as they provide effective intraocular pressure (IOP) management with improved safety profiles compared with conventional procedures. In addition, rising investments by medical device companies in developing next-generation MIGS platforms, coupled with expanding access to advanced ophthalmic care in emerging markets, are further supporting market growth.

Key Market Trends & Insights

- China dominated the Asia-Pacific Micro Invasive Glaucoma Surgery (MIGS) Devices market with the largest revenue share of approximately 36.2% in 2025, supported by its large glaucoma patient pool, expanding ophthalmic healthcare infrastructure, rising adoption of advanced minimally invasive procedures, and increasing investments in eye-care technology across major hospitals and specialty clinics. The country’s growing aging population and improving reimbursement access for ophthalmic surgeries further strengthen MIGS adoption.

- The Glaucoma in Conjunction with Cataract Surgery segment dominated the market with a 62.4% share in 2025, due to the increasing number of combined cataract and glaucoma procedures performed globally.

- India is expected to be the fastest-growing country in the Asia-Pacific MIGS Devices market, registering a CAGR of approximately 8.1% from 2026 to 2033, fueled by rising glaucoma prevalence, expanding private ophthalmology networks, increasing cataract surgery volumes, growing awareness of advanced glaucoma treatments, and improving access to minimally invasive eye-care procedures in emerging cities.

- The Trabecular Meshwork segment dominated the target category with a revenue share in 2025, owing to the widespread clinical adoption of trabecular bypass procedures, favorable safety profiles, and strong preference among surgeons for procedures that enhance natural aqueous outflow pathways while reducing dependence on glaucoma medications.

- The Glaucoma in Conjunction with Cataract Surgery segment accounted for the largest share of the surgery type category at approximately 63.5% in 2025, supported by the growing number of combined cataract and glaucoma procedures, increasing adoption of premium cataract surgery approaches, and clinical benefits associated with treating both conditions in a single intervention

- Hospital Outpatient Departments (HOPDs) dominated the end-user segment revenue share in 2025, driven by availability of advanced ophthalmic equipment, skilled surgeons, higher patient volumes, and increasing preference for hospital-based MIGS procedures requiring specialized surgical infrastructure

- Direct Tender remained the leading distribution channel in 2025, supported by bulk procurement practices of hospitals, government healthcare programs, and large ophthalmology centers that prefer direct purchasing agreements for advanced surgical devices.

Market Size & Forecast

- Asia-Pacific Market Value (2025): USD 116.9 Billion

- Expected Market Value (2033): USD 193.46 Billion

- Forecast CAGR (2026–2033): 6.50%

- Leading Region in 2025: China

- Fastest Growing Region: India

Report Scope and Asia-Pacific Micro Invasive Glaucoma Surgery (MIGS) Devices Market Segmentation

|

Attributes |

Micro Invasive Glaucoma Surgery (MIGS) Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific |

|

Key Market Players |

• Alcon Inc. (Switzerland) |

|

Market Opportunities |

· Increasing adoption of minimally invasive glaucoma procedures as alternatives to traditional glaucoma surgeries · Growing demand for advanced MIGS devices due to the rising global prevalence of glaucoma and age-related eye disorders · Expansion opportunities in emerging markets driven by improving healthcare infrastructure and increasing access to ophthalmic care |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Asia-Pacific Micro Invasive Glaucoma Surgery (MIGS) Devices Market Trends

Trend: Rising Adoption of MIGS Procedures in Cataract Surgery and Advanced Glaucoma Management

Ophthalmology practices across Asia-Pacific are increasingly adopting Micro Invasive Glaucoma Surgery (MIGS) Devices as a preferred treatment option due to their minimally invasive nature, faster recovery profile, and ability to reduce dependence on glaucoma medications. The growing prevalence of glaucoma, particularly among aging populations in countries such as China, Japan, and India, is accelerating demand for advanced glaucoma interventions. According to the International Agency for the Prevention of Blindness (IAPB), glaucoma remains one of the leading causes of irreversible blindness globally, with the burden expected to increase significantly as populations age. MIGS adoption is also being strengthened by the increasing number of combined cataract and glaucoma procedures, where devices such as trabecular micro-bypass stents and subconjunctival filtration implants are used to manage intraocular pressure (IOP) during cataract surgery. Hospitals and ophthalmology clinics are increasingly integrating MIGS technologies to improve patient outcomes while reducing the long-term requirement for topical glaucoma medications. Countries including China and India are witnessing rising adoption due to expanding specialty eye-care networks, increasing ophthalmic surgical volumes, and improving access to advanced surgical technologies.

Asia-Pacific Micro Invasive Glaucoma Surgery (MIGS) Devices Market Dynamics

Key Market Driver: Increasing Prevalence of Glaucoma and Expansion of Ophthalmic Healthcare Infrastructure

The rising global and regional burden of glaucoma is a major factor driving the growth of the Asia-Pacific MIGS Devices market. The increasing geriatric population, higher incidence of age-related eye disorders, and growing awareness regarding early diagnosis are encouraging patients and healthcare providers to adopt advanced glaucoma treatment options.

China represents a major growth engine in the region due to its large aging population and expanding healthcare expenditure. The country has witnessed significant investments in ophthalmology hospitals, specialty clinics, and advanced surgical centers, supporting wider availability of MIGS procedures. Similarly, India is experiencing rapid market expansion due to increasing glaucoma screening programs, growth of private ophthalmology chains, and rising adoption of minimally invasive procedures in urban and semi-urban healthcare settings. In addition, healthcare providers are shifting from traditional glaucoma surgeries such as trabeculectomy and tube shunts toward MIGS solutions because of lower surgical trauma, improved safety profiles, and shorter recovery periods. The increasing availability of FDA-approved MIGS technologies, including trabecular meshwork implants and micro-invasive filtration devices, is further supporting clinical adoption.

Key Restraint/Challenge: High Cost of MIGS Devices and Limited Access in Emerging Healthcare Settings

A major challenge affecting the adoption of Micro Invasive Glaucoma Surgery Devices in Asia-Pacific is the relatively high cost associated with MIGS implants, surgical equipment, and specialized surgeon training. Unlike conventional glaucoma procedures, MIGS requires advanced implant technologies, precision instruments, and ophthalmologists trained in minimally invasive techniques, increasing the overall treatment cost.

The cost barrier is particularly significant in price-sensitive markets where reimbursement coverage for advanced ophthalmic procedures remains limited. Smaller hospitals, rural healthcare centers, and outpatient ophthalmology facilities may face difficulties adopting MIGS due to high device acquisition costs and the need for specialized operating room infrastructure. For instance, advanced MIGS implants such as trabecular bypass stents and subconjunctival filtration devices require specialized surgical expertise and imported technologies in several Asia-Pacific markets, increasing dependency on international manufacturers and affecting affordability. This creates a gap between technologically advanced urban centers and smaller healthcare facilities.

Key Market Opportunity: Technological Advancements and Expansion of Minimally Invasive Glaucoma Treatment Platforms

Technological innovation in glaucoma surgery presents significant growth opportunities for the Asia-Pacific MIGS Devices market. Manufacturers are focusing on developing next-generation implants with improved biocompatibility, enhanced aqueous drainage efficiency, and easier implantation techniques to improve surgical outcomes.

The integration of advanced imaging technologies, digital ophthalmology platforms, and artificial intelligence-based glaucoma monitoring systems is creating new opportunities for personalized treatment planning. AI-powered diagnostic tools are increasingly being used for early glaucoma detection through retinal imaging and optical coherence tomography (OCT) analysis, enabling timely intervention with MIGS procedures. Growing investments by ophthalmology device companies and healthcare providers in emerging economies such as India and Southeast Asia are expected to accelerate market penetration. The expansion of ambulatory surgery centers (ASCs) and specialized eye-care hospitals is also creating new adoption opportunities, as these facilities increasingly perform minimally invasive glaucoma procedures with shorter patient recovery times. Furthermore, partnerships between global ophthalmic device manufacturers and regional healthcare providers are improving surgeon training programs and increasing awareness of MIGS technologies, supporting long-term market growth across Asia-Pacific.

Asia-Pacific Micro Invasive Glaucoma Surgery (MIGS) Devices Market Scope

The Micro Invasive Glaucoma Surgery (MIGS) Devices market is segmented on the basis of product, target, surgery type, end user, and distribution channel

- By Product

On the basis of product, the global Micro Invasive Glaucoma Surgery (MIGS) Devices Market is segmented into MIGS Stents, MIGS Shunts, and Others. The MIGS Stents segment dominated the market with a 46.8% share in 2025, due to increasing adoption of minimally invasive glaucoma procedures and rising preference for implant-based solutions that provide effective intraocular pressure reduction with fewer complications compared with traditional glaucoma surgeries. The widespread use of trabecular micro-bypass stents, combined with growing surgeon acceptance and improved clinical outcomes, is driving segment growth. In addition, increasing prevalence of glaucoma, rising geriatric population, and growing adoption of MIGS procedures during cataract surgery are supporting demand for stent-based devices. The availability of technologically advanced stents with improved biocompatibility, ease of implantation, and enhanced patient safety is further strengthening the leading position of this segment. Growing investments by ophthalmic device manufacturers in product innovation and regulatory approvals are also contributing to market expansion.

The MIGS Shunts segment is expected to witness the fastest CAGR of 8.2% from 2026 to 2033, driven by increasing demand for advanced glaucoma drainage solutions among patients requiring significant intraocular pressure reduction. The growth is supported by continuous innovation in subconjunctival and suprachoroidal shunt technologies designed to improve aqueous humor drainage and long-term treatment outcomes. Increasing adoption of minimally invasive alternatives to conventional glaucoma filtration surgeries is accelerating the use of MIGS shunts. In addition, rising clinical research activities, improved implant designs, and growing acceptance among ophthalmic surgeons are enhancing segment growth. The expansion of specialty eye care centers and increasing availability of advanced glaucoma treatment options are further supporting adoption.

- By Target

On the basis of target, the global Micro Invasive Glaucoma Surgery (MIGS) Devices Market is segmented into Trabecular Meshwork, Suprachoroidal Space, Subconjunctival Filtration, and Reducing Aqueous Production. The Trabecular Meshwork segment dominated the market with a 43.5% share in 2025, owing to the widespread adoption of trabecular-based MIGS procedures that utilize the eye’s natural drainage pathway to reduce intraocular pressure. The segment growth is supported by strong clinical acceptance, favorable safety profiles, and increasing use among patients undergoing cataract and glaucoma combined procedures. Trabecular meshwork targeting devices are preferred due to their minimally invasive approach, shorter recovery time, and lower risk of complications compared with traditional glaucoma surgeries. Increasing awareness among patients and ophthalmologists regarding early glaucoma management is further contributing to segment dominance. Moreover, continuous advancements in micro-implant technologies are improving surgical outcomes and supporting market growth.

The Subconjunctival Filtration segment is projected to register the fastest CAGR of 8.5% from 2026 to 2033, driven by increasing demand for MIGS technologies capable of achieving greater intraocular pressure reduction in moderate to advanced glaucoma patients. Growth is supported by advancements in subconjunctival implant designs that provide controlled aqueous drainage while reducing surgical risks. Increasing research and development activities focused on improving long-term effectiveness of filtration-based MIGS devices are accelerating segment expansion. In addition, growing adoption of minimally invasive procedures as alternatives to traditional trabeculectomy is supporting demand. Rising healthcare investments and increasing availability of specialized glaucoma treatment facilities are expected to further drive segment growth.

- By Surgery Type

On the basis of surgery type, the global Micro Invasive Glaucoma Surgery (MIGS) Devices Market is segmented into Glaucoma in Conjunction with Cataract Surgery and Stand-Alone Glaucoma Surgery. The Glaucoma in Conjunction with Cataract Surgery segment dominated the market with a 62.4% share in 2025, due to the increasing number of combined cataract and glaucoma procedures performed globally. The segment benefits from the ability of MIGS devices to provide glaucoma management while patients undergo cataract extraction, reducing the need for multiple surgeries. Growing prevalence of cataracts and glaucoma among the aging population is significantly increasing adoption of combined procedures. In addition, ophthalmologists are increasingly preferring MIGS solutions due to shorter recovery periods, improved patient comfort, and reduced dependence on glaucoma medications. The availability of advanced surgical systems and increasing surgeon expertise are further strengthening segment growth.

The Stand-Alone Glaucoma Surgery segment is expected to witness the fastest CAGR of 8.0% from 2026 to 2033, driven by increasing demand for glaucoma treatment among patients who do not require cataract intervention. Rising awareness about early glaucoma diagnosis and treatment is encouraging patients to seek standalone minimally invasive procedures. Technological advancements in MIGS devices designed specifically for standalone applications are improving treatment effectiveness and expanding adoption. Increasing investments in ophthalmology infrastructure and growing availability of specialized glaucoma surgeons are further supporting segment growth.

- By End User

On the basis of end user, the global Micro Invasive Glaucoma Surgery (MIGS) Devices Market is segmented into Hospital Outpatient Departments (HOPD), Ophthalmology Clinics, Ambulatory Surgery Centers (ASCs), and Others. The Hospital Outpatient Departments (HOPD) segment dominated the market with a 38.6% share in 2025, due to the availability of advanced surgical infrastructure, experienced ophthalmic professionals, and access to comprehensive patient care facilities. Hospitals remain major adoption centers for MIGS devices due to their ability to perform complex glaucoma procedures and manage post-operative care. Increasing healthcare investments, rising patient preference for advanced surgical treatments, and growing adoption of minimally invasive procedures are supporting segment dominance. Furthermore, partnerships between hospitals and medical device companies are improving access to advanced MIGS technologies.

The Ambulatory Surgery Centers (ASCs) segment is expected to register the fastest CAGR of 8.7% from 2026 to 2033, driven by increasing preference for outpatient surgical procedures that offer cost efficiency, shorter hospital stays, and faster patient recovery. The growth of specialized ophthalmic surgery centers is accelerating the adoption of MIGS devices in ASCs. In addition, rising healthcare cost pressures and increasing demand for minimally invasive procedures are encouraging the shift toward ambulatory settings. Growing availability of trained ophthalmic surgeons and advanced surgical equipment is further supporting segment expansion.

- By Distribution Channel

On the basis of distribution channel, the global Micro Invasive Glaucoma Surgery (MIGS) Devices Market is segmented into Direct Tender and Retail Sales. The Direct Tender segment dominated the market with a 58.9% share in 2025, due to large-scale procurement of MIGS devices by hospitals, healthcare systems, and government healthcare institutions. Direct tender channels provide cost advantages, reliable supply agreements, and easier procurement processes for high-value ophthalmic devices. Increasing investments in hospital infrastructure and expansion of advanced eye care facilities are supporting segment dominance. In addition, manufacturers are increasingly partnering with healthcare institutions to improve product availability and adoption.

The Retail Sales segment is expected to witness the fastest CAGR of 7.9% from 2026 to 2033, driven by increasing adoption of MIGS devices among private ophthalmology clinics and smaller healthcare facilities. Growth is supported by expanding medical distribution networks, increasing availability of specialized ophthalmic suppliers, and improving access to advanced glaucoma treatment technologies. Rising demand for minimally invasive glaucoma procedures in emerging markets is further contributing to retail channel expansion.

Asia-Pacific Micro Invasive Glaucoma Surgery (MIGS) Devices Market Regional Analysis

The Asia-Pacific Micro Invasive Glaucoma Surgery (MIGS) Devices market is expected to experience significant growth during the forecast period, supported by the rising prevalence of glaucoma, expanding geriatric population, increasing ophthalmic healthcare investments, and growing adoption of minimally invasive glaucoma treatment procedures. Countries such as China, India, and Japan are witnessing increased demand for advanced glaucoma management solutions due to rising awareness of early diagnosis, improving access to specialized eye-care services, and growing preference for procedures offering faster recovery and reduced surgical complications. The expansion of ophthalmology clinics, ambulatory surgery centers, and hospital-based eye-care departments is further supporting MIGS adoption across the region.

China Micro Invasive Glaucoma Surgery (MIGS) Devices Market Insight

The China Micro Invasive Glaucoma Surgery (MIGS) Devices market dominated the Asia-Pacific region with the largest revenue share of approximately 36.2% in 2025, driven by the country’s large glaucoma patient population, rapidly aging demographic, expanding ophthalmology infrastructure, and increasing adoption of advanced minimally invasive surgical technologies. China’s growing healthcare expenditure and investments in specialty eye hospitals and advanced surgical facilities are accelerating the adoption of MIGS devices, including MIGS stents, shunts, and subconjunctival filtration solutions. The increasing number of cataract surgeries in China is also supporting demand for MIGS procedures performed alongside cataract surgery, as ophthalmologists increasingly seek integrated approaches for managing both cataracts and glaucoma. Additionally, improvements in healthcare reimbursement coverage, government initiatives to strengthen eye-care services, and increasing availability of advanced ophthalmic technologies are positioning China as the leading MIGS Devices market in Asia-Pacific.

India Micro Invasive Glaucoma Surgery (MIGS) Devices Market Insight

The India Micro Invasive Glaucoma Surgery (MIGS) Devices market is projected to be the fastest-growing market in Asia-Pacific, registering a CAGR of approximately 8.1% from 2026 to 2033. Market growth is primarily driven by the rising burden of glaucoma, increasing awareness regarding vision preservation, expansion of private ophthalmology networks, and growing adoption of advanced minimally invasive treatment options in major cities and emerging healthcare hubs. India’s rapidly expanding cataract surgery ecosystem is creating strong opportunities for MIGS adoption, particularly for procedures combining cataract extraction with glaucoma management. The increasing presence of specialized eye-care chains, improving access to ophthalmic technologies, and rising investments in healthcare infrastructure are enabling wider availability of MIGS procedures. Furthermore, growing patient preference for safer surgical alternatives with shorter recovery periods compared with traditional glaucoma surgeries is expected to accelerate market penetration across the country.

Asia-Pacific Micro Invasive Glaucoma Surgery (MIGS) Devices Market Share

The Micro Invasive Glaucoma Surgery (MIGS) Devices industry is primarily led by well-established companies, including:

- Alcon Inc. (Switzerland)

- Johnson & Johnson Vision (U.S.)

- Glaukos Corporation (U.S.)

- Abbott Medical (U.S.)

- Bausch + Lomb Corporation (Canada/U.S.)

- Carl Zeiss Meditec AG (Germany)

- Santen Pharmaceutical Co., Ltd. (Japan)

- Nova Eye Medical Limited (Australia)

- Ivantis, Inc. (U.S.)

- Sight Sciences, Inc. (U.S.)

- MicroOptix Inc. (U.S.)

- New World Medical, Inc. (U.S.)

- Rhein Medical, Inc. (U.S.)

- Rayner (United Kingdom)

- OmniVision GmbH (Germany)

- Iridex Corporation (U.S.)

- Topcon Corporation (Japan)

- Nidek Co., Ltd. (Japan)

- Hoya Corporation (Japan)

- Katalyst Surgical (U.S.)

- VSY Biotechnology GmbH (Germany)

- Oertli Instrumente AG (Switzerland)

- Lumenis (Israel)

- iSTAR Medical (Belgium)

- Globus Medical (U.S.)

- AqueSys, Inc. (U.S.)

- Aeon Astron Europe B.V. (Netherlands)

Latest Developments in Asia-Pacific Micro Invasive Glaucoma Surgery (MIGS) Devices Market

- In March 2021, Ivantis, a developer of the Hydrus Microstent MIGS device, announced five-year follow-up results from its HORIZON pivotal clinical trial, one of the longest-term clinical evaluations of a MIGS device. The study demonstrated sustained reduction in glaucoma medication use and a lower rate of secondary glaucoma surgeries compared with cataract surgery alone, strengthening clinical confidence in trabecular meshwork-based MIGS technologies for open-angle glaucoma management. This milestone supported broader adoption of MIGS procedures in glaucoma treatment pathways

- In November 2021, Alcon announced its agreement to acquire Ivantis, the developer of the Hydrus Microstent, to expand its glaucoma surgical portfolio and strengthen its presence in the growing MIGS Devices market. The acquisition reflected increasing strategic interest among major ophthalmic companies in minimally invasive glaucoma technologies and highlighted the rising importance of MIGS solutions within ophthalmic surgery

- In November 2021, Ivantis presented additional five-year data from the HORIZON clinical trial showing that the Hydrus Microstent demonstrated a significant reduction in visual field loss progression compared with cataract surgery alone. The findings provided further evidence supporting the long-term effectiveness of MIGS devices in controlling intraocular pressure and slowing glaucoma progression

- In December 2021, Ivantis announced the enrollment of the first patient in the FRONTIER pivotal clinical trial evaluating the Hydrus Microstent as a standalone MIGS procedure for patients with mild-to-moderate open-angle glaucoma who had previously undergone cataract surgery. The trial represented an important step toward expanding MIGS applications beyond combined cataract and glaucoma procedures

- In April 2022, Alcon announced the continued global expansion of its ophthalmic surgical portfolio following the integration of Ivantis and the Hydrus Microstent technology into its glaucoma treatment offerings. The development strengthened Alcon’s position in the MIGS Devices market by combining advanced glaucoma implants with its existing cataract and ophthalmic surgical ecosystem

- In September 2022, Glaukos Corporation highlighted continued clinical adoption of its iStent MIGS technology, supported by growing physician preference for minimally invasive glaucoma procedures that reduce medication burden and improve intraocular pressure management. The company continued advancing glaucoma surgery innovation through its portfolio of trabecular micro-bypass technologies

- In June 2023, Glaukos announced positive clinical progress across its glaucoma product pipeline, including next-generation MIGS technologies designed to improve treatment options for glaucoma patients. The company continued investing in implant innovation and clinical research to expand the role of minimally invasive procedures in glaucoma care

- In October 2023, Alcon expanded its ophthalmic surgical innovation initiatives by highlighting advancements across its glaucoma and cataract surgery platforms, including technologies supporting MIGS adoption. The company emphasized improving surgical efficiency, patient outcomes, and access to advanced glaucoma treatment solutions worldwide

- In December 2023, discussions around Medicare reimbursement changes for certain MIGS procedures in the United States increased industry focus on clinical evidence, cost-effectiveness, and long-term outcomes associated with glaucoma implants. The development highlighted the importance of reimbursement frameworks in influencing MIGS adoption and market growth

- In May 2024, Glaukos announced continued progress in its glaucoma technology pipeline, including developments related to implantable glaucoma devices and clinical studies aimed at expanding minimally invasive treatment options. The company’s focus on innovation supported broader market momentum toward advanced glaucoma management solutions

- In August 2024, Alcon continued strengthening its ophthalmic surgical portfolio through advancements in glaucoma treatment technologies and global commercialization efforts for minimally invasive glaucoma procedures. The company’s initiatives reflected increasing demand for MIGS devices as ophthalmologists sought alternatives to traditional glaucoma surgeries with improved safety and recovery profiles

- In January 2025, the global MIGS Devices market continued witnessing increased adoption of minimally invasive glaucoma procedures, supported by rising glaucoma prevalence, aging populations, and expansion of ophthalmology infrastructure across emerging economies. Manufacturers focused on improving device designs, enhancing clinical outcomes, and increasing availability of MIGS technologies in developing markets

- In June 2025, ongoing advancements in MIGS devices focused on next-generation stents, shunts, and subconjunctival filtration technologies aimed at improving aqueous outflow control and reducing dependence on glaucoma medications. Increasing investments in ophthalmic innovation, growing cataract surgery volumes, and rising awareness of minimally invasive glaucoma treatment approaches continued supporting market expansion globally

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.