Europe Blood Plasma And Plasma Derived Medicinal Products Market

Market Size in USD Billion

CAGR :

%

USD

7.88 Billion

USD

14.02 Billion

2025

2033

USD

7.88 Billion

USD

14.02 Billion

2025

2033

| 2026 –2033 | |

| USD 7.88 Billion | |

| USD 14.02 Billion | |

| % | |

|

Europe Blood Plasma & Plasma Derived Medicinal Products Market Size

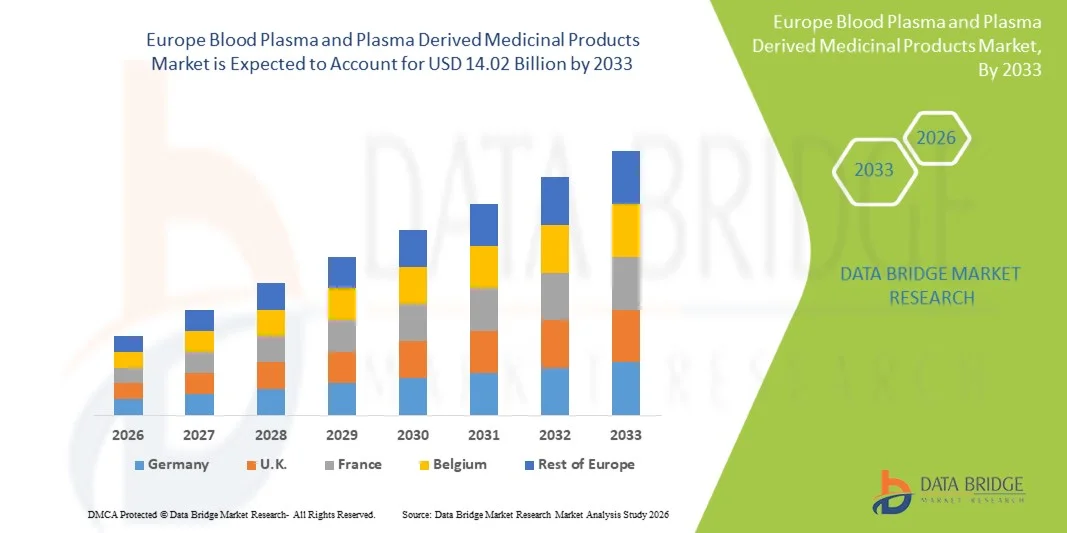

- The Europe blood plasma & plasma derived medicinal products market is expected to reach USD 14.02 Billion by 2033 from USD 7.88 Billion in 2025, growing with a substantial CAGR of 8.57% in the forecast period of 2026 to 2033

- The Europe Blood Plasma & Plasma-Derived Medicinal Products market growth is strongly driven by the rising prevalence of chronic, autoimmune, and rare diseases, such as immunodeficiency disorders, hemophilia, and neurological conditions. Increasing diagnosis rates, an aging population, and improved access to advanced therapies are significantly boosting demand for plasma-derived treatments including immunoglobulins, albumin, and clotting factors.

- Market expansion is further supported by advancements in plasma collection infrastructure and fractionation technologies, along with favorable regulatory frameworks and strong healthcare expenditure in the region. The growing number of plasma donation centers, coupled with increasing investments by major biopharmaceutical companies, is enhancing plasma supply availability and supporting the large-scale production of high-value plasma-derived medicinal products.

Europe Blood Plasma & Plasma Derived Medicinal Products Market Analysis

- The Europe Blood Plasma & Plasma-Derived Medicinal Products market is expanding at a steady CAGR, supported by the rising prevalence of chronic, autoimmune, and rare diseases, increasing demand for biologic therapies, well-established public healthcare systems, and continuous investments in plasma collection and fractionation capacity across the region.

- Blood plasma and plasma-derived medicinal products play a vital role in life-saving and long-term disease management therapies across Europe, supporting applications such as immunoglobulin replacement therapy, hemophilia treatment, critical care, and management of neurological and immunological disorders. Their essential role in advanced therapeutic care strengthens healthcare system resilience and innovation throughout the region.

- Germany dominates the Europe blood plasma & plasma-derived medicinal products market, accounting for approximately 14.55% market share in 2025, supported by its advanced healthcare infrastructure, strong biopharmaceutical manufacturing presence, high healthcare expenditure, and well-established plasma collection and processing network.

- Germany is also the fastest-growing country in the region, registering a CAGR of 9.35%, reflecting increasing demand for plasma-derived therapies, rising awareness and diagnosis of rare diseases, expansion of plasma donation centers, and continuous investments in domestic biopharmaceutical production and supply chain strengthening initiatives.

- Immunoglobulins are the dominating segment, accounting for 41.63% of the total market share in 2025, driven by their widespread use in treating primary immunodeficiency disorders, autoimmune diseases, and neurological conditions, along with expanding clinical indications and strong reimbursement coverage across major European countries.

Report Scope and Europe Blood Plasma & Plasma Derived Medicinal Products Market Segmentation

|

Attributes |

Europe Blood Plasma & Plasma Derived Medicinal Products Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Europe Blood Plasma & Plasma Derived Medicinal Products Market Trends

“Integration of Modern Healthcare Infrastructure”

- Expansion of advanced hospital networks and specialty care centers is driving higher adoption of plasma-derived medicinal products, as modern facilities are better equipped to administer complex biologic therapies such as immunoglobulins, clotting factors, and albumin.

- Improved cold-chain logistics and storage infrastructure across healthcare systems is supporting the safe handling, transportation, and long-term preservation of plasma-derived products, ensuring product efficacy and reducing wastage.

- Integration of digital health systems and electronic medical records (EMRs) is enhancing treatment tracking, dosing accuracy, and patient monitoring, enabling more efficient and outcome-based use of plasma-derived therapies.

- Strengthening of reimbursement frameworks and insurance coverage within modern healthcare ecosystems is improving patient access to high-cost plasma-derived treatments, particularly for chronic, rare, and life-threatening conditions.

- Adoption of standardized treatment protocols and regulatory-compliant practices in upgraded healthcare infrastructures is ensuring consistent quality, safety, and clinical effectiveness of plasma-derived medicinal products across hospitals and infusion centers.

Europe Blood Plasma & Plasma Derived Medicinal Products Market Dynamics

Driver

“Rising Prevalence of Rare and Chronic Diseases”

- The increasing prevalence of rare and chronic diseases globally is a critical driver for the growth of the blood plasma and Plasma-Derived Medicinal Products (PDMPs) market. Diseases such as Primary Immunodeficiency (PID), hemophilia, von Willebrand disease, alpha-1 antitrypsin deficiency, and various autoimmune and neurological disorders are being diagnosed more frequently due to advancements in diagnostic technologies and improved awareness among healthcare providers and patients.

- Demographic shifts, particularly the aging global population, further amplify demand for PDMPs. Older adults are more prone to chronic and degenerative conditions such as liver cirrhosis, multiple myeloma, chronic inflammatory disorders, and neurological diseases, many of which rely on plasma-derived products for effective management.

- These conditions often require long-term, sometimes lifelong, treatment with plasma-derived therapies such as immunoglobulins, coagulation factors, and albumin. For instance, patients with PID rely heavily on Intravenous Immunoglobulin (IVIG) to maintain immune function, while those with hemophilia require regular infusions of clotting factors to prevent bleeding episodes.

- The global aging population further contributes to this trend, as older adults are more susceptible to chronic conditions such as liver cirrhosis, multiple myeloma, and chronic inflammatory diseases that also require plasmaderived products. In addition, governments and health organizations are increasingly recognizing the burden of rare diseases, resulting in improved disease surveillance, the establishment of national registries, and more inclusive reimbursement policies.

For Instances

- In April 2025, CDC data showed that 76.4% of U.S. adults had at least one chronic condition, with 51.4% facing multiple conditions. This rising trend, including among young adults, highlights the growing burden of chronic diseases such as hemophilia, primary immunodeficiency diseases, and von willebrand disease, demanding greater focus on lifelong care and management.

- In March 2025, research featured in PMC emphasized the substantial global impact of rare diseases, collectively affecting millions worldwide, especially pediatric patients. The review highlights the complex interplay between genetic and environmental factors, as well as the persistent diagnostic challenges and delays. Despite advancements in genomic medicine and orphan drug development, effective treatments remain limited, necessitating comprehensive, multidisciplinary care approaches. This reinforces the ongoing struggle for timely and accurate diagnoses for these often-debilitating conditions

- In February 2025, a study focused on the Middle East and North Africa (MENA) region, published in PMC, underscores the disproportionately high prevalence of rare diseases in this area due to genetic and cultural factors, such as consanguinity. The report highlights critical challenges faced by patients, including limited disease knowledge and delayed diagnoses, despite governments and organizations implementing incentives for orphan drug development. This highlights that, despite global efforts, access to timely treatment for rare diseases remains limited in many region.

Restraint/Challenge

“High Cost and Complex Manufacturing Process”

- The high cost and complexity associated with the manufacturing of Plasma-Derived Medicinal Products (PDMPs) represent a major restraint in the global market. The production process involves multiple intricate stages, beginning with the collection of human plasma under strict medical and regulatory conditions. Each donation must be thoroughly tested for pathogens and other contaminants to ensure the safety and integrity of the source material. The subsequent fractionation and purification processes are technologically advanced, requiring specialized equipment, skilled labor, and a sterile environment.

- Manufacturing can take up to 12 months, from plasma collection to the final product, with each step needing rigorous quality control and compliance with international Good Manufacturing Practices (GMP). In addition, the need for cold-chain logistics throughout storage, transportation, and distribution further increases operational costs. These factors collectively lead to high capital investment and operational expenses, limiting the ability of smaller manufacturers and emerging economies to enter or expand in the market.

For Instances,

- A detailed analysis by Aykon Biosciences highlights that pharmaceutical manufacturing, particularly for complex biologics such as plasma-derived products, faces significant cost management challenges due to rising raw material and labor expenses, combined with increasingly stringent regulatory compliance requirements. The demand for personalized medicine and specialized therapies further drives the need for new, often expensive manufacturing processes. This necessitates substantial investment in advanced technology, highly trained personnel, and rigorous quality control measures, adding considerably to the final product cost.

Blood Plasma & Plasma Derived Medicinal Products Market Scope

The Europe blood plasma & plasma derived medicinal products market is segmented into six notable segments based on product, application, by processing technology, mode, end user, and distribution channel.

• By Product

On the basis of application, the market is segmented into Immunoglobulins, Coagulation Factors, Albumin, Protease Inhibitors, Monoclonal Antibodies, Other Plasma-Derived Proteins. In 2025 the Immunoglobulins type segment is excpected to dominate the market with 41.63% share which is driven by the rising prevalence of primary immunodeficiency disorders, autoimmune diseases, and neurological conditions requiring immunoglobulin replacement therapy. Increasing diagnosis rates, expanding therapeutic indications, and growing off-label use in inflammatory and rare disorders further support segment growth.

Coagulation Factors segment projected to be the fastest-growing segment in the global blood plasma & plasma derived medicinal products market, registering a CAGR of approximately 9.1%, this growth is primarily driven by the increasing prevalence of bleeding disorders such as hemophilia A and hemophilia B, along with rising awareness and improved diagnosis rates, particularly in emerging economies. Expanding access to prophylactic treatment, strong support from patient advocacy programs, and favorable reimbursement policies are further accelerating demand.

• By Application

On the basis of application, the market is segmented into immunology, hematology, critical care, neurology, pulmonology, haemato-oncology, rheumatology, and other applications. In 2025, Immunology is dominating segment with 31.02% market share primarily attributed to the rising prevalence of primary and secondary immunodeficiency disorders, autoimmune diseases, and inflammatory conditions requiring long-term immunoglobulin therapy. Increasing awareness, early diagnosis, and expanding clinical indications for plasma-derived immunoglobulins are significantly driving segment growth.

In 2025, the Neurology segment projected to be the fastest-growing segment in the global blood plasma & plasma derived medicinal products market, registering a CAGR of approximately 9.6%, due to the primarily driven by the rising prevalence of neurological disorders such as chronic inflammatory demyelinating polyneuropathy (CIDP), Guillain–Barré syndrome, myasthenia gravis, and multifocal motor neuropathy, where immunoglobulin therapies play a critical role. Increasing clinical acceptance of intravenous immunoglobulin (IVIG) and subcutaneous immunoglobulin (SCIG) for neurological indications, along with expanding research into new therapeutic applications, is further accelerating demand.

• By Technology

On the basis of processing technology, the market is segmented into ion exchange chromatography, affinity chromatography, cryoprecipitation, ultrafiltration, and microfiltration. In 2025, Ion exchange chromatography is the dominating segment with 32.95% share due to primarily attributed to its high efficiency in separating and purifying plasma proteins based on charge differences, ensuring superior product purity and yield. The technology is widely adopted in large-scale plasma fractionation due to its cost-effectiveness, scalability, and compatibility with stringent regulatory standards.

In 2025, the Ultrafiltration segment projected to be the fastest-growing segment in the global blood plasma & plasma derived medicinal products market, registering a CAGR of approximately 9.1%, due to the during the forecast period. This growth is primarily driven by increasing demand for efficient protein concentration and purification processes in plasma fractionation. Ultrafiltration enables precise separation based on molecular size, ensuring high product purity, improved recovery rates, and reduced processing time. The technology is widely utilized for concentration, desalting, and buffer exchange steps in the production of immunoglobulins and other plasma-derived proteins.

• By Mode

On the basis of mode, the market is segmented into modern and traditional plasma fractionation. In 2025, Modern is the dominating segment with 71.81% share due to the widespread adoption of advanced fractionation technologies that offer higher protein yield, enhanced purity levels, and improved safety profiles compared to conventional methods. Modern plasma fractionation integrates sophisticated chromatography techniques, automated processing systems, and stringent viral inactivation and removal steps, ensuring compliance with evolving regulatory standards.

In 2025, the Modern segment is segment projected to be the fastest-growing segment in the global blood plasma & plasma derived medicinal products market, registering a CAGR of approximately 8.7% due to increasing adoption of advanced plasma fractionation technologies that enhance product purity, safety, and overall manufacturing efficiency. Modern processes incorporate automated systems, advanced chromatography techniques, improved viral inactivation methods, and real-time quality monitoring, ensuring compliance with stringent regulatory standards. Rising demand for high-quality immunoglobulins, coagulation factors, and other plasma-derived therapies is accelerating the transition from traditional to technologically advanced fractionation methods.

• By End user

On the basis of end user, the market is segmented into hospitals & clinics, research labs, academic institutes, and others. In 2025, Hospitals & Clinics is the dominating segment with 66.68% share due to high volume of plasma-derived therapies administered in hospital settings for the treatment of immunological disorders, hemophilia, neurological conditions, and critical care cases. Hospitals serve as primary centers for diagnosis, emergency care, surgical procedures, and long-term disease management, resulting in consistent demand for immunoglobulins, coagulation factors, and albumin products.

In 2025, the research labs segment is segment projected to be the fastest-growing segment in the global blood plasma & plasma derived medicinal products market, registering a CAGR of approximately 9.2% due to increasing research activities focused on developing advanced plasma-derived therapies, novel biologics, and improved fractionation techniques. Rising investments in biotechnology and life sciences research, along with expanding clinical trials for rare and immune-related disorders, are accelerating demand for high-quality plasma proteins in laboratory settings.

• By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender, retail sales, and others. In 2025, Direct Tenders is the dominating segment with 53.07% share due to attributed to large-scale procurement by government bodies, public healthcare institutions, and major hospital networks through centralized purchasing agreements. Direct tender systems enable bulk purchasing at negotiated prices, ensuring cost efficiency, stable supply, and improved budget management for high-value plasma-derived therapies such as immunoglobulins and coagulation factors.

In 2025, the research labs segment is segment projected to be the fastest-growing segment in the global blood plasma & plasma derived medicinal products market, registering a CAGR of 8.8% due to rising focus on advanced biologics research, increasing clinical trials for rare and immune-related disorders, and expanding development of next-generation plasma-derived therapies. Research laboratories are actively involved in exploring novel therapeutic indications, improving protein purification techniques, and enhancing fractionation efficiency..

Europe Blood Plasma & Plasma Derived Medicinal Products Market Regional Analysis

- Germany dominates the Europe market with a significant share driven by advanced healthcare infrastructure, strong plasma collection and fractionation capabilities, and broad access to specialty biologic therapies. High healthcare expenditure, well-established reimbursement frameworks, and a substantial patient population requiring immunological and rare disease treatments further reinforce its leadership position in the region.

- Germany is strengthening its position through expanded plasma donation programs, increased domestic fractionation capacity, and supportive regulatory policies aimed at improving plasma self-sufficiency. Rising awareness of rare and autoimmune disorders, along with growing demand for high-quality plasma-derived therapies, is contributing to sustained market expansion within the country.

Across Europe, harmonized regulatory standards, strong pharmacovigilance systems, and increasing collaboration among biopharmaceutical companies are accelerating product development and approvals. Continued investments in advanced fractionation technologies, quality assurance systems, and regional supply chain resilience are enabling broader access to plasma-derived medicinal products throughout the European market.

Germany Blood Plasma & Plasma Derived Medicinal Products Market Insight

The Germany blood plasma and plasma-derived medicinal products market is driven by a strong plasma collection network, advanced biopharmaceutical manufacturing capabilities, and high healthcare expenditure. Rising prevalence of chronic, autoimmune, and rare diseases is fueling sustained demand for immunoglobulins, clotting factors, and albumin therapies. Supportive reimbursement policies, continuous technological advancements in plasma fractionation, and the presence of major industry players further strengthen market growth and ensure steady expansion across therapeutic applications.

France Blood Plasma & Plasma Derived Medicinal Products Market Insight

The France blood plasma and plasma-derived medicinal products market is supported by expanding healthcare infrastructure and growing demand for therapies used in immunodeficiency, neurological, and rare disease treatment. Government initiatives to strengthen plasma collection programs and reduce reliance on imports are improving domestic supply capabilities. Rising awareness of plasma-based therapies, favorable reimbursement frameworks, and ongoing investments in biologics manufacturing are contributing to steady market growth and improved patient access nationwide.

U.K. Blood Plasma & Plasma Derived Medicinal Products Market Insight

The U.K. blood plasma and plasma-derived medicinal products market is supported by expanding healthcare infrastructure and growing demand for therapies used in immunodeficiency, neurological, and rare disease treatment. Government initiatives to strengthen plasma collection programs and reduce reliance on imports are improving domestic supply capabilities. Rising awareness of plasma-based therapies, favorable reimbursement frameworks, and ongoing investments in biologics manufacturing are contributing to steady market growth and improved patient access nationwide.

Italy Blood Plasma & Plasma Derived Medicinal Products Market Insight

The Italy blood plasma and plasma-derived medicinal products market is supported by expanding healthcare infrastructure and growing demand for therapies used in immunodeficiency, neurological, and rare disease treatment. Government initiatives to strengthen plasma collection programs and reduce reliance on imports are improving domestic supply capabilities. Rising awareness of plasma-based therapies, favorable reimbursement frameworks, and ongoing investments in biologics manufacturing are contributing to steady market growth and improved patient access nationwide.

Spain Blood Plasma & Plasma Derived Medicinal Products Market Insight

The Spain blood plasma and plasma-derived medicinal products market is supported by expanding healthcare infrastructure and growing demand for therapies used in immunodeficiency, neurological, and rare disease treatment. Government initiatives to strengthen plasma collection programs and reduce reliance on imports are improving domestic supply capabilities. Rising awareness of plasma-based therapies, favorable reimbursement frameworks, and ongoing investments in biologics manufacturing are contributing to steady market growth and improved patient access nationwide.

Europe Blood Plasma & Plasma Derived Medicinal Products Market Share

The blood plasma & plasma derived medicinal products industry is primarily led by well-established companies, including:

- CSL Limited (Australia)

- Takeda Pharmaceutical Company Limited (Japan)

- Grifols, S.A. (Spain)

- Octapharma AG (Switzerland)

- Kedrion S.p.A. (Italy)

- ADMA Biologics, Inc. – (U.S.)

- Aegros (Australia)

- Bharat Serums (India)

- Biotest AG (Germany)

- Fresenius Kabi AG (Germany)

- GC Biopharma Corporate (South Korea)

- ICHOR (India)

- Intas Pharmaceuticals Ltd (India)

- Kamada Pharmaceuticals (Israel)

- KM Biologics (Japan)

- LFB (France)

- PlasmaGen BioSciences Pvt. Ltd. (India)

- Proliant Health & Biologicals (U.S.)

- Promea (India)

- Reliance Life Sciences (India)

- Sichuan Yuanda Shyuang Pharmaceutical Co., Ltd. (China)

- SK Plasma (South Korea)

- Synthaverse S.A. (Poland)

- Taibang Bio Group Co., Ltd. (China)

- VIRCHOW BIOTECH (India)

Latest Developments in Europe Blood Plasma & Plasma Derived Medicinal Products Market

- In November 2025, CSL announced a planned ~US$1.5 billion capital investment in the U.S. to expand its manufacturing footprint for plasma-derived therapies over the next five years. This investment is intended to strengthen domestic production, secure supply chains for critical products like immunoglobulins and other plasma-derived medicines, and generate hundred of skilled jobs in the U.S. manufacturing sector. This builds on more than US$3 billion already invested in U.S. operations since 2018.

- In October 2025, CSL’s Broadmeadows plasma fractionation facility in Victoria, Australia was recognized as a Facility of the Year winner by the International Society for Pharmaceutical Engineering (ISPE) in 2025. This facility one of the world’s largest for plasma processing uses advanced automation, robotics, digital twin technology, and sustainability features to significantly boost plasma processing capacity (over 10 million liters annually) and improve manufacturing efficiency.

- In February, Octapharma completed a USD 216 million USD expansion at its Vienna site, increasing production capacity by 50%, adding 160 jobs, and enhancing packaging, visual inspection, and logistics facilities—strengthening global supply of plasmaderived therapies for haemophilia, immunology, and critical care.

- In November 2024, CSL Plasma expanded its adoption of the advanced Rika Plasma Donation System across six U.S. donation centers near Denver, Colorado. These new devices, developed jointly with Terumo Blood & Cell Technologies, cut collection times by ~30% while improving donor comfort, safety, and efficiency.

- In June 2024, Takeda announced a USD 30 million expansion of its Los Angeles plasma‑fractionation facility, its global leader per capacity. This upgrade is expected to add up to 2 million liters/year of production volume, helping to meet rising global demand for plasma‑derived therapies used in treating immunodeficiencies and bleeding disorders.

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Table of Content

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW OF THE EUROPE BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET

1.4 LIMITATIONS

1.5 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 MARKETS COVERED

2.2 GEOGRAPHICAL SCOPE

2.3 YEARS CONSIDERED FOR THE STUDY

2.4 CURRENCY AND PRICING

2.5 DBMR TRIPOD DATA VALIDATION MODEL

2.6 MULTIVARIATE MODELLING

2.7 PRODUCT LIFELINE CURVE

2.8 PRIMARY INTERVIEWS WITH KEY OPINION LEADERS

2.9 DBMR MARKET POSITION GRID

2.1 MARKET END USER COVERAGE GRID

2.11 VENDOR SHARE ANALYSIS

2.12 SECONDARY SOURCES

2.13 ASSUMPTIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 PESTEL ANALYSIS

4.1.1 POLITICAL FACTORS

4.1.2 ECONOMIC FACTORS

4.1.3 SOCIAL FACTORS

4.1.4 TECHNOLOGICAL FACTORS

4.1.5 LEGAL FACTORS

4.1.6 ENVIRONMENTAL FACTORS

4.2 PORTER’S FIVE FORCES

4.2.1 THREAT OF NEW ENTRANTS

4.2.2 BARGAINING POWER OF SUPPLIERS

4.2.3 BARGAINING POWER OF BUYERS

4.2.4 THREAT OF SUBSTITUTES

4.2.5 COMPETITIVE RIVALRY

4.3 INNOVATION STRATEGIES

4.3.1 KEY INNOVATION STRATEGIES

4.3.2 EMERGING DELIVERY TECHNIQUES

4.3.3 STRATEGIC IMPLICATIONS

4.3.4 CONCLUSION

4.4 INNOVATION STRATEGIES

4.4.1 KEY INNOVATION STRATEGIES

4.4.2 EMERGING DELIVERY TECHNIQUES

4.4.3 STRATEGIC IMPLICATIONS

4.4.4 CONCLUSION

4.5 SUPPLY CHAIN ANALYSIS

4.5.1 OVERVIEW

4.5.2 RAW MATERIAL AVAILABILITY

4.5.3 MANUFACTURING CAPACITY

4.5.4 LOGISTICS AND LAST-MILE HURDLES

4.5.5 PRICING MODELS AND MARKET POSITIONING

4.6 RISK AND MITIGATION

4.7 VENDOR SELECTION DYNAMICS

4.7.1 PRODUCT QUALITY AND REGULATORY EXCELLENCE

4.7.2 PLASMA SUPPLY SECURITY AND SUPPLY CHAIN RESILIENCE

4.7.3 CLINICAL PERFORMANCE, INDICATION BREADTH, AND INNOVATION

4.7.4 COST STRUCTURE, CONTRACT FLEXIBILITY, AND REIMBURSEMENT ALIGNMENT

4.7.5 GEOGRAPHIC FOOTPRINT AND LOCAL MARKET SUPPORT

4.7.6 ETHICAL PLASMA SOURCING, ESG COMMITMENTS, AND TRANSPARENCY

4.7.7 STRATEGIC PARTNERSHIPS AND LONG-TERM VALUE CREATION

4.7.8 CONCLUSION

5 TARIFFS & IMPACT ON THE MARKET

5.1 CURRENT TARIFF RATES IN TOP-5 COUNTRY MARKETS

5.2 OUTLOOK: LOCAL PRODUCTION VS. IMPORT RELIANCE

5.3 VENDOR SELECTION CRITERIA DYNAMICS

5.4 IMPACT ON SUPPLY CHAIN

5.4.1 PLASMA COLLECTION & RAW MATERIAL AVAILABILITY

5.4.2 MANUFACTURING AND FRACTIONATION

5.4.3 LOGISTICS AND DISTRIBUTION

5.4.4 PRICING AND MARKET POSITIONING

5.5 INDUSTRY PARTICIPANTS: PROACTIVE MOVES

5.5.1 SUPPLY CHAIN OPTIMIZATION

5.5.2 STRATEGIC PARTNERSHIPS & JOINT VENTURES

5.6 IMPACT ON PRICES

5.7 REGULATORY INCLINATION

5.7.1 GCC TRADE ALIGNMENT & FTAS

5.7.2 SPECIAL ZONES AND RE-EXPORT MODELS

5.7.3 LOCAL SUBSIDY & POLICY RESPONSE

5.7.4 DOMESTIC COURSE OF CORRECTION

6 REGULATION COVERAGE

7 MARKET OVERVIEW

7.1 DRIVER

7.1.1 RISING PREVALENCE OF RARE AND CHRONIC DISEASES

7.1.2 EXPANDING GERIATRIC POPULATION

7.1.3 TECHNOLOGICAL ADVANCEMENTS IN PLASMA FRACTIONATION

7.1.4 GOVERNMENT AND INSTITUTIONAL SUPPORT

7.2 RESTRAINTS

7.2.1 HIGH COST AND COMPLEX MANUFACTURING PROCESS

7.2.2 LACK OF PLASMA SUPPLY AND DONOR

7.3 OPPORTUNITIES

7.3.1 ADVANCEMENTS IN PLASMA PROCESSING TECHNOLOGIES TO ENHANCE YIELD AND REDUCE COSTS

7.3.2 REIMBURSEMENT FRAMEWORKS AND INCREASED GOVERNMENTAL FOCUS ON RARE DISEASE TREATMENT

7.3.3 STRATEGIC ALLIANCES, MERGERS, AND ACQUISITIONS TO STRENGTHEN EUROPE MARKET PENETRATION

7.4 CHALLENGES

7.4.1 COMPETITIVE PRESSURE FROM RECOMBINANT AND ALTERNATIVE BIOLOGICAL THERAPIES

7.4.2 INFRASTRUCTURE LIMITATIONS IN COLD CHAIN LOGISTICS IMPACTING PRODUCT DISTRIBUTION

8 EUROPE BLOOD PLASMA AND PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY PRODUCT

8.1 OVERVIEW

8.2 IMMUNOGLOBULINS

8.3 COAGULATION FACTORS

8.4 ALBUMIN

8.5 PROTEASE INHIBITORS

8.6 MONOCLONAL ANTIBODIES

8.7 OTHER PLASMA DERIVED PROTEINS

8.8 EUROPE IMMUNOGLOBULINS IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.8.1 NORTH AMERICA

8.8.2 EUROPE

8.8.3 ASIA-PACIFIC

8.8.4 SOUTH AMERICA

8.8.5 MIDDLE EAST AND AFRICA

8.9 EUROPE COAGULATION FACTORS IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.9.1 NORTH AMERICA

8.9.2 EUROPE

8.9.3 ASIA-PACIFIC

8.9.4 SOUTH AMERICA

8.9.5 MIDDLE EAST AND AFRICA

8.1 EUROPE ALBUMIN IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.10.1 NORTH AMERICA

8.10.2 EUROPE

8.10.3 ASIA-PACIFIC

8.10.4 SOUTH AMERICA

8.10.5 MIDDLE EAST AND AFRICA

8.11 EUROPE PROTEASE INHIBITORS IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.11.1 NORTH AMERICA

8.11.2 EUROPE

8.11.3 ASIA-PACIFIC

8.11.4 SOUTH AMERICA

8.11.5 MIDDLE EAST AND AFRICA

8.12 EUROPE MONOCLONAL ANTIBODIES IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.12.1 NORTH AMERICA

8.12.2 EUROPE

8.12.3 ASIA-PACIFIC

8.12.4 SOUTH AMERICA

8.12.5 MIDDLE EAST AND AFRICA

8.13 EUROPE OTHER PLASMA DERIVED PROTEINS IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.13.1 NORTH AMERICA

8.13.2 EUROPE

8.13.3 ASIA-PACIFIC

8.13.4 SOUTH AMERICA

8.13.5 MIDDLE EAST AND AFRICA

9 EUROPE BLOOD PLASMA AND PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY APPLICATION

9.1 OVERVIEW

9.2 IMMUNOLOGY

9.3 HAEMATOLOGY

9.4 CRITICAL CARE

9.5 NEUROLOGY

9.6 PULMONOLOGY

9.7 HAEMATO-ONCOLOGY

9.8 RHEUMATOLOGY

9.9 OTHER APPLICATIONS

9.1 EUROPE IMMUNOLOGY IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.10.1 NORTH AMERICA

9.10.2 EUROPE

9.10.3 ASIA-PACIFIC

9.10.4 SOUTH AMERICA

9.10.5 MIDDLE EAST AND AFRICA

9.11 EUROPE HAEMATOLOGY IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.11.1 NORTH AMERICA

9.11.2 EUROPE

9.11.3 ASIA-PACIFIC

9.11.4 SOUTH AMERICA

9.11.5 MIDDLE EAST AND AFRICA

9.12 EUROPE CRITICAL CARE IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.12.1 NORTH AMERICA

9.12.2 EUROPE

9.12.3 ASIA-PACIFIC

9.12.4 SOUTH AMERICA

9.12.5 MIDDLE EAST AND AFRICA

9.13 EUROPE NEUROLOGY IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.13.1 NORTH AMERICA

9.13.2 EUROPE

9.13.3 ASIA-PACIFIC

9.13.4 SOUTH AMERICA

9.13.5 MIDDLE EAST AND AFRICA

9.14 EUROPE PULMONOLOGY IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.14.1 NORTH AMERICA

9.14.2 EUROPE

9.14.3 ASIA-PACIFIC

9.14.4 SOUTH AMERICA

9.14.5 MIDDLE EAST AND AFRICA

9.15 EUROPE HAEMATO-ONCOLOGY IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.15.1 NORTH AMERICA

9.15.2 EUROPE

9.15.3 ASIA-PACIFIC

9.15.4 SOUTH AMERICA

9.15.5 MIDDLE EAST AND AFRICA

9.16 EUROPE RHEUMATOLOGY IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.16.1 NORTH AMERICA

9.16.2 EUROPE

9.16.3 ASIA-PACIFIC

9.16.4 SOUTH AMERICA

9.16.5 MIDDLE EAST AND AFRICA

9.17 EUROPE OTHER APPLICATIONS IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.17.1 NORTH AMERICA

9.17.2 EUROPE

9.17.3 ASIA-PACIFIC

9.17.4 SOUTH AMERICA

9.17.5 MIDDLE EAST AND AFRICA

10 EUROPE BLOOD PLASMA AND PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY TECHNOLOGY

10.1 OVERVIEW

10.2 ION EXCHANGE CHROMATOGRAPHY

10.3 AFFINITY CHROMATOGRAPHY

10.4 CRYOPRECIPITATION

10.5 ULTRAFILTRATION

10.6 MICROFILTRATION

10.7 EUROPE ION EXCHANGE CHROMATOGRAPHY IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

10.7.1 NORTH AMERICA

10.7.2 EUROPE

10.7.3 ASIA-PACIFIC

10.7.4 SOUTH AMERICA

10.7.5 MIDDLE EAST AND AFRICA

10.8 EUROPE AFFINITY CHROMATOGRAPHY IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

10.8.1 NORTH AMERICA

10.8.2 EUROPE

10.8.3 ASIA-PACIFIC

10.8.4 SOUTH AMERICA

10.8.5 MIDDLE EAST AND AFRICA

10.9 EUROPE CRYOPRECIPITATION IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

10.9.1 NORTH AMERICA

10.9.2 EUROPE

10.9.3 ASIA-PACIFIC

10.9.4 SOUTH AMERICA

10.9.5 MIDDLE EAST AND AFRICA

10.1 EUROPE ULTRAFILTRATION IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

10.10.1 NORTH AMERICA

10.10.2 EUROPE

10.10.3 ASIA-PACIFIC

10.10.4 SOUTH AMERICA

10.10.5 MIDDLE EAST AND AFRICA

10.11 EUROPE MICROFILTRATION IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

10.11.1 NORTH AMERICA

10.11.2 EUROPE

10.11.3 ASIA-PACIFIC

10.11.4 SOUTH AMERICA

10.11.5 MIDDLE EAST AND AFRICA

11 EUROPE BLOOD PLASMA AND PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY MODE

11.1 OVERVIEW

11.2 MODERN

11.3 TRADITIONAL PLASMA FRACTIONATION

11.4 EUROPE MODERN IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.4.1 NORTH AMERICA

11.4.2 EUROPE

11.4.3 ASIA-PACIFIC

11.4.4 SOUTH AMERICA

11.4.5 MIDDLE EAST AND AFRICA

11.5 EUROPE TRADITIONAL PLASMA FRACTIONATION IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.5.1 NORTH AMERICA

11.5.2 EUROPE

11.5.3 ASIA-PACIFIC

11.5.4 SOUTH AMERICA

11.5.5 MIDDLE EAST AND AFRICA

12 EUROPE BLOOD PLASMA AND PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY END USER

12.1 OVERVIEW

12.2 HOSPITALS & CLINICS

12.3 RESEARCH LABS

12.4 ACADEMIC INSTITUTES

12.5 OTHERS

12.6 EUROPE HOSPITALS & CLINICS IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.6.1 NORTH AMERICA

12.6.2 EUROPE

12.6.3 ASIA-PACIFIC

12.6.4 SOUTH AMERICA

12.6.5 MIDDLE EAST AND AFRICA

12.7 EUROPE RESEARCH LABS IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.7.1 NORTH AMERICA

12.7.2 EUROPE

12.7.3 ASIA-PACIFIC

12.7.4 SOUTH AMERICA

12.7.5 MIDDLE EAST AND AFRICA

12.8 EUROPE ACADEMIC INSTITUTES IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.8.1 NORTH AMERICA

12.8.2 EUROPE

12.8.3 ASIA-PACIFIC

12.8.4 SOUTH AMERICA

12.8.5 MIDDLE EAST AND AFRICA

12.9 EUROPE OTHERS IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.9.1 NORTH AMERICA

12.9.2 EUROPE

12.9.3 ASIA-PACIFIC

12.9.4 SOUTH AMERICA

12.9.5 MIDDLE EAST AND AFRICA

13 EUROPE BLOOD PLASMA AND PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY DISTRIBUTION CHANNEL

13.1 OVERVIEW

13.2 DIRECT TENDERS

13.3 THIRD PARTY DISTRIBUTORS

13.4 OTHERS

13.5 EUROPE DIRECT TENDERS IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

13.5.1 NORTH AMERICA

13.5.2 EUROPE

13.5.3 ASIA-PACIFIC

13.5.4 SOUTH AMERICA

13.5.5 MIDDLE EAST AND AFRICA

13.6 EUROPE THIRD PARTY DISTRIBUTORS IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

13.6.1 NORTH AMERICA

13.6.2 EUROPE

13.6.3 ASIA-PACIFIC

13.6.4 SOUTH AMERICA

13.6.5 MIDDLE EAST AND AFRICA

13.7 EUROPE OTHERS IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

13.7.1 NORTH AMERICA

13.7.2 EUROPE

13.7.3 ASIA-PACIFIC

13.7.4 SOUTH AMERICA

13.7.5 MIDDLE EAST AND AFRICA

14 EUROPE BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION

14.1 EUROPE

14.1.1 GERMANY

14.1.2 FRANCE

14.1.3 UNITED KINGDOM

14.1.4 ITALY

14.1.5 SPAIN

14.1.6 RUSSIA

14.1.7 SWITZERLAND

14.1.8 TURKEY

14.1.9 NETHERLANDS

14.1.10 POLAND

14.1.11 SWEDEN

14.1.12 DENMARK

14.1.13 BELGIUM

14.1.14 IRELAND

14.1.15 NORWAY

14.1.16 FINLAND

14.1.17 REST OF EUROPE

15 EUROPE BLOOD PLASMA AND PLASMA DERIVED MEDICINAL PRODUCTS MARKET: COMPANY LANDSCAPE

15.1 COMPANY SHARE ANALYSIS: GLOBAL

16 SWOT ANALYSIS

17 COMPANY PROFILE

17.1 CSL

17.1.1 COMPANY SNAPSHOT

17.1.2 REVENUE ANALYSIS

17.1.3 COMPANY SHARE ANALYSIS

17.1.4 PRODUCT PORTFOLIO

17.1.5 RECENT DEVELOPMENT

17.2 TAKEDA PHARMACEUTICAL COMPANY LIMITED

17.2.1 COMPANY SNAPSHOT

17.2.2 REVENUE ANALYSIS

17.2.3 COMPANY SHARE ANALYSIS

17.2.4 PRODUCT PORTFOLIO

17.2.5 RECENT DEVELOPMENT

17.3 GRIFOLS, S.A.

17.3.1 COMPANY SNAPSHOT

17.3.2 REVENUE ANALYSIS

17.3.3 COMPANY SHARE ANALYSIS

17.3.4 PRODUCT PORTFOLIO

17.3.5 RECENT DEVELOPMENT

17.4 OCTAPHARMA AG

17.4.1 COMPANY SNAPSHOT

17.4.2 COMPANY SHARE ANALYSIS

17.4.3 PRODUCT PORTFOLIO

17.4.4 RECENT DEVELOPMENT

17.5 KEDRION

17.5.1 COMPANY SNAPSHOT

17.5.2 COMPANY SHARE ANALYSIS

17.5.3 PRODUCT PORTFOLIO

17.5.4 RECENT DEVELOPMENT

17.6 ADMA BIOLOGICS, INC

17.6.1 COMPANY SNAPSHOT

17.6.2 REVENUE ANALYSIS

17.6.3 PRODUCT PORTFOLIO

17.6.4 RECENT DEVELOPMENT

17.7 AEGROS

17.7.1 COMPANY SNAPSHOT

17.7.2 PRODUCT PORTFOLIO

17.7.3 RECENT DEVELOPMENT

17.8 BHARAT SERUMS

17.8.1 COMPANY SNAPSHOT

17.8.2 PRODUCT PORTFOLIO

17.8.3 RECENT DEVELOPMENT

17.9 BIOTEST AG.

17.9.1 COMPANY SNAPSHOT

17.9.2 REVENUE ANALYSIS

17.9.3 PRODUCT PORTFOLIO

17.9.4 RECENT DEVELOPMENT

17.1 FRESENIUS KABI AG

17.10.1 COMPANY SNAPSHOT

17.10.2 PRODUCT PORTFOLIO

17.10.3 RECENT DEVELOPMENT

17.11 GC BIOPHARMA CORPORATE

17.11.1 COMPANY SNAPSHOT

17.11.2 REVENUE ANALYSIS

17.11.3 PRODUCT PORTFOLIO

17.11.4 RECENT DEVELOPMENT

17.12 ICHOR

17.12.1 COMPANY SNAPSHOT

17.12.2 PRODUCT PORTFOLIO

17.12.3 RECENT DEVELOPMENT

17.13 INTAS PHARMACEUTICALS LTD.

17.13.1 COMPANY SNAPSHOT

17.13.2 PRODUCT PORTFOLIO

17.13.3 RECENT DEVELOPMENT

17.14 KAMADA PHARMACEUTICALS

17.14.1 COMPANY SNAPSHOT

17.14.2 REVENUE ANALYSIS

17.14.3 PRODUCT PORTFOLIO

17.14.4 RECENT DEVELOPMENT

17.15 KM BIOLOGICS

17.15.1 COMPANY SNAPSHOT

17.15.2 PRODUCT PORTFOLIO

17.15.3 RECENT DEVELOPMENT

17.16 LFB

17.16.1 COMPANY SNAPSHOT

17.16.2 THERAPY PORTFOLIO

17.16.3 RECENT DEVELOPMENT

17.17 PLASMAGEN BIOSCIENCES PVT. LTD.

17.17.1 COMPANY SNAPSHOT

17.17.2 PRODUCT PORTFOLIO

17.17.3 RECENT DEVELOPMENT

17.18 PROLIANT HEALTH & BIOLOGICALS

17.18.1 COMPANY SNAPSHOT

17.18.2 PRODUCT PORTFOLIO

17.18.3 RECENT DEVELOPMENT

17.19 PROMEA

17.19.1 COMPANY SNAPSHOT

17.19.2 PRODUCT PORTFOLIO

17.19.3 RECENT DEVELOPMENT

17.2 RELIANCE LIFE SCIENCES.

17.20.1 COMPANY SNAPSHOT

17.20.2 PRODUCT PORTFOLIO

17.20.3 RECENT DEVELOPMENT

17.21 SICHUAN YUANDA SHYUANG PHARMACEUTICAL CO., LTD.

17.21.1 COMPANY SNAPSHOT

17.21.2 PRODUCT PORTFOLIO

17.21.3 RECENT DEVELOPMENT

17.22 SK PLASMA

17.22.1 COMPANY SNAPSHOT

17.22.2 PRODUCT PORTFOLIO

17.22.3 RECENT DEVELOPMENT

17.23 SYNTHAVERSE S. A.

17.23.1 COMPANY SNAPSHOT

17.23.2 REVENUE ANALYSIS

17.23.3 PRODUCT PORTFOLIO

17.23.4 RECENT DEVELOPMENT

17.24 TAIBANG BIO GROUP CO., LTD

17.24.1 COMPANY SNAPSHOT

17.24.2 PRODUCT PORTFOLIO

17.24.3 RECENT DEVELOPMENT

17.25 VIRCHOW BIOTECH

17.25.1 COMPANY SNAPSHOT

17.25.2 PRODUCT PORTFOLIO

17.25.3 RECENT DEVELOPMENT

18 QUESTIONNAIRE

19 RELATED REPORTS

List of Table

TABLE 1 EUROPE BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY PRODUCT, 2018-2033 (USD THOUSAND)

TABLE 2 EUROPE IMMUNOGLOBULINS IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 3 EUROPE COAGULATION FACTORS IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 4 EUROPE ALBUMIN IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 5 EUROPE PROTEASE INHIBITORS IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 6 EUROPE MONOCLONAL ANTIBODIES IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 7 EUROPE OTHER PLASMA DERIVED PROTEINS IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 8 EUROPE BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 9 EUROPE IMMUNOLOGY IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 10 EUROPE HAEMATOLOGY IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 11 EUROPE CRITICAL CARE IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 12 EUROPE NEUROLOGY IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 13 EUROPE PULMONOLOGY IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 14 EUROPE HAEMATO-ONCOLOGY IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 15 EUROPE RHEUMATOLOGY IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 16 EUROPE OTHER APPLICATIONS IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 17 EUROPE BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY TECHNOLOGY, 2018-2033 (USD THOUSAND)

TABLE 18 EUROPE ION EXCHANGE CHROMATOGRAPHY IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 19 EUROPE AFFINITY CHROMATOGRAPHY IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 20 EUROPE CRYOPRECIPITATION IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 21 EUROPE ULTRAFILTRATION IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 22 EUROPE MICROFILTRATION IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 23 EUROPE BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY MODE, 2018-2033 (USD THOUSAND)

TABLE 24 EUROPE MODERN IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 25 EUROPE TRADITIONAL PLASMA FRACTIONATION IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 26 EUROPE BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 27 EUROPE HOSPITALS & CLINICS IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 28 EUROPE RESEARCH LABS IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 29 EUROPE ACADEMIC INSTITUTES IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 30 EUROPE OTHERS IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 31 EUROPE BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 32 EUROPE DIRECT TENDERS IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 33 EUROPE THIRD PARTY DISTRIBUTORS IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 34 EUROPE OTHERS IN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 35 EUROPE BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY COUNTRY, 2018-2033 (USD THOUSAND)

TABLE 36 EUROPE BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY PRODUCT, 2018-2033 (USD THOUSAND)

TABLE 37 EUROPE BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 38 EUROPE BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY TECHNOLOGY, 2018-2033 (USD THOUSAND)

TABLE 39 EUROPE BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY MODE, 2018-2033 (USD THOUSAND)

TABLE 40 EUROPE BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 41 EUROPE BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 42 GERMANY BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY PRODUCT, 2018-2033 (USD THOUSAND)

TABLE 43 GERMANY BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 44 GERMANY BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY TECHNOLOGY, 2018-2033 (USD THOUSAND)

TABLE 45 GERMANY BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY MODE, 2018-2033 (USD THOUSAND)

TABLE 46 GERMANY BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 47 GERMANY BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 48 FRANCE BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY PRODUCT, 2018-2033 (USD THOUSAND)

TABLE 49 FRANCE BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 50 FRANCE BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY TECHNOLOGY, 2018-2033 (USD THOUSAND)

TABLE 51 FRANCE BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY MODE, 2018-2033 (USD THOUSAND)

TABLE 52 FRANCE BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 53 FRANCE BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 54 UNITED KINGDOM BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY PRODUCT, 2018-2033 (USD THOUSAND)

TABLE 55 UNITED KINGDOM BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 56 UNITED KINGDOM BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY TECHNOLOGY, 2018-2033 (USD THOUSAND)

TABLE 57 UNITED KINGDOM BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY MODE, 2018-2033 (USD THOUSAND)

TABLE 58 UNITED KINGDOM BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 59 UNITED KINGDOM BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 60 ITALY BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY PRODUCT, 2018-2033 (USD THOUSAND)

TABLE 61 ITALY BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 62 ITALY BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY TECHNOLOGY, 2018-2033 (USD THOUSAND)

TABLE 63 ITALY BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY MODE, 2018-2033 (USD THOUSAND)

TABLE 64 ITALY BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 65 ITALY BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 66 SPAIN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY PRODUCT, 2018-2033 (USD THOUSAND)

TABLE 67 SPAIN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 68 SPAIN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY TECHNOLOGY, 2018-2033 (USD THOUSAND)

TABLE 69 SPAIN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY MODE, 2018-2033 (USD THOUSAND)

TABLE 70 SPAIN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 71 SPAIN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 72 RUSSIA BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY PRODUCT, 2018-2033 (USD THOUSAND)

TABLE 73 RUSSIA BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 74 RUSSIA BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY TECHNOLOGY, 2018-2033 (USD THOUSAND)

TABLE 75 RUSSIA BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY MODE, 2018-2033 (USD THOUSAND)

TABLE 76 RUSSIA BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 77 RUSSIA BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 78 SWITZERLAND BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY PRODUCT, 2018-2033 (USD THOUSAND)

TABLE 79 SWITZERLAND BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 80 SWITZERLAND BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY TECHNOLOGY, 2018-2033 (USD THOUSAND)

TABLE 81 SWITZERLAND BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY MODE, 2018-2033 (USD THOUSAND)

TABLE 82 SWITZERLAND BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 83 SWITZERLAND BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 84 TURKEY BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY PRODUCT, 2018-2033 (USD THOUSAND)

TABLE 85 TURKEY BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 86 TURKEY BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY TECHNOLOGY, 2018-2033 (USD THOUSAND)

TABLE 87 TURKEY BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY MODE, 2018-2033 (USD THOUSAND)

TABLE 88 TURKEY BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 89 TURKEY BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 90 NETHERLANDS BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY PRODUCT, 2018-2033 (USD THOUSAND)

TABLE 91 NETHERLANDS BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 92 NETHERLANDS BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY TECHNOLOGY, 2018-2033 (USD THOUSAND)

TABLE 93 NETHERLANDS BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY MODE, 2018-2033 (USD THOUSAND)

TABLE 94 NETHERLANDS BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 95 NETHERLANDS BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 96 POLAND BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY PRODUCT, 2018-2033 (USD THOUSAND)

TABLE 97 POLAND BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 98 POLAND BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY TECHNOLOGY, 2018-2033 (USD THOUSAND)

TABLE 99 POLAND BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY MODE, 2018-2033 (USD THOUSAND)

TABLE 100 POLAND BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 101 POLAND BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 102 SWEDEN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY PRODUCT, 2018-2033 (USD THOUSAND)

TABLE 103 SWEDEN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 104 SWEDEN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY TECHNOLOGY, 2018-2033 (USD THOUSAND)

TABLE 105 SWEDEN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY MODE, 2018-2033 (USD THOUSAND)

TABLE 106 SWEDEN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 107 SWEDEN BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 108 DENMARK BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY PRODUCT, 2018-2033 (USD THOUSAND)

TABLE 109 DENMARK BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 110 DENMARK BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY TECHNOLOGY, 2018-2033 (USD THOUSAND)

TABLE 111 DENMARK BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY MODE, 2018-2033 (USD THOUSAND)

TABLE 112 DENMARK BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 113 DENMARK BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 114 BELGIUM BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY PRODUCT, 2018-2033 (USD THOUSAND)

TABLE 115 BELGIUM BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 116 BELGIUM BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY TECHNOLOGY, 2018-2033 (USD THOUSAND)

TABLE 117 BELGIUM BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY MODE, 2018-2033 (USD THOUSAND)

TABLE 118 BELGIUM BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 119 BELGIUM BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 120 IRELAND BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY PRODUCT, 2018-2033 (USD THOUSAND)

TABLE 121 IRELAND BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 122 IRELAND BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY TECHNOLOGY, 2018-2033 (USD THOUSAND)

TABLE 123 IRELAND BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY MODE, 2018-2033 (USD THOUSAND)

TABLE 124 IRELAND BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 125 IRELAND BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 126 NORWAY BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY PRODUCT, 2018-2033 (USD THOUSAND)

TABLE 127 NORWAY BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 128 NORWAY BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY TECHNOLOGY, 2018-2033 (USD THOUSAND)

TABLE 129 NORWAY BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY MODE, 2018-2033 (USD THOUSAND)

TABLE 130 NORWAY BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 131 NORWAY BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 132 FINLAND BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY PRODUCT, 2018-2033 (USD THOUSAND)

TABLE 133 FINLAND BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 134 FINLAND BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY TECHNOLOGY, 2018-2033 (USD THOUSAND)

TABLE 135 FINLAND BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY MODE, 2018-2033 (USD THOUSAND)

TABLE 136 FINLAND BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 137 FINLAND BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 138 REST OF EUROPE BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY PRODUCT, 2018-2033 (USD THOUSAND)

TABLE 139 REST OF EUROPE BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 140 REST OF EUROPE BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY TECHNOLOGY, 2018-2033 (USD THOUSAND)

TABLE 141 REST OF EUROPE BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY MODE, 2018-2033 (USD THOUSAND)

TABLE 142 REST OF EUROPE BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 143 REST OF EUROPE BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

List of Figure

FIGURE 1 EUROPE BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET: SEGMENTATION

FIGURE 2 EUROPE BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET: DATA TRIANGULATION

FIGURE 3 EUROPE BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET: DROC ANALYSIS

FIGURE 4 EUROPE BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET: EUROPE VS REGIONAL MARKET ANALYSIS

FIGURE 5 EUROPE BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET: COMPANY RESEARCH ANALYSIS

FIGURE 6 EUROPE BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET: INTERVIEW DEMOGRAPHICS

FIGURE 7 EUROPE BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET: DBMR MARKET POSITION GRID

FIGURE 8 EUROPE BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET: MARKET END USER COVERAGE GRID

FIGURE 9 EUROPE BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET: VENDOR SHARE ANALYSIS

FIGURE 10 EUROPE BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET: SEGMENTATION

FIGURE 11 EUROPE BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET: EXECUTIVE SUMMARY

FIGURE 12 STRATEGIC DECISIONS

FIGURE 13 NORTH AMEIRCA IS EXPECTED TO DOMINATE THE MARKET AND ASIA-PACIFIC IS EXPECTED TO GROW WITH THE HIGHEST CAGR IN THE EUROPE BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET IN THE FORECAST PERIOD OF 2025 TO 2032

FIGURE 14 EUROPE BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, BY PRODUCT (2024)

FIGURE 15 RISING PREVELANCE OF RARE & CHRONIC DISEASES IS EXPECTED TO DRIVE THE EUROPE BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET, IN THE FORECAST PERIOD OF 2026 TO 2033

FIGURE 16 IMMUNOGLOBULINS SEGMENT IS EXPECTED TO ACCOUNT FOR THE LARGEST SHARE OF THE EUROPE BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET IN THE FORECAST PERIOD OF 2026 & 2033

FIGURE 17 ASIA-PACIFIC IS THE FASTEST-GROWING REGION FOR EUROPE BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET IN THE FORECAST PERIOD OF 2026 TO 2033

FIGURE 18 DRIVERS, RESTRAINTS, OPPORTUNITIES AND CHALLENGES FOR THE EUROPE BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET

FIGURE 19 EUROPE BLOOD PLASMA AND PLASMA DERIVED MEDICINAL PRODUCTS MARKET: BY PRODUCT, 2025

FIGURE 20 EUROPE BLOOD PLASMA AND PLASMA DERIVED MEDICINAL PRODUCTS MARKET: BY PRODUCT, 2026 TO 2033 (USD THOUSAND)

FIGURE 21 EUROPE BLOOD PLASMA AND PLASMA DERIVED MEDICINAL PRODUCTS MARKET: BY PRODUCT, CAGR (2026- 2033)

FIGURE 22 EUROPE BLOOD PLASMA AND PLASMA DERIVED MEDICINAL PRODUCTS MARKET: BY PRODUCT, LIFELINE CURVE

FIGURE 23 EUROPE BLOOD PLASMA AND PLASMA DERIVED MEDICINAL PRODUCTS MARKET: BY APPLICATION, 2025

FIGURE 24 EUROPE BLOOD PLASMA AND PLASMA DERIVED MEDICINAL PRODUCTS MARKET: BY APPLICATION, 2026 TO 2033 (USD THOUSAND)

FIGURE 25 EUROPE BLOOD PLASMA AND PLASMA DERIVED MEDICINAL PRODUCTS MARKET: BY APPLICATION, CAGR (2026- 2033)

FIGURE 26 EUROPE BLOOD PLASMA AND PLASMA DERIVED MEDICINAL PRODUCTS MARKET: BY APPLICATION, LIFELINE CURVE

FIGURE 27 EUROPE BLOOD PLASMA AND PLASMA DERIVED MEDICINAL PRODUCTS MARKET: BY TECHNOLOGY, 2025

FIGURE 28 EUROPE BLOOD PLASMA AND PLASMA DERIVED MEDICINAL PRODUCTS MARKET: BY TECHNOLOGY, 2026 TO 2033 (USD THOUSAND)

FIGURE 29 EUROPE BLOOD PLASMA AND PLASMA DERIVED MEDICINAL PRODUCTS MARKET: BY TECHNOLOGY, CAGR (2026- 2033)

FIGURE 30 EUROPE BLOOD PLASMA AND PLASMA DERIVED MEDICINAL PRODUCTS MARKET: BY TECHNOLOGY, LIFELINE CURVE

FIGURE 31 EUROPE BLOOD PLASMA AND PLASMA DERIVED MEDICINAL PRODUCTS MARKET: BY MODE, 2025

FIGURE 32 EUROPE BLOOD PLASMA AND PLASMA DERIVED MEDICINAL PRODUCTS MARKET: BY MODE, 2026 TO 2033 (USD THOUSAND)

FIGURE 33 EUROPE BLOOD PLASMA AND PLASMA DERIVED MEDICINAL PRODUCTS MARKET: BY MODE, CAGR (2026- 2033)

FIGURE 34 EUROPE BLOOD PLASMA AND PLASMA DERIVED MEDICINAL PRODUCTS MARKET: BY MODE, LIFELINE CURVE

FIGURE 35 EUROPE BLOOD PLASMA AND PLASMA DERIVED MEDICINAL PRODUCTS MARKET: BY END USER, 2025

FIGURE 36 EUROPE BLOOD PLASMA AND PLASMA DERIVED MEDICINAL PRODUCTS MARKET: BY END USER, 2026 TO 2033 (USD THOUSAND)

FIGURE 37 EUROPE BLOOD PLASMA AND PLASMA DERIVED MEDICINAL PRODUCTS MARKET: BY END USER, CAGR (2026- 2033)

FIGURE 38 EUROPE BLOOD PLASMA AND PLASMA DERIVED MEDICINAL PRODUCTS MARKET: BY END USER, LIFELINE CURVE

FIGURE 39 EUROPE BLOOD PLASMA AND PLASMA DERIVED MEDICINAL PRODUCTS MARKET: BY DISTRIBUTION CHANNEL, 2025

FIGURE 40 EUROPE BLOOD PLASMA AND PLASMA DERIVED MEDICINAL PRODUCTS MARKET: BY DISTRIBUTION CHANNEL, 2026 TO 2033 (USD THOUSAND)

FIGURE 41 EUROPE BLOOD PLASMA AND PLASMA DERIVED MEDICINAL PRODUCTS MARKET: BY DISTRIBUTION CHANNEL, CAGR (2026- 2033)

FIGURE 42 EUROPE BLOOD PLASMA AND PLASMA DERIVED MEDICINAL PRODUCTS MARKET: BY DISTRIBUTION CHANNEL, LIFELINE CURVE

FIGURE 43 EUROPE BLOOD PLASMA & PLASMA DERIVED MEDICINAL PRODUCTS MARKET: SNAPSHOT (2025)

FIGURE 44 EUROPE BLOOD PLASMA AND PLASMA DERIVED MEDICINAL PRODUCTS MARKET: COMPANY SHARE 2025 (%)

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.