Europe Circuit Breaker And Fuses Market

Market Size in USD Billion

CAGR :

%

USD

10.14 Billion

USD

16.28 Billion

2025

2033

USD

10.14 Billion

USD

16.28 Billion

2025

2033

| 2026 –2033 | |

| USD 10.14 Billion | |

| USD 16.28 Billion | |

| % | |

|

Circuit Breaker and Fuses Market Size

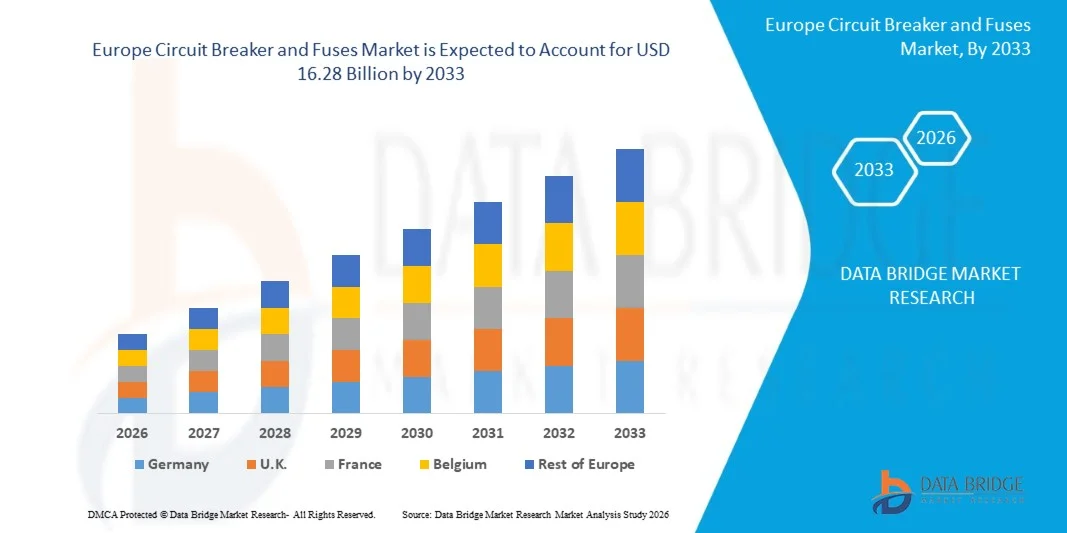

- The Europe circuit breaker and fuses market size was valued at USD 10.14 billion in 2025 and is expected to reach USD 16.28 billion by 2033, at a CAGR of 6.1% during the forecast period

- The market growth is largely fueled by the increasing demand for reliable and safe electrical protection devices across industrial, commercial, and residential sectors, driven by rapid electrification, expansion of power infrastructure, and the adoption of advanced electrical systems

- Furthermore, rising investments in renewable energy projects, smart grids, and industrial automation are accelerating the deployment of circuit breakers and fuses. For instance, companies such as Siemens and Eaton are introducing intelligent breakers and integrated protection solutions that enhance grid reliability and operational efficiency, significantly boosting market growth

Circuit Breaker and Fuses Market Analysis

- Circuit breakers and fuses are electrical protection devices designed to prevent overcurrent, short circuits, and electrical faults in power distribution systems. These devices ensure the safety of equipment, personnel, and infrastructure by interrupting excessive electrical flow and providing controlled protection across low, medium, and high-voltage applications

- Germany dominated the circuit breaker and fuses market in 2025, due to its strong electrical equipment manufacturing base, advanced industrial infrastructure, and high demand for reliable power protection systems across sectors such as automotive, energy, and industrial machinery

- K. is expected to be the fastest growing country in the circuit breaker and fuses market during the forecast period due to rapid modernization of power infrastructure and increasing focus on grid reliability and energy transition initiatives

- High voltage segment dominated the market with a market share of 62.22% in 2025, due to its necessity in industrial and utility applications to protect large electrical equipment from overload and fault conditions. High power fuses are preferred for their rapid response, high interrupting capacity, and long service life, ensuring minimal downtime in critical operations. Their adoption is widespread across heavy industries, power generation plants, and electrical substations

Report Scope and Circuit Breaker and Fuses Market Segmentation

|

Attributes |

Circuit Breaker and Fuses Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe |

|

Key Market Players |

· Eaton (U.S.) · Maxwell Technologies Inc (U.S.) · Alstom (France) · Mitsubishi Electric (Japan) · ABB (Switzerland) · Schneider Electric (France) · General Electric (U.S.) · Siemens (Germany) · Powell Electronics, Inc. (U.S.) · TE Connectivity (Switzerland) · Fuli Electric Co. Ltd (China) · LARSEN & TOUBRO LIMITED (India) · Efacec (Portugal) · HAWKER SIDDELEY SWITCHGEAR (U.K.) · Tavrida Electric (Switzerland) · Legrand (France) · Honeywell International Inc. (U.S.) · CAMSCO ELECTRIC CO., LTD (China) · Pennsylvania Breaker LLC (U.S.) · G&W Electric Company (U.S.) |

|

Market Opportunities |

· Expansion in Renewable Energy Infrastructure · Development of Advanced Protective Relay Technologies |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Circuit Breaker and Fuses Market Trends

“Rising Adoption of Smart and IoT-Enabled Circuit Breakers”

- A significant trend in the circuit breaker and fuses market is the growing adoption of smart and IoT-enabled circuit breakers, driven by the increasing need for real-time monitoring, predictive maintenance, and enhanced electrical safety in residential, commercial, and industrial settings. These advanced devices allow for remote control, energy management, and fault detection, positioning them as essential components for modern electrical infrastructure

- For instance, Schneider Electric and Siemens are deploying smart circuit breakers equipped with IoT sensors and communication modules that enable continuous monitoring of power consumption and system health. These solutions help reduce downtime, improve energy efficiency, and strengthen overall electrical system reliability

- The integration of smart breakers is accelerating the shift toward digitalized energy management systems where automated fault isolation and load balancing capabilities improve operational efficiency. This adoption is particularly strong in large commercial complexes and industrial plants that demand stable power supply and minimal interruptions

- The rising use of renewable energy sources such as solar and wind is driving the need for adaptive protection devices that can handle variable loads and fluctuating power inputs. Circuit breakers and fuses capable of intelligent load management are increasingly favored to ensure grid stability and prevent equipment damage

- Industries focusing on automation and manufacturing are leveraging smart circuit breakers to enhance process safety and reduce energy losses. Intelligent devices support predictive maintenance, helping facility managers anticipate failures and optimize operational performance

- The market is witnessing strong demand for compact and modular circuit protection solutions suitable for smart buildings and data centers. This trend is reinforcing the overall transition toward safer, energy-efficient, and digitally connected electrical networks across global markets

Circuit Breaker and Fuses Market Dynamics

Driver

“Growing Demand for Energy-Efficient and Reliable Electrical Systems”

- The rising focus on energy efficiency and uninterrupted power supply is driving the demand for advanced circuit breakers and fuses capable of precise fault detection and minimal energy loss. These devices play a critical role in reducing operational costs while enhancing safety standards in commercial, industrial, and residential applications

- For instance, ABB offers energy-efficient circuit breakers with integrated monitoring and control functions that help reduce downtime and improve load management in industrial plants. These products enable better energy utilization and support sustainability initiatives

- The expansion of smart grids and microgrid projects is creating a need for reliable protection systems that can manage dynamic power flows and maintain network stability. Circuit breakers with intelligent trip mechanisms and communication interfaces are becoming central to modern grid infrastructure

- The increasing adoption of electric vehicles and charging stations is contributing to higher electricity demand, necessitating protective devices that can handle variable and high-load conditions efficiently. Reliable circuit breakers and fuses ensure safety and prevent system overloads in these applications

- The need for compliance with international electrical safety standards and regulatory requirements continues to reinforce this driver. Manufacturers and facility operators are increasingly prioritizing devices that guarantee system reliability, reduce risks, and support sustainable energy management

Restraint/Challenge

“High Initial Costs and Complex Installation Requirements”

- The circuit breaker and fuses market faces challenges due to the high upfront costs of advanced devices and the technical complexity involved in their installation. Smart and IoT-enabled breakers require specialized integration with existing electrical systems, which can increase project timelines and investment requirements

- For instance, Eaton and Legrand provide intelligent protection systems that demand precise configuration and professional installation to ensure optimal performance. These requirements can pose adoption barriers for smaller businesses and residential projects

- Installing modular and high-capacity breakers involves careful planning, compatibility verification, and adherence to safety regulations, which adds to operational complexity. These factors can limit market penetration in regions with less technical expertise or limited infrastructure support

- The reliance on skilled labor and advanced tools for commissioning and maintenance further increases operational costs and resource dependency. Manufacturers must invest in training programs and support services to facilitate smooth deployment

- The market continues to experience constraints in balancing technological sophistication with affordability. These challenges collectively place pressure on manufacturers and end-users to optimize investment strategies while ensuring reliable, safe, and efficient electrical protection across applications

Circuit Breaker and Fuses Market Scope

The market is segmented on the basis of voltage, breaker product type, fuse product type, arc quenching media type, and application.

- By Voltage

On the basis of voltage, the circuit breaker and fuses market is segmented into 300V–500V, 500V–1000V, 1000V–1500V, 1500V–2000V, 2000V–2500V, 2500V–3000V, and 3000V–3600V. The 500V–1000V segment dominated the largest market revenue share in 2025, driven by its extensive application in industrial and commercial electrical systems where moderate voltage distribution is most common. This voltage range offers a balance of safety, reliability, and cost-effectiveness, making it highly preferred by electrical engineers for medium-scale installations. Furthermore, its widespread compatibility with standard circuit breaker and fuse products enhances adoption across varied sectors, including manufacturing plants and commercial buildings. The availability of standardized components and strong regulatory support for safety also contributes to its dominant position in the market.

The 1500V–2000V segment is anticipated to witness the fastest CAGR from 2026 to 2033, fueled by increasing demand in renewable energy projects, particularly solar and wind power plants, where higher voltage systems are essential for efficient transmission. For instance, companies such as Siemens have introduced high-voltage switchgear and breakers specifically designed for this range, supporting rapid deployment in large-scale energy infrastructure. The adoption is also supported by technological advancements that allow safer and more compact high-voltage solutions. Rising electrification in emerging economies further boosts the demand for higher voltage equipment, positioning this segment as the fastest-growing in the market.

- By Breaker Product Type

On the basis of breaker product type, the market is segmented into low voltage and high voltage breakers. The low voltage segment dominated the largest market revenue share in 2025, driven by its critical role in residential, commercial, and small industrial installations where electrical systems require protection below 1000V. Low voltage breakers are favored due to their cost efficiency, ease of installation, and integration with modern building management and automation systems. Their ability to prevent electrical overloads and short circuits ensures operational safety, making them a first choice for engineers and contractors. Compatibility with a wide range of fuses and protection devices further strengthens their dominance.

The high voltage segment is expected to witness the fastest growth from 2026 to 2033, driven by the increasing deployment of large-scale power transmission and distribution networks. For instance, ABB has been expanding its portfolio of high voltage circuit breakers designed for grid modernization and renewable energy applications. The demand is also propelled by the rising need for reliable and robust solutions in industrial plants and critical infrastructure projects. Innovations in materials and switching mechanisms improve efficiency and safety, accelerating adoption in high-capacity electrical systems.

- By Fuse Product Type

On the basis of fuse product type, the market is segmented into specialty fuse, traction fuse, thermal fuse, high power fuse, telecom fuse, and others. The high power fuse segment dominated the largest market revenue share of 62.22% in 2025, driven by its necessity in industrial and utility applications to protect large electrical equipment from overload and fault conditions. High power fuses are preferred for their rapid response, high interrupting capacity, and long service life, ensuring minimal downtime in critical operations. Their adoption is widespread across heavy industries, power generation plants, and electrical substations. Regulatory standards and safety compliance requirements also enhance market preference for high power fuses.

The traction fuse segment is anticipated to witness the fastest CAGR from 2026 to 2033, fueled by the expanding electrification of railways and metro networks globally. For instance, Schneider Electric has developed specialized traction fuses for railway propulsion systems that ensure high performance under dynamic loads. The segment benefits from increasing urban transportation projects and government initiatives to modernize public transport. Compact design, high durability, and ease of replacement make traction fuses particularly suitable for this rapid-growth segment.

- By Arc Quenching Media Type

On the basis of arc quenching media type, the market is segmented into vacuum circuit breakers, oil circuit breakers, and air circuit breakers. The vacuum circuit breaker segment dominated the largest market revenue share in 2025, driven by its superior reliability, low maintenance needs, and high electrical endurance in medium-voltage applications. Vacuum breakers are widely adopted in industrial and commercial facilities due to their ability to quickly extinguish arcs and ensure operator safety. Their compact design and environmental benefits over oil-based alternatives enhance market preference. Manufacturers also emphasize improved lifecycle performance, making them a preferred solution for modern electrical distribution systems.

The air circuit breaker segment is expected to witness the fastest CAGR from 2026 to 2033, fueled by increasing demand in industrial and power generation applications that require high interrupting capacities and flexible configurations. For instance, Eaton has launched advanced air circuit breakers capable of handling large-scale electrical networks efficiently. Air circuit breakers are gaining popularity due to their robustness, ease of customization, and compatibility with smart monitoring systems. The segment’s growth is also supported by the rising need for electrical safety and automation in industrial plants and critical infrastructure.

- By Application

On the basis of application, the market is segmented into transmission and distribution, construction, industrial, power generation, and consumer electronics. The industrial segment dominated the largest market revenue share in 2025, driven by extensive use of circuit breakers and fuses in manufacturing plants, chemical processing units, and heavy machinery. Industrial applications require robust protection systems to prevent equipment damage and operational downtime, making reliable breakers and fuses indispensable. Compliance with safety regulations and the need for system automation further drive adoption. High demand for maintenance-free and long-lasting solutions reinforces the industrial segment’s market dominance.

The power generation segment is anticipated to witness the fastest CAGR from 2026 to 2033, fueled by increasing investment in renewable and conventional power projects worldwide. For instance, General Electric has supplied advanced high-voltage breakers for solar and hydroelectric plants, supporting safe and efficient power distribution. Rising electricity demand and grid modernization initiatives accelerate the deployment of circuit protection devices in power generation. The segment benefits from technological innovations, enhanced durability, and integration with smart monitoring systems, making it the fastest-growing application in the market.

Circuit Breaker and Fuses Market Regional Analysis

- Germany dominated the circuit breaker and fuses market with the largest revenue share in 2025, driven by its strong electrical equipment manufacturing base, advanced industrial infrastructure, and high demand for reliable power protection systems across sectors such as automotive, energy, and industrial machinery

- The presence of major electrical and engineering companies such as Siemens AG and ABB strengthens Germany’s adoption of advanced circuit protection solutions across power distribution networks, industrial facilities, and renewable energy installations

- Increasing investments in smart grid infrastructure, renewable energy integration, and industrial automation, along with strict regulatory standards for electrical safety and energy efficiency, continue to reinforce Germany’s leading position in the regional market

U.K. Circuit Breaker and Fuses Market Insight

The U.K. is projected to register the fastest CAGR in the Europe circuit breaker and fuses market during the forecast period, supported by rapid modernization of power infrastructure and increasing focus on grid reliability and energy transition initiatives. Growing adoption of renewable energy sources is driving demand for advanced circuit protection systems to ensure grid stability and safety. Leading companies such as Schneider Electric and Eaton Corporation are expanding their product portfolios and strengthening their market presence in the U.K. Increasing deployment of smart grids and digital monitoring solutions is enhancing fault detection and system efficiency. Rising investments in commercial and residential electrification projects are further accelerating market growth. Strong emphasis on energy efficiency and infrastructure resilience positions the U.K. as the fastest-growing market in Europe.

France Circuit Breaker and Fuses Market Insight

France is expected to witness steady growth in the Europe circuit breaker and fuses market during the forecast period, driven by increasing investments in power distribution infrastructure and rising demand for reliable electrical safety solutions across industrial and residential sectors. The country’s focus on expanding renewable energy capacity and upgrading aging electrical networks is accelerating the adoption of advanced circuit protection equipment. Growing demand for efficient and durable electrical components is supporting market expansion. French companies and utilities such as Legrand are enhancing their circuit protection product offerings to meet evolving energy and safety requirements. Increasing adoption of smart electrical systems and automation technologies is improving system performance and operational reliability. Continuous infrastructure development and energy transition initiatives are reinforcing France’s stable growth trajectory in the regional market.

Circuit Breaker and Fuses Market Share

The circuit breaker and fuses industry is primarily led by well-established companies, including:

- Eaton (U.S.)

- Maxwell Technologies Inc (U.S.)

- Alstom (France)

- Mitsubishi Electric (Japan)

- ABB (Switzerland)

- Schneider Electric (France)

- General Electric (U.S.)

- Siemens (Germany)

- Powell Electronics, Inc. (U.S.)

- TE Connectivity (Switzerland)

- Fuli Electric Co. Ltd (China)

- LARSEN & TOUBRO LIMITED (India)

- Efacec (Portugal)

- HAWKER SIDDELEY SWITCHGEAR (U.K.)

- Tavrida Electric (Switzerland)

- Legrand (France)

- Honeywell International Inc. (U.S.)

- CAMSCO ELECTRIC CO., LTD (China)

- Pennsylvania Breaker LLC (U.S.)

- G&W Electric Company (U.S.)

Latest Developments in Europe Circuit Breaker and Fuses Market

- In March 2026, Mersen introduced its latest generation of ProGrid NH fuse‑switch disconnectors and Surge‑Trap K surge protection systems, enhancing protection and digital monitoring for low‑voltage industrial and commercial networks. These devices improve overcurrent and surge protection performance while enabling smart diagnostics and real‑time monitoring, strengthening grid reliability and supporting the trend toward digitalization of electrical infrastructure. This development accelerates adoption of intelligent protection solutions in industrial facilities and smart grids, addressing growing demand for resilient and connected power distribution

- In October 2024, Littelfuse expanded its circuit protection offerings by launching the 871 Series high‑current SMD fuses with 150 A and 200 A ratings, traditionally achievable only with larger through‑hole packages. By consolidating high‑power protection into compact surface‑mount components, this innovation helps designers significantly reduce PCB space and supports high‑performance AI computing servers and data centers. The 871 Series enhances the market’s ability to meet demanding power requirements, particularly in data‑intensive applications where space, efficiency, and reliability are critical

- In September 2024, Eaton announced a strategic collaboration with Tesla to integrate its smart circuit breaker technology with Tesla Powerwall systems, aiming to enhance residential energy management via intelligent load control. This partnership enables automated load management to extend backup power duration during outages by controlling heavy loads, reflecting increased convergence of traditional protection hardware with smart energy storage and home automation technologies. The initiative underlines market trends toward integrated home energy systems and energy resilience

- In August 2024, Hitachi Energy advanced high‑voltage circuit protection by launching an SF6‑free high‑voltage circuit breaker rated at 550 kV, part of its EconiQ portfolio. By eliminating the use of the potent greenhouse gas SF6, this product supports utilities in decarbonizing power grids while maintaining reliable performance in critical transmission infrastructure. The innovation aligns with industry sustainability priorities and regulatory pressure to reduce environmental impact, boosting adoption in eco‑efficient grid modernization

- In June 2024, Siemens achieved a sustainability milestone by transitioning production of the SIRIUS 3RV2 circuit breaker to use biomass‑balanced plastics, reducing carbon emissions by approximately 270 tons annually. This shift highlights a broader market movement toward lowering embodied carbon in electrical hardware while maintaining performance and safety standards in industrial control systems. It reinforces manufacturer efforts to integrate sustainability into product manufacturing and appeal to eco‑conscious industrial buyers

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Europe Circuit Breaker And Fuses Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Europe Circuit Breaker And Fuses Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Europe Circuit Breaker And Fuses Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.