Asia Pacific Teleradiology Market

Market Size in USD Million

CAGR :

%

USD

547.46 Million

USD

2,246.34 Million

2025

2033

USD

547.46 Million

USD

2,246.34 Million

2025

2033

| 2026 –2033 | |

| USD 547.46 Million | |

| USD 2,246.34 Million | |

| % | |

|

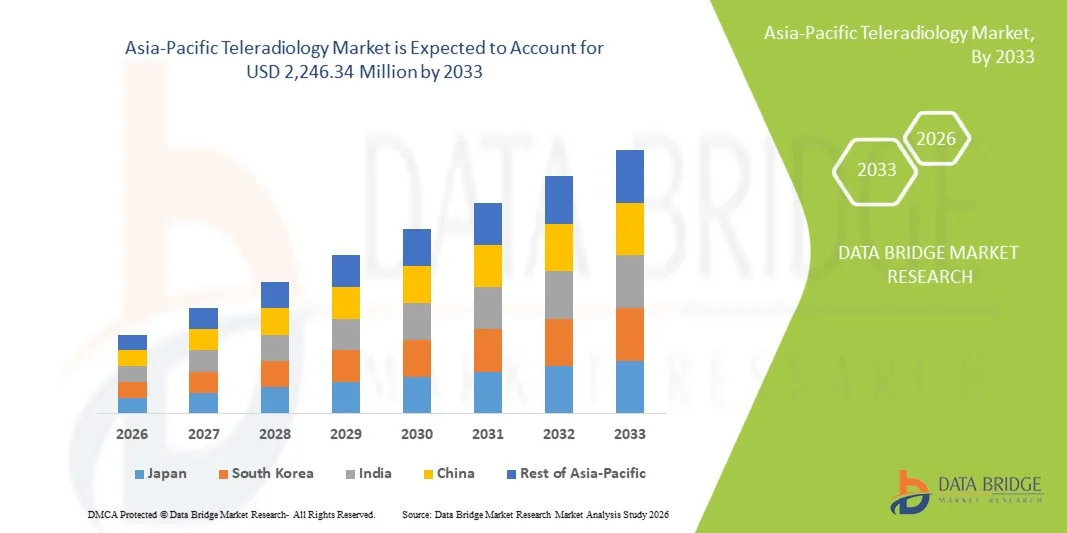

Asia-Pacific Teleradiology Market Size

- The Asia-Pacific teleradiology market size was valued at USD 547.46 million in 2025 and is expected to reach USD 2,246.34 million by 2033, at a CAGR of 19.3% during the forecast period

- The market growth is largely fueled by the increasing burden of diagnostic imaging demand, shortage of radiology specialists, and rapid adoption of telemedicine and digital healthcare infrastructure across emerging and developed economies in the region, leading to improved access to remote diagnostic services

- Furthermore, rising demand for faster, cost-effective, and high-quality radiology reporting, along with the integration of AI-enabled imaging solutions, cloud-based PACS systems, and cross-border diagnostic collaborations, is establishing teleradiology as a critical component of modern healthcare delivery in the Asia-Pacific region, thereby significantly boosting the industry's growth

Asia-Pacific Teleradiology Market Analysis

- Teleradiology, enabling remote transmission and interpretation of medical imaging such as X-rays, CT scans, and MRI scans, is becoming a critical component of modern healthcare delivery systems in the Asia-Pacific region due to rising diagnostic workloads, uneven distribution of radiology professionals, and increasing adoption of digital health infrastructure in both urban and rural healthcare settings

- The escalating demand for teleradiology services is primarily fueled by the growing burden of chronic diseases requiring advanced imaging, shortage of qualified radiologists in many Asia-Pacific countries, and rising demand for faster, round-the-clock diagnostic reporting supported by telemedicine expansion

- China dominated the Asia-Pacific teleradiology market with the largest revenue share of 34.8% in 2025, supported by strong hospital networks, rapid healthcare digitalization, and increasing integration of AI-enabled imaging platforms

- India is expected to be the fastest growing country in the teleradiology market during the forecast period due to increasing government investments in digital healthcare infrastructure, expansion of hospital and diagnostic center networks, and rising cross-border collaboration for remote diagnostic services

- The tele-diagnosis segment dominated the Asia-Pacific teleradiology market with the largest revenue share of 62.4% in 2025, driven by its ability to enable real-time remote interpretation of imaging data, improve diagnostic turnaround times, and support efficient clinical decision-making across hospitals and imaging centers

Report Scope and Asia-Pacific Teleradiology Market Segmentation

|

Attributes |

Asia-Pacific Teleradiology Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Asia-Pacific Teleradiology Market Trends

“Rising Adoption of AI-Enabled Remote Diagnostic Platforms”

- A significant and accelerating trend in the Asia-Pacific teleradiology market is the rapid integration of artificial intelligence (AI) and cloud-based imaging platforms with hospital information systems and radiology workflows, improving diagnostic accuracy and operational efficiency across healthcare networks

- For instance, AI-enabled platforms such as Aidoc and Google Cloud Healthcare API integrated radiology tools are increasingly being adopted in hospitals across India, China, and Japan to assist radiologists in detecting abnormalities faster and improving reporting turnaround time

- AI integration in teleradiology enables features such as automated image prioritization, anomaly detection in CT and MRI scans, and intelligent reporting support systems that help reduce radiologist workload and improve diagnostic precision over time

- The seamless integration of teleradiology systems with hospital PACS and EMR platforms facilitates centralized access to imaging data, enabling real-time collaboration between radiologists and clinicians across different geographic locations in the Asia-Pacific region

- This trend towards intelligent, connected, and cloud-enabled diagnostic ecosystems is fundamentally reshaping healthcare delivery expectations, with companies such as Teleradiology Solutions and RamSoft expanding AI-powered reporting and cloud-based imaging services across Asia-Pacific markets

- The demand for advanced AI-driven teleradiology solutions is growing rapidly across hospitals and diagnostic centers, as healthcare providers increasingly prioritize faster diagnosis, scalability, and improved patient outcomes through digital transformation

- Moreover, rising cross-border collaboration between healthcare providers and specialized radiology groups is expanding access to expert second opinions, enhancing diagnostic confidence and treatment planning across the region

Asia-Pacific Teleradiology Market Dynamics

Driver

“Growing Need Due to Rising Imaging Demand and Radiologist Shortage”

- The increasing burden of chronic diseases and growing demand for advanced diagnostic imaging, coupled with a shortage of qualified radiologists in many Asia-Pacific countries, is a significant driver for the heightened demand for teleradiology services

- For instance, in April 2025, major hospital networks in India expanded their digital radiology infrastructure to support remote reporting, aiming to reduce diagnostic delays and improve access to specialist interpretation in rural and semi-urban regions

- As healthcare providers face increasing patient loads and demand for faster diagnostic turnaround, teleradiology offers scalable solutions such as remote reporting, 24/7 radiology coverage, and reduced dependency on on-site specialists

- Furthermore, the growing adoption of telemedicine and digital health platforms is making teleradiology an essential component of modern healthcare systems, enabling seamless integration of imaging services with broader clinical workflows

- The convenience of faster reporting, cost efficiency, and improved access to expert radiologists are key factors propelling the adoption of teleradiology in hospitals, diagnostic centers, and outpatient care facilities across the Asia-Pacific region

- In addition, increasing government initiatives supporting digital health transformation are accelerating the deployment of teleradiology systems in public healthcare networks across emerging economies in the region

Restraint/Challenge

“Cybersecurity Risks and Infrastructure Limitations”

- Concerns surrounding data privacy, cybersecurity vulnerabilities, and inconsistent digital infrastructure pose a significant challenge to broader adoption of teleradiology systems across the Asia-Pacific region

- For instance, reports of healthcare data breaches in 2024 involving cloud-based medical systems have increased caution among hospitals regarding secure transmission and storage of sensitive imaging data

- Addressing these cybersecurity risks through strong encryption protocols, regulatory compliance frameworks, and secure cloud deployment strategies is essential for building trust among healthcare providers and patients

- In addition, limited digital infrastructure and uneven internet connectivity in rural and semi-urban areas of developing Asia-Pacific economies can restrict real-time image transmission and delay diagnostic workflows

- While investments in healthcare IT infrastructure are increasing, cost barriers and lack of standardized interoperability between systems continue to hinder seamless adoption of advanced teleradiology solutions

- Overcoming these challenges through stronger cybersecurity frameworks, infrastructure modernization, and affordable cloud-based solutions will be vital for sustained market growth

- Furthermore, the shortage of trained IT personnel in healthcare facilities can slow down the implementation and maintenance of advanced teleradiology systems, affecting overall efficiency and scalability

Asia-Pacific Teleradiology Market Scope

The market is segmented on the basis of type, delivery mode, imaging technique, technology, procedure, application, site, age, mode of purchase, and end user.

- By Type

On the basis of type, the Asia-Pacific teleradiology market is segmented into hardware, systems, software, telecom, and networking services. The software segment dominated the market with the largest revenue share in 2025, driven by the increasing reliance on advanced imaging platforms, PACS integration, and AI-enabled diagnostic tools that streamline radiology workflows. Hospitals and diagnostic centers prefer software solutions due to their ability to enable remote reporting, real-time image sharing, and seamless interoperability across healthcare systems. The growing adoption of cloud-based imaging software and AI-assisted diagnostic applications further strengthens this segment’s dominance. In addition, continuous upgrades in imaging analytics and reporting tools are enhancing diagnostic accuracy and operational efficiency. Rising investments in digital healthcare infrastructure across China, India, and Japan are further accelerating software adoption in teleradiology. The shift toward centralized and scalable diagnostic platforms continues to reinforce this segment’s leading position.

The telecom and networking services segment is expected to witness the fastest growth from 2026 to 2033, driven by the increasing need for high-speed data transmission, secure connectivity, and reliable bandwidth for real-time imaging transfer. Expansion of 5G networks and improved internet penetration in emerging Asia-Pacific economies are significantly supporting this growth. Hospitals and diagnostic centers are increasingly dependent on robust networking infrastructure to handle large imaging files such as CT and MRI scans. Furthermore, growing demand for uninterrupted remote diagnostics and cross-border reporting services is boosting investments in advanced telecom solutions. Increasing partnerships between healthcare providers and IT service companies are also accelerating deployment. The rising focus on secure, low-latency communication networks is expected to further drive this segment’s expansion.

- By Delivery Mode

On the basis of delivery mode, the market is segmented into web-based delivery mode, cloud-based delivery mode, and on-premise delivery mode. The cloud-based delivery mode dominated the market with the largest revenue share in 2025, driven by its scalability, cost-effectiveness, and ability to support remote access to imaging data from multiple locations. Hospitals and diagnostic centers increasingly prefer cloud platforms due to their ability to store, process, and share large imaging datasets efficiently. Cloud-based systems also support AI integration and real-time collaboration between radiologists and clinicians across geographies. The rising adoption of telemedicine and digital health ecosystems further strengthens cloud deployment. In addition, reduced infrastructure costs and improved data backup capabilities are enhancing its adoption. Growing investments by healthcare IT providers in secure cloud architecture are reinforcing market dominance.

The web-based delivery mode is expected to witness the fastest growth from 2026 to 2033, driven by its ease of access, minimal installation requirements, and compatibility with existing hospital systems. Healthcare providers are increasingly adopting browser-based platforms for quick deployment and remote accessibility without heavy infrastructure investments. The growing demand for flexible diagnostic solutions in smaller hospitals and diagnostic centers is supporting this segment. Web-based systems also enable faster updates and improved interoperability with imaging tools. Rising digital literacy among healthcare professionals is further accelerating adoption. Expanding use of teleconsultation services is also contributing to strong growth momentum.

- By Imaging Technique

On the basis of imaging technique, the market is segmented into small matrix size and large matrix size. The large matrix size segment dominated the market with the largest revenue share in 2025, driven by the increasing demand for high-resolution imaging in complex diagnostic procedures such as oncology, neurology, and cardiology. Large matrix images provide greater clarity and detail, enabling more accurate interpretation of CT, MRI, and advanced radiology scans. Hospitals prefer these imaging formats for critical care diagnosis and surgical planning. The rising prevalence of chronic diseases requiring advanced imaging is further boosting this segment. Integration of AI-based image enhancement tools also supports large matrix adoption. Expanding investments in high-end imaging infrastructure across Asia-Pacific are reinforcing dominance.

The small matrix size segment is expected to witness the fastest growth from 2026 to 2033, driven by its lower storage requirements, faster transmission speeds, and suitability for basic diagnostic applications. Smaller healthcare facilities and rural centers prefer this format due to limited infrastructure and bandwidth constraints. The increasing use of mobile-based diagnostic tools also supports adoption. Cost-effectiveness and ease of integration into existing systems further drive growth. Rising demand for quick preliminary diagnostics in emergency settings is also contributing to expansion. Growing penetration of telemedicine in rural Asia-Pacific regions strengthens this segment’s growth outlook.

- By Technology

On the basis of technology, the Asia-Pacific teleradiology market is segmented into advanced graphics processing, volume rendering, multiplanar reconstructions, and image compression. The volume rendering segment dominated the market with the largest revenue share in 2025, driven by its ability to provide highly detailed 3D visualization of complex anatomical structures, improving diagnostic accuracy in oncology, neurology, and cardiovascular imaging. Hospitals and imaging centers increasingly rely on volume rendering for surgical planning and complex case evaluations. The growing prevalence of chronic diseases requiring advanced imaging interpretation further strengthens this segment. Integration of AI-based visualization tools is also enhancing rendering quality and efficiency. Continuous upgrades in imaging software across Asia-Pacific healthcare systems are supporting adoption. Rising demand for precise diagnostic imaging in tertiary care hospitals reinforces market dominance.

The image compression segment is expected to witness the fastest growth from 2026 to 2033, driven by the increasing need to efficiently transmit large imaging files over limited bandwidth networks. Compression technologies help reduce data size without significantly compromising image quality, enabling faster remote diagnosis. This is particularly important in rural and semi-urban areas of Asia-Pacific with weaker connectivity. Growing adoption of cloud-based teleradiology platforms is further accelerating demand. Increasing use of mobile and web-based diagnostic systems also supports this growth. The rising focus on real-time reporting and reduced latency is boosting adoption of advanced compression technologies.

- By Procedure

On the basis of procedure, the market is segmented into tele-consultation, tele-diagnosis, and tele-monitoring. The tele-diagnosis segment dominated the market with the largest revenue share of 62.4% in 2025, driven by its central role in enabling remote interpretation of imaging studies such as CT, MRI, and X-rays. Hospitals and diagnostic centers widely depend on tele-diagnosis for faster reporting and improved clinical decision-making. The shortage of radiologists in many Asia-Pacific countries further strengthens this segment. Integration of AI-assisted diagnostic tools is improving accuracy and efficiency. Increasing adoption of PACS and cloud-based systems is also supporting dominance. Expanding hospital networks and rising imaging volumes reinforce strong demand for tele-diagnosis services.

The tele-monitoring segment is expected to witness the fastest growth from 2026 to 2033, driven by increasing demand for continuous patient monitoring in chronic disease management and post-treatment care. Remote monitoring allows physicians to track patient progress using imaging and diagnostic data in real time. Growing prevalence of cancer, cardiovascular, and neurological disorders is supporting this segment. Expansion of home healthcare and telemedicine platforms is also accelerating adoption. Integration of wearable and connected diagnostic devices is further enhancing remote monitoring capabilities. Rising focus on preventive healthcare and early intervention is boosting growth.

- By Application

On the basis of application, the market is segmented into cardiology, neurology, oncology, musculoskeletal, gastroenterology, pelvic and abdominal, gynecology, urology, mammography, dental, and others. The oncology segment dominated the market with the largest revenue share in 2025, driven by the rising prevalence of cancer and increasing reliance on advanced imaging techniques for tumor detection, staging, and treatment planning. Teleradiology plays a critical role in enabling timely cancer diagnosis across urban and rural healthcare settings. Increasing adoption of CT, PET, and MRI imaging in oncology further supports dominance. AI-based image analysis tools are improving tumor detection accuracy. Expanding cancer screening programs across Asia-Pacific are boosting demand. Strong hospital investments in oncology infrastructure reinforce segment leadership.

The neurology segment is expected to witness the fastest growth from 2026 to 2033, driven by the rising incidence of neurological disorders such as stroke, epilepsy, and Alzheimer’s disease. Increasing demand for early and accurate brain imaging is fueling adoption of teleradiology services. Expanding availability of advanced MRI and CT scanning facilities supports growth. AI-assisted neurological imaging tools are improving diagnostic precision. Growing awareness of neurological health and early diagnosis is further accelerating demand. Rising healthcare investments in neuro-care infrastructure across Asia-Pacific also contribute significantly.

- By Site

On the basis of site, the market is segmented into in-house, offshore, and onshore. The in-house segment dominated the market with the largest revenue share in 2025, driven by hospitals and large diagnostic centers preferring internal control over imaging data, workflow, and reporting accuracy. In-house teleradiology systems enable faster communication between radiologists and clinicians. Strong data security and compliance requirements further support adoption. Integration with hospital IT systems and PACS platforms enhances operational efficiency. Large tertiary hospitals across China, Japan, and India increasingly rely on in-house setups. Continuous investment in digital infrastructure reinforces dominance.

The offshore segment is expected to witness the fastest growth from 2026 to 2033, driven by increasing demand for cost-effective radiology reporting services from developed markets within Asia-Pacific and beyond. Offshore teleradiology enables 24/7 reporting support and access to global radiology expertise. Rising shortage of radiologists in developed countries is boosting outsourcing. Improvements in secure cloud connectivity are enabling seamless offshore operations. Growing cross-border healthcare collaborations are also supporting growth. Cost advantages and scalability are key drivers for this segment.

- By Age

On the basis of age, the market is segmented into pediatric, geriatric, and adults. The adult segment dominated the market with the largest revenue share in 2025, driven by the high prevalence of chronic diseases such as cancer, cardiovascular disorders, and respiratory conditions in the working-age population. Adults undergo the highest volume of diagnostic imaging procedures across hospitals. Increasing lifestyle-related diseases further strengthen demand. Expanding outpatient and emergency care services also support dominance. AI-based diagnostic tools are widely used in adult imaging workflows. Strong healthcare utilization rates across Asia-Pacific reinforce this segment.

The geriatric segment is expected to witness the fastest growth from 2026 to 2033, driven by the rapidly aging population in countries such as Japan, China, and South Korea. Elderly patients require frequent imaging for age-related conditions. Rising incidence of neurodegenerative and musculoskeletal diseases is further boosting demand. Expanding geriatric healthcare infrastructure supports growth. Increased use of remote diagnostics for elderly home care is also accelerating adoption. Government healthcare programs focusing on aging populations further enhance segment expansion.

- By Mode of Purchase

On the basis of mode of purchase, the market is segmented into group purchase and individual purchase. The group purchase segment dominated the market with the largest revenue share in 2025, driven by large hospital networks and healthcare organizations adopting centralized procurement of teleradiology systems. Group purchasing enables cost efficiency and standardized technology deployment across multiple facilities. Strong bargaining power and long-term service contracts support dominance. Increasing adoption by government healthcare systems further strengthens this segment. Integration of enterprise-level PACS and cloud solutions also supports group adoption. Expanding hospital chains across Asia-Pacific reinforce this trend.

The individual purchase segment is expected to witness the fastest growth from 2026 to 2033, driven by smaller clinics, diagnostic centers, and standalone radiology practices adopting flexible and affordable teleradiology solutions. Increasing availability of subscription-based cloud platforms is supporting adoption. Ease of deployment and lower upfront costs are key drivers. Rising penetration of digital healthcare tools in semi-urban regions also contributes to growth. Growing demand for independent radiology practices is further accelerating this segment.

- By End User

On the basis of end user, the market is segmented into hospitals, ambulatory surgical centers, private physician offices, diagnostic imaging centers, and others. The hospitals segment dominated the market with the largest revenue share in 2025, driven by high patient inflow, advanced imaging infrastructure, and strong adoption of integrated teleradiology systems for faster diagnosis and treatment planning. Hospitals serve as primary hubs for complex imaging procedures. Increasing demand for emergency and critical care imaging further strengthens dominance. Integration of AI and cloud-based platforms improves workflow efficiency. Strong government investments in hospital digitalization across Asia-Pacific support growth. Expanding tertiary care networks reinforce leadership.

The diagnostic imaging centers segment is expected to witness the fastest growth from 2026 to 2033, driven by rising outsourcing of imaging services and increasing demand for specialized diagnostic facilities. These centers benefit from high patient volume and cost-efficient operations. Adoption of advanced imaging technologies and AI-assisted diagnostics is accelerating growth. Increasing preference for standalone imaging services supports expansion. Growing urbanization and private healthcare investment in Asia-Pacific are further boosting this segment. Rising demand for quick and accurate reporting enhances adoption significantly.

Asia-Pacific Teleradiology Market Regional Analysis

- China dominated the Asia-Pacific teleradiology market with the largest revenue share of 34.8% in 2025, supported by strong hospital networks, rapid healthcare digitalization, and increasing integration of AI-enabled imaging platforms

- Healthcare providers in the country are increasingly utilizing teleradiology solutions to manage high patient volumes, reduce diagnostic turnaround times, and improve access to specialist radiologists in urban as well as tier-2 and tier-3 cities

- This strong dominance is further supported by substantial government investments in digital health infrastructure, widespread deployment of AI-enabled imaging platforms, and growing integration of cloud-based PACS systems, establishing China as a key leader in regional teleradiology adoption

The China Teleradiology Market Insight

The China teleradiology market captured the largest revenue share in Asia-Pacific in 2025, fueled by rapid hospital digitalization, strong expansion of imaging infrastructure, and high adoption of AI-based diagnostic platforms. The country’s large patient population and increasing burden of chronic diseases are significantly driving imaging demand. Moreover, strong government support for smart hospitals and cloud-based healthcare systems is further accelerating market expansion. Integration of advanced PACS systems and AI-powered radiology tools is improving diagnostic efficiency and reducing reporting time across healthcare facilities.

Japan Teleradiology Market Insight

The Japan teleradiology market is gaining strong momentum due to the country’s advanced healthcare infrastructure, high adoption of medical imaging technologies, and strong focus on precision diagnostics. The aging population is significantly increasing demand for continuous diagnostic monitoring and advanced imaging services. Furthermore, integration of AI-assisted radiology systems and cloud-based imaging platforms is enhancing workflow efficiency. Japan’s strong emphasis on healthcare quality and early disease detection is further supporting widespread adoption of teleradiology solutions across hospitals and diagnostic centers.

India Teleradiology Market Insight

The India teleradiology market accounted for the fastest growth rate in Asia-Pacific during the forecast period, driven by rising healthcare digitization, large patient pool, and shortage of radiology specialists, particularly in rural and semi-urban regions. Increasing adoption of telemedicine platforms and cloud-based diagnostic solutions is enabling wider access to expert radiology services. Government initiatives supporting digital health infrastructure and smart hospital development are further accelerating growth. In addition, the expansion of private diagnostic chains and AI-enabled imaging startups is making teleradiology more affordable and accessible across the country.

South Korea Teleradiology Market Insight

The South Korea teleradiology market is experiencing steady growth due to the country’s highly developed healthcare system, strong digital infrastructure, and early adoption of advanced medical imaging technologies. Increasing prevalence of chronic diseases and rising demand for high-quality diagnostic services are driving adoption of teleradiology solutions. Furthermore, widespread integration of AI-based imaging analysis and cloud-enabled hospital systems is improving diagnostic accuracy and efficiency. Government support for digital health innovation and smart hospital initiatives is further strengthening market growth across the country.

Asia-Pacific Teleradiology Market Share

The Asia-Pacific Teleradiology industry is primarily led by well-established companies, including:

- vRad (U.S.)

- Radiology Partners, Inc., (U.S.)

- StatRad, LLC, (U.S.)

- ONRAD, Inc., (U.S.)

- USARAD Holdings, Inc., (U.S.)

- Teleradiology Solutions, Inc., (U.S.)

- NightHawk Radiology Services, Inc., (U.S.)

- RadNet, Inc., (U.S.)

- Ambra Health, Inc., (U.S.)

- Intelerad Medical Systems Incorporated, (Canada)

- RamSoft Inc., (Canada)

- GE HealthCare (U.S.)

- Koninklijke Philips N.V. (U.S.)

- FUJIFILM Medical Systems (U.S.)

- Siemens Medical Solutions (U.S.)

- Agfa HealthCare Corporation, (Canada)

- Carestream Health, Inc., (U.S.)

- Aidoc Medical, Inc., (U.S.)

- Viz.ai, Inc., (U.S.)

What are the Recent Developments in Asia-Pacific Teleradiology Market?

- In October 2025, Asia-Pacific AI-assisted imaging market expanded rapidly supporting teleradiology growth. The Asia-Pacific region saw strong acceleration in AI-assisted imaging adoption across healthcare systems, including radiology workflows. Hospitals increasingly integrated AI tools for image analysis, triage, and diagnostic support, strengthening remote radiology capabilities.

- In July 2025, India announced state-wide teleradiology hub expansion for government hospitals. India’s health department announced the development of a state-wide teleradiology hub across government hospitals in phases, connecting district hospitals and primary health centers through digital radiology networks. The initiative includes integration of MRI, CT, and X-ray reporting systems to improve diagnostic access in rural and semi-urban areas

- In April 2025, Asia-Pacific teleradiology expansion strengthened through rapid cloud PACS adoption. Hospitals and imaging networks across Asia-Pacific significantly expanded the use of cloud-based PACS integrated teleradiology systems to support remote diagnostic workflows. The adoption enabled real-time sharing of CT, MRI, and X-ray images between hospitals and off-site radiologists, improving turnaround times

- In March 2025, India-based AI teleradiology system deployed across multi-site hospital networks. A large-scale AI-driven radiology system was deployed across 17 healthcare systems in India, processing over 150,000 scans with autonomous analysis support. The system used advanced deep learning models to detect multiple pathologies from chest X-rays with high accuracy

- In January 2025, Philips launched AI-enabled CT 5300 system enhancing advanced imaging and remote diagnostic workflows. Royal Philips introduced its AI-enabled CT 5300 system at the Asian Oceanian Congress of Radiology (AOCR) 2025, designed to improve diagnostic precision, workflow efficiency, and remote imaging support for healthcare providers

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.