Europe Beverage Coolers Market

Market Size in USD Billion

CAGR :

%

USD

7.43 Billion

USD

11.40 Billion

2025

2033

USD

7.43 Billion

USD

11.40 Billion

2025

2033

| 2026 –2033 | |

| USD 7.43 Billion | |

| USD 11.40 Billion | |

| % | |

|

Europe Beverage Coolers Market Size

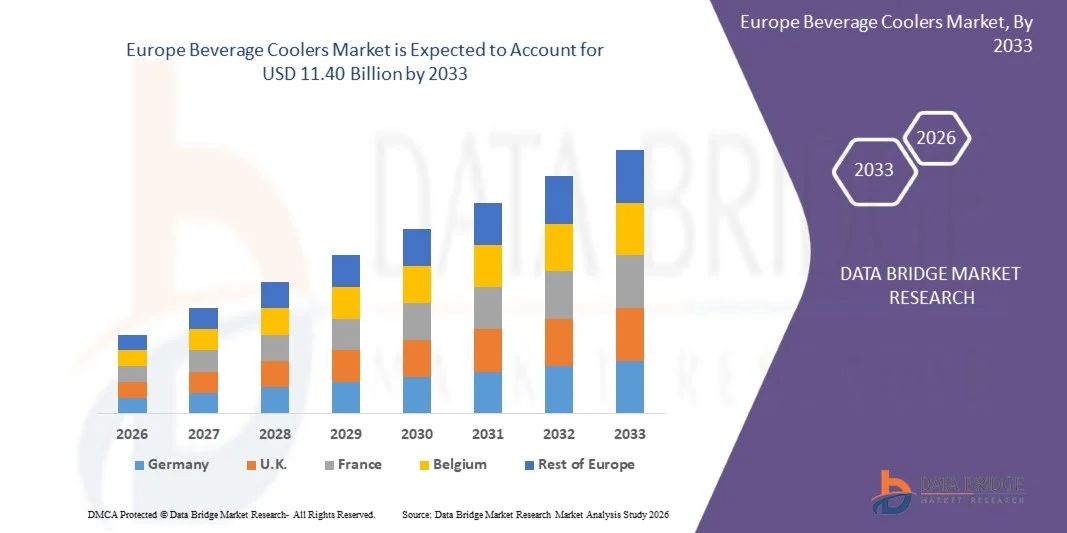

- The Europe beverage coolers market size was valued at USD 7.43 billion in 2025 and is expected to reach USD 11.40 billion by 2033, at a CAGR of 5.50% during the forecast period

- The market growth is largely fuelled by the rising demand for commercial refrigeration equipment across foodservice outlets, retail stores, and hospitality sectors driven by increasing consumption of chilled beverages

- Growing preference for energy-efficient and eco-friendly cooling systems is further accelerating market expansion as businesses focus on reducing operational costs and meeting sustainability regulations

Europe Beverage Coolers Market Analysis

- The Europe beverage coolers market is witnessing steady growth driven by strong demand from restaurants, bars, and quick-service food outlets across major European economies

- Rising innovation in refrigeration technologies, including smart temperature control and energy-efficient compressors, is enhancing product performance and boosting market adoption

- Germany beverage coolers market captured the largest revenue share in Europe in 2025, driven by strong demand for high-quality, energy-efficient refrigeration appliances and a well-established consumer preference for premium home appliances

- U.K. is expected to witness the highest compound annual growth rate (CAGR) in the Europe beverage coolers market due to rising demand for compact and stylish beverage storage solutions in urban households, increasing adoption of home entertainment systems, and growing preference for premium kitchen upgrades. In addition, expanding e-commerce penetration and availability of international appliance brands are further accelerating market growth across the country

- The 200–500L segment held the largest market revenue share in 2025 driven by strong adoption in both residential and small commercial setups such as cafés, bars, and boutique stores. This segment is preferred due to its balanced storage capacity and compact footprint, making it suitable for urban living spaces. Growing demand for energy-efficient mid-capacity cooling systems further supports segment dominance. Manufacturers are also focusing on improved insulation and smart temperature control features in this range

Report Scope and Europe Beverage Coolers Market Segmentation

|

Attributes |

Europe Beverage Coolers Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

• Electrolux AB (Sweden) |

|

Market Opportunities |

• Expansion Of Energy Efficient Refrigeration Systems |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Europe Beverage Coolers Market Trends

“Rising Demand For Energy Efficient And Smart Cooling Solutions”

• The increasing demand for energy efficient and technologically advanced refrigeration systems is significantly shaping the Europe beverage coolers market, as commercial establishments prioritize low energy consumption and improved cooling performance. Beverage coolers are increasingly being equipped with smart temperature control, LED lighting, and eco-friendly refrigerants to enhance operational efficiency while reducing environmental impact. This trend is further strengthened by stringent European energy regulations and sustainability targets across commercial sectors

• Growing consumption of chilled beverages across foodservice outlets, supermarkets, and convenience stores is accelerating demand for advanced beverage cooling solutions. Rising urban lifestyles and increasing preference for ready-to-drink beverages are encouraging retailers to invest in high-capacity and visually appealing beverage coolers that improve product visibility and boost sales

• Sustainability and carbon reduction initiatives are influencing purchasing decisions, with manufacturers focusing on eco-friendly cooling technologies, recyclable materials, and energy optimized compressor systems. These factors are helping companies reduce operational costs while aligning with environmental compliance standards, especially in Western European markets

• For instance, in 2024, Electrolux Professional in Sweden and Liebherr in Germany expanded their commercial refrigeration portfolios with next-generation beverage coolers featuring low-GWP refrigerants and improved energy efficiency. These product launches were targeted at hospitality and retail sectors to support sustainability goals while enhancing cooling performance across high-traffic environments

• Continuous innovation in refrigeration technology, including inverter compressors and IoT-enabled monitoring systems, is further improving temperature precision, reducing energy waste, and enhancing product reliability across commercial beverage cooling applications

Europe Beverage Coolers Market Dynamics

Driver

“Growing Expansion Of Hospitality And Retail Infrastructure”

• The rapid expansion of hotels, restaurants, bars, and quick service restaurants across Europe is a major driver for beverage coolers, as these establishments require efficient refrigeration systems to store and display chilled beverages. Increasing tourism activity and rising consumer spending on dining out are further supporting demand for commercial cooling equipment

• Growth of organized retail chains such as supermarkets, hypermarkets, and convenience stores is also boosting adoption of beverage coolers, as retailers focus on improving product visibility and customer experience through attractive refrigerated display units. These systems play a key role in driving impulse purchases and increasing beverage sales

• Rising preference for energy efficient and durable cooling equipment is encouraging businesses to replace traditional refrigeration systems with advanced beverage coolers that offer better temperature consistency and lower operating costs. This shift is further supported by strict energy efficiency regulations across European countries

• For instance, in 2023, Carrier Commercial Refrigeration in the U.K. and Frigoglass in Greece expanded their beverage cooler installations across major retail and hospitality chains to meet rising demand for efficient beverage storage solutions. These deployments helped improve product accessibility and enhanced cooling efficiency in high-traffic commercial environments

• Although demand is increasing, market growth depends on high initial investment costs and ongoing technological upgrades required to meet evolving energy efficiency standards

Restraint/Challenge

“High Installation Costs And Energy Compliance Requirements”

• The Europe beverage coolers market faces challenges due to high initial installation and maintenance costs associated with advanced refrigeration systems. Energy efficient and smart coolers often require significant upfront investment, limiting adoption among small and medium sized businesses

• Strict regulatory standards on energy consumption and refrigerant usage also increase compliance complexity for manufacturers and end users. Companies must continuously upgrade systems to meet evolving EU environmental regulations, which raises operational costs

• Dependence on electricity intensive cooling systems can also impact long term operational expenses, especially in regions with high energy prices. This creates cost pressure for businesses operating large scale retail and hospitality operations

• For instance, in 2024, several hospitality operators in Italy and Spain reported increased operational costs due to rising energy prices and mandatory upgrades to low-emission refrigeration systems, affecting profitability and delaying replacement cycles for beverage cooling equipment

• Addressing these challenges will require innovation in low-energy cooling technologies, wider adoption of eco-friendly refrigerants, and cost optimized product designs to ensure long term market sustainability and broader adoption across Europe

Europe Beverage Coolers Market Scope

The market is segmented on the basis of product type, type, temperature zones, size, cooler height, number of shelves, shelves material, finish, door swing, control type, distribution channel, application, and end-user.

• By Product Type

On the basis of product type, the Europe beverage coolers market is segmented into less than 200L, 200–500L, 500–1000L, and more than 1000L. The 200–500L segment held the largest market revenue share in 2025 driven by strong adoption in both residential and small commercial setups such as cafés, bars, and boutique stores. This segment is preferred due to its balanced storage capacity and compact footprint, making it suitable for urban living spaces. Growing demand for energy-efficient mid-capacity cooling systems further supports segment dominance. Manufacturers are also focusing on improved insulation and smart temperature control features in this range.

The more than 1000L segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing deployment in large commercial environments such as hotels, supermarkets, and event venues. These units provide high-volume storage, making them ideal for bulk beverage handling and continuous service requirements. Rising hospitality expansion across Europe is accelerating demand for large-capacity cooling solutions. In addition, advancements in modular design and multi-door configurations are improving usability and operational efficiency.

• By Type

On the basis of type, the market is segmented into freestanding, built-in and undercounter, countertop, dual zone, thermoelectric, and others. The freestanding segment held the largest market revenue share in 2025 driven by its flexibility, easy installation, and suitability for diverse spatial layouts. It is widely used in residential kitchens, retail outlets, and small commercial spaces due to its mobility. Freestanding coolers are also preferred for their lower installation cost and maintenance convenience. Increasing availability of stylish designs and compact models is further boosting demand.

The built-in and undercounter segment is expected to witness the fastest growth rate from 2026 to 2033, driven by rising demand for integrated kitchen and bar aesthetics in modern European homes. These systems offer seamless installation within cabinetry, improving space utilization and visual appeal. They are increasingly adopted in premium residential and hospitality applications. Technological advancements such as improved ventilation systems and noise reduction are also supporting segment growth.

• By Temperature Zones

On the basis of temperature zones, the market is segmented into single zone beverage coolers, dual zone beverage coolers, triple zone beverage coolers, and multi zone (4 or more zones) beverage coolers. The single zone segment held the largest market revenue share in 2025 driven by its simplicity, affordability, and ease of operation. These coolers are widely used for storing a single beverage category such as wine or soft drinks at a uniform temperature. They are especially popular in households and small cafés due to low maintenance requirements. Rising demand for cost-effective cooling solutions continues to support this segment.

The dual zone beverage coolers segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing consumer preference for storing multiple beverage types at different temperature settings. This functionality is highly valued in premium households and bars where wine and beer require separate cooling conditions. Dual zone systems enhance flexibility and improve beverage preservation quality. Growing interest in home entertainment setups is also contributing to demand growth.

• By Size

On the basis of size, the market is segmented into 6–50 bottle, 51–100 bottle, 101–200 bottle, and more than 201 bottle. The 6–50 bottle segment held the largest market revenue share in 2025 driven by strong adoption in residential applications with limited storage needs. These compact units are suitable for small households and personal beverage storage. Their affordability and space-saving design make them highly attractive in urban apartments. Increasing demand for entry-level beverage coolers further supports segment dominance.

The 101–200 bottle segment is expected to witness the fastest growth rate from 2026 to 2033, driven by rising demand from mid-sized restaurants, wine bars, and premium households. These units offer a strong balance between capacity and space efficiency. They are increasingly used in commercial establishments requiring moderate-to-high storage volume. Improvements in cooling consistency and shelf customization are also boosting adoption.

• By Cooler Height

On the basis of cooler height, the market is segmented into 28 to 32 inch, 33 to 36 inch, 38 to 56 inch, and above 56 inch. The 33 to 36 inch segment held the largest market revenue share in 2025 driven by compatibility with standard kitchen counter installations. This height range fits well in modular kitchen designs commonly used across Europe. It offers ergonomic access and efficient space utilization. Growing residential renovation activities are further driving demand for this segment.

The 38 to 56 inch segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing preference for high-capacity beverage storage solutions. These taller units provide enhanced storage flexibility and better organization of beverages. They are widely used in commercial and semi-commercial environments. Rising demand for premium lifestyle appliances is also supporting growth.

• By Number of Shelves

On the basis of number of shelves, the market is segmented into 1–2 shelves, 3–4 shelves, 5–6 shelves, 7–9 shelves, 9–12 shelves, and more than 13 shelves. The 3–4 shelves segment held the largest market revenue share in 2025 driven by optimal storage organization and compact internal design. This configuration is widely used in small beverage coolers for residential use. It allows efficient categorization of bottles while maintaining cooling efficiency. Increasing demand for mid-range coolers supports segment dominance.

The 7–9 shelves segment is expected to witness the fastest growth rate from 2026 to 2033, driven by rising adoption in commercial establishments such as bars and restaurants. These units support higher storage density and better product segmentation. Improved shelving materials and adjustable designs are enhancing usability. Growing beverage consumption in hospitality venues is further driving demand.

• By Shelves Material

On the basis of shelves material, the market is segmented into metal, tempered glass, wood, and others. The metal shelves segment held the largest market revenue share in 2025 driven by durability, strength, and ability to support heavy loads. Metal shelving is widely used in both residential and commercial beverage coolers. It offers long-term reliability and resistance to wear and tear. Cost-effectiveness also contributes to its strong market presence.

The tempered glass segment is expected to witness the fastest growth rate from 2026 to 2033, driven by rising demand for premium aesthetics and improved product visibility. Glass shelves enhance the visual appeal of beverage storage systems. They are increasingly used in luxury residential and hospitality environments. Advancements in reinforced glass technology are improving safety and durability.

• By Finish

On the basis of finish, the market is segmented into blacks, glass, panel ready, silver tones, stainless steel, and wood finishes. The stainless steel segment held the largest market revenue share in 2025 driven by its modern appearance and corrosion resistance. It is widely preferred in commercial kitchens and premium residential settings. Stainless steel finishes also offer easy maintenance and long-lasting durability. Increasing demand for professional-grade appliances supports this segment.

The panel ready segment is expected to witness the fastest growth rate from 2026 to 2033, driven by rising demand for fully integrated kitchen designs. These finishes allow beverage coolers to blend seamlessly with cabinetry. They are highly popular in luxury homes and high-end hospitality spaces. Growing focus on minimalist interior design trends is further accelerating adoption.

• By Door Swing

On the basis of door swing, the market is segmented into French door, left side door, reversible door, right side door, and side by side door. The reversible door segment held the largest market revenue share in 2025 driven by installation flexibility and adaptability to different room layouts. This feature is especially useful in compact kitchens and commercial spaces. It reduces spatial constraints and improves accessibility. Increasing demand for versatile appliance designs supports this segment.

The French door segment is expected to witness the fastest growth rate from 2026 to 2033, driven by rising preference for premium and aesthetically appealing appliances. French door designs enhance convenience and improve user experience. They are widely adopted in luxury residential and hospitality environments. Growing interest in high-end kitchen upgrades is supporting growth.

• By Control Type

On the basis of control type, the market is segmented into digital, electronic, touch, and turn knob. The digital control segment held the largest market revenue share in 2025 driven by precise temperature regulation and user-friendly interfaces. Digital systems are widely integrated into modern beverage coolers. They allow better monitoring and consistent cooling performance. Increasing adoption of smart appliances further supports this segment.

The touch control segment is expected to witness the fastest growth rate from 2026 to 2033, driven by rising demand for advanced and intuitive appliance interfaces. Touch controls enhance convenience and improve aesthetic appeal. They are increasingly used in premium beverage coolers. Growth in smart home adoption is also contributing to expansion.

• By Distribution Channel

On the basis of distribution channel, the market is segmented into specialty stores, supermarkets/hypermarkets, e-commerce, and others. The specialty stores segment held the largest market revenue share in 2025 driven by customer preference for expert guidance and product demonstration. These stores offer a wide range of premium appliance options. Consumers often prefer in-person evaluation before purchase. Strong retail presence across Europe supports this segment.

The e-commerce segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing digital adoption and convenience of online shopping. Online platforms offer wider product variety and competitive pricing. Home delivery and easy comparison features further enhance demand. Expanding internet penetration is also supporting growth.

• By Application

On the basis of application, the market is segmented into alcoholic and non-alcoholic. The alcoholic segment held the largest market revenue share in 2025 driven by strong demand for wine and beer storage solutions. Beverage coolers are widely used in households, bars, and restaurants for maintaining optimal serving temperatures. Wine culture across Europe further strengthens this segment. Increasing premium beverage consumption supports steady growth.

The non-alcoholic segment is expected to witness the fastest growth rate from 2026 to 2033, driven by rising consumption of soft drinks, juices, and energy beverages. Expanding café culture and quick-service restaurants are boosting demand. Growing health-conscious consumer trends are also contributing to this segment.

• By End-User

On the basis of end-user, the market is segmented into residential, commercial, bars, hotels and restaurants, lounges, corporate offices, movie theatres, bookstores, and others. The residential segment held the largest market revenue share in 2025 driven by increasing adoption of modern home appliances and lifestyle upgrades. Consumers are investing more in home entertainment and beverage storage solutions. Compact and stylish designs are further boosting residential demand.

The hotels and restaurants segment is expected to witness the fastest growth rate from 2026 to 2033, driven by expansion of the hospitality sector across Europe. These establishments require high-capacity and efficient beverage storage systems. Increasing tourism and dining-out trends are also supporting demand. Growing emphasis on service quality and beverage presentation further accelerates adoption.

Europe Beverage Coolers Market Regional Analysis

- The Germany beverage coolers market captured the largest revenue share in Europe in 2025, driven by strong demand for high-quality, energy-efficient refrigeration appliances and a well-established consumer preference for premium home appliances

- German consumers place high importance on durability, engineering precision, and sustainable energy consumption, which strongly supports the adoption of advanced beverage cooling systems. The expansion of modern kitchens, coupled with growing consumption of chilled beverages such as wine and beer, further fuels market growth

- In addition, Germany’s strong hospitality sector, including restaurants, bars, and hotels, continues to drive steady demand for commercial-grade beverage coolers

U.K. Beverage Coolers Market Insight

The U.K. beverage coolers market is expected to witness the fastest growth rate in Europe from 2026 to 2033, driven by increasing consumer inclination toward home entertainment systems and premium kitchen upgrades. The rising popularity of compact urban housing is boosting demand for space-efficient and stylish beverage cooling solutions. In addition, growing wine and craft beverage consumption across households and commercial establishments is accelerating market expansion. The rapid growth of e-commerce platforms and easy availability of international appliance brands are further supporting market penetration across the country.

Europe Beverage Coolers Market Share

The Europe beverage coolers industry is primarily led by well-established companies, including:

• Electrolux AB (Sweden)

• BSH Hausgeräte GmbH (Germany)

• Liebherr Group (Germany)

• Gorenje Group (Slovenia)

• Arçelik A.Ş. (Turkey)

• Vestel Elektronik Sanayi ve Ticaret A.Ş. (Turkey)

• Groupe SEB (France)

• EuroCave (France)

• Climadiff (France)

• Frigel Group (Italy)

• SMEG S.p.A. (Italy)

• Elica S.p.A. (Italy)

• Dometic Group AB (Sweden)

• Glen Dimplex Group (Ireland)

• Gram Commercial A/S (Denmark)

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.