China Solar Panel Recycling Market

Market Size in USD Million

CAGR :

%

USD

87.85 Million

USD

391.13 Million

2025

2033

USD

87.85 Million

USD

391.13 Million

2025

2033

| 2026 - 2033 | |

| USD 87.85 Million | |

| USD 391.13 Million | |

| % | |

|

China Solar Panel Recycling Market Size

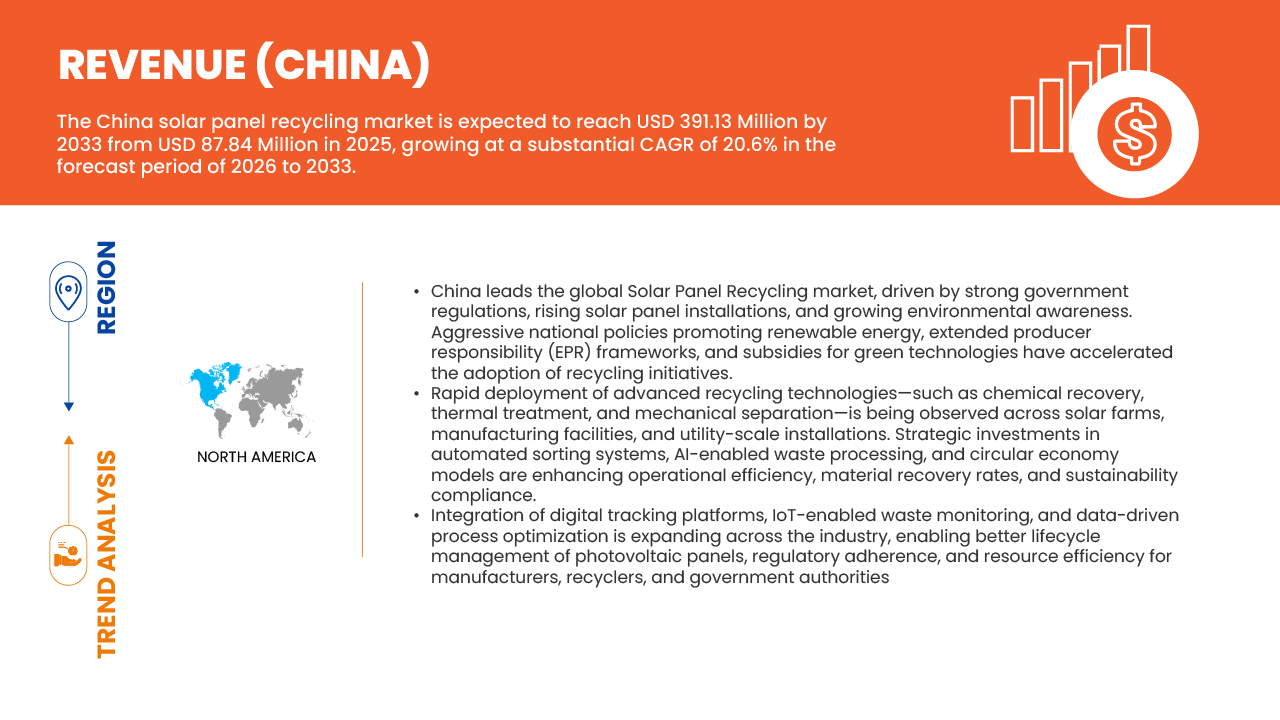

- The China solar panel recycling market is expected to reach USD 391.13 million by 2033 from USD 87.85 million in 2025, growing at a CAGR of 20.6% during the forecast period of 2026 to 2033.

- The China solar panel recycling market is witnessing steady growth, driven by the increasing volume of end-of-life photovoltaic (PV) modules, rising environmental concerns, and stronger regulatory emphasis on sustainable waste management. Government initiatives supporting renewable energy lifecycle management, along with the need to recover valuable materials such as silicon, silver, and aluminum, are significantly contributing to market expansion across the country.

- Continuous advancements in recycling technologies, including automated dismantling, thermal and chemical separation processes, and high-purity material recovery techniques, are enhancing operational efficiency and economic viability. In addition, innovations in reverse logistics, digital tracking systems, and integrated recycling solutions are improving collection rates and enabling better traceability across the solar value chain.

China Solar Panel Recycling Market Analysis

- The China solar panel recycling market serves a diverse range of end-user segments, including photovoltaic manufacturers, utility-scale solar farm operators, commercial & industrial (C&I) energy users, and government-backed waste management entities. Demand is primarily driven by the increasing volume of end-of-life solar panels, rising environmental concerns, and stringent regulatory frameworks promoting responsible disposal and resource recovery.

- The market caters to multiple recycling and material recovery segments, including silicon recovery, glass recycling, aluminum frame extraction, and precious metal recovery (such as silver and copper). Additionally, recycling solutions are designed for different panel types, including monocrystalline, polycrystalline, and thin-film modules, with varying levels of material recovery efficiency and processing complexity.

- Adoption is fueled by continuous technological advancements in recycling processes, such as automated dismantling systems, thermal and chemical separation techniques, and high-purity material extraction methods. Innovations in logistics, reverse supply chains, and digital tracking systems are also improving collection efficiency and traceability. Furthermore, increasing government support, extended producer responsibility (EPR) policies, and the expansion of recycling infrastructure across China are significantly enhancing market accessibility and scalability.

- In 2025, the Glass segment is projected to dominate the China solar panel recycling market with a share of approximately 55.31%, owing to the high value and reusability of recovered silicon in new photovoltaic module manufacturing. The growing focus on circular economy practices, coupled with the rising cost of raw materials, is driving strong demand for high-purity silicon recovery, thereby strengthening its revenue contribution within the overall market.

Report Scope and China Solar Panel Recycling Market Segmentation

|

Attributes |

China Solar Panel Recycling Market Insights |

|

Segments Covered |

|

|

Countries Covered |

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

China Solar Panel Recycling Market Trends

“Rapid Advancement in Recycling Technologies and Circular Economy Integration”

- A key trend shaping the China solar panel recycling market is the increasing focus on advanced recycling technologies and circular economy integration. As the volume of end-of-life photovoltaic modules continues to rise, companies are shifting from basic material recovery methods to more sophisticated processes that enable higher-value extraction of silicon, silver, and other critical materials. This transition is driven by the need to improve recovery efficiency while reducing environmental impact, aligning with national sustainability goals and resource security priorities.

- In addition, the market is witnessing significant product and process innovation, with companies developing specialized recycling solutions tailored to different panel types, including monocrystalline, polycrystalline, and thin-film modules. These innovations have enabled recyclers to move beyond simple waste treatment and position themselves as providers of high-value secondary raw materials, supporting upstream solar manufacturing industries.

- Technological advancements are playing a crucial role in market development. Modern recycling facilities increasingly utilize automated dismantling systems, thermal and chemical separation techniques, and AI-enabled sorting technologies to enhance precision and efficiency. Closed-loop recycling systems and digital tracking solutions are also gaining traction, allowing manufacturers and recyclers to monitor material flows and ensure compliance with environmental regulations. Collectively, these advancements are strengthening China’s position as a global leader in solar panel recycling while improving economic viability and scalability of recycling operations.

China Solar Panel Recycling Market Dynamics

Driver

“Rapid Expansion of Solar PV Installations Generating Large Volumes of End-of-Life Panels in China”

- China’s solar photovoltaic (PV) sector has undergone unprecedented expansion over the past decade, fundamentally reshaping the country’s energy mix while simultaneously laying the foundation for a significant future waste stream. This rapid deployment is now emerging as a primary driver for the growth of the China Solar Panel Recycling Market.

- China has established itself as the global leader in solar PV installations, crossing the 1,100 GW installed capacity mark by 2025, making it the first country to exceed the terawatt threshold. Annual additions remain exceptionally high, with ~277 GW installed in 2024 alone, reflecting aggressive renewable energy targets and strong policy support. This large-scale deployment is further supported by a robust project pipeline exceeding 700 GW under development, ensuring sustained growth in installed capacity over the next decade.

- Quantitative projections clearly highlight the scale of this emerging challenge. According to the China Photovoltaic Industry Association, retired PV panels are expected to reach ~1.4 million tonnes (18 GW) by 2030, rising sharply to ~20 million tonnes by 2040. Other studies indicate even more aggressive scenarios, estimating cumulative PV waste could reach 36 million tonnes by 2040, depending on installation and degradation assumptions. Long-term forecasts suggest that by 2050, China could generate nearly 100 million tonnes of recyclable PV materials, underscoring the massive material recovery opportunity.

- This growth trajectory is further amplified by China’s dominance in global solar deployment. The country accounted for over 60% of global PV additions in 2024, reinforcing its position as the central contributor to future global solar waste streams. As installations continue at scale, waste generation will follow a nonlinear curve; initially gradual, then accelerating rapidly post-2030 as early large-scale solar farms reach decommissioning age.

Restraint/Challenge

“High Capital and Operational Costs of Recycling Facilities”

- Despite strong policy support and growing material recovery value, the China Solar Panel Recycling Market faces a significant restraint in the form of high capital investment and operational costs associated with recycling infrastructure. The economic viability of recycling remains challenged due to expensive technologies, complex processes, and unfavorable cost comparisons with alternative disposal methods.

- Establishing solar panel recycling facilities requires substantial upfront capital expenditure, particularly for advanced material recovery systems. Industrial-scale recycling plants using thermal and chemical treatment technologies can cost between USD 800,000 to USD 2.5 million, depending on automation levels and recovery efficiency.

- These high initial investments create entry barriers for new players and limit the expansion of formal recycling capacity, especially in early-stage markets where waste volumes are still ramping up.

- Operational costs further intensify the economic challenge. Recycling solar panels is a technically complex, multi-step process involving dismantling, separation of bonded materials, and recovery of metals such as silicon and silver. This complexity leads to high processing costs, often exceeding the value of recovered materials. Industry estimates suggest recycling costs range between USD 800-1,200 per tonne, while the cost of sourcing equivalent virgin materials is lower at USD 600-900 per tonne, making recycling economically less attractive.

- Additionally, the cost disparity between recycling and disposal significantly discourages adoption. According to estimates from the National Renewable Energy Laboratory (NREL), recycling a solar panel can cost USD 15-45 per unit, compared to just USD 1-5 for landfill disposal, creating a strong financial disincentive for proper recycling.

China Solar Panel Recycling Market Scope

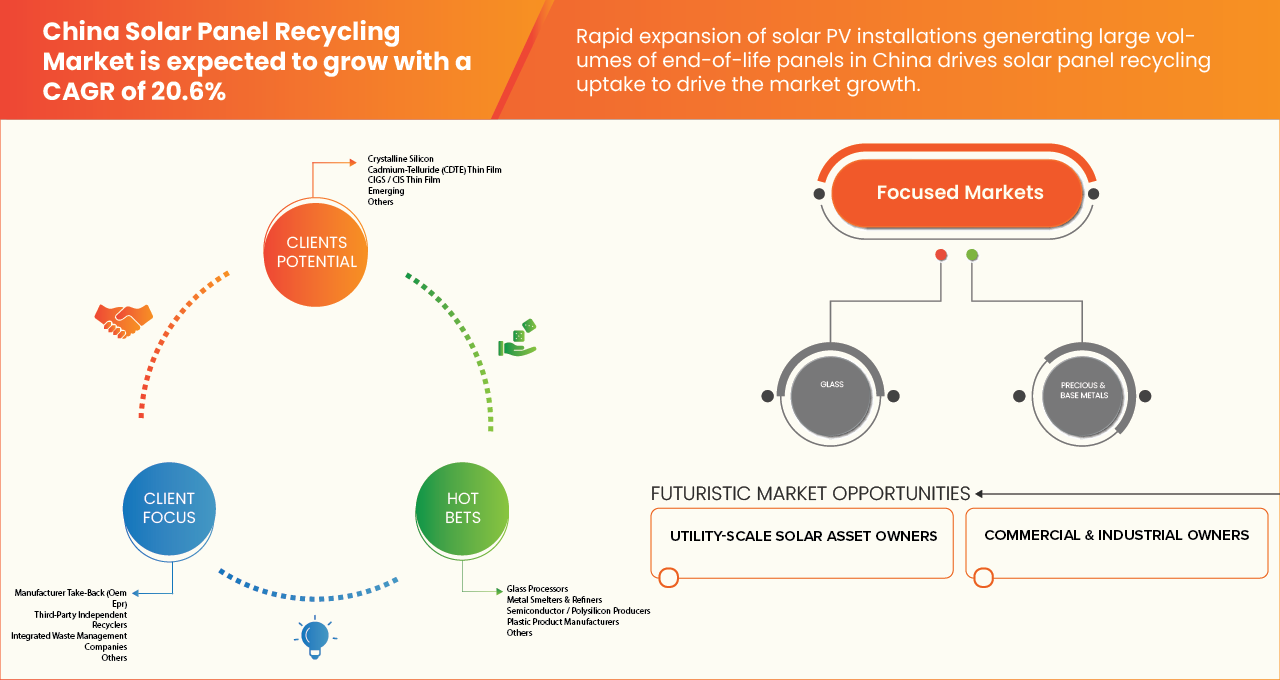

The China solar panel recycling market is segmented into multiple notable segments based on recovered material, panel type, recycler type, service offering, lifecycle stage, client type, and end-user of recovered materials.

• By Recovered Material

On the basis of recovered material, the China Solar Panel Recycling Market is segmented into components, glass, silicon/wafer remnants, precious & base metals, polymers & encapsulants, and rare/critical materials.

In 2026, the glass segment is expected to dominate the market, accounting for the highest share of 55.27%, due to the high economic value and reusability of recovered silicon in new photovoltaic module manufacturing. Increasing focus on reducing dependence on virgin raw materials and improving resource efficiency is further strengthening demand for silicon recovery.

The Precious & Base Metals segment is expected to be the fastest-growing, registering a CAGR of 21.3% in the China solar panel recycling market. Growth is driven by rising demand for high-purity silicon in photovoltaic manufacturing and increasing investments in advanced material recovery technologies.

• By Solar Panel Type Recycled

On the basis of solar panel type recycled, the market is segmented into crystalline silicon, cadmium-telluride (CdTe) thin film, CIGS/CIS thin film, emerging technologies, and others.

In 2026, the crystalline silicon segment is expected to dominate the market, accounting for the highest share of 89.06%, owing to its dominant installed base across China’s solar infrastructure. The large volume of crystalline silicon panels reaching end-of-life is driving higher recycling demand in this segment.

The Cadmium-Telluride (CDTE) Thin Film segment is expected to be the fastest-growing, registering a CAGR of 21.4% in the China solar panel recycling market. Growth is driven by increasing adoption of thin-film technologies and growing need for efficient recovery of rare materials such as cadmium and tellurium.

• By Recycler Type

On the basis of recycler type, the market is segmented into manufacturer take-back (OEM EPR), third-party independent recyclers, integrated waste management companies, and others.

In 2026, the Manufacturer Take-Back (OEM EPR) segment is expected to dominate the market, accounting for the highest share of 43.95%, due to their specialized expertise, scalable recycling capabilities, and increasing partnerships with solar asset owners and manufacturers.

The third-party independent recyclers segment is expected to be the fastest-growing, registering a CAGR of 21.0% in the China solar panel recycling market. Growth is driven by increasing outsourcing of recycling services and rising demand for cost-effective and flexible recycling solutions.

• By Service Offering

On the basis of service offering, the market is segmented into collection & logistics service, module refurbishment & remarketing, full recycling (materials recovery), hazardous material handling & compliance, and consulting/certification/traceability.

In 2026, the full recycling (materials recovery) segment is expected to dominate the market, accounting for the highest share of 43.33% driven by the growing need for complete material extraction and circular economy integration across the solar value chain.

The Collection & Logistics Service segment is expected to be the fastest-growing, registering a CAGR of 21.2% in the China solar panel recycling market. Growth is driven by increasing demand for cost-effective reused solar panels and growing emphasis on extending product lifecycle.

• By Panel Lifecycle Stage at Entry

On the basis of lifecycle stage, the market is segmented into manufacturing scrap & rejects, pre-installation damage/logistics loss, early-life failure, end-of-life retirement, repowering/upgrade displacement, and others.

In 2026, the Early-Life Failure segment is expected to dominate the market, accounting for the highest share of 58.19%, due to the increasing number of aging solar installations reaching their operational lifespan and requiring proper disposal and recycling.

The end-of-life retirement segment is expected to be the fastest-growing, registering a CAGR of 21.6% in the China solar panel recycling market. Growth is driven by the rising volume of decommissioned solar panels and increasing regulatory focus on proper disposal and recycling.

• By Client Type

On the basis of client type, the market is segmented into utility-scale solar asset owners, commercial & industrial (C&I) owners, residential aggregators/installers, manufacturers/OEMs, insurance/lenders/asset-recovery firms, and others.

In 2026, the utility-scale solar asset owners’ segment is expected to dominate the market, accounting for the highest share of 45.92owing to the large volume of decommissioned panels generated from large solar farms and infrastructure projects.

The Commercial & Industrial Owners segment is expected to be the fastest-growing, registering a CAGR of 21.2% in the China solar panel recycling market. Growth is driven by increasing regulatory pressure under extended producer responsibility (EPR) frameworks and growing adoption of take-back programs.

By End User of Recovered Materials

On the basis of end users, the market is segmented into glass processors, semiconductor/polysilicon producers, metal smelters & refiners, plastic product manufacturers, and others.

In 2026, the glass Processors segment is expected to dominate the market, accounting for the highest share of 46.83%, driven by increasing demand for high-purity silicon in new solar panel manufacturing and electronic applications.

The Semiconductor / Polysilicon Producers segment is expected to be the fastest-growing, registering a CAGR of 21.4% in the China solar panel recycling market. Growth is driven by increasing regulatory pressure under extended producer responsibility (EPR) frameworks and growing adoption of take-back programs.

China Solar Panel Recycling Market Insight

The China Solar Panel Recycling Market is experiencing steady growth, driven by the increasing volume of end-of-life photovoltaic modules, rising environmental concerns, and stronger regulatory frameworks promoting sustainable waste management. The shift toward a circular economy, along with the need to recover valuable materials such as silicon, silver, and aluminum, is significantly supporting market expansion.

Additionally, advancements in recycling technologies, improved reverse logistics systems, and increasing collaboration between solar manufacturers and recycling companies are enhancing operational efficiency and scalability. The expansion of recycling infrastructure and supportive government policies are further contributing to higher market penetration across both developed and emerging regions within China.

China Solar Panel Recycling Market Share

The China Solar Panel Recycling Market is primarily led by well-established companies,

- Resolartech (China)

- Changzhou Ruisai Environmental Protection Technology Co., Ltd. (China)

- ESUN SOLAR PTE. LTD. (Singapore)

- LONGi Green Energy Technology Co., Ltd. (China)

- Trina Solar Co., Ltd. (China)

- DAS Solar Co., Ltd. (China)

- Hanwha Group (South Korea)

- Jinko Solar Holding Co., Ltd. (China)

- Yingli Energy Company Limited (China)

- State Power Investment Corporation (China)

- SUNY GROUP (China)

- Henan Reliable Environmental Protection Technology Co., Ltd. (China)

- TM-Machine (China)

- WANROOE MACHINERY CO., LTD. (China)

- Henan Renewable Energy Technology Co., Ltd. (China)

Latest Developments in China Solar Panel Recycling Market

- In March 2025, Changzhou Ruisai Environmental Technology Co., Ltd. has been selected to lead China’s first national circular economy standardization pilot project for retired photovoltaic module recycling, jointly approved by the Standardization Administration of China and the National Development and Reform Commission. The initiative will develop technical benchmarks and advance high‑pressure jet grinding and green leaching technologies and serve as an industry model for sustainable PV recycling. This milestone positions Ruisai Environmental Technology as a national leader in PV recycling and supports China’s broader circular economy goals.

- In March 2025, ESUN (CyclePV) has expanded its solar panel recycling operations across multiple provinces in China, establishing over 300 distributed recycling sites. The company focuses on scalable, decentralized recycling solutions to handle increasing volumes of end-of-life PV panels, supporting circular economy practices in the solar industry.

- In June 2025, The Trina Solar Co., Ltd. has implemented advanced PV recycling technology capable of recovering high-value materials such as glass, silicon, and metals. This enhances resource efficiency and reduces environmental impact associated with solar panel disposal.

- In In September, DAS Solar has entered the back-contact (BC) solar cell segment with plans to build a 5 GW high-efficiency cell manufacturing facility in Guizhou, China, marking a strategic shift beyond its established TOPCon technology base. The company is advancing its proprietary DBC (DAS Back Contact) technology, combining TOPCon architecture with full back-contact design to improve efficiency, eliminate front-side busbars, and enable scalable next-generation PV production

- In March 2026, LONGi Green Energy Technology Co. has achieved a world-record 34.85% efficiency for its crystalline silicon–perovskite tandem solar cell, certified by the U.S. National Renewable Energy Laboratory (NREL), marking another breakthrough in next-generation photovoltaic technology. The company’s two-terminal tandem cell architecture significantly surpasses traditional single-junction efficiency limits, reinforcing its leadership in high-efficiency solar R&D. This innovation accelerates the development of ultra-high-efficiency solar technologies.

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

China Solar Panel Recycling Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its China Solar Panel Recycling Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as China Solar Panel Recycling Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.