Europe Automated Cell Cultures Market

Market Size in USD Billion

CAGR :

%

USD

3.25 Billion

USD

7.06 Billion

2025

2033

USD

3.25 Billion

USD

7.06 Billion

2025

2033

| 2026 –2033 | |

| USD 3.25 Billion | |

| USD 7.06 Billion | |

| % | |

|

Europe Automated Cell Cultures Market Overview

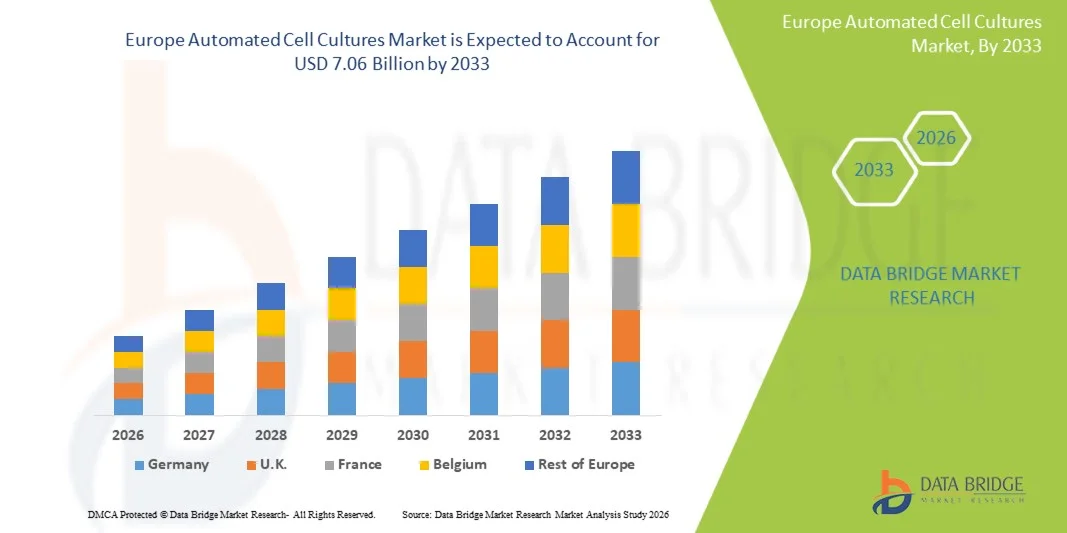

The Europe Automated Cell Cultures market was valued at USD 3.25 billion in 2025 and is projected to reach USD 7.06 billion by 2033, growing at a CAGR of 10.20% from 2026 to 2033. The market is witnessing steady growth driven by the increasing demand for high-throughput and contamination-free cell culture processes, rapid advancements in laboratory automation technologies, and expanding applications across biopharmaceutical production, regenerative medicine, and drug discovery.

The growing prevalence of chronic diseases and rising investments in biologics, cell therapies, and vaccine development are encouraging pharmaceutical companies, biotechnology firms, and research institutes to adopt automated cell culture systems for improved scalability and reproducibility. Automated platforms integrated with robotics, AI-based monitoring, and real-time analytics are gradually replacing conventional manual culture methods in many laboratories, enabling reduced human intervention, enhanced process consistency, lower contamination risks, and efficient large-scale production of complex cell-based products.

Key Market Trends & Insights

- The U.K. dominated the Europe Automated Cell Cultures market with the largest revenue share of 33.95% in 2025, supported by advanced biopharmaceutical research infrastructure, rising investments in cell therapy development, and increasing adoption of laboratory automation technologies.

- The Automated Bioreactor Systems segment led the market with a 42.05% share in 2025, driven by high demand for scalable cell expansion, reduced contamination risks, and widespread use in biologics and vaccine production.

- Germany is expected to be the fastest-growing country in the Europe Automated Cell Cultures market at a CAGR of 7.7% from 2026 to 2033, fueled by expanding pharmaceutical R&D activities, growing biotechnology manufacturing capabilities, and increasing adoption of automated cell processing technologies.

- The Consumables segment dominates the product category with a 54.62% revenue share in 2025, driven by recurring demand for culture media, sera, reagents, and single-use laboratory plastics used extensively across drug development and research applications.

- The Drug Development segment dominates the application category with a 36.87% revenue share in 2025, supported by rising demand for preclinical testing, high-throughput screening, and biologics development pipelines across global pharmaceutical companies.

- The Biotech Companies segment dominates the end-user category with a 42.26% revenue share in 2025, led by increasing production of monoclonal antibodies, cell therapies, and regenerative medicine products across China, Japan, and South Korea.

- The infinite cell line cultures segment dominated the market with a share of 61.28% in 2025 due to its extensive utilization in long-term biological research, cancer studies, drug screening, vaccine development, and biopharmaceutical production

Market Size & Forecast

- Europe Market Value (2025): USD 3.25 Billion

- Expected Market Value (2033): USD 7.06 Billion

- Forecast CAGR (2026–2033): 10.20%

- Dominating Country in 2025: U.K.

- Fastest Growing Country: Germany

Report Scope and Europe Automated Cell Cultures Market Segmentation

|

Attributes |

Automated Cell Cultures Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe |

|

Key Market Players |

• Thermo Fisher Scientific Inc. (U.S.) |

|

Market Opportunities |

· Rising Adoption of AI-Integrated Automated Cell Culture Platforms in Biopharmaceutical Manufacturing · Expanding Demand for Automated Cell Culture Systems in Regenerative Medicine and Cell Therapy Research · Growing Investments in High-Throughput Drug Discovery and Personalized Medicine Research Using Automated Cell Culture Technologies |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Europe Automated Cell Cultures Market Trends

Trend: Rising Adoption of AI-Driven and Robotic Cell Culture Automation

Biopharmaceutical and biotechnology companies are increasingly adopting AI-enabled automated cell culture systems to improve scalability, reproducibility, and contamination control in laboratory workflows. Advanced robotic platforms integrated with machine learning algorithms are enabling real-time monitoring of cell viability, nutrient utilization, and growth kinetics, significantly reducing manual intervention and experimental variability. Research institutes and pharmaceutical manufacturers are leveraging automated systems for high-throughput drug screening, monoclonal antibody production, and stem cell expansion, while cloud-connected analytics platforms are improving process optimization and predictive maintenance capabilities. For instance, in March 2025, Thermo Fisher Scientific Inc. expanded its automated cell therapy manufacturing capabilities with AI-integrated monitoring technologies aimed at accelerating biologics and regenerative medicine workflows. Similarly, the increasing adoption of robotic liquid handling systems in large-scale bioprocessing facilities is reinforcing the transition toward fully automated laboratories globally.

Europe Automated Cell Cultures Market Dynamics

Key Market Driver: Expanding Biopharmaceutical Production and Cell Therapy Research

The rapid growth of the biopharmaceutical industry and increasing investment in regenerative medicine are creating substantial demand for automated cell culture systems across Asia-Pacific. Pharmaceutical companies, CROs, and academic research institutes are deploying automated platforms to support large-scale production of biologics, vaccines, stem cells, and cell-based therapies while ensuring process consistency and regulatory compliance. Countries such as China, Japan, South Korea, and India are significantly expanding biotechnology infrastructure and government-backed life sciences initiatives, accelerating adoption of automated laboratory technologies. According to industry estimates, global biologics account for over 35% of the pharmaceutical pipeline, increasing the need for scalable and contamination-free cell expansion systems. In addition, the rise in cancer and chronic disease prevalence has intensified demand for cell-based drug discovery and precision medicine applications, further strengthening market growth.

Key Restraint/Challenge: High Capital Investment and Complex System Integration

A significant restraint in the Europe Automated Cell Cultures market is the high initial investment associated with advanced automation platforms. Modern systems incorporate robotic handling units, automated incubators, real-time imaging systems, AI-enabled analytics software, and integrated bioreactors, requiring substantial capital expenditure for installation, validation, and maintenance. The total cost of ownership also includes software upgrades, consumables, technical training, and regulatory compliance expenses, limiting adoption among small research laboratories and emerging biotechnology startups. For instance, the deployment of fully automated GMP-compliant cell therapy manufacturing facilities in Japan and Singapore often requires multimillion-dollar infrastructure investments, reflecting the broader challenge of accessibility for cost-sensitive organizations. In addition, integration complexities between legacy laboratory systems and next-generation automation platforms continue to create operational and technical barriers in several developing markets.

Key Market Opportunity: Growth of Personalized Medicine and Regenerative Therapies

The increasing focus on personalized medicine, stem cell therapy, and regenerative medicine presents a significant growth opportunity for the Automated Cell Cultures market. Automated systems enable precise and reproducible cell processing workflows essential for individualized therapies, tissue engineering, and advanced biologics manufacturing. AI-integrated platforms can optimize cell growth conditions, automate quality control, and support real-time data-driven decision-making, improving production efficiency and reducing human error. The development of closed-loop automated bioprocessing systems and cloud-based laboratory management platforms is further expanding access to advanced cell culture technologies across emerging economies in Asia-Pacific. In 2024, several biotechnology firms in China and South Korea announced investments in automated stem cell manufacturing and CAR-T therapy production facilities, highlighting the region’s growing emphasis on scalable regenerative medicine infrastructure and next-generation biomanufacturing capabilities.

Europe Automated Cell Cultures Market Scope

The market is segmented on the basis of product, type, application, and end user.

- By Product

On the basis of product, the Automated Cell Cultures market is segmented into consumables and instruments. The consumables segment dominated the market with a share of 58.74% in 2025, owing to the recurring demand for culture media, sera, reagents, assay kits, flasks, plates, and filtration products used extensively in continuous cell culture workflows. The increasing adoption of automated bioprocessing systems in pharmaceutical and biotechnology companies has significantly accelerated the consumption of cell culture consumables across research and commercial manufacturing applications. In addition, rising investments in biologics production, regenerative medicine, stem cell therapy, and vaccine manufacturing are supporting high-volume usage of sterile and high-performance consumable products. The growing need for contamination-free processing, reproducibility, and scalability in laboratory operations further strengthens segment growth. Automation platforms also require specialized single-use consumables compatible with robotic handling systems, which is contributing to recurring revenue generation for manufacturers. Furthermore, increasing outsourcing of drug discovery and cell-based testing to CROs and research laboratories is expanding product demand globally. Strong distribution networks, continuous product innovation, and increasing regulatory emphasis on quality-controlled laboratory materials are further reinforcing the dominance of the consumables segment in the market.

The instruments segment is expected to witness the fastest CAGR of 7.1% from 2026 to 2033, driven by the rising adoption of automated incubators, robotic liquid handling systems, bioreactors, imaging systems, and automated cell monitoring platforms across advanced research facilities and biopharmaceutical manufacturing plants. Increasing focus on laboratory automation, operational efficiency, and reduction of manual intervention is accelerating the deployment of sophisticated cell culture instruments. In addition, the growing integration of AI-enabled monitoring, real-time analytics, cloud connectivity, and robotics into automated culture systems is enhancing process precision and scalability. Pharmaceutical companies are increasingly investing in advanced instrumentation to support high-throughput screening, personalized medicine, and large-scale biologics production. Moreover, the expansion of cell and gene therapy pipelines, coupled with rising demand for GMP-compliant automated systems, is further boosting segment growth. Continuous technological advancements in imaging accuracy, contamination control, and automated workflow management are also supporting widespread adoption of automated cell culture instruments across academic, clinical, and industrial settings.

- By Type

On the basis of type, the Automated Cell Cultures market is segmented into infinite cell line cultures and finite cell line cultures. The infinite cell line cultures segment dominated the market with a share of 61.28% in 2025 due to its extensive utilization in long-term biological research, cancer studies, drug screening, vaccine development, and biopharmaceutical production. These cell lines possess the ability to proliferate indefinitely, making them highly suitable for repetitive experimental procedures and large-scale commercial applications. The increasing use of immortalized cell lines in pharmaceutical R&D and toxicology studies has significantly strengthened segment demand. In addition, automated systems are increasingly being integrated with continuous cell line workflows to improve reproducibility, reduce contamination risks, and enhance throughput efficiency. Growing investments in monoclonal antibody production, biosimilar development, and precision medicine research are further supporting adoption. Academic institutions and biotechnology companies are also leveraging automated platforms to optimize cell maintenance and experimental consistency. Furthermore, advancements in genetic engineering, CRISPR technologies, and cell imaging systems are improving the functionality and scalability of immortalized cell culture operations. The strong presence of established research protocols and commercially available standardized cell lines continues to reinforce the leading position of this segment.

The finite cell line cultures segment is anticipated to witness the fastest CAGR of 6.8% from 2026 to 2033, driven by increasing demand for physiologically relevant cellular models in regenerative medicine, stem cell research, and tissue engineering applications. Finite cell cultures offer more accurate biological representation of normal cellular behavior, making them increasingly valuable in translational research and therapeutic development. Rising adoption of patient-derived cells and primary cell cultures in personalized medicine and disease modeling is significantly accelerating segment growth. In addition, advancements in automated culture technologies are enabling researchers to maintain delicate finite cultures with improved precision and reduced manual variability. The growing emphasis on cell-based therapies, organoid development, and advanced toxicology testing is further expanding market opportunities. Pharmaceutical and research organizations are increasingly utilizing finite cultures for predictive drug response studies and biomarker discovery. Moreover, regulatory preference for biologically relevant testing models and increasing investment in advanced cell therapy research are supporting the rapid expansion of this segment across global healthcare and life sciences industries.

- By Application

On the basis of application, the Automated Cell Cultures market is segmented into drug development, stem cell research, regenerative medicine, cancer research, vaccines, and others. The drug development segment dominated the market with a share of 31.94% in 2025 due to the extensive use of automated cell culture systems in preclinical testing, toxicity analysis, biologics development, and high-throughput screening applications. Pharmaceutical and biotechnology companies are increasingly adopting automated platforms to accelerate drug discovery workflows, improve reproducibility, and reduce operational errors associated with manual handling. The rising prevalence of chronic diseases and growing investment in novel therapeutics are further driving the need for efficient and scalable cell-based testing solutions. In addition, integration of robotics, AI-driven analytics, and real-time monitoring systems is enhancing experimental accuracy and research productivity. Automated cell cultures are also playing a critical role in reducing time-to-market for pharmaceutical products by streamlining assay preparation and compound testing processes. Increasing demand for personalized medicine and targeted therapies is further strengthening adoption across advanced drug development programs. Furthermore, continuous advancements in cell imaging, automated incubation, and bioinformatics integration are supporting widespread deployment of automated culture technologies in pharmaceutical R&D environments.

The regenerative medicine segment is projected to witness the fastest CAGR of 7.3% from 2026 to 2033, driven by the increasing development of stem cell therapies, tissue engineering solutions, and personalized regenerative treatments. Automated cell culture systems are becoming essential for maintaining consistency, sterility, and scalability in the production of therapeutic cells and engineered tissues. Rising investments in regenerative medicine research by governments, biotechnology companies, and academic institutions are significantly accelerating market expansion. In addition, advancements in 3D cell culture technologies, organoid development, and bioprinting are creating new opportunities for automated culture platforms. The growing burden of degenerative disorders, organ failure, and chronic diseases is also increasing demand for regenerative therapeutic solutions. Automated systems help improve cell viability, reduce contamination risks, and ensure standardized production processes required for clinical-grade therapies. Moreover, expanding clinical trials for stem cell-based treatments and supportive regulatory initiatives for advanced therapy medicinal products are further contributing to the rapid growth of the regenerative medicine segment globally.

- By End User

On the basis of end user, the Automated Cell Cultures market is segmented into biotech companies, research organizations, academic research institutes, and other. The biotech companies segment dominated the market with a share of 38.46% in 2025 due to increasing investments in biologics manufacturing, cell therapy development, monoclonal antibody production, and advanced biopharmaceutical research. Biotechnology firms are rapidly adopting automated cell culture systems to enhance operational efficiency, improve scalability, and reduce contamination risks associated with manual laboratory processes. The growing focus on precision medicine, gene therapies, and personalized treatment approaches is significantly increasing demand for high-throughput automated platforms. In addition, automated technologies enable biotech companies to accelerate drug discovery timelines, optimize production workflows, and maintain regulatory compliance in GMP environments. Rising collaboration between biotechnology companies and research institutions for advanced therapeutic development is also strengthening market growth. Furthermore, integration of AI-enabled analytics, robotics, and cloud-based monitoring systems is improving productivity and experimental reproducibility across automated laboratories. Strong funding support for biotechnology innovation and expanding global biopharmaceutical pipelines continue to reinforce the dominant position of this segment in the market.

The research organizations segment is expected to witness the fastest CAGR of 6.9% from 2026 to 2033, driven by increasing outsourcing of pharmaceutical research activities and growing reliance on contract research organizations for drug discovery and preclinical testing services. Research organizations are increasingly implementing automated cell culture technologies to manage large sample volumes, improve experimental consistency, and reduce turnaround times for clients. In addition, rising demand for cost-effective and scalable research infrastructure is accelerating automation adoption across independent laboratories and CRO facilities. The integration of advanced imaging systems, robotic liquid handling, and AI-powered data analytics is enhancing research efficiency and accuracy. Expanding clinical research activities, increasing biologics development, and rising investments in translational medicine are also contributing to segment growth. Moreover, the growing need for standardized and reproducible experimental workflows in toxicology testing, biomarker discovery, and cell-based assays is further supporting the rapid expansion of automated cell culture systems among research organizations globally.

Europe Automated Cell Cultures Market Regional Analysis

The Europe Automated Cell Cultures market is expected to witness rapid growth, driven by expanding biopharmaceutical manufacturing activities, increasing investments in biotechnology research, and rising adoption of laboratory automation technologies across countries such as the U.K., Germany, France, and Italy. Growing demand for biologics, cell therapies, and regenerative medicine solutions, along with increasing focus on contamination-free and high-throughput cell processing, is supporting regional market expansion. In addition, the growing presence of pharmaceutical R&D centers, contract research organizations (CROs), and advanced bioprocessing facilities is accelerating the adoption of automated cell culture systems across commercial and academic sectors.

Germany Automated Cell Cultures Market Insight

The Germany Automated Cell Cultures market is witnessing consistent growth due to rising investments in pharmaceutical R&D, expanding biotechnology manufacturing infrastructure, and increasing focus on biologics and vaccine production. Biotech companies, research institutes, and CROs are increasingly adopting automated cell culture platforms for drug discovery, stem cell research, and regenerative medicine applications. Moreover, increasing government support for biotechnology innovation, rising adoption of AI-enabled laboratory automation systems, and growing demand for efficient bioprocessing technologies are further contributing to market growth. Germany is also expected to be the fastest-growing country in the Europe Automated Cell Cultures market at a CAGR of 7.7% from 2026 to 2033, fueled by expanding pharmaceutical research activities and increasing investments in automated cell processing technologies.

U.K. Automated Cell Cultures Market Insight

The U.K. Automated Cell Cultures market is growing rapidly, driven by advanced biopharmaceutical research capabilities, rising investments in life sciences, and increasing adoption of automated laboratory technologies. Expanding use of AI-integrated cell culture systems across pharmaceutical, biotechnology, and regenerative medicine sectors is significantly boosting market demand. In addition, rising investments in biologics manufacturing, increasing focus on precision medicine, and rapid advancements in laboratory automation are positioning the U.K. as the dominant country in the Europe Automated Cell Cultures market, accounting for the largest revenue share of 33.95% in 2025.

Europe Automated Cell Cultures Market Share

The Automated Cell Cultures industry is primarily led by well-established companies, including:

- Thermo Fisher Scientific Inc. (U.S.)

- Danaher Corporation (U.S.)

- Merck KGaA (Germany)

- Sartorius AG (Germany)

- Eppendorf SE (Germany)

- Lonza Group AG (Switzerland)

- Corning Incorporated (U.S.)

- FUJIFILM Irvine Scientific (U.S.)

- Becton, Dickinson and Company (U.S.)

- Bio-Rad Laboratories, Inc. (U.S.)

- Agilent Technologies, Inc. (U.S.)

- Hamilton Company (U.S.)

- PerkinElmer Inc. (U.S.)

- Getinge AB (Sweden)

- Tecan Group Ltd. (Switzerland)

- Promega Corporation (U.S.)

- Takara Bio Inc. (Japan)

- Nikon Corporation (Japan)

- Leica Microsystems (Germany)

- GE HealthCare Technologies Inc. (U.S.)

- Cell Culture Company, LLC (U.S.)

- HiMedia Laboratories Pvt. Ltd. (India)

- Panasonic Healthcare Holdings Co., Ltd. (Japan)

- Miltenyi Biotec GmbH (Germany)

- Repligen Corporation (U.S.)

- Cytiva (U.S.)

- Avantor, Inc. (U.S.)

- BioSpherix, Ltd. (U.S.)

- Esco Lifesciences Group (Singapore)

- Infors AG (Switzerland)

Latest Developments in Europe Automated Cell Cultures Market

- In October 2021, Sartorius announced the open-source release of the LIVECell deep learning dataset for label-free live cell segmentation, designed to advance AI-driven automated cell analysis and imaging workflows. The dataset included more than 1.6 million annotated cells across multiple cell types, enabling researchers to improve automated cell culture monitoring, image-based analytics, and high-throughput biological experimentation

- In June 2022, Sartorius announced that Richard Wales and Neil Bargh received the 2022 ESACT Innovation Award for the development of the Ambr automated bioreactor technology. The Ambr platform has become widely adopted in automated cell culture applications for clone selection, process optimization, biologics manufacturing, vaccine production, and cell and gene therapy development, significantly accelerating biopharmaceutical R&D workflows

- In July 2022, Sartorius highlighted its advanced automated cell line development technologies during its “Accelerate Time to Clinic by Automating Cell Line Development” initiative. The company showcased integrated platforms including Octet®, iQue®, Ambr®15, and the ALS CellCelector automated cell picking system to improve clone selection, characterization, and scalable cell culture process development for biologics commercialization

- In October 2022, Sartorius reported continued double-digit growth in its Bioprocess Solutions division, supported by rising demand for automated bioprocessing and cell culture technologies. The company emphasized increasing adoption of automated systems for biologics manufacturing, advanced therapeutics, and cell-based research applications across pharmaceutical and biotechnology industries

- In January 2023, Sartorius announced strong fiscal 2022 growth driven by expanding demand for bioprocess solutions and laboratory automation technologies. The company confirmed continued investments in automated cell culture systems, biopharmaceutical manufacturing capabilities, and scalable upstream bioprocessing platforms to support the rapidly growing biologics and cell therapy markets

- In April 2023, Cytiva announced the launch of its X-platform bioreactors designed to simplify single-use upstream bioprocessing operations for automated cell culture applications. The platform incorporated Figurate automation software, scalable bioreactor configurations, and enhanced process efficiency features to support monoclonal antibody production, viral vector manufacturing, and cell and gene therapy developmen

- In April 2024, GEA Group unveiled its advanced perfusion platform for food biomanufacturing and cell cultivation applications. The system combined GEA Axenic-line bioreactors with kytero single-use separation technology to improve cell density, productivity, and automated culture efficiency while reducing media consumption and operational costs in large-scale cell cultivation processes

- In May 2025, researchers introduced RoboCulture, an advanced robotics platform for automated biological experimentation and cell culture management. The platform utilized robotic manipulation, computer vision, liquid handling automation, and real-time growth monitoring to autonomously conduct long-duration cell culture experiments with minimal human intervention, demonstrating the growing integration of robotics and AI in automated cell culture systems

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.