Canada Fleet Electrification As A Service Feaas Market

Market Size in USD Million

USD

650.58 Million

USD

3,622.28 Million

2025

2033

USD

650.58 Million

USD

3,622.28 Million

2025

2033

| 2026 - 2033 | |

| USD 650.58 Million | |

| USD 3,622.28 Million | |

| % | |

|

Canada Fleet Electrification as a Service (FEaaS) Market Size

- The Canada Fleet Electrification as a Service (FEaaS) Market size was valued at USD 3,622.28 million by 2033 from USD 650.58 million in 2025, growing with a CAGR of 24.3% during the forecast period

- The Canada Fleet Electrification as a Service Market is experiencing steady growth, driven by increasing demand from commercial fleet operators, logistics providers, public transit agencies, and corporate mobility companies seeking cost-effective and sustainable transportation solutions, supported by Canada’s strong decarbonization commitments.

- Rising investments in EV charging infrastructure, grid modernization, battery management systems, and renewable energy integration—along with federal and provincial incentives promoting zero-emission vehicles—are significantly accelerating fleet transition from internal combustion engines to electric platforms across the country.

- Advancements in telematics, energy management software, smart charging technologies, and vehicle-to-grid integration, coupled with expanding partnerships between utilities, technology providers, and fleet operators, are enhancing operational efficiency and enabling scalable, long-term fleet electrification deployment models across Canada.

Canada Fleet Electrification as a Service (FEaaS) Market Analysis

- The Canada Fleet Electrification as a Service (FEaaS) Market is experiencing steady growth, driven by rising demand from logistics providers, municipal transit agencies, corporate fleets, and last-mile delivery operators, supported by national net-zero targets, expanding EV infrastructure, and increasing adoption of zero-emission mobility solutions across industries.

- Growth is further reinforced by supportive government policies, decarbonization mandates, and increasing investments in charging infrastructure and smart energy management solutions across provinces.

- The Medium-Duty Vehicles (MDVs) (Class 4–6) segment leads the market, holding a 46.35% share in 2025, driven by high utilization rates, predictable route patterns, and strong suitability for urban and regional logistics operations.

- MDVs are particularly attractive for fleet operators due to optimized charging cycles, lower total cost of ownership, and reliable operational performance in high-density delivery environments.

- The dominance of the MDVs segment is supported by its cost-effectiveness, reduced upfront capital requirements, and seamless integration of vehicles, charging infrastructure, maintenance, and energy management services, making it the preferred choice for large-scale commercial and municipal fleet deployments across Canada.

Report Scope and Canada Fleet Electrification as a Service (FEaaS) Market Segmentation

|

Attributes |

Canada Fleet Electrification as a Service (FEaaS) Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Canada Fleet Electrification as a Service (FEaaS) Market Trends

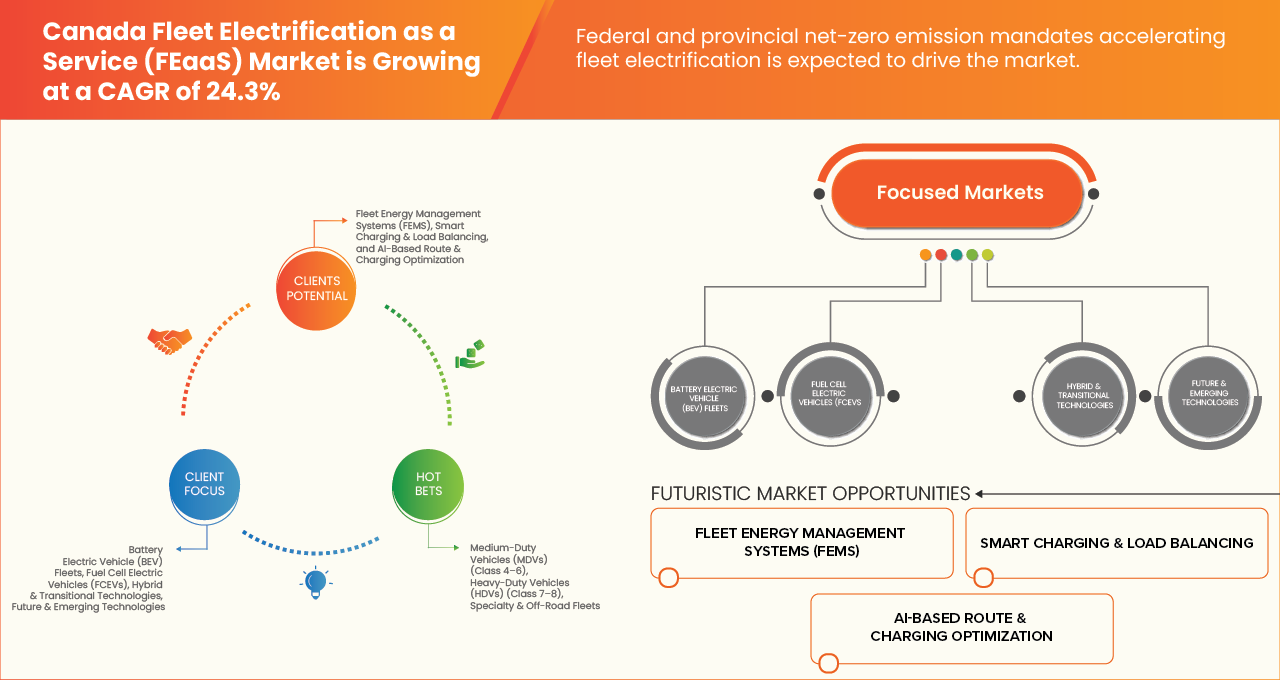

“Federal and provincial net-zero emission mandates accelerating fleet electrification”

- Federal and provincial net-zero emission mandates in Canada are functioning as a structural catalyst for the Canada Fleet Electrification as a Service (FaaS) market by institutionalizing demand for zero-emission vehicles (ZEVs), accelerating public and commercial fleet transition timelines, and embedding compliance obligations into procurement, infrastructure, and operational planning frameworks.

- Through legislated sales targets, clean fuel standards, carbon pricing mechanisms, and direct public fleet decarbonization commitments, Canadian authorities are shifting fleet electrification from a voluntary sustainability initiative to a regulatory and financial imperative.

- This regulatory certainty enhances long-term visibility for service providers offering bundled solutions encompassing vehicle procurement, charging infrastructure deployment, energy management, financing, telematics integration, and lifecycle optimization, thereby reinforcing the commercial viability and scalability of fleet electrification as a managed service model across municipal, transit, logistics, and government-operated fleets.

Canada Fleet Electrification as a Service (FEaaS) Market Dynamics

Driver

“Rising diesel price volatility improving electric fleet total cost of ownership”

- Rising diesel price volatility across Canada is materially strengthening the economic rationale for fleet electrification and accelerating adoption of Fleet Electrification as a Service (FaaS) models.

- Persistent fluctuations in global crude markets, geopolitical supply disruptions, refinery constraints, and carbon pricing escalations have introduced cost unpredictability for commercial fleet operators dependent on diesel. In contrast, electricity pricing frameworks in most Canadian provinces are comparatively regulated and stable, enabling improved forecasting of operating expenditures.

- This widening predictability gap enhances the total cost of ownership profile of electric fleets, particularly when integrated with managed charging, energy optimization, and lifecycle analytics offered under service-based electrification models.

- As a result, diesel market instability is not only influencing procurement decisions but also driving demand for bundled electrification solutions that mitigate fuel cost exposure, optimize charging schedules, and provide structured financial visibility over multi-year fleet operations.

For instance:

- In February 2026, the Province of British Columbia published official fuel price adjustment schedules for hired equipment that explicitly account for monthly fuel price changes, demonstrating government acknowledgment of fuel cost volatility impacting vehicle operating rates

- In May 2025, Corporate Fleet Services prepared a Fuel Price Update report for the Treasury Board of Canada Secretariat, noting that global crude price volatility persisted in recent months and directly influenced average fuel costs used to calculate operating cost components in government fleet reimbursement rates.

- In January 2025, Natural Resources Canada published national weekly diesel prices for 45 Canadian cities, reflecting ongoing price changes in transportation fuels that fleet operators must manage when estimating operating expenditures and fuel budgets.

- Sustained diesel price volatility, compounded by carbon pricing mechanisms and global crude market fluctuations, is increasing cost uncertainty for fleet operators while comparatively stable electricity pricing enhances long-term operating expenditure predictability.

Restraint/Challenge

“High upfront capital requirements for charging infrastructure deployment”

- High upfront capital requirements associated with charging infrastructure deployment represent a material restraint to the growth of the Canada Fleet Electrification as a Service (FaaS) market. While vehicle acquisition costs are progressively declining through scale and incentives, fleet electrification projects require substantial parallel investment in depot-based charging systems, grid interconnection upgrades, transformer capacity expansion, civil works, energy management systems, and software integration.

- For medium- and heavy-duty fleets in particular, demand charges, site redesign, and utility coordination introduce additional financial and operational complexity.

- These capital-intensive prerequisites can delay project approvals, constrain small and mid-sized fleet participation, and increase reliance on third-party financing or service-based models.

- In February 2026, the Government of Canada announced a federal funding package under the Zero Emission Vehicle Infrastructure Program directed to install thousands of EV chargers across the country, implicitly recognizing that public investment is necessary to bridge funding shortfalls and catalyze private sector deployment due to the high upfront costs of charging infrastructure.

- In January 2025, Natural Resources Canada published a resource on Electric Vehicle Charging Infrastructure for Canada that discusses projected capital requirements for medium- and heavy-duty vehicle charging infrastructure deployment, underscoring large investment needs to build out charging systems at scale for commercial fleets

- In December 2024, OSLER article published stated that legal and policy analysts reviewing Canada’s EV ecosystem noted that despite federal programs subsidizing a portion of charging station costs, a significant “charger gap” remains with only tens of thousands of public ports installed against much larger projected needs by 2040, reflecting the high capital intensity and scale of infrastructure expansion required.

- The substantial capital outlay required for charging infrastructure—including grid upgrades, site preparation, hardware installation, and energy management systems—continues to constrain the pace and breadth of fleet electrification across Canada. While public funding programs and service-based financing models alleviate part of the burden, infrastructure scale requirements and associated demand charges remain financially intensive, particularly for medium- and heavy-duty fleets.

Canada Fleet Electrification as a Service (FEaaS) Market Scope

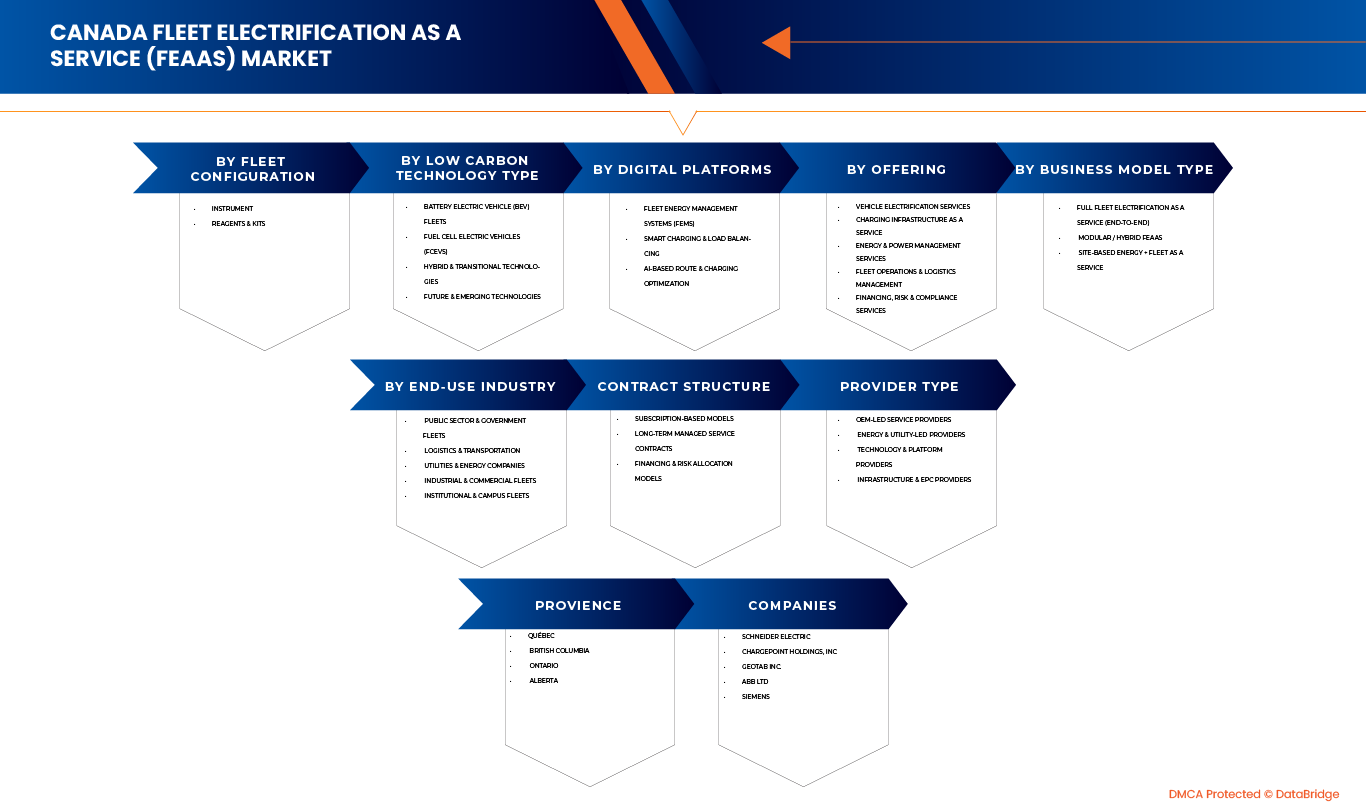

The canada fleet electrification as a service market is segmented into nine notable segments, which are based on fleet configuration, low-carbon technology type, digital platforms, offering, business model type, end-use industry, contract structure, provider type, province.

By Fleet Configuration

On the basis of fleet configuration, the Canada Fleet Electrification as a Service Market is segmented into Medium-Duty Vehicles (MDVs) (Class 4–6), Heavy-Duty Vehicles (HDVs) (Class 7–8), and Specialty & Off-Road Fleets.

In 2026, the Medium-Duty Vehicles (MDVs) (Class 4–6) segment is anticipated to dominate the market with a 46.21% market share, due to its critical role in urban logistics, last-mile delivery, municipal services, and regional distribution operations. Their predictable routes, centralized depot charging suitability, and high daily utilization make them ideal for electrification under service-based models, enabling cost optimization, operational efficiency, and emissions reduction.

The Heavy-Duty Vehicles (HDVs) (Class 7–8) segment is expected to grow the fastest, registering a CAGR of 24.9% from 2026 to 2033, driven by accelerating investments in high-capacity charging infrastructure, advancements in battery range and performance, expanding government incentives for zero-emission freight transport, and increasing commitments from large logistics and industrial fleet operators to decarbonize long-haul and high-load transportation operations..

By Digital Platforms

On the basis of digital platforms, the Canada Fleet Electrification as a Service Market is segmented into Fleet Energy Management Systems (FEMS), Smart Charging & Load Balancing, and AI-Based Route & Charging Optimization.

In 2026, the Fleet Energy Management Systems (FEMS) segment is anticipated to dominate the market with a 42.82% share, driven by its critical role in monitoring real-time energy consumption, optimizing fleet charging schedules, reducing operational costs, and ensuring grid stability across large and medium-sized fleet operations.

The Smart Charging & Load Balancing segment is expected to grow the fastest, with a CAGR of 24.7% from 2026 to 2033, fueled by rising adoption of dynamic load management solutions, increasing integration of renewable energy sources, and the need for intelligent distribution of charging across depots to prevent grid congestion while maximizing vehicle availability and operational efficiency

By Offering

On the basis of offering, the Canada Fleet Electrification as a Service Market is segmented into Vehicle Electrification Services, Charging Infrastructure as a Service, Energy & Power Management Services, Fleet Operations & Logistics Management, and Financing, Risk & Compliance Services.

In 2026, the Vehicle Electrification Services segment is anticipated to dominate the market with a 31.44% share, driven by its critical role in providing end-to-end electric vehicle deployment, conversion, and retrofitting solutions for medium- and heavy-duty fleets, enabling cost-effective and rapid fleet decarbonization.

The Charging Infrastructure as a Service segment is expected to grow the fastest, registering a CAGR of 24.7% from 2026 to 2033, fueled by increasing deployment of smart charging stations, government incentives for zero-emission fleets, rising adoption of depot and public charging solutions, and the need for scalable, managed infrastructure that supports efficient energy distribution and maximizes vehicle uptime.

By Business Model Type

On the basis of business model type, the Canada Fleet Electrification as a Service (FEaaS) Market is segmented into Full Fleet Electrification as a Service (End-to-End), Modular / Hybrid FEaaS, and Site-Based Energy + Fleet as a Service.

In 2026, the Full Fleet Electrification as a Service (End-to-End) segment is anticipated to dominate the market with a 48.60% share, driven by its ability to offer comprehensive solutions covering vehicle procurement, charging infrastructure, energy management, maintenance, and operational support, making it the preferred choice for large fleets seeking complete decarbonization with minimal upfront investment.

The Site-Based Energy + Fleet as a Service segment is expected to grow the fastest, registering a CAGR of 24.7% from 2026 to 2033, fueled by rising adoption of integrated energy and fleet management solutions, increasing investments in on-site renewable energy generation, smart microgrid deployment, and demand for flexible, modular services that allow fleets to scale electrification based on operational and energy requirements.

By End User Industry

On the basis of end-use industry, the Canada Fleet Electrification as a Service Market is segmented into Public Sector & Government Fleets, Logistics & Transportation, Utilities & Energy Companies, Industrial & Commercial Fleets, and Institutional & Campus Fleets.

In 2026, the Logistics & Transportation segment is anticipated to dominate the market with a 31.99% share, driven by the high adoption of electric medium- and heavy-duty vehicles for last-mile delivery, regional distribution, and freight operations, where operational efficiency, lower total cost of ownership, and emission reduction are critical.

The Utilities & Energy Companies segment is expected to grow the fastest, registering a CAGR of 24.8% from 2026 to 2033, fueled by increasing deployment of electrified service and maintenance fleets, integration with renewable energy and smart grid operations, and rising commitments from energy providers to decarbonize field operations while enhancing sustainability and operational reliability.

By Contract Structure

On the basis of contract structure, the Canada Fleet Electrification as a Service Market is segmented into Subscription-Based Models, Long-Term Managed Service Contracts, and Financing & Risk Allocation Models.

In 2026, the Subscription-Based Models segment is anticipated to dominate the market with a 39.87% share, driven by its ability to provide fleets with predictable monthly costs, minimal upfront investment, and access to end-to-end electrification services—including vehicles, charging infrastructure, energy management, and maintenance—making it highly attractive for commercial and municipal operators.

The Financing & Risk Allocation Models segment is expected to grow the fastest, registering a CAGR of 24.6% from 2026 to 2033, fueled by increasing adoption of flexible financing solutions, shared investment structures, and risk mitigation strategies that allow fleet operators to scale electrification initiatives while managing capital expenditures, battery lifecycle risks, and operational uncertainties.

By Provider Type

On the basis of provider type, the Canada Fleet Electrification as a Service Market is segmented into OEM-Led Service Providers, Energy & Utility-Led Providers, Technology & Platform Providers, and Infrastructure & EPC Providers.

In 2026, the OEM-Led Service Providers segment is anticipated to dominate the market with a 36.18% share, driven by their ability to offer integrated electrification solutions, including vehicle supply, fleet management, and maintenance services, leveraging brand expertise, warranties, and established service networks to ensure reliability and efficiency for fleet operators.

The Energy & Utility-Led Providers segment is expected to grow the fastest, registering a CAGR of 25.5% from 2026 to 2033, fueled by increasing investments in smart charging infrastructure, grid management solutions, and renewable energy integration, enabling fleets to optimize energy usage, reduce operational costs, and achieve sustainability targets

By Province

On the basis of province, the Canada Fleet Electrification as a Service Market is segmented into Québec, British Columbia, Ontario, and Alberta.

In 2026, the Québec segment is anticipated to dominate the market with a 40.21% share, driven by strong provincial policies promoting zero-emission vehicles, extensive EV charging infrastructure, and high adoption of electric fleets by public sector, logistics, and commercial operators.

The Ontario segment is expected to grow the fastest, registering a CAGR of 24.9% from 2026 to 2033, fueled by increasing fleet electrification initiatives in urban centers, rising investments in smart charging networks, and growing corporate and municipal commitments to decarbonize medium- and heavy-duty vehicles across the province.

Canada Fleet Electrification as a Service (FEaaS) Market Share

The Fleet Electrification as a Service (FEaaS) industry is primarily led by well-established companies, including:

- 7Gen (Canada)

- Jim Pattison Lease (Canada)

- ENGIE (France)

- Comco Canada Ltd. (Canada)

- Ziing (Canada)

- Shell plc (U.K.)

- LION ELECTRIC (FLEET SOLUTIONS) (Canada)

- Zeemac (Canada)

- ELECTRAMECCANICA (COMMERCIAL EV SOLUTIONS) (Canada)

- Hitachi Energy Ltd (Switzerland)

- Schneider Electric (France)

- ABB (Switzerland)

- Siemens (Germany)

- BC Hydro (Canada)

- ChargePoint, Inc. (U.S.)

- eCAMION Inc. (Canada)

- Teal Electrification Systems (Canada)

- Geotab Inc. (Canada)

- Hydro One Networks Inc. (Canada)

- InCharge Energy (U.S.)

- PowerON Energy Solutions (Canada)

- Merchants Fleet (U.S.)

- Ryder System, Inc. (U.S.)

Latest Developments in Canada Fleet Electrification as a Service (FEaaS) Market

- In January 2025, ChargePoint has teamed up with Midwestern Wheels, a licensee of Avis Budget Group, to install new public EV charging stations at rental car locations in Appleton and Madison, Wisconsin, making it easier for both rental customers and local EV drivers to charge their vehicles. The installations feature a mix of AC and DC stations and include ChargePoint’s Omni Port technology, which lets different EV models charge in any parking space without needing adapters, helping future-proof the infrastructure. These stations are managed through the new ChargePoint Platform, which provides real-time insights and remote performance monitoring to ensure chargers remain functional and responsive to user needs.

- In March 2025, AVAIO Digital has joined forces with Schneider Electric to secure essential data center infrastructure, including switchgear, power distribution units (PDUs), uninterruptible power supplies (UPSs), and cooling systems, for the development of four state-of-the-art AI ready data centers in the United States. This collaboration highlights Schneider Electric’s pivotal role in supporting the next generation of data center construction, providing the advanced electrical and thermal management solutions necessary to handle high-density compute workloads and AI-driven applications, while ensuring operational efficiency, reliability, and scalability.

- In January 2025 siemens introduced advanced industrial AI and digital twin technologies designed to enhance operational efficiency with real-time decision-making. They launched the Siemens Industrial Co-pilot for Operations, bringing AI directly to the shop floor. Siemens also announced a partnership with Jet Zero to develop a fuel-efficient, zero-emission blended-wing aircraft. These innovations highlight Siemens’ focus on driving sustainability and digital transformation across industries.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Table of Content

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW OF CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET

1.4 LIMITATIONS

1.5 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 MARKETS COVERED

2.2 GEOGRAPHICAL SCOPE

2.3 YEARS CONSIDERED FOR THE STUDY

2.4 CURRENCY AND PRICING

2.5 DBMR TRIPOD DATA VALIDATION MODEL

2.6 MULTIVARIATE MODELLING

2.7 PRIMARY INTERVIEWS WITH KEY OPINION LEADERS

2.8 DBMR MARKET POSITION GRID

2.9 MARKET END USER COVERAGE GRID

2.1 SECONDARY SOURCES

2.11 ASSUMPTIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 INDUSTRIAL AUTOMATION ADOPTION

4.2 TECHNOLIGICAL ADVANCEMENT

4.3 CASE STUDY ANALYSIS

4.3.1 FLEET CHARACTERISTICS & CASE SUBJECT

4.3.2 OPERATIONAL MODELING

4.3.3 CHARGING STRATEGY & INFRASTRUCTURE

4.3.4 COST & FINANCIAL ANALYSIS

4.3.5 SENSITIVITY & ROBUSTNESS CHECKS

4.3.6 BARRIERS & PRACTICAL CONSIDERATIONS

4.3.7 KEY FINDINGS & IMPLICATIONS

4.4 PRICING ANALYSIS

4.5 COMPANY COMPARATIVE ANALYSIS: SOLUTION ADOPTION VS ROI

4.5.1 7GEN – INTEGRATED FEAAS MODEL (IKEA CANADA CASE)

4.5.2 SOLUTION ADOPTION

4.5.2.1 ROI ANALYSIS

4.5.3 GEOTAB – DATA-LED ELECTRIFICATION (NB POWER CASE)

4.5.3.1 SOLUTION ADOPTION

4.5.3.2 ROI OUTCOMES

4.5.4 ABB – HEAVY-DUTY TRANSIT INFRASTRUCTURE (TTC CASE)

4.5.4.1 SOLUTION ADOPTION

4.5.4.2 ROI ANALYSIS

4.5.5 SIEMENS – DEPOT360 MANAGED ELECTRIFICATION MODEL

4.5.5.1 SOLUTION ADOPTION

4.5.5.2 ROI ANALYSIS

4.5.6 CHARGEPOINT – NETWORKED CHARGING & SUBSCRIPTION MODEL

4.5.6.1 SOLUTION ADOPTION

4.5.6.2 OI ANALYSIS

4.5.7 STRATEGIC INTERPRETATION FOR CANADA FEAAS MARKET

4.6 CONSUMER BUYING BEHAVIOUR

4.6.1 GROUP 1 MISSION-CRITICAL & STRATEGIC USERS

4.6.2 GROUP 2 PROFESSIONAL & COMMERCIAL OPERATORS

4.6.3 GROUP 3 COST-CONSCIOUS INDUSTRIAL USERS

4.6.4 GROUP 4 VOLUME-DRIVEN COMMERCIAL BUYERS

4.6.5 GROUP 5 RESEARCH & INNOVATION-FOCUSED INSTITUTIONS

4.6.6 GROUP 6 ENTRY-LEVEL & BUDGET-FOCUSED USERS

5 MARKET OVERVIEW

5.1 DRIVER

5.1.1 FEDERAL AND PROVINCIAL NET-ZERO EMISSION MANDATES ACCELERATING FLEET ELECTRIFICATION

5.1.2 RISING DIESEL PRICE VOLATILITY IMPROVING ELECTRIC FLEET TOTAL COST OF OWNERSHIP

5.1.3 INCREASING CORPORATE ESG AND DECARBONIZATION COMMITMENTS ACROSS LOGISTICS AND RETAIL SECTORS

5.2 RESTRAINT

5.2.1 HIGH UPFRONT CAPITAL REQUIREMENTS FOR CHARGING INFRASTRUCTURE DEPLOYMENT

5.2.2 PERFORMANCE CONCERNS OF ELECTRIC VEHICLES IN EXTREME COLD CLIMATES

5.3 OPPORTUNITIES

5.3.1 INTEGRATION OF SMART CHARGING, LOAD MANAGEMENT, AND VEHICLE-TO-GRID TECHNOLOGIES

5.3.2 PARTNERSHIP MODELS WITH UTILITIES FOR ENERGY-ALIGNED FLEET DEPLOYMENT

5.3.3 PUBLIC TRANSIT AND MUNICIPAL FLEET ELECTRIFICATION SERVICE CONTRACTS

5.4 CHALLENGES

5.4.1 PROVINCIAL REGULATORY VARIATIONS IMPACTING INCENTIVE ACCESSIBILITY

5.4.2 RID INTERCONNECTION DELAYS AND UTILITY COORDINATION COMPLEXITIES

6 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY FLEET CONFIGURATION,

6.1 OVERVIEW

6.2 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, 2018-2033 (USD THOUSAND)

6.3 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY FLEET CONFIGURATION, 2018-2033 (USD THOUSAND)

6.3.1 MEDIUM-DUTY VEHICLES (MDVS) (CLASS 4–6)

6.3.2 HEAVY-DUTY VEHICLES (HDVS) (CLASS 7–8)

6.3.3 SPECIALTY & OFF-ROAD FLEETS

6.4 MEDIUM-DUTY VEHICLES (MDVS) (CLASS 4–6) IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

6.4.1 PARCEL & POSTAL DELIVERY VANS

6.4.2 MUNICIPAL SERVICE VEHICLES

6.4.3 UTILITY SERVICE TRUCKS

6.5 HEAVY-DUTY VEHICLES (HDVS) (CLASS 7–8) IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

6.5.1 REGIONAL HAUL TRUCKS

6.5.2 LONG-HAUL TRUCKS

6.5.3 REFUSE & WASTE COLLECTION TRUCKS

6.5.4 TRANSIT & SCHOOL BUSES

6.5.5 CONSTRUCTION & VOCATIONAL TRUCKS

7 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY LOW-CARBON TECHNOLOGY TYPE

7.1 OVERVIEW

7.2 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY LOW-CARBON TECHNOLOGY TYPE, 2018-2033 (USD THOUSAND)

7.2.1 BATTERY ELECTRIC VEHICLE (BEV) FLEETS

7.2.2 FUEL CELL ELECTRIC VEHICLES (FCEVS)

7.2.3 HYBRID & TRANSITIONAL TECHNOLOGIES

7.2.4 FUTURE & EMERGING TECHNOLOGIES

7.3 BATTERY ELECTRIC VEHICLE (BEV) FLEETS IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

7.3.1 DEPOT-CHARGED BEVS

7.3.2 OPPORTUNITY-CHARGED BEVS

7.3.3 OVERNIGHT CHARGING MODELS

7.3.4 HIGH-UTILIZATION URBAN BEVS

7.4 FUEL CELL ELECTRIC VEHICLES (FCEVS) IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

7.4.1 HYDROGEN TRANSIT FLEETS

7.4.2 LONG-HAUL HYDROGEN TRUCKS

7.4.3 PORT & INDUSTRIAL FLEETS

7.5 HYBRID & TRANSITIONAL TECHNOLOGIES IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

7.5.1 PLUG-IN HYBRID ELECTRIC (PHEV) MHDVS

7.5.2 RANGE-EXTENDED ELECTRIC TRUCKS

7.5.3 ICE RETROFIT + ELECTRIFICATION KITS

7.6 FUTURE & EMERGING TECHNOLOGIES IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

7.6.1 BATTERY-SWAPPING FLEETS

7.6.2 VEHICLE-TO-GRID (V2G) ENABLED FLEETS

7.6.3 AUTONOMOUS ELECTRIC FREIGHT VEHICLES

8 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY DIGITAL PLATFORMS,

8.1 OVERVIEW

8.2 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY DIGITAL PLATFORMS, 2018-2033 (USD THOUSAND)

8.2.1 FLEET ENERGY MANAGEMENT SYSTEMS (FEMS)

8.2.2 SMART CHARGING & LOAD BALANCING

8.2.3 AI-BASED ROUTE & CHARGING OPTIMIZATION

9 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY OFFERING,

9.1 OVERVIEW

9.2 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY OFFERING, 2018-2033 (USD THOUSAND)

9.2.1 VEHICLE ELECTRIFICATION SERVICES

9.2.2 CHARGING INFRASTRUCTURE AS A SERVICE

9.2.3 ENERGY & POWER MANAGEMENT SERVICES

9.2.4 FLEET OPERATIONS & LOGISTICS MANAGEMENT

9.2.5 FINANCING, RISK & COMPLIANCE SERVICES

9.3 VEHICLE ELECTRIFICATION SERVICES IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

9.3.1 BATTERY ELECTRIC VEHICLE (BEV) FLEET CONVERSION

9.3.2 FUEL CELL ELECTRIC VEHICLE (FCEV) INTEGRATION (LIMITED PILOTS IN CANADA)

9.3.3 PLUG-IN HYBRID MHDV TRANSITION (BRIDGE SOLUTIONS)

9.3.4 VEHICLE RIGHT-SIZING AND ROUTE SUITABILITY ANALYSIS

9.3.5 OEM-AGNOSTIC VS OEM-PARTNERED PROCUREMENT MODELS

9.4 CHARGING INFRASTRUCTURE AS A SERVICE IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

9.4.1 DEPOT CHARGING DESIGN & ENGINEERING

9.4.2 ON-SITE LEVEL 2 VS DC FAST CHARGING DEPLOYMENT

9.4.3 GRID CONNECTION & UTILITY COORDINATION

9.4.4 MOBILE AND TEMPORARY CHARGING SOLUTIONS

9.4.5 PUBLIC–PRIVATE CHARGING ACCESS MODELS

9.5 ENERGY & POWER MANAGEMENT SERVICES IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

9.5.1 LOAD MANAGEMENT & DEMAND RESPONSE

9.5.2 ENERGY MANAGEMENT SYSTEMS (EMS)

9.5.3 PEAK SHAVING AND TIME-OF-USE OPTIMIZATION

9.5.4 RENEWABLE ENERGY INTEGRATION (SOLAR + STORAGE)

9.5.5 VEHICLE-TO-GRID (V2G) PILOTS

9.6 FLEET OPERATIONS & LOGISTICS MANAGEMENT IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

9.6.1 ROUTE OPTIMIZATION FOR EV RANGE

9.6.2 CHARGING SCHEDULING & FLEET DISPATCH TOOLS

9.6.3 TELEMATICS & REAL-TIME MONITORING

9.6.4 PREDICTIVE MAINTENANCE

9.6.5 DRIVER TRAINING & CHANGE MANAGEMENT

9.7 FINANCING, RISK & COMPLIANCE SERVICES IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

9.7.1 CAPEX-TO-OPEX CONVERSION MODELS

9.7.2 BATTERY PERFORMANCE GUARANTEES

9.7.3 RESIDUAL VALUE & END-OF-LIFE MANAGEMENT

9.7.4 REGULATORY COMPLIANCE MANAGEMENT

9.7.5 CARBON ACCOUNTING & ESG REPORTING

10 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY BUSINESS MODEL TYPE

10.1 OVERVIEW

10.2 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY BUSINESS MODEL TYPE, 2018-2033 (USD THOUSAND)

10.2.1 FULL FLEET ELECTRIFICATION AS A SERVICE (END-TO-END)

10.2.2 MODULAR / HYBRID FEAAS

10.2.3 SITE-BASED ENERGY + FLEET AS A SERVICE

11 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY END-USE INDUSTRY,

11.1 OVERVIEW

11.2 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY END-USE INDUSTRY, 2018-2033 (USD THOUSAND)

11.2.1 PUBLIC SECTOR & GOVERNMENT FLEETS

11.2.2 LOGISTICS & TRANSPORTATION

11.2.3 UTILITIES & ENERGY COMPANIES

11.2.4 INDUSTRIAL & COMMERCIAL FLEETS

11.2.5 INSTITUTIONAL & CAMPUS FLEETS

11.3 PUBLIC SECTOR & GOVERNMENT FLEETS IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

11.3.1 MUNICIPAL FLEETS

11.3.2 PROVINCIAL & FEDERAL FLEETS

11.3.3 TRANSIT AUTHORITIES

11.3.4 CROWN CORPORATIONS

11.4 LOGISTICS & TRANSPORTATION IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

11.4.1 PARCEL & EXPRESS DELIVERY

11.4.2 REGIONAL FREIGHT OPERATORS

11.4.3 PORT & INTERMODAL FLEETS

11.5 UTILITIES & ENERGY COMPANIES IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

11.5.1 ELECTRICITY UTILITIES

11.5.2 GAS UTILITIES (TRANSITION FLEETS)

11.5.3 GRID SERVICE PROVIDERS

11.6 INDUSTRIAL & COMMERCIAL FLEETS IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

11.6.1 CONSTRUCTION & MINING

11.6.2 WASTE MANAGEMENT

11.6.3 FOOD & BEVERAGE DISTRIBUTION

11.7 INSTITUTIONAL & CAMPUS FLEETS IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

11.7.1 UNIVERSITIES

11.7.2 HOSPITALS

11.7.3 AIRPORTS

11.7.4 PORTS

12 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY CONTRACT STRUCTURE,

12.1 OVERVIEW

12.2 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY CONTRACT STRUCTURE, 2018-2033 (USD THOUSAND)

12.2.1 SUBSCRIPTION-BASED MODELS

12.2.2 LONG-TERM MANAGED SERVICE CONTRACTS

12.2.3 FINANCING & RISK ALLOCATION MODELS

12.3 SUBSCRIPTION-BASED MODELS IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

12.3.1 PER-VEHICLE MONTHLY FEE

12.3.2 PER-MILE OR PER-KWH PRICING

12.3.3 PERFORMANCE-BASED PRICING

12.4 LONG-TERM MANAGED SERVICE CONTRACTS IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

12.4.1 5–15 YEAR FLEET CONTRACTS

12.4.2 GUARANTEED TCO CONTRACTS

12.4.3 SLA-DRIVEN UPTIME AGREEMENTS

12.5 FINANCING & RISK ALLOCATION MODELS IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

12.5.1 PROVIDER-OWNED ASSETS

12.5.2 SHARED SAVINGS MODELS

12.5.3 CARBON CREDIT MONETIZATION

13 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY PROVIDER TYPE,

13.1 OVERVIEW

13.2 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY PROVIDER TYPE, 2018-2033 (USD THOUSAND)

13.2.1 OEM-LED SERVICE PROVIDERS

13.2.2 ENERGY & UTILITY-LED PROVIDERS

13.2.3 TECHNOLOGY & PLATFORM PROVIDERS

13.2.4 INFRASTRUCTURE & EPC PROVIDERS

13.3 OEM-LED SERVICE PROVIDERS IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

13.3.1 TRUCK OEM ELECTRIFICATION ARMS

13.3.2 OEM FINANCIAL SERVICES

13.4 ENERGY & UTILITY-LED PROVIDERS IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

13.4.1 UTILITIES OFFERING FLEET SERVICES

13.4.2 ENERGY-AS-A-SERVICE PROVIDERS

13.5 TECHNOLOGY & PLATFORM PROVIDERS IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

13.5.1 CHARGING NETWORK OPERATORS

13.5.2 FLEET SOFTWARE COMPANIES

13.6 INFRASTRUCTURE & EPC PROVIDERS IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

13.6.1 CHARGING EPCS

13.6.2 GRID INTERCONNECTION SPECIALISTS

14 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY PROVINCE

14.1 OVERVIEW

14.2 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY PROVINCE, 2018-2033 (USD THOUSAND)

14.2.1 QUÉBEC

14.2.2 BRITISH COLUMBIA

14.2.3 ONTARIO

14.2.4 ALBERTA

15 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, COMPANY LANDSCAPE

15.1 COMPANY SHARE ANALYSIS: CANADA

16 SWOT ANALYSIS

17 COMPANY PROFILES

17.1 ABB

17.1.1 COMPANY SNAPSHOT

17.1.2 REVENUE ANALYSIS

17.1.3 PRODUCT PORTFOLIO

17.1.4 RECENT DEVELOPMENT

17.2 SIEMENS

17.2.1 COMPANY SNAPSHOT

17.2.2 REVENUE ANALYSIS

17.2.3 PRODUCT PORTFOLIO

17.2.4 RECENT DEVELOPMENT

17.3 LION ELECTRIC (FLEET SOLUTIONS)

17.3.1 COMPANY SNAPSHOT

17.3.2 PRODUCT PORTFOLIO

17.3.3 RECENT DEVELOPMENT

17.4 CHARGEPOINT, INC.

17.4.1 COMPANY SNAPSHOT

17.4.2 REVENUE ANALYSIS

17.4.3 PRODUCT PORTFOLIO

17.4.4 RECENT DEVELOPMENT

17.5 SCHNEIDER ELECTRIC

17.5.1 COMPANY SNAPSHOT

17.5.2 REVENUE ANALYSIS

17.5.3 PRODUCT PORTFOLIO

17.5.4 RECENT DEVELOPMENT

17.6 7GEN

17.6.1 COMPANY SNAPSHOT

17.6.2 PRODUCT PORTFOLIO

17.6.3 RECENT DEVELOPMENT

17.7 BC HYDRO

17.7.1 COMPANY SNAPSHOT

17.7.2 PRODUCT PORTFOLIO

17.7.3 RECENT DEVELOPMENT

17.8 COMCO CANADA LTD.

17.8.1 COMPANY SNAPSHOT

17.8.2 PRODUCT PORTFOLIO

17.8.3 RECENT DEVELOPMENT

17.9 ECAMION INC.

17.9.1 COMPANY SNAPSHOT

17.9.2 PRODUCT PORTFOLIO

17.9.3 RECENT DEVELOPMENT

17.1 ELECTRAMECCANICA (COMMERCIAL EV SOLUTIONS)

17.10.1 COMPANY SNAPSHOT

17.10.2 PRODUCT PORTFOLIO

17.10.3 RECENT DEVELOPMENT

17.11 ENGIE

17.11.1 COMPANY SNAPSHOT

17.11.2 REVENUE ANALYSIS

17.11.3 PRODUCT PORTFOLIO

17.11.4 RECENT DEVELOPMENT

17.12 GEOTAB INC.

17.12.1 COMPANY SNAPSHOT

17.12.2 PRODUCT PORTFOLIO

17.12.3 RECENT DEVELOPMENT

17.13 HITACHI ENERGY LTD

17.13.1 COMPANY SNAPSHOT

17.13.2 PRODUCT PORTFOLIO

17.13.3 RECENT DEVELOPMENT

17.14 HYDRO ONE NETWORKS INC.

17.14.1 COMPANY SNAPSHOT

17.14.2 REVENUE ANALYSIS

17.14.3 PRODUCT PORTFOLIO

17.14.4 RECENT DEVELOPMENT

17.15 INCHARGE ENERGY

17.15.1 COMPANY SNAPSHOT

17.15.2 PRODUCT PORTFOLIO

17.15.3 RECENT DEVELOPMENT

17.16 JIM PATTISON LEASE

17.16.1 COMPANY SNAPSHOT

17.16.2 PRODUCT PORTFOLIO

17.16.3 RECENT DEVELOPMENT

17.17 MERCHANTS FLEET

17.17.1 COMPANY SNAPSHOT

17.17.2 PRODUCT PORTFOLIO

17.17.3 RECENT DEVELOPMENT

17.18 POWERON ENERGY SOLUTIONS

17.18.1 COMPANY SNAPSHOT

17.18.2 PRODUCT PORTFOLIO

17.18.3 RECENT DEVELOPMENT

17.19 RYDER SYSTEM, INC.

17.19.1 COMPANY SNAPSHOT

17.19.2 REVENUE ANALYSIS

17.19.3 PRODUCT PORTFOLIO

17.19.4 RECENT DEVELOPMENT

17.2 SHELL PLC

17.20.1 COMPANY SNAPSHOT

17.20.2 REVENUE ANALYSIS

17.20.3 PRODUCT PORTFOLIO

17.20.4 RECENT DEVELOPMENT

17.21 TEAL ELECTRIFICATION SYSTEMS

17.21.1 COMPANY SNAPSHOT

17.21.2 PRODUCT PORTFOLIO

17.21.3 RECENT DEVELOPMENT

17.22 ZEEMAC

17.22.1 COMPANY SNAPSHOT

17.22.2 PRODUCT PORTFOLIO

17.22.3 RECENT DEVELOPMENT

17.23 ZIING

17.23.1 COMPANY SNAPSHOT

17.23.2 PRODUCT PORTFOLIO

17.23.3 RECENT DEVELOPMENT

18 QUESTIONNAIRE

19 RELATED REPORTS

List of Table

TABLE 1 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, 2018-2033 (USD THOUSAND)

TABLE 2 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY FLEET CONFIGURATION, 2018-2033 (USD THOUSAND)

TABLE 3 MEDIUM-DUTY VEHICLES (MDVS) (CLASS 4–6) IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 4 HEAVY-DUTY VEHICLES (HDVS) (CLASS 7–8) IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 5 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY LOW-CARBON TECHNOLOGY TYPE, 2018-2033 (USD THOUSAND)

TABLE 6 BATTERY ELECTRIC VEHICLE (BEV) FLEETS IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 7 FUEL CELL ELECTRIC VEHICLES (FCEVS) IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 8 HYBRID & TRANSITIONAL TECHNOLOGIES IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 9 FUTURE & EMERGING TECHNOLOGIES IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 10 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY DIGITAL PLATFORMS, 2018-2033 (USD THOUSAND)

TABLE 11 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY OFFERING, 2018-2033 (USD THOUSAND)

TABLE 12 VEHICLE ELECTRIFICATION SERVICES IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 13 CHARGING INFRASTRUCTURE AS A SERVICE IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 14 ENERGY & POWER MANAGEMENT SERVICES IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 15 FLEET OPERATIONS & LOGISTICS MANAGEMENT IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 16 FINANCING, RISK & COMPLIANCE SERVICES IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 17 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY BUSINESS MODEL TYPE, 2018-2033 (USD THOUSAND)

TABLE 18 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY END-USE INDUSTRY, 2018-2033 (USD THOUSAND)

TABLE 19 PUBLIC SECTOR & GOVERNMENT FLEETS IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 20 LOGISTICS & TRANSPORTATION IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 21 UTILITIES & ENERGY COMPANIES IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 22 INDUSTRIAL & COMMERCIAL FLEETS IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 23 INSTITUTIONAL & CAMPUS FLEETS IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 24 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY CONTRACT STRUCTURE, 2018-2033 (USD THOUSAND)

TABLE 25 SUBSCRIPTION-BASED MODELS IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 26 LONG-TERM MANAGED SERVICE CONTRACTS IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 27 FINANCING & RISK ALLOCATION MODELS IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 28 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY PROVIDER TYPE, 2018-2033 (USD THOUSAND)

TABLE 29 OEM-LED SERVICE PROVIDERS IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 30 ENERGY & UTILITY-LED PROVIDERS IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 31 TECHNOLOGY & PLATFORM PROVIDERS IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 32 INFRASTRUCTURE & EPC PROVIDERS IN CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 33 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY PROVINCE, 2018-2033 (USD THOUSAND)

List of Figure

FIGURE 1 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET: SEGMENTATION

FIGURE 2 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET: DATA TRIANGULATION

FIGURE 3 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET: DROC ANALYSIS

FIGURE 4 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET: GLOBAL VS REGIONAL ANALYSIS

FIGURE 5 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET: COMPANY RESEARCH ANALYSIS

FIGURE 6 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET: INTERVIEW DEMOGRAPHICS

FIGURE 7 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET: DBMR MARKET POSITION GRID

FIGURE 8 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET: MARKET END USER COVERAGE GRID

FIGURE 9 EXECUTIVE SUMMARY

FIGURE 10 STRATEGIC DECISIONS

FIGURE 11 THREE SEGMENTS COMPRISE THE CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY FLEET CONFIGURATION (2025)

FIGURE 12 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET: SEGMENTATION

FIGURE 13 EXPANSION OF ZERO-EMISSION VEHICLE INCENTIVE PROGRAMS FOR COMMERCIAL FLEETS EXPECTED TO DRIVE THE CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET IN THE FORECAST PERIOD OF 2025 TO 2033

FIGURE 14 MEDIUM-DUTY VEHICLES (MDVS) (CLASS 4–6) SEGMENT IS EXPECTED TO ACCOUNT FOR THE LARGEST SHARE OF THE CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET IN 2026 & 2033

FIGURE 15 DRIVERS, RESTRAINS, OPPORUTNITY AND CHANLLENGES (DROC) ANALYSIS OF CANADA FLEET ELECTRIFICATION AS A SERVICE MARKET

FIGURE 16 PUBLIC LIGHT-DUTY EV CHARGING INFRASTRUCTURE AND STOCK GROWTH TO 2040

FIGURE 17 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY FLEET CONFIGURATION, 2025

FIGURE 18 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY LOW-CARBON TECHNOLOGY TYPE, 2025

FIGURE 19 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY DIGITAL PLATFORMS, 2025

FIGURE 20 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY OFFERING, 2025

FIGURE 21 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY BUSINESS MODEL TYPE, 2025

FIGURE 22 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY END-USE INDUSTRY, 2025

FIGURE 23 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY CONTRACT STRUCTURE, 2025

FIGURE 24 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY PROVIDER TYPE, 2025

FIGURE 25 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET, BY PROVINCE, 2025

FIGURE 26 CANADA FLEET ELECTRIFICATION AS A SERVICE (FEAAS) MARKET: COMPANY SHARE 2025 (%)

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.